Since the 1970s, financial markets have seen brokers develop to continuously meet the growing needs of market participants.

In traditional markets, prime brokers offer liquidity provision, trading execution, custody, clearing, settlement, capital introduction, trading on margin and derivatives services, and more, effectively providing a one-stop-shop of financial services for institutional clients.

However, many brokers rely on services provided from “core brokers” (i.e., brokers of brokers), which allows them to focus on value-added services through marketing, client acquisition strategy, dedicated customer support, and liquidity & settlement services.

Similarly, the emerging crypto industry has seen the development of two categories: prime brokers and broker service providers (i.e., “core brokers”). On the other hand, fintech and FX brokers have displayed a greater appetite to be more involved in the space, following initial attempts to offer CFD crypto trading to clients.

Institutional investors show a persistent demand for trading, compliance, and liquidity services from prime brokers, even though the cryptocurrency market typically offers easier access to trading venues than conventional markets.

Due to regulatory restrictions, traditional brokers have not opened up spot crypto services (only derivatives and other instruments). As a result, crypto exchanges have established themselves as the center of the emerging crypto brokerage industry.

Consequently, large crypto exchanges have launched prime brokerage services to provide institutional investors with custody, block trading, aggregation trading, and other services.

Meanwhile, crypto broker service providers have empowered brokers to offer services to institutional participants from both crypto and traditional brokerage environments, promoting the lateral expansion of the industry through non-crypto companies offering dedicated crypto trading to their users, which is expected to further lower entry barriers in the industry.

As institutional trading has become widely spread in the crypto industry, brokers have become a fundamental block of the services provided for institutional clients. The crypto brokerage industry has seen rapid growth and development, constantly matching the unique demands of large market participants.

This report uses case studies to analyze the brokerage industry in the crypto space and evaluate its similarities with the traditional financial broker industry, before discussing some of the trends regarding the outlook of crypto brokerage.

1. Overview of the brokerage industry

1.1 How does the traditional brokerage industry work?

The traditional financial market has a fine-grained labor division, with brokers providing investors with various trading services, which significantly promotes market development. As of now, there are more than 3,600 security brokers in the US alone, which are estimated to realize a market revenue of $300 billion by the end of 2023.

There are three primary participants in the traditional equity brokerage industry: exchanges, investors (including institutional and retail), and security brokers.

Figure 1 - Organization of the equity brokerage industry

A stock exchange is a facility where investors can buy and sell securities. In the traditional equity markets, only qualified members have access to trade on exchange venues. Its main functions include:

Providing investors with trading access and infrastructure.

Organizing and supervising trading activities, including maintaining orders.

In traditional markets, investors (both institutional and retail) often encounter the following limitations:

Most investors cannot trade directly on exchanges for regulatory reasons.

They have high requirements for value-added services.

Security brokers are the bridge between exchanges and investors. For them, their main functions are:

Earn commissions when entrusted by investors to buy and sell securities.

Provide investors with consulting services, such as investment advice and asset management services.

Provide financial instruments, such as leveraged products and securities lending.

There are various brokers to fulfill the multiple needs of different participants in the financial market. In general, brokers can be classified with respect to numerous categories, such as the object of trading, the business model, and the partnership model. Large institutions turned to have multiple types of brokerage services with segmentations that might be tailored to their own business lines.

(1) Divided by the object of trading

Security brokers advise customers who wish to conduct financial investments. Securities brokers arrange for the purchase or sale of stocks, bonds, and other securities on their customers' behalf.

Foreign exchange (or Forex) brokers are firms that provide traders with access to a platform that allows them to buy and sell foreign currencies.

Futures brokers are traders that specialize in dealing with commodities futures contracts.

Crypto brokers: are firms (or individuals) that act as intermediaries between the cryptocurrency markets to facilitate the buying and selling of cryptocurrencies.

(2) Divided by business model

Discount brokers charge users lower commission for trading execution and usually don’t provide any consulting services. Examples include Robinhood and E-trade.

Full-service brokers focus more on providing value-added services (such as wealth management) and charge higher fees. In the traditional financial industry, popular companies include Merrill Lynch, Morgan Stanley, and UBS.

(3) Divided by partnership mode

Introducing brokers introduce clients to brokers who execute trading and settlement to earn commissions. Such brokers usually pay more attention to marketing.

Non-disclosed brokers have wholly-owned brands and products, which are built on the underlying infrastructures backed by larger brokers. Compared to introducing brokers, non-disclosed brokers usually provide a complete set of solutions for their clients.

Although there are many categories of brokers, they all attempt to build a bridge between exchanges and users. Brokers are in never-ending competition regarding the integration of business-side resources to foster business/client-side relationships or the growing number of direct business/client-side relationships.

1.2 Typical traditional financial brokers: the case of prime brokers

Prime brokerage first appeared in the late 1970s. Before then, trading, settlement, and custody were performed by separate entities. Institutional customers often appointed multiple security providers to work together to carry out these functions. Hence, the large volume of trading data was putting a heavy burden on fund managers.

Centralizing functions such as trading, settlement, and custody turned out to be the initial motivation behind the prime broker industry's birth. Since then, prime brokerage companies have incorporated a lot of functions to provide a one-stop financial shop to institutional investors.

In conventional financial markets, prime brokerage companies provide their clients with services such as:

Trading, custody, settlement, valuation, risk control, and operations.

Portfolio reports/business reports.

Design and implementation of derivatives such as margin, stock buybacks.

Trading on margin.

Cash management.

Personalized tech support.

Other value-added services (including capital introduction, risk management consulting, and more).

As a result, prime brokers mainly acquire income from:

Trading commissions.

Custody/settlement fees.

Margin trading and other leveraged trading spreads.

Fees related to asset management and consulting services.

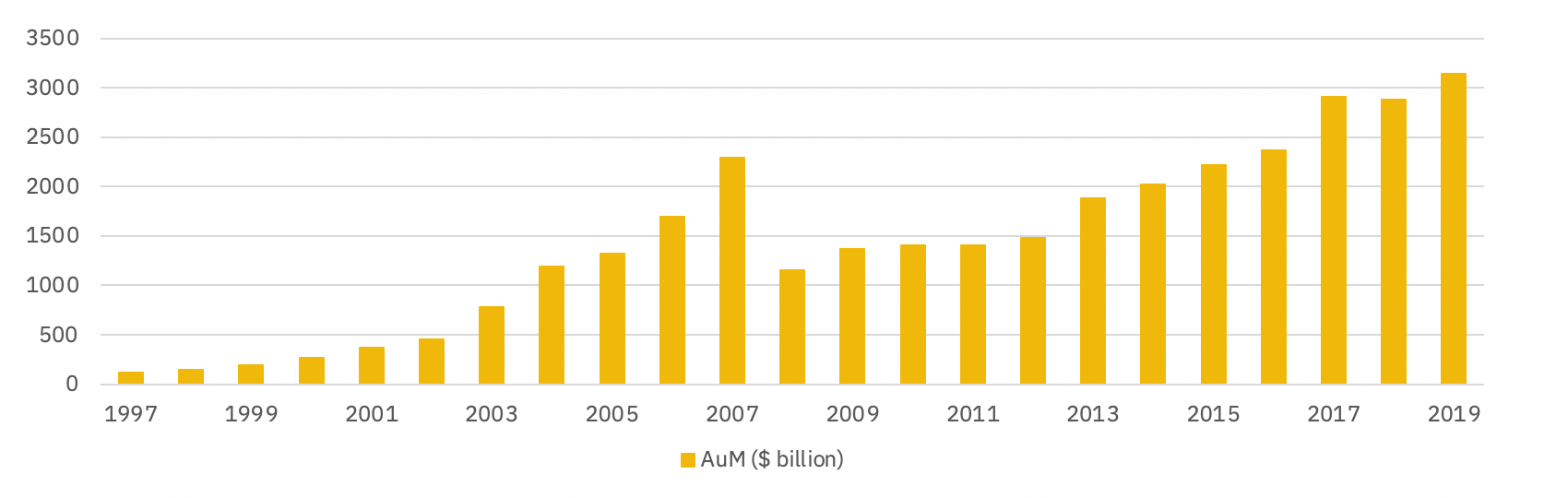

Funds, especially hedge funds, rely on prime brokers. Although settlement services make up only a small part of securities brokers' income, a decent amount of prime brokers' income is derived from providing services to hedge funds that are based on settlement, such as margin trading and more.

Chart 1 - Asset under management (AuM) of the global hedge fund management industry from 1997 to 2019 ($ billion)

Source: Statista.

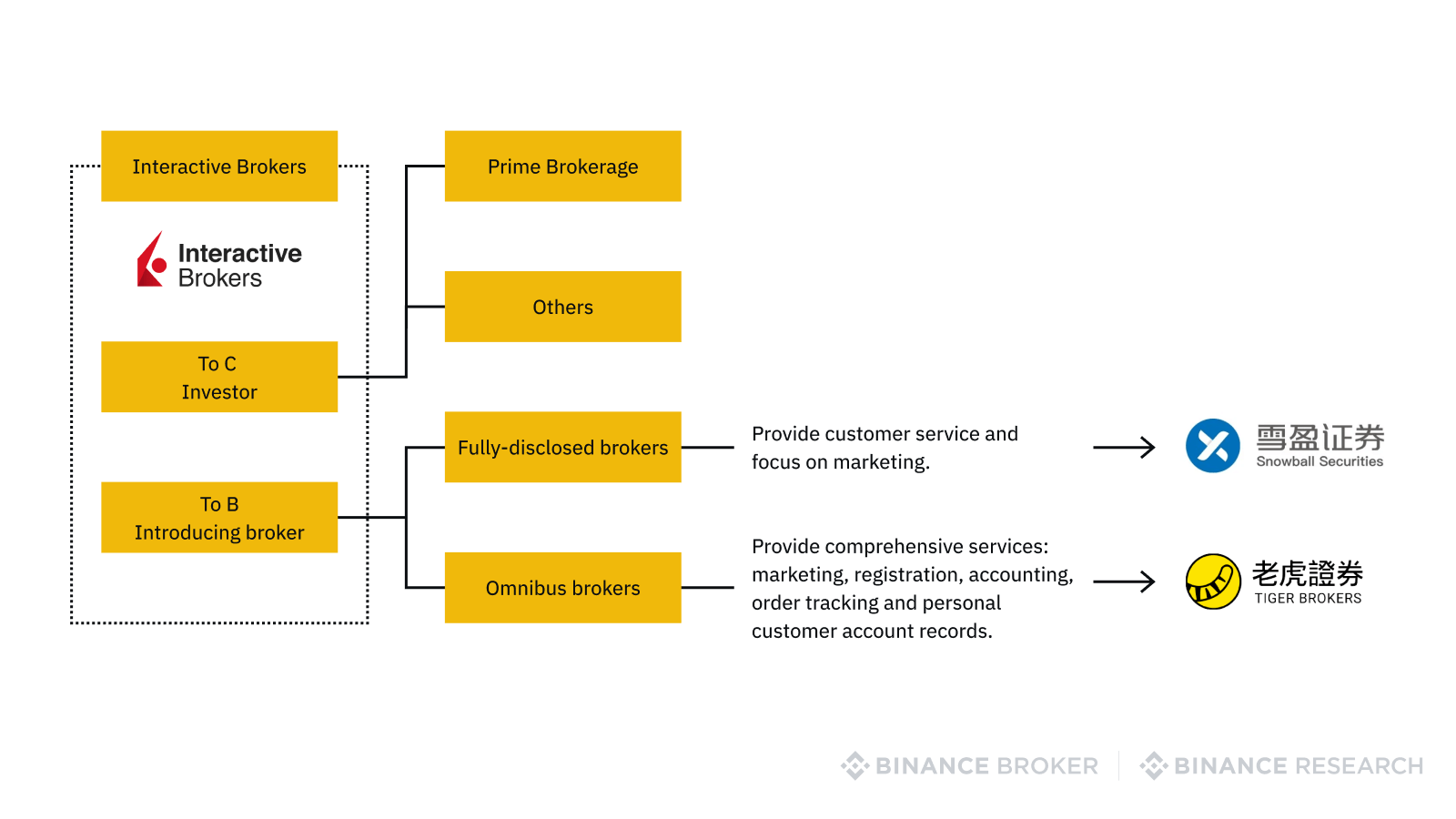

In addition to the brokerage business, companies like Interactive Brokers also provide other brokers with underlying channel services for institutions and retail users.

One example of how such a tiered configuration of brokers and broker services look like is displayed below.

Figure 2 - Interactive Brokers organization with local brokers

“Interactive Brokers” is one of the largest online security brokers in the US. It provides underlying channel services for online securities, acting as a one-stop service that includes trading, settlement, and others, for fully disclosed brokers and omnibus brokers1.

“Tiger Brokers”, an omnibus broker, catering to Chinese investors wishing to get exposure to overseas securities like US equities. Interactive Brokers provides Tiger Brokers with trading, settlement, and other underlying services for US stock trading. Hence, Tiger Brokers focuses primarily on user acquisition through aggressive marketing operations and dedicated customer support.

“Snowball Securities” is a fully-disclosed broker for equities, built to provide investors access to global securities listed on major stock exchanges (e.g., Hong Kong (SEHK), New York Stock Exchange (NYSE), NASDAQ).

1.3 What is crypto brokerage?

1.3.1 The needs for crypto brokerage

The crypto brokerage industry's state is rapidly changing, especially so because of the current influx of forex brokers and fintech companies into the crypto world. Initially dominated by a retail presence, the crypto industry has been snowballing for the past few years.

Pioneers in the crypto brokerage industry have gradually built an underlying framework that has become increasingly similar to that of the traditional financial sector.

Initially, Forex brokers entered the market by offering CFD products, while Fintech companies penetrated the market by setting up fiat channels.

Figure 3 - Traditional and fintech companies offering crypto products

In the shaping of the crypto brokerage space, the environment has been naturally evolving into two primary segments:

Prime brokers with aggregated liquidity for institutional clients, such as Tagomi. They service sophisticated investors and institutional clients.

Large exchanges are taking the role of brokers, and they also provide underlying liquidity to other brokers, such as Binance and Paxos (through itBit). They attempt to connect the liquidity for outside market participants, hence effectively expanding beyond their scope to ultimately service a larger user base.

Unlike the traditional financial sector, the crypto industry does not have the concept of “trading seats”, since market participants' requirements are minimal compared to conventional financial markets.

Yet, brokers remain relevant in regards to multiple elements:

Brokers are conducive to integrating market resources and play a considerable role for small and medium players in the industry due to high entry barriers at bigger venues.

The resource integration capabilities of top players are gradually increasing with the changes in market demand.

Figure 4 - Organization between crypto exchanges, brokers, and investors

Some of the benefits include lower costs, reduced operational risks, and the ability to specialize on a restricted sub-segment of functions.

(1) Lower costs

Internal and external market makers: by using brokerage service, market participants do not need to pay for internal and external market makers.

Build matching/trading engines: participants can save money on building matching/trading engines, which are very time resource consuming.

Wallet system infrastructure: it is not required to build and maintain a complicated wallet system for crypto assets.

(2) Reduced operational risks

Underlying system for trading: reduce operational risks from the underlying trading system.

Risk control system: from the perspective of end-users, it reduces technical risk by using mature and robust risk control systems from brokerage service providers.

Product design: business risk is often lowered because market participants rely directly on designed products from third-party vendors.

(3) Increased innovative and high value-added services

Value-added services: crypto brokers could provide value-added services for clients like trading strategies/trading bots/asset management, etc.

Product innovation: since a third party handles heavy technical parts, brokers can invest more time in product innovation, opening up new channels, and acquisition of new clients. For instance, brokers need not actively follow network upgrades (e.g., soft forks, etc.).

Traditional financial exchanges could not open up brokerage business because of regulatory restrictions. In reaction, cryptocurrency exchanges have evolved by setting up dedicated brokerage activities.

The chart below shows that normal exchanges are already doing a lot of work as broker service providers and more and more exchanges have begun to step foot in the prime broker area.

Figure 5 - Functions of prime brokers and broker service providers

1.3.2 Prime brokerage in the crypto industry

The need for trading and financial services of institutional investors is the driving force behind crypto prime brokerages. Some crypto exchanges, wallets, and trading terminals have begun prime brokerage businesses. For instance, Coinbase offers prime brokerage starting from custody, whereas Huobi and Bequant offer prime brokerage with OTC block trading. The core purpose of a prime broker is to serve institutional investors.

Client needs: liquidity, financial instruments (such as margin, lending, etc.), settlement, and compliance.

Product services: such as custody, trading, financial services, etc:

Block trading and other professional trading instruments. Brokers combine liquidity from multiple exchanges for investors to benefit from optimal liquidity leading to improved trading execution. Examples include Coinbase and Huobi.

Financial services - margin, lending, and other services to institutional investors.

Table 1 - Overview of major prime brokers in the crypto industry

Prime brokers | Date established | Product |

|---|---|---|

Coinbase | Early 2019 | Custody, Trading (Tagomi acquisition), Lending |

BitGo Prime | May 2020 | Custody, Lending, Trading (Lumina acquisition) |

Genesis Prime | May 2020 | Trading (soon to offer OTC options), Custody (Vo1t acquisition), Lending |

Bequant | May 2020 | Trading (OTC block and aggregate trading), Custody |

Huobi Brokerage | July 2020 | OTC block trading |

Figure 6 - Relationship between prime brokerage and institutional investors

While prime brokers focus on institutional participants, broker service providers ultimately target individual investors through liquidity services provided to intermediate companies.

As discussed before, crypto brokers can be split into these two categories:

Crypto prime brokers: companies like Coinbase and Paxos are geared towards providing compliant crypto trading services to fintech companies, banks, and similar institutions.

Broker service providers: those like Binance Brokerage that provide crypto services like liquidity provision and custodianship to other brokers servicing individual investors.

For the purpose of this report, this terminology was introduced to distinguish participants in the crypto brokerage market. Conversely, in traditional markets, brokers usually provide services for retail and institutional clients at the same time catering to a wide range of needs, ultimately creating a diversified income stream.

Since crypto markets have not fully matured, this breakdown helps in the classification of those brokers who only provide services for institutional clients in the crypto industry, and the brokers offering services ultimately aimed at other brokers, catering to retail traders. As the industry and business grow, changes are bound to take place, making this breakdown less relevant.

Figure 7 - Comparison of companies between traditional and crypto brokerage industries

2. Case studies in the crypto brokerage industry

2.1 Coinbase (prime broker + broker service provider)

Coinbase provides both prime broker services as well as broker service solutions.

2.1.1 Coinbase as a prime broker (Tagomi)

Tagomi, acquired by Coinbase in May 2020, is a prime broker that provides institutional clients with a full range of services, including aggregated trading (from Coinbase, Bittrex, Kraken, Gemini, Bitstamp, Binance, and other large liquidity venues), custody, margin, lending, and staking.

Target clients: institutional customers (e.g., hedge funds, private equity funds, crypto funds, quant funds).

Strengths: BitLicense, insured custodianship services.

Services:

Custody services: Coinbase Custody.

Lending: margin trading (on Coinbase Pro), etc.

Trading: aggregated trading and professional trading instruments.

Example of clients: Paradigm, Pantera, Bitwise, and Multicoin Capital.

Figure 8 - Coinbase as a prime broker

2.1.2 Coinbase as a broker service provider

Coinbase has provided broker service solutions since 2019.

Target clients: fintech companies, brokers, banks.

Strengths: BitLicense, insured custodianship services.

Services: broker service solutions.

Example of clients:

SoFi: US online personal financial company that provides loans, mortgages, stocks, and crypto investment services to 1 million users. SoFi has offered crypto trading in partnership with Coinbase since September 2019. It received the BitLicense in December 2019.

Figure 9 - Coinbase as a broker service provider

2.2 Paxos as a broker service provider

Paxos Brokerage, launched in July 2020, aims to provide brokers with a set of API-based, compliant crypto trading and custody solutions. Its liquidity relies on Paxos’ own exchange itBit (with a base rate of 0.35%).

Target clients: payment companies, wealth management companies, banks, or other fintech companies.

Strengths: BitLicense, API integration, custody services.

Services: broker service provider for institutional clients.

Examples of clients:

Revolut: a fintech company with 12 million users and a valuation of $5 billion USD headquartered in London. Revolut currently provides payments, forex, stock trading, digital currency trading, and other services.

PayPal (unofficially public2).

2.3 Binance as a broker service provider

Binance Brokerage aims to become the liquidity provider for the crypto industry.

Clients: exchanges, wallets, trading bots, market data platforms, asset management platforms, etc.

Strengths:

Deep liquidity from exchange operations.

A variety of trading products: such as derivatives, lending or margin.

Crypto-native services: such as staking and on-chain services.

Services:

Core trading types: spot trading, futures trading, fiat trading.

Upstream/downstream integration: lending, financial management, mining, payments.

Support for a wide range of assets for spot and futures trading.

600+ spot trading pairs: many unique trading pairs and large altcoin availability.

30+ futures trading pairs, including unique altcoin derivatives assets, with settlement in both base and quote assets.

Asset custody system: asset custodianship is handled at the exchange service level, thus, offering services for any of the supported assets by Binance.com.

Trade settlement system: trades are settled at the exchange level, with settlement directly into the wallet.

Figure 10 - Binance Brokerage as a broker service provider

Through the use of the Binance’s broker API, it offers integration for both back-end and front-end infrastructure for clients.

3. What is the industry outlook for crypto brokerage?

As the crypto industry continues to develop, the gap between the conventional financial market and the crypto market will continue to narrow.

With a growing base of retail and institutional users, an expanding market and the emergence of increasingly specialized functions, a virtuous cycle of growth started.

Brokers have become the equivalent of "supernodes" that connect users looking to trade a wide variety of assets.

In that regards, we have identified three main trends in regards to:

Traditional brokers offering crypto services.

Diversification of existing crypto prime broker activities.

Compliance requirements for broker service providers.

Trend 1 - Traditional brokers offering crypto services

Top prime brokers are expected to shift their focus to wealth management as they develop toward a full-service brokerage model.

Traditional financial companies have been entering the cryptocurrency & digital asset market by offering spot trading services to their existing client base (mostly non-crypto users).

Meanwhile, the transition from discount broker to comprehensive financial services provider could draw customers through technological & product innovation, leading to greater customer segmentation.

Trend 2 - Diversification of crypto prime broker activities

Companies offering prime brokerage have been exploring high value-added services.

In 2020, Coinbase (for its prime broker activity), BitGo, and other competitors began to dabble in prime brokerage but currently remains in an exploratory stage.

In the traditional financial industry, prime brokers have established a diversified income structure owing to a wider variety of profit-generating business lines. Conversely, crypto prime brokers have a very concentrated income structure (highly dependent on a single asset class). Still, they are expected to diversify in the future, as the differences between the conventional and crypto markets are declining.

Crypto prime brokers have started providing services such as custody services to explore new ways to meet the demand of institutional traders and other financial companies (e.g., mutual funds, hedge funds).

Trend 3 - Compliance requirements for broker service providers

While more fintech companies, traditional brokers, and other banking institutions look to offer crypto services for their clients, the subject of compliance remains crucial.

Fintech companies have increasingly shown interest in cryptocurrencies and other digital assets. Once compliance requirements are better formalized and addressed, fintech companies could help to expand the horizons of the crypto industry.

Despite being compliant in multiple jurisdictions, brokers' crypto CFD products (like Robinhood and eToro) are imperfect for reasons such as slippage, high spreads, and pricing complexity.

Brokerage service providers (e.g., Binance Brokerage) are attempting to establish a more compliant environment for clients by leveraging liquidity from crypto exchanges to partner brokers and clients conventional and crypto markets, to foster the expansion of the crypto industry as a whole.

Binance Broker offers brokerage services for a wide range of clients. To learn more about its program: send a mail at broker@binance.com or bingyao.song@binance.com.