Crypto has been at the epicenter of discussions regarding the Russia-Ukraine conflict;

Exchange data for Russian and Ukrainian users shows increases in activity in the last few weeks as the local populace respond to the realities of sanctions and military conflict. Despite this, the volumes are not materially significant and indicate the nascent stage of crypto adoption that both nations are currently in;

It is clear that crypto cannot be used by Russians to evade sanctions in any meaningful way, both from a liquidity and anonymity point of view, data supports this;

Directional correlation between crypto and equities and internally within crypto markets is hitting recent highs, however, crypto is notably outperforming. The contrast that commodity markets are displaying versus equities points towards a recalibration of correlation expectations and supports an argument for crypto outperformance;

While the digital gold hypothesis appeared to break down in the initial days of the conflict, crypto has bounced back strongly in following weeks, while gold price remains muted. The impacts of the crisis on the already high global inflation levels will likely support the Bitcoin inflation hedge thesis going forward;

Monetary weaponisation through reserve asset freezing, the recent actions of the Canadian government and the shift in the globalization narrative combine together to support a bullish view of crypto in the medium term, with the crisis further driving mass adoption and hastening the move towards a more digital world.

The Russia-Ukraine conflict represents the first major militarized European conflict in decades. The crisis is very much in the process of unfolding and the fog of war is thick in both the media and on the ground. With the extensive usage of international sanctions on Russia and the digitally inclined population of Ukraine, crypto has been at the epicenter of the discussions on the crisis. On one hand, Ukraine has reportedly seen upwards of $70m1 in crypto donations, while on the other hand, there is regulatory discussion of how Russians may use it to evade sanctions and calls for major exchanges to ban local users. It can be said that, in many ways, this might be the first ever crypto war.

In this report, we analyze what has happened so far, how it compares to previous market moving events, how the situation has impacted crypto in the short term and what we expect the effects will be in a longer time horizon.

What has happened so far?

To start our analysis, we look at how the situation has panned out so far from a capital flow perspective. A preliminary analysis of trading flows shows that weekly crypto asset flows demonstrated a notable increase in inflows in the weeks surrounding the start of the crisis on February 24th. Comparing this to global equity flows, we can see a clear divergence emerge, with equities seeing net outflows in the weeks that crypto assets saw inflows. Perhaps a pre-emptive signal of some market participants rotating out of equities and into harder crypto assets. The fact that they were seeing outflows prior to the crisis, while equities were seeing inflows and that we saw this pattern reverse, as shown below, is indicative of crypto’s role as a hedge to traditional market securities being recognised and exercised upon.

Figure 1 - Weekly Crypto Asset Flows (US$m)

Source: CoinShares2

Figure 2 - Fund flows: Global equities, bonds and money markets

Source: Refinitiv Lipper data3

Delving deeper into flows of the individual nations, using data from major exchanges for Russian and Ukrainian users, while we do observe somewhat of an increase in net fiat inflows and activity, the numbers are not particularly high. What does this reflect? For Russians, this can be assumed to be the populace selling rubles in exchange of crypto assets in order to preserve their wealth and respond to the capital controls that the Bank of Russia has put in place. Let’s not forget that the ruble is down by approximately 11% to the U.S. Dollar since the start of the crisis and at one point was down 96% as incoming sanctions news combined to deliver a near ‘rug pull’ of the currency. Crypto assets might have been and still be the only viable way to preserve wealth for some individuals in the country. Ukrainians also share the concerns regarding the preservation of wealth, albeit, not from a currency devaluation perspective, but rather from the viewpoint of those who may have to swiftly evacuate their homes without any time to liquidate their assets. Outside this, UAH pairs on crypto exchanges will also represent some liquidation of the reported $70m of crypto donations that the country has received as support. The fact that levels of activity are not materially high indicate to us that crypto adoption is still in its nascent stages in both nations and is far from the preferred method of transacting with one another - at least at this early stage in the crisis.

Another aspect to consider is the narrative around how Russians may seek to use crypto as a means of evading sanctions. We can start with dismissing the very notion that any such evasion could happen on a large scale. A simple way we can illustrate this is by understanding that Russia is reported to have lost access to at least half, and upto all, of its $630bn in central bank reserves. With the current global market capitalisation of all crypto only ~$2.1tn, it is clear that the crypto markets cannot be used to move or replace any meaningful amount of those frozen reserves. This rules out any large-scale evasion on a national scale.

On a more granular level, individual actors could theoretically use crypto to move funds and possibly attempt to evade personal sanctions. However, if this was to be the case, given that blockchains are traceable by nature, we can consider a number of indicators that could help us probe deeper. Firstly, we can consider the fact that crypto wallets themselves can provide a level of anonymity, particularly when combined with the use of mixer protocols like Tornado cash. To this end, we would reference a recent report4 by crypto data provider, Chanalysis, who have kept a close watch on known Russian whale wallets and activity on high-risk services like Tornado cash and smaller, riskier exchanges like Garantex and Bitzlato. Their report confirms no meaningful spikes in inflows, outflows or unusual activities for all of the various channels they monitor. This is perfectly in line with the testimonies that co-founder Jonathan Levin, alongside a number of other experts, delivered to the U.S. Senate in a recent hearing5 on the subject of digital assets in illicit finance.

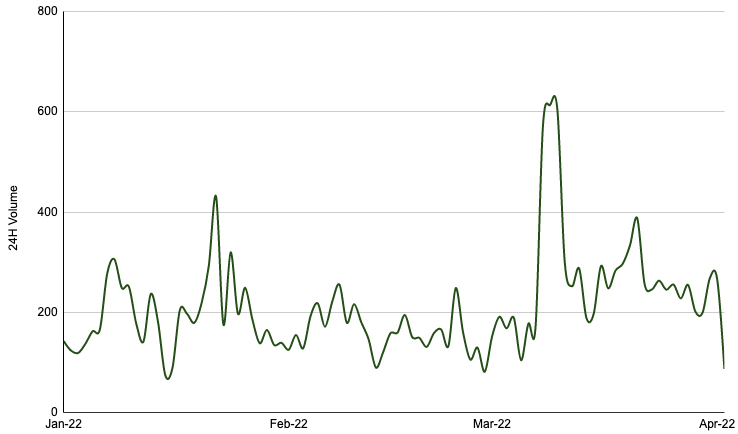

Furthermore, we can consider a brief analysis of specialized privacy coins, which individuals may seek to use to their advantage to hide transactions. However, as you can see below, data clearly shows no meaningful increase in transaction levels of the top privacy coins, while Russian activity in general has seen a meaningful surge (the slight spike in early March in privacy tokens was largely attributed to then-upcoming crypto executive order from President Biden). In addition, the liquidity that it would take to aid any material evasion of sanctions is simply not available on decentralized platforms. Add to this the fact that any fiat off-ramps, which only exist via centralized intermediaries, will be unable to be used without getting tracked, and it is clear that it is highly improbable and largely impossible for the Russian administration and population to be utilizing crypto to evade sanctions.

Figure 3 - Privacy Token Volumes (US$m)

Source: CoinMarketCap6

*tokens used: XMR, ZEC, ZEN, XVG, FIRO, BEAM, PIVX, NAV, DASH across the top six exchanges in the market

How does this compare to previous periods of market turbulence?

A recent case study we can consider for how global markets have reacted to this news is the beginning of the Covid-19 pandemic in early 2020. At that time, we saw a 44% fall in total crypto market capitalisation in the space of 10 days (in hindsight the best buying opportunity in recent years), followed by a sharp rebound and rapid escalation, breaking past the previous local high within two months. In equity markets, using the MSCI World Index7 as a proxy for global equities, there was a 32% drop through March. This took over five months to get back to the previous level and then went on to spend all of 2021 in an ascending trend. Comparing this to the current market dip, crypto saw a 24% fall from its February highs, while global equities fell ~10%. However, since then, the crypto markets saw a sharp rebound, recovering within the month, whereas global equities continued to trade rather mixed. Looking more specifically, Bitcoin bottomed out around ~11% lower after the start of the crisis, while the MSCI World Index went ~5% lower. However, since then Bitcoin has recovered all losses and trades in the context of 35% higher, in and around $47,000, whereas the MSCI World Index is up less than 8%.

Figure 4 - Bitcoin vs Equities

Source: Binance Research

When looking at these patterns from a correlation perspective, we can see that directionally, crypto does indeed appear to trade akin to a risk asset and respond to equity movements. It was recently reported8 that the Bitcoin to S&P500 90-day correlation hit its highest level since October 2020. It is worth noting that while the 90-day correlation paints this picture, shorter duration metrics look very different as crypto markets tend to bounce back and outperform at a much faster rate than traditional equity markets, as one would expect. Another type of correlation we can consider is that of Bitcoin’s to Ether and to the wider crypto market. Data shows that the 90–day correlation for both of these figures is approaching all-time highs, similar to the bear markets of 2018 and 2019 and the Covid-19 sell-off of 2020. The interesting point is that in previous cycles, this high crypto correlation was caused by sudden sharp selloffs, whereas this period of high correlation has coincided with a steadier growth pattern, suggesting that diversification of Bitcoin holdings through altcoin exposure is not a straightforward process. Furthermore, the fact that both of these correlations tend to peak out near periods of market stress can be attributed to a lower desire to rotate into altcoins and thus a prevailing risk-averse market environment.

The recalibration of the correlations that market participants are expecting is already evident in the commodity market, which has seen a divergence from equities, in what is very different to last year for example. As we can see below, 2021 saw both markets grow, albeit at slightly different paces. However, as tensions flared in Eastern Europe, we saw commodities shoot up in price in a sharp divergence to global equities, which nosedived. While the drivers for this move are largely supply-side driven, given both nations’ energy and agricultural production capabilities, the idea of changing correlations does lend itself well to forming an argument towards crypto outperformance in the medium term. Similar to how commodity markets are reacting to this shift in the globalization narrative, there is a compelling case for crypto markets to do the same, given all that a permissionless and trustless system can provide in comparison to the clearly censorable and permissioned fiat system many of us are observing up close for the first time.

Figure 5 - Commodities vs Equities (% return since last year)

Source: Binance Research

What does this mean in the short term?

In addressing the immediate effects, we can consider what this recent performance means for the classic Bitcoin as digital gold thesis. As we discussed above, as the conflict started to take shape, Bitcoin, alongside most other risk assets, saw a fall in their valuations. In contrast, gold saw a ~3% jump and went on to see a local peak of $2,044/oz, up ~8% from the start of the crisis. Taking this at face value, it would appear that some very vocal gold maxi’s have finally been vindicated, however, what has happened immediately after the initial shock? As we can see, Bitcoin has climbed with strength and is now up around ~35% from its local bottom, while gold seems to have adjusted downwards and appears to be trading sideways at this early stage. We could argue that this ensuing price movement is indicative of the reinforced position of Bitcoin as digital gold, but perhaps it is better to consider that, whether digital gold or not, Bitcoin and crypto assets are part of the safe haven conversation. The battle isn’t against gold because the drawbacks of holding your wealth in a physical metal versus an online crypto wallet are obvious and clear. Simply the fact that crypto assets are in the bucket of hard assets and the contrast between them and fiat currency is becoming more clear, in itself, justifies Bitcoin’s position as digital gold. As the year goes on and we can look at more data, perhaps Bitcoin and crypto will continue to outperform physical gold and we can settle that conversation once and for all.

Figure 6 - Bitcoin vs Gold (% return since the start of the crisis)

Source: Binance Research

Another narrative we can look at evaluating is the role of Bitcoin as an inflation hedge. Inflation has been coming in hot across most developed nations for a few months now, while Bitcoin and broader crypto markets have had a relatively bearish first quarter, at least in terms of price action. Is this to say that Bitcoin isn’t the inflation hedge that everyone had been talking about in the absence of actual inflation? Yes and no. In the short term, the price movements do not necessarily correspond to what could be considered an effective hedge. However, we firmly believe that you have to extend the time horizon to properly evaluate this role of Bitcoin, and crypto at large. Examining US monetary policy, it has been clear to many, including Fed officials, that, for want of a better term, the Fed fell asleep at the wheel. US CPI had been breaking multi-decade records for months prior to the start of the Russia-Ukraine crisis with the infamous ‘transitory’ inflation narrative running rampant, ascribing the pent-up demand from two years of lockdowns as the driver behind inflation. Only a few months after Fed Chair Jerome Powell formally dropped the term ‘transitory’ did we see the crisis emerge and the sudden spike in energy and commodity prices. This supply-driven inflation is yet to officially feed into most developed nations’ inflation readings and is what drives our view that the Fed, alongside many of its peers, might be too late in controlling inflation. As and when this additional source of price movement starts showing up in CPI readings, the Fed will be in an even more desperate position, where stagflation looks to be the most likely outcome. It is in this environment that Bitcoin’s role as an inflation hedge will be truly put to the test and, in our view, confirm it.

Figure 7 - G7 CPI (annual growth rate, %)9

What about the medium term?

The weaponization of the monetary system that we saw unfold across the globe as countries banded together to freeze Russia’s central bank reserves will undoubtedly have far-reaching consequences on the global financial system at large. No longer are a country’s central bank reserves something they can rely upon to the extent they could have in the past, and a re-pricing of every nations’ foreign reserve assets has been necessitated. In a financial sense, the discount rate with which we have been pricing sovereign savings has increased all across the world, and especially so for nations that might not be friendly to Nato, the US or any other group, whether local or international. Whose foreign reserves will be targeted next?

Looking 7,000km west of Moscow we have another incident, which may have been overshadowed by the events in Eastern Europe, but may possibly be even more significant in driving forward crypto adoption. February saw the Canadian government evoke the Emergency Act to force traditional finance companies to freeze the accounts of those who were supporting a Covid-19 mandate truck driver protest in Ottawa. Other than the fact that the government resorted to this weaponization of the monetary system, it also included those who simply indirectly supported the protest via their donations. While the freeze ended within a week, the actions have set a dangerous precedent. For those who would argue that the freezing of Russian central bank assets is an act done in the heat of war and not something expected during more ‘peaceful times’, the actions in Canada exemplify that this is simply not the case.

One other idea to consider here is the narrative shift around globalization and how it relates here. For the last few decades, nations found that massive benefits are to be gained by looking abroad, whether for cheaper labor or for lower regulatory standards, the positives were apparent and the risks overlooked. Countries and companies continued to globalize and interdependence became the norm. Next came Covid-19 and the first big realization that our interdependence has reached a level that had not previously been obvious and just a small disruption to our supply chains can lead to the rapid emergence of chaos. The Russia-Ukraine crisis has significantly added to this narrative shift, not least because while the US keeps increasing sanctions, ultimately, Europe has been unable to sanction that which is most important to Russia - their energy. The realization that continental Europe is overly reliant on Russia’s energy has been a chilling reminder that globalization does indeed have its pitfalls and that we increasingly live in a world where positive relations with foreign nations may be crucial to our national infrastructure. The recognition of our dependencies has already started to and will continue to prompt nations and companies alike to reevaluate their operations and likely lead to an increase of onshoring or nearshoring. Perhaps a shift towards obtaining the safest, rather than the cheapest or easiest, sources for our economic needs will be the next major narrative. To reference Howard Marks, the pendulum certainly seems to be shifting away from globalization.

Taking these ideas together we should have a stronger idea of what we can expect from crypto in the medium term. It is clear that the above instances of monetary weaponization are setting a dangerous precedent and undoubtedly drive the use case for governments, companies and individuals to hold non-fiat instruments. The shift away from globalization towards a more localized economy further adds to this use case, as more and more nations look to build wealth in assets that cannot be frozen or censored. Crypto can be the clear winner here, driven forward by its role as a payments mechanism that is subject to significantly less interference than the current financial system. Furthermore, if the next iteration of the global age is one of more distrust than the last few decades, a trustless and permissionless system based on blockchain technology is inevitable.

Conclusion

The Russia-Ukraine crisis, or perhaps the first crypto war, has changed things forever. The ability to connect with a worldwide community of individuals and raise financing in the context of a military crisis is a step change to what has been considered possible until now. The weaponization of our existing monetary system further catalyzes the importance and reach of non-fiat, crypto assets and does a major service towards hastening the move towards a digital, crypto-centric world. Markets appear to be bouncing back strongly, with Bitcoin trading around well and total crypto market cap up ~24% over March and rising. The question remains, how much of the ~$13tn in global foreign exchange reserves10 do we see enter the ~$2tn crypto market?

https://www.reuters.com/business/global-markets-flows-graphic-2022-03-25/ ↩

https://blog.chainalysis.com/reports/cryptocurrency-ukraine-russia-sanctions/ ↩

https://www.banking.senate.gov/hearings/understanding-the-role-of-digital-assets-in-illicit-finance ↩

https://www.coindesk.com/markets/2022/03/23/bitcoins-correlation-to-sp-500-hits-17-month-high/ ↩

https://data.imf.org/?sk=E6A5F467-C14B-4AA8-9F6D-5A09EC4E62A4 ↩