Original author: Chase Devens Original source: Messari Original title: State of Crypto Fundraising - Q3 2023 Compiler: Zen, PANews

The cryptocurrency industry’s funding data may be the best example of the industry’s ongoing bear market. Since the beginning of 2022, there has been a downward trend in many quarters, and the third quarter of 2023 is no exception. Its total financing amount and number of transactions have hit new lows since the fourth quarter of 2020. There were 297 financings completed in the quarter, with a total capital size of nearly US$2.1 billion, both down 36% from the previous quarter.

Financing focused on early stages

After dividing the financing events in Q3 by stage, we can see that most are concentrated in the early stages (including pre-seed, seed and series A transactions). Among them, seed round financing accounts for the largest share, with a total of 98 rounds of financing raising US$488 million. Volume trends across different financing stages indicate that over the past three years, the primary market is undergoing a significant shift from late-stage projects (Series B or subsequent financing rounds) to early-stage projects.

Specifically, the share of deals for early-stage investments increased from 37% in Q4 2020 to 48% in Q3 2023, while the share of deals for late-stage deals decreased from 8% in Q4 2020 to 1.4% in Q3 2023. This suggests that investors are pursuing a bear market investment strategy, trying to fund early-stage projects with potentially huge upside that could deliver more returns when market sentiment eventually turns positive.

There was also a large amount of funding provided in the form of strategic investments in the third quarter, with the most prominent being corporate and private equity transactions, such as the Islamic crypto project Islamic Coin's $200 million financing. Strategic financing transactions have been steadily increasing throughout the bear market. At the peak of the bull market in the fourth quarter of 2021, strategic rounds accounted for only 0.2% of total financing. In the third quarter of 2023, this proportion climbed to 22%, indicating that severe market conditions are forcing projects to raise short-term bridge funds or eventually be acquired by larger projects.

Investment and financing situation of each track

Infrastructure, DeFi and Games

From the perspective of investment tracks, the allocation of industry funds in the third quarter of this year is similar to that in the past 12 months. During this period, public chain infrastructure, DeFi and games have been the most funded tracks. In addition to them, only the service industry, which includes functions such as marketing, incubators, security and legal services, can achieve an average monthly financing scale of more than US$100 million in the past 12 months. Although other fields are also important to the development of the entire crypto industry, most investors are currently focusing on these four fields.

Another notable trend over the past year is the increase in the amount of funding for infrastructure-based projects compared to user-facing applications (Dapps). In the track division, we classify the consumer, DeFi and gaming fields into the "Application" category, and classify areas such as application infrastructure, blockchain infrastructure, custody and DePIN into the "Infrastructure" category.

Funding in the third quarter was relatively dispersed across various verticals, with public chain infrastructure accounting for the largest share of funding, reaching 18%; DeFi led in terms of the number of financings, reaching 67 deals; the gaming industry remained strong in the third quarter, raising nearly $250 million in the sector.

When looking at the percentage of the amount raised by each category, a subtle shift from user-facing applications to infrastructure projects can be seen. Compared to applications with a higher funding differential, infrastructure projects continue to receive funding. However, this trend may not last long as more investors begin to realize that without successful user-facing crypto applications, infrastructure investments are unlikely to generate expected returns.

Public chain infrastructure occupies the largest market share

Despite only 21 deals, the blockchain infrastructure sector still accounted for the largest share of financing in the third quarter. One-third of the financing belongs to the subcategory of smart contract platforms, such as the blockchain project Fhenix, which completed a $7 million seed round of financing. It is the first blockchain supported by fully homomorphic encryption. By using fhEVM, Fhenix enables Ethereum developers to seamlessly build encrypted smart contracts and perform data encryption calculations while using Solidity and other familiar and easy-to-use tools.

Scaling solutions accounted for 43% of the funds raised in the industry. This represents a continued shift from smart contract platforms to scaling solutions. In the first quarter of 2022, Polygon raised $450 million for its suite of scaling solutions, marking the first time that scaling solutions funding exceeded that of smart contract platforms. In three of the past four quarters, the ratio of funds invested in scaling solutions to smart contract platforms exceeded the previous high in the first quarter of 2022. In particular, in the fourth quarter of 2022, the ratio was as high as 7 times, mainly due to the lack of investment activity in the smart contract platform category in that quarter.

More than 40% of the $387 million in funding for public chain infrastructure in the third quarter of 2023 came from the Optimism Foundation, which sold approximately 116 million OP tokens in late September to further its development. Other significant transactions include Flashbots’ $60 million Series B funding to continue the development of SUAVE, and Bitmain’s $54 million strategic investment in Core Scientific, a leading Bitcoin mining company.

Decentralized finance focuses on DEX investment

DeFi was the track with the largest number of financing projects in the third quarter, with a total of 68 investment and financing events, raising $210 million, and an average transaction size of $3 million. Investment in DeFi projects is highly concentrated, with 33 financings in the DEX (decentralized exchange) category alone, and the funds raised accounted for 38% of all investments.

Binance Labs is an active investor in the DeFi space, completing seven investments this quarter, including $10 million strategic investments in Helio Protocol, a liquid equity platform on BNB Chain, and Radiant Capital, a LayerZero-based money market. The largest DeFi financing this quarter was a $16.5 million Series A for Brine, an order book DEX based on Starkware.

Three of the top four DeFi investors by deal count in Q3 are investment entities in various public chain ecosystems. Binance Labs, Base Ecosystem Fund, and Polygon participated in 16 deals in total.

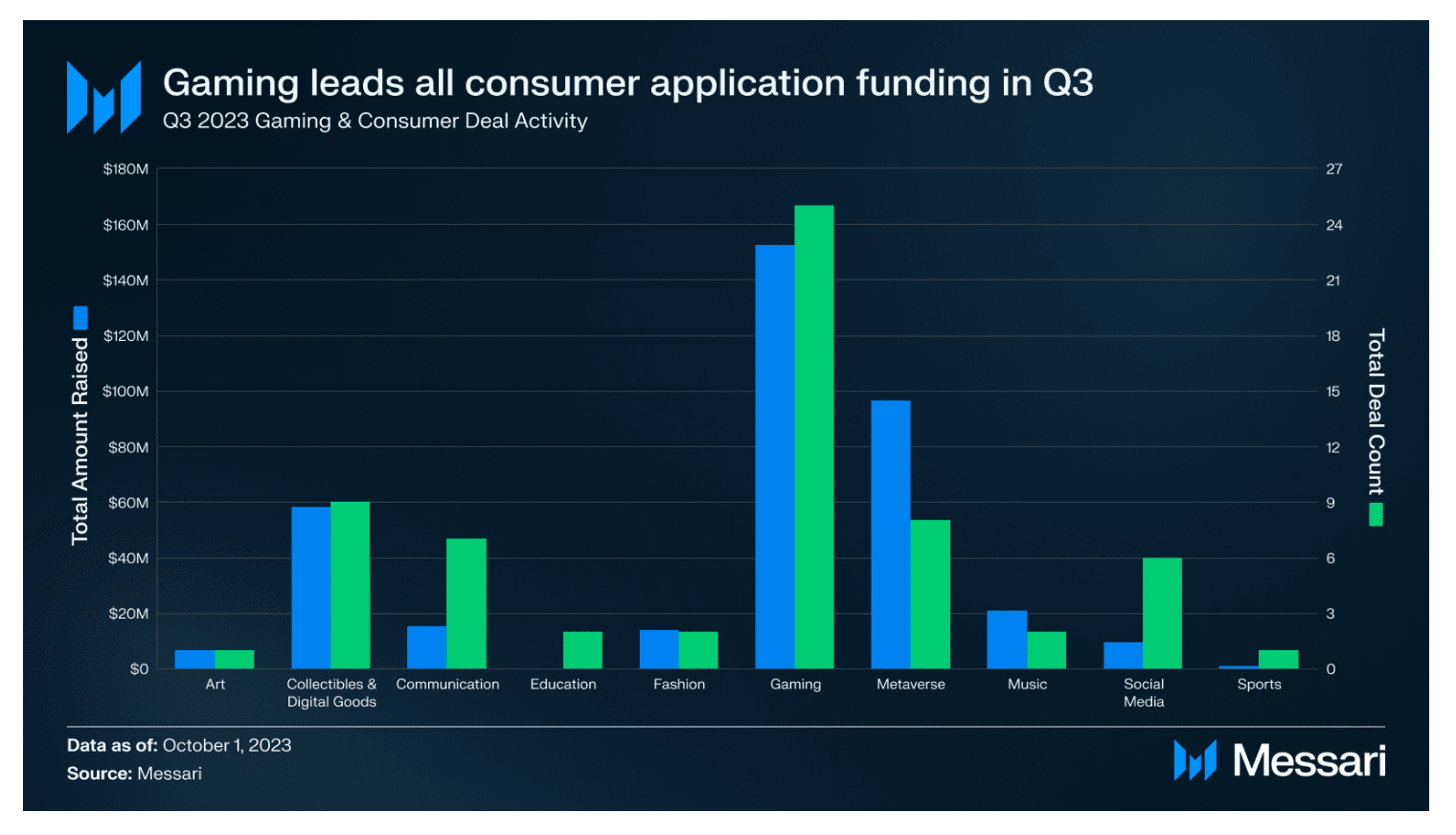

Game investors show a long tail phenomenon

The gaming industry has accumulated a large number of early-stage rounds, making it the third most funded industry in the third quarter, with 33 rounds raising a total of $249 million. Compared to other user-facing applications in the consumer space, games accounted for 67% of capital investment in the third quarter.

The vast majority of funding in the gaming industry comes from long-tail investors. Only 7 entities have made investments in two or more projects, while 104 investors have made single-project investments in the industry.

The largest deal in the gaming space was a $54 million Series A round for Futureverse, a platform that combines AI and virtual worlds. Other virtual world-based gaming projects such as Mocaverse and Mahjong Meta also received funding during the quarter. In addition, Proof of Play received $33 million in seed funding from lead investors a16z and Greenoaks. The online gaming studio was founded by Amitt Mahajan, one of the creators of Zynga's hit game Farmville.

Binance Labs becomes the most active VC, and the United States still accounts for half of the investment

In the third quarter, the 10 most active investors in the cryptocurrency industry made a total of 98 investments, accounting for only 7% of all investor transactions, indicating that cryptocurrency financing is still dominated by long-tail investors.

Binance Labs is by far the most active investor, having completed 23 investments in the third quarter, more than twice as many as the second largest investor, Robot Ventures. Binance Labs has been actively investing throughout 2023, focusing on DeFi and gaming. In addition, projects developing ZK and privacy technologies are also their investment targets. It is worth noting that 12 of Binance Labs' 23 transactions were projects participating in its accelerator program. However, even if these investments are excluded, its remaining 11 investments would still make it the most active investment institution in the third quarter, tied with Robot Ventures.

Finally, it is worth noting that 54% of active investors in the third quarter were from the United States. This figure is roughly consistent with the quarterly average of the past four years (55%). This shows that although project founders are slowly leaving the United States in favor of more regulatory friendly jurisdictions, the United States is still home to the majority of cryptocurrency investors.