When I try to understand a token beyond a good week on the chart, I always come back to one simple question:

Who actually needs to buy this token, who keeps holding it, and does the value created by the ecosystem really flow back into the token — or quietly leak somewhere else?

That’s the lens I’ve been using with $VANRY.

Vanar is not presenting itself as just another fast Layer-1. The team keeps talking about building a full stack around data, memory, and reasoning on top of the base chain. Whether someone fully buys that vision or not, it does change how you should evaluate the token.

Because in the end, a token only survives long term if the economic loop makes sense.

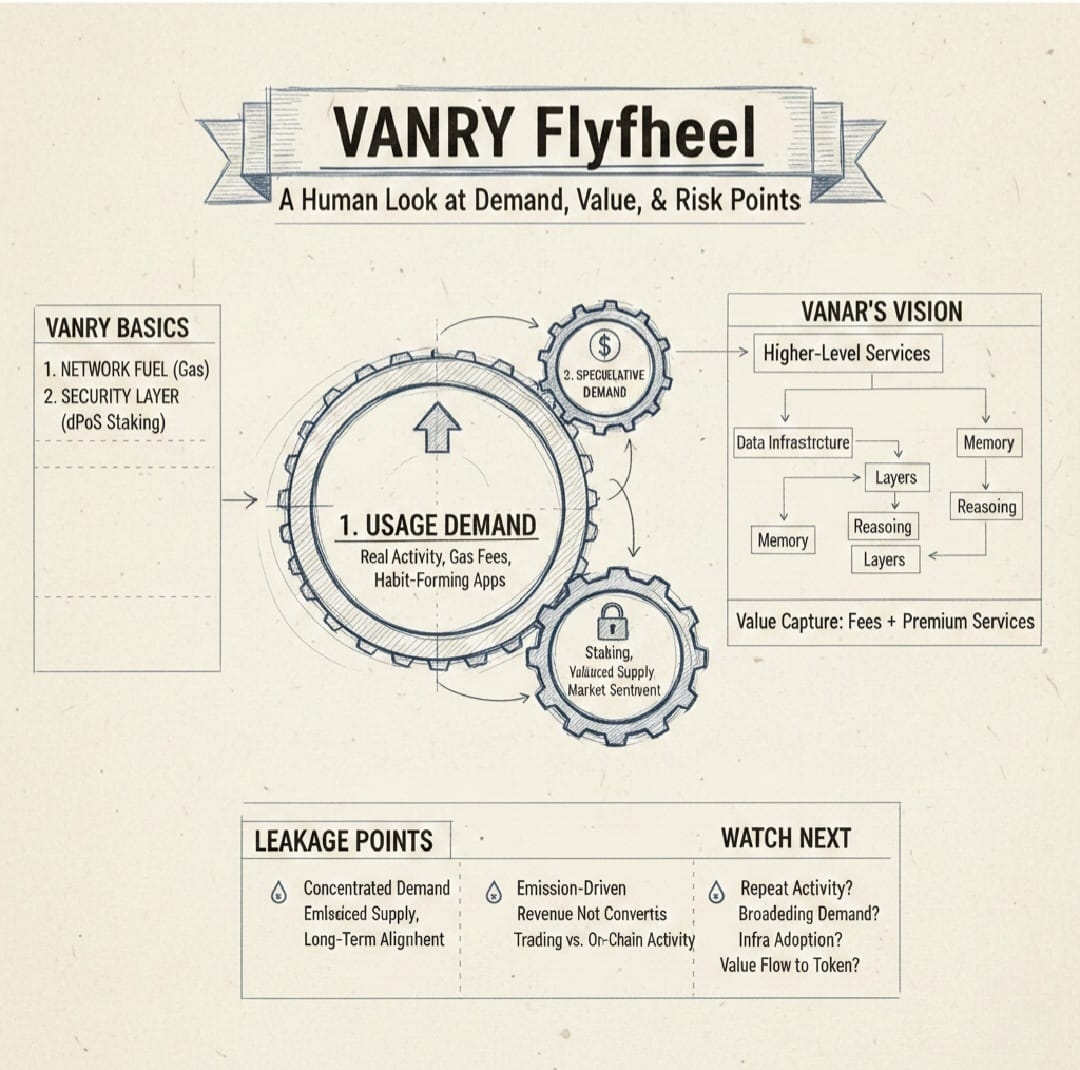

Start with the basics: what VANRY is supposed to do

At the most fundamental level, VANRY has two clear jobs.

First, it is the fuel of the network. Every time an application interacts with Vanar — moving assets, calling contracts, updating state — the system needs gas, and gas is priced in VANRY. That creates the baseline demand.

Second, VANRY is part of the security layer. Through delegated proof of stake, holders can stake and validators earn rewards for securing the network. This creates a holding channel, not just a spending one.

On paper, that is already healthier than a token that only exists to be spent once and forgotten.

But the real question is not whether utility exists.

The real question is whether the loop becomes strong at scale.

Where real demand begins

Every ecosystem starts with simple usage.

If people are genuinely using applications on Vanar every day, then some party — either the user or the application operator — must continuously acquire VANRY to pay for computation and settlement.

This is the most honest form of demand. It does not depend on hype. It depends on activity.

However, modern consumer chains often try to hide gas from the user to make onboarding smooth. And that’s where things get more nuanced.

If millions of small users each buy a little VANRY, demand becomes broad and naturally distributed.

But if most fees are sponsored by a small number of app operators, then demand becomes more concentrated. Operators behave differently than retail users. They optimize costs, they hedge exposure, and they manage inventory carefully.

So the network can look very busy while open-market token pressure grows more slowly than people expect.

That doesn’t kill the model — but it does change the dynamics in an important way.

The holding side of the story

Staking is where the token economy becomes more delicate.

In theory, staking is healthy. It removes liquid supply from the market and aligns participants with the long-term success of the network. It turns the token from something purely transactional into something closer to productive capital.

But staking only strengthens the system if the reward structure is balanced.

If most rewards come from heavy emissions, validators and delegators often sell a portion of those rewards to fund operations. Over time, that can create steady background sell pressure that the ecosystem must constantly absorb.

If, on the other hand, more of the security budget is supported by real network activity and fee flows, the system becomes more self-sustaining.

So the important question is not simply whether staking exists.

It’s whether staking is supported by real economic activity or mainly by inflation.

Where Vanar is trying to go further

This is where Vanar’s broader positioning becomes interesting.

The project is not only talking about blockspace. It is talking about higher-level services — memory layers, reasoning layers, and structured data infrastructure.

Why does that matter?

Because a pure Layer-1 mostly captures value through fees. And fee-only models are often fragile. They depend heavily on constant congestion.

But if higher-level services generate recurring paid usage, and that usage reliably converts back into VANRY demand — for example through subscription conversion and buy mechanisms — then the token starts capturing value from multiple directions.

That is the difference between a chain that is merely busy and a chain that is economically sticky.

Of course, the key word here is consistency.

Markets do not reward occasional buybacks or one-off campaigns. They reward systems where value routing is predictable and observable over time.

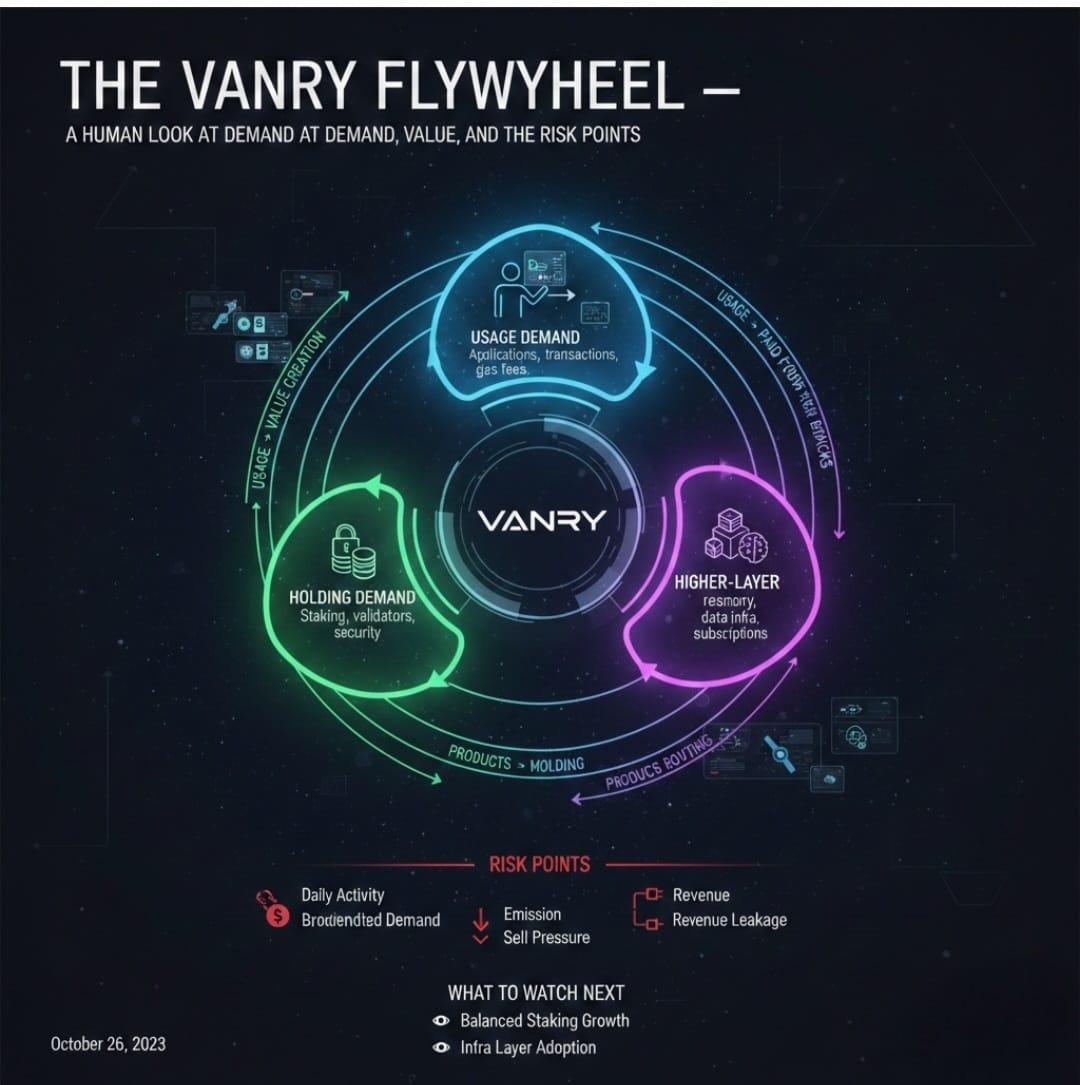

The three layers of VANRY demand

If you step back, VANRY demand really lives in three buckets.

The first is usage demand. This is the healthiest layer because it is forced by real activity. If the network becomes habit-forming for users and builders, this demand becomes quietly powerful.

The second is holding demand from staking and validator participation. This reduces circulating supply and aligns long-term participants, but it must stay balanced with real usage to avoid becoming a sell-pressure machine.

The third is speculative demand. This will always exist in crypto. It only becomes dangerous when it runs too far ahead of actual usage for too long.

Healthy ecosystems eventually let the first two layers carry more weight than the third.

Where the flywheel can still leak

Even well-designed systems have weak points, and it is better to say them clearly.

Leakage can happen if most gas responsibility is pushed to a small set of sponsors and demand becomes overly concentrated.

Leakage can happen if emissions dominate the reward structure and recipients sell continuously.

Leakage can happen if premium products generate revenue but that revenue does not reliably convert into VANRY demand.

And leakage can happen if most attention and liquidity sits in trading markets that are disconnected from real on-chain activity.

None of these are fatal on their own — but they are the pressure points worth watching closely.

Why this project matters

Because the real problem in this industry is not launching tokens.

It is building tokens that actually capture the value of the ecosystems they power.

Vanar is clearly trying to design a system where:

usage creates recurring demand

staking commits supply to security

higher-layer products create additional paid flows

and part of that value is routed back into the token economy

If that loop strengthens over time, VANRY stops behaving like a simple gas coin and starts looking more like a network asset tied to real economic activity.

That is the long game.

What to watch next

If you want to stay grounded and avoid noise, keep an eye on a few simple things:

Are applications generating repeat daily activity, not just short spikes?

Is VANRY demand broadening over time or staying concentrated?

Is staking growing in a way that doesn’t overwhelm the market with sell pressure?

Are paid infrastructure layers showing measurable adoption?

And most importantly, is the value created by the ecosystem visibly flowing back into the token?

Those answers will matter far more than any single green candle.

Because in the end, flywheels don’t prove themselves in weeks.

They prove themselves in habits.