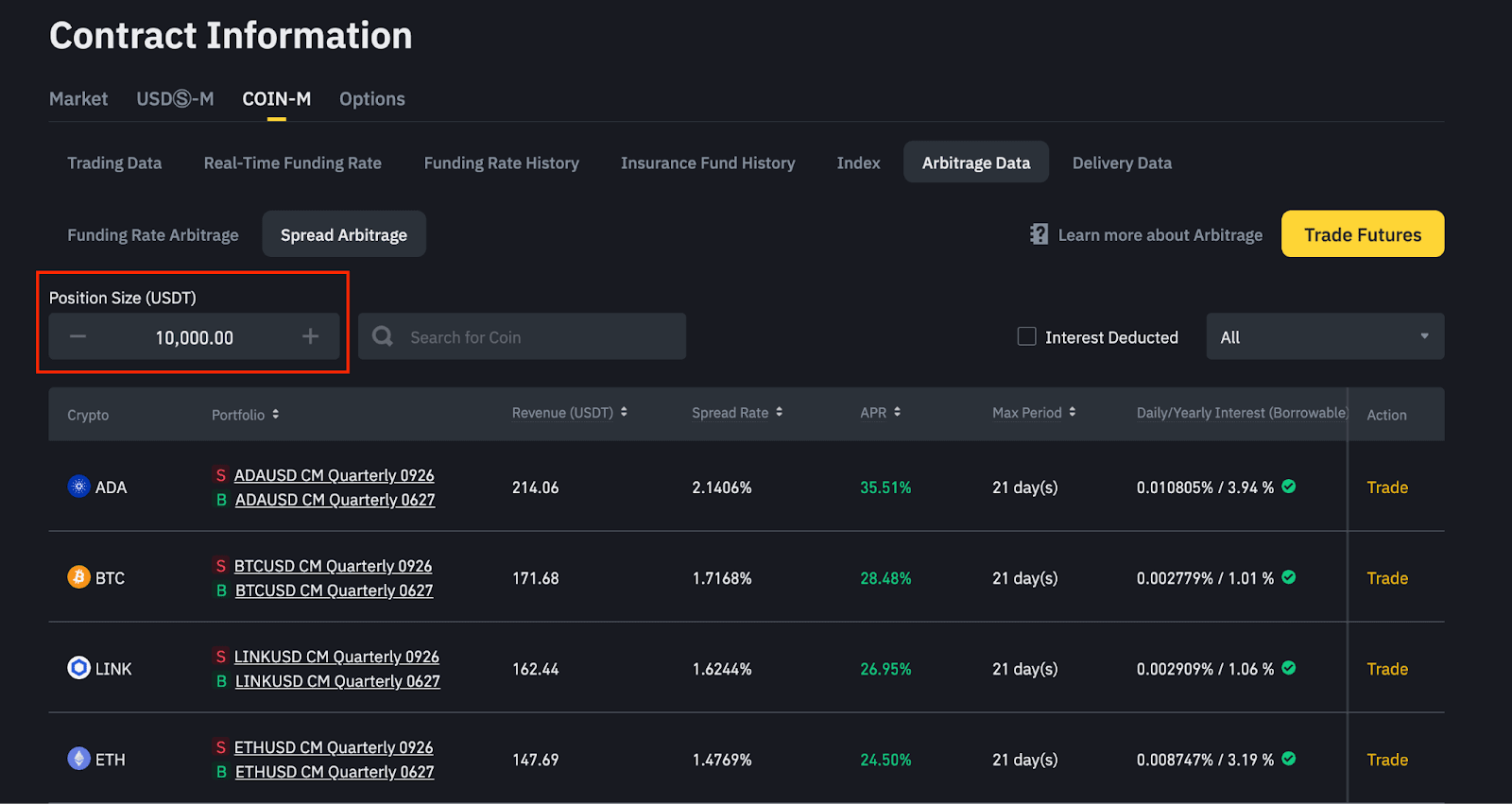

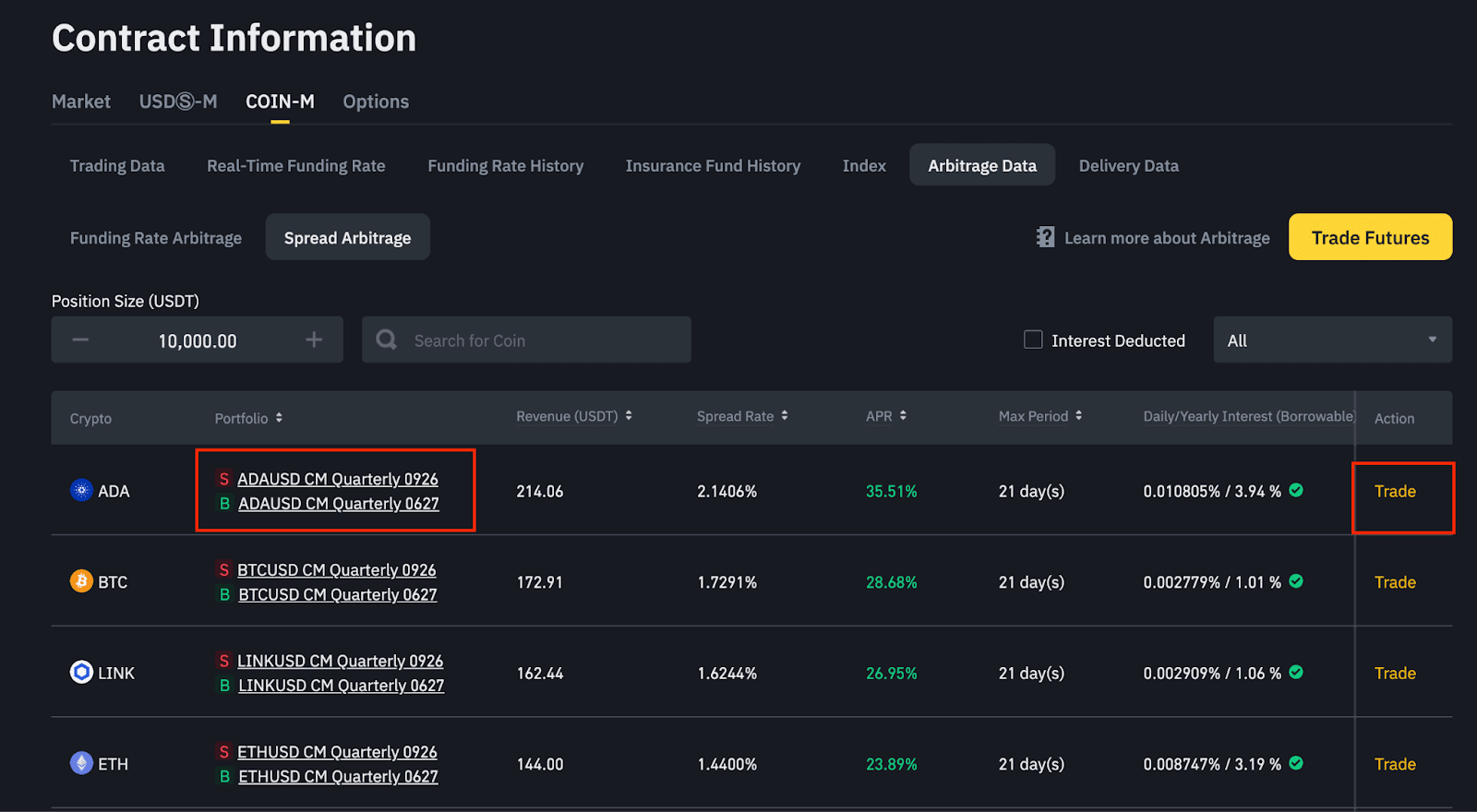

The Spread Arbitrage section on Binance Futures provides you with the relevant arbitrage information about Quarterly Futures Contracts and their spot equivalents in the market.

Also known as “Calendar Spread Arbitrage,” Spread Arbitrage is a common hedging technique that uses deltas in extrinsic value between 2 distinct expiration contracts of the same token to generate a profit.

The Futures price reflects the market sentiment of the subject’s price. In the Futures market, a different settlement time contract of the same token will differ. For example, at writing time, the Mark Price of the quarterly contract is USD 10,033.3, while that of the bi-weekly contract is USD 9,973.88.

Delivery Futures contracts with different expiry dates (e.g., BTCUSDT Quarterly 220930 and BTCUSDT Quarterly 221230) will almost always show different prices.

The Futures prices of a given asset reflect the market sentiment toward its Spot price. Unlike Perpetual Futures contracts with no expiry dates, Delivery Futures contracts always converge with Spot prices at expiration dates.

This convergence allows you to identify and anticipate Delivery Futures price trends while taking advantage of the spread between Spot and Futures contracts of the same asset with different expiries to make profits.

The “Spread” refers to the difference between the price of an asset in the Spot market and its quarterly equivalent (e.g., BTCUSDT Quarterly 220930 - BTC/USDT) or between the prices of its quarterlies with different expiries (e.g., BTCUSDT Quarterly 221230 - BTCUSDT Quarterly 220930).

Spread Arbitrage describes a delta-neutral strategy consisting of taking two opposite positions on contracts with different expiries (spot-futures or futures-futures) while collecting their spread at a given time.

Go to Binance Futures and mouse over [Data]. Click [Futures Data] - [Arbitrage Data]. Then, click on [Spread Arbitrage] above the table.

Examples of Spread Arbitrage strategies on Binance Futures

Binance Futures displays the arbitrage data for USDⓈ-M and Coin-M contracts, covering two types of Spread Arbitrage: Spot-Derivatives and Derivatives-Derivatives arbitrages.

Let’s take DOT Spot and Quarterly contracts as an example:

For Spot-Derivatives portfolios, Spread Rate = (Futures Price - Spot Price) / Spot Price

= (6.424 - 6.45) / 6.45 = -0.4 % (at the time of trading)

Since the Spread Rate is negative, you sell it on the Spot market (i.e., DOT/USD) and buy a long quarterly contract (i.e., DOTUSD Quarterly 220930):

Let’s assume the DOT Spot Price drops by 10% from its initial price on 220930 at the expiry time of 08:00 (UTC):

Estimated Revenue = | Current Spread Rate | * Position Size (USDT)

Now let’s assume the DOT Spot Price increases by 10% from its initial price on 220930 at expiry time 08:00 (UTC):

Let’s take BCH quarterly contracts as an example:

For Derivatives-Derivatives portfolios, Spread Rate = (Longer-Term Contract Price - Near-Term Contract Price) / Near-Term Contract Price = (107.61 - 109.58) / 109.58 = -1.7978% (at the time of trading)

Unlike perpetual contracts, quarterly contracts will converge with the Spot Price at their respective expiries. The spread will narrow as both the near-term and the longer-term contract price will converge toward the Spot Price.

Let’s assume both contract prices drop by 10% from their initial price at their respective expiry times:

Now let’s assume both contract prices increase by 10% from their initial price at their respective expiry times:

You can adjust the USDT position size used to calculate the estimated revenue for USDⓈ-M and Coin-M trading pairs arising from Spread Arbitrage.

The [Portfolio] column indicates the direction of the arbitraging trades between Quarterly Futures and Spot or between Quarterly Futures with different prices and expiries.

You can click the contract links or the [Trade] button on the right to access the corresponding trading interfaces for both markets and start arbitraging with order placements.

Based on the Spread Rate sign (positive or negative), the [Portfolio] column will display arbitrage trade directions of a given trading pair as per the following:

An estimation of the revenue generated by the selected position size when employing the corresponding arbitrage strategy, taking the current Spread Rate as a reference.

The difference between the prices of the two contracts is considered part of the arbitrage strategy.

The Annual Percentage Rate generated by extrapolating the Spread Rate to a year.

Coin-M APR = | Current Spread Rate | * 365 / Max Period (in days)

USDⓈ-M APR = | Current Spread Rate | * 365 / Max Period (in days)

*Max Period less than 1 day will be calculated as 1 day

Arbitrage traders will collect the estimated revenue at the end of the Max Period.

The current cost of borrowing the corresponding asset.

The interest rate of the crypto is based on your Binance VIP level. Please note that the Borrow function (borrowable) may be disabled during extreme market conditions.

You can quickly navigate to Perpetual or Spot markets via the [Trade] button.