In the DeFi market, stablecoins have always been the core medium connecting crypto assets with real value. However, most stablecoins either rely on a single collateral or have insufficient yield, making it difficult to meet the diverse liquidity needs of users. The over-collateralized synthetic stablecoin USDf launched by Falcon Finance breaks this limitation with its 'dual minting model', supporting both 1:1 exchanges of stablecoins and allowing non-stablecoin assets to be used as collateral for minting, balancing security and flexibility. This article will analyze the core logic, applicable scenarios, and considerations of the two minting models of USDf from the user's perspective.

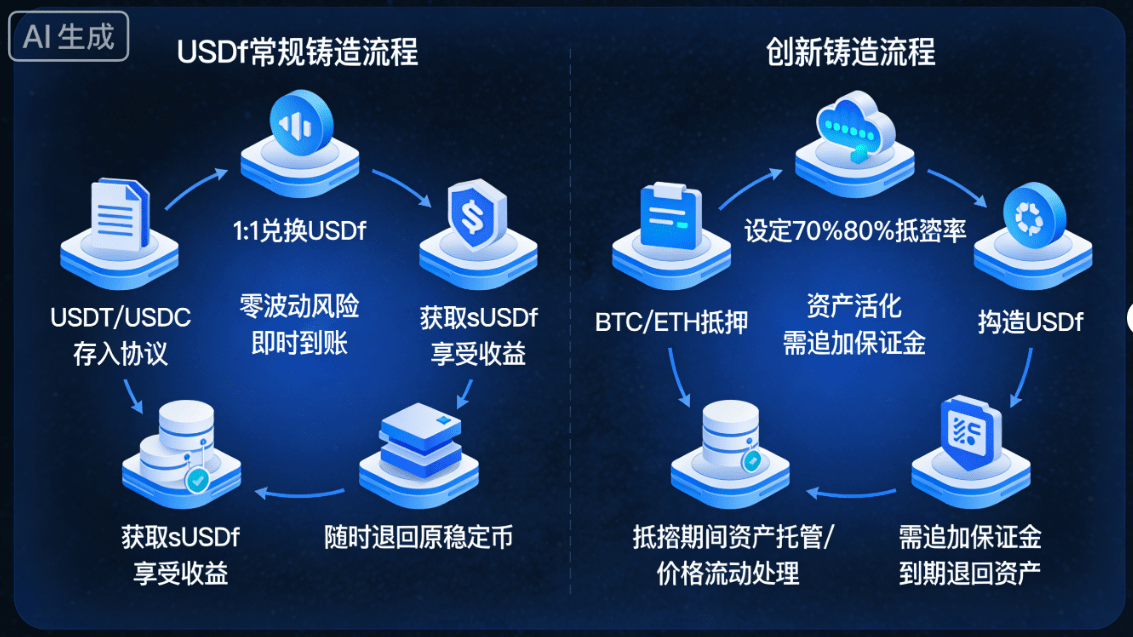

1. Conventional Minting: 'Zero Threshold Monetization' for Stablecoin Holders

The conventional minting mode of USDf focuses on 'convenience', primarily targeting users holding mainstream stablecoins like USDT and USDC. The operation logic is very simple: users only need to deposit USDT, USDC, etc., into the Falcon Finance protocol to exchange 1:1 for USDf, with no extra fees, and the exchange rate remains constant. The core advantage of this mode is 'zero volatility risk', as the collateral itself is stablecoins, eliminating concerns about liquidation risk due to market price fluctuations, making it suitable for users seeking stable and quick access to on-chain liquidity.

For example, if a user holds 1000 USDT and wants to participate in Falcon Finance's staking yield activities, they can directly mint 1000 USDf through conventional minting and deposit it into the protocol's treasury to obtain sUSDf, thereby enjoying subsequent yield appreciation. In addition, USDf from conventional minting can be redeemed at any time for the original stablecoin, providing strong liquidity, suitable for short-term capital turnover or flexible allocation needs.

2. Innovative Minting: A New Path to 'Asset Activation' for Non-Stablecoin Holders

Compared to conventional minting, innovative minting is the core differentiated highlight of USDf, primarily targeting users holding non-stablecoin assets like BTC and ETH who are unwilling to liquidate. The core logic is: users collateralize BTC, ETH, and other assets, and lock them for a certain period to mint USDf, while still being able to enjoy potential appreciation of the collateral. However, due to the significant price volatility of non-stablecoin assets, this mode requires users to add a certain proportion of collateral to avoid liquidation risk.

Specifically, suppose a user holds 1 BTC, and the current market price is $40,000. If they choose to mint USDf innovatively, the protocol will set the collateral rate (usually 70%-80%) based on the market price and volatility coefficient of BTC, allowing the user to mint approximately $28,000 to $32,000 of USDf. During the collateral period, the user's BTC is still held by an independent custody institution. If the price of BTC rises, the user can unlock the appreciation by supplementing with a small amount of collateral or redeeming part of the USDf; if the price falls and the collateral rate falls below the warning line, the protocol will alert the user to add collateral to avoid asset liquidation.

The core value of this mode lies in 'asset activation', allowing users to obtain stable dollar-pegged liquidity without liquidating their crypto assets, retaining the long-term appreciation potential of the assets while being able to use USDf to participate in various DeFi activities, achieving 'one asset, two yields'. This is suitable for users who hold crypto assets long-term and wish to enhance the utilization of their funds.

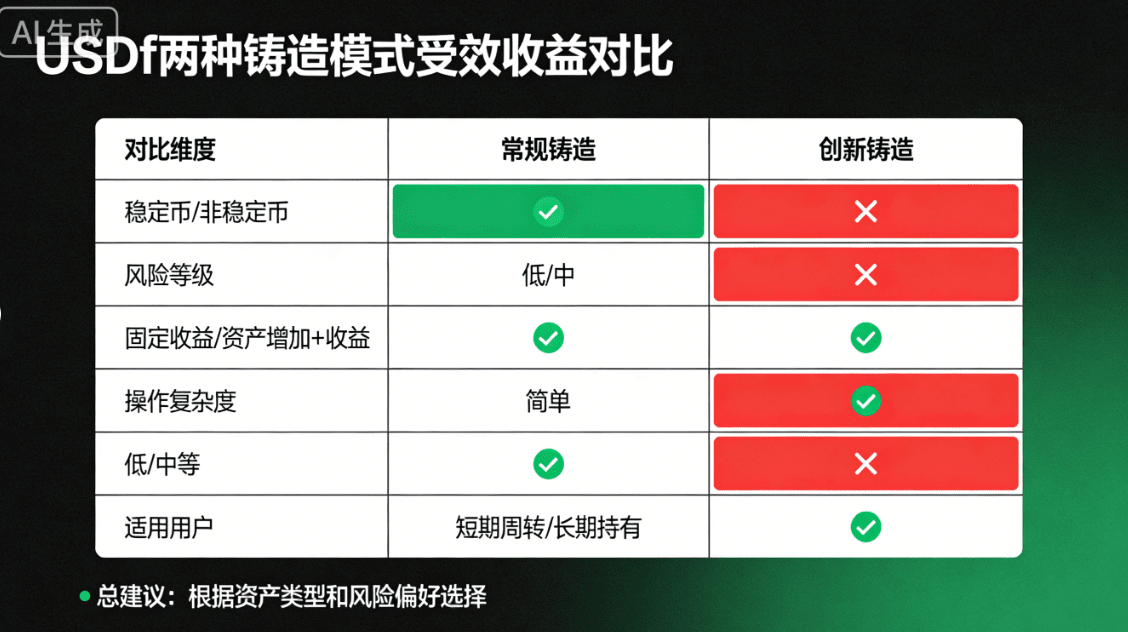

3. Core Comparison and Selection Suggestions for Two Minting Modes

Overall, the two minting modes of USDf cater to different user groups, with core differences concentrated in three dimensions: collateral type, risk level, and yield potential. Conventional minting is suitable for stablecoin holders, with low risk and simple operations; innovative minting is suitable for non-stablecoin holders, with moderate risk and higher yield potential. Users can choose the corresponding mode based on their asset allocation and risk tolerance.

It is important to note that regardless of which minting mode is chosen, users need to pay attention to the risk control measures of the protocol: Falcon Finance has established a $10 million insurance fund, and it is audited weekly by the third-party auditing firm Harris & Trotter LLP to maximize the safety of user assets. Meanwhile, users are advised to reasonably plan the minting amount based on their own funding needs to avoid liquidity risks caused by over-collateralization.