The current round of interest rate hikes in the United States started in March last year, and it has been a year and a half since then. This rapid and substantial financial tightening is actually what we usually call financial warfare. It’s just that we are in it, and it doesn’t seem so obvious, because some of the problems we encounter in reality are often not associated with financial tightening.

In fact, on the surface, they seem unrelated, but at a deeper level, they are inextricably linked. When the US loosens its monetary policy, it prospers, and when it tightens its monetary policy, it often suffers from depression. The US dollar is the world currency, so its influence is usually global. This time, coupled with the US's containment and containment of us, the impact is naturally more serious.

What everyone is most concerned about now is that the global economy seems to be in trouble. Can we withstand the financial offensive of the United States this time? If the United States cannot successfully carry out financial harvesting, what impact will it have on the future world? What changes will occur in the global structure and future economic conditions?

I want to understand these issues, so I try to compare the current situation with that of 2015. At the end of 2015, the United States conducted a financial tightening, but it failed to reap the benefits. Let's compare the current situation and see if the United States has failed again or won the battle.

I plan to start with the most significant changes in the United States and China, and compare the past and present. Let's see where this competition will go in the end.

Let’s talk about the United States first.

【Three major differences facing the United States】

In December 2015, at the end of 2015, the United States launched its first financial tightening since 2008. This was actually a financial war against us. At that time, the United States felt that the situation was slowly getting out of control, at least on the surface, for two main reasons.

The first reason is that if a large amount of money flows out, there will be a passive and uncontrollable monetary tightening in the country.

The second reason is that on August 11, 2015, we launched a historic exchange rate reform, which was called the 811 exchange rate reform. It changed the exchange rate of our currency from being closely linked to the US dollar to being pegged to a basket of currencies.

The essence of these two things is that we have to take back our currency issuance rights. Why? If the currency issuance rights and pricing rights are tied to the US dollar, then in terms of currency and finance, the United States actually indirectly holds the initiative and control.

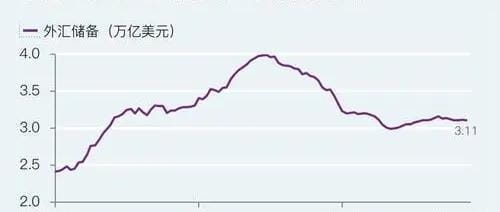

After the currency decoupling, the United States felt that it had to quickly carry out financial harvesting. At the end of that year, the United States began a round of financial tightening. However, if we look back at the last financial war of the United States, the financial harvesting of the United States was obviously a failure. Our first financial firewall is foreign exchange reserves, and the United States has not even been able to break through this.

Before the financial war, our total foreign exchange reserves were as high as $4 trillion. After the US started tightening, a lot of dollars flowed out, and the foreign exchange reserves were less than $3 trillion at the lowest point. But since then, it has never been lower than this scale, which has built the first firewall for us in terms of national financial security.

The United States has not even broken through the first firewall, let alone the so-called financial harvesting operations that followed. If we look back at the last round of financial war and compare it with the present, we can find that the United States has also undergone some changes internally over the years.

There are mainly three differences among them.

The first difference is that the monetary base of the dollar contraction is different compared to 2015.

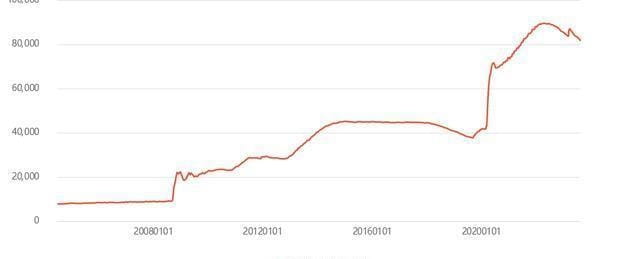

The United States began financial tightening at the end of 2015. After the 2008 financial crisis, the U.S. balance sheet expanded significantly, and later carried out several rounds of quantitative easing (QE). But even so, at the end of 2015, the Federal Reserve's balance sheet had only expanded from less than $1 trillion in 2008 to $4 trillion.

The situation of monetary easing in the United States was relatively not so serious as to be out of control. Generally speaking, the financial risks in the United States were more controllable at that time, and it was not to the point where it had to gamble everything on one throw.

Before this round of financial war, the US stock market collapsed during the epidemic. In order to save the market, the Federal Reserve had no choice but to release money without limit. As a result, the Federal Reserve's balance sheet expanded rapidly in a short period of time, doubling from less than 4 trillion US dollars to more than 8 trillion US dollars.

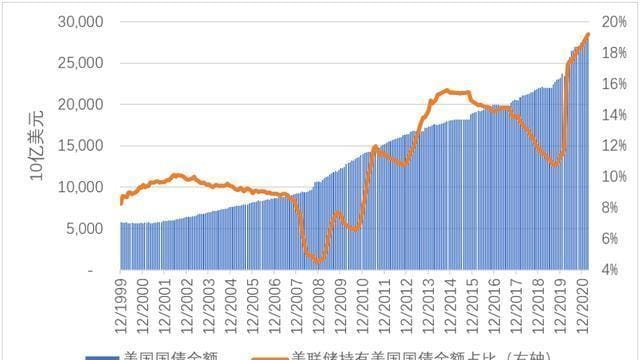

Now let's take a look at the size of the US national debt. In 2015, the US national debt was less than 20 trillion US dollars, but when interest rates began to rise last year, it was almost 32 trillion US dollars.

The biggest difference between the last round of US interest rate hikes and this round of financial tightening is that there was an unlimited amount of money released by the Federal Reserve in the middle. By the beginning of last year, the United States had no other choice but to go all out. This is the difference determined by the monetary and financial foundations of the United States.

The second difference is that compared to 2015, the United States has almost completed its internal mobilization.

During the last financial war, Sino-US relations were at least calm on the surface. The US had not yet officially torn its relationship apart, and had not publicly adopted all its containment and containment measures. In 2018, all this has completely changed.

The United States failed to reap the financial war it started in 2015. This became the fuse for Trump to publicly adopt various containment measures in 2018. During his term in office, Trump constantly indoctrinated and brainwashed the United States, and then the United States began to realize that the world is no longer the same as before.

However, they are running wildly on a crazy but wrong path. By 2022, both the Democratic Party and the Republican Party in the United States have reached a basic consensus on many international issues. In other words, after several years of preparation, the United States has completed basic internal mobilization at least at its top level.

This can be said to be a major change in the internal politics of the United States compared to 2015.

The third difference is that compared to 2015, the United States is pushing for international mobilization.

In 2015, the interests of Europe and the United States were not yet tied together. The core of Europe, especially Germany, under the leadership of Merkel, had a relatively independent foreign policy. The United States wanted to hold Europe's interests hostage, but in 2015, it was still somewhat unable to do so.

But in 2023, after experiencing the pandemic and the conflict between Russia and Ukraine, populist forces in Europe have suddenly grown a lot. Those Western politicians who firmly stand with the interests of the United States have taken the opportunity of elections to come to the fore in recent years.

Especially after the explosion of the Nord Stream pipeline, the interests of European countries suffered great damage, but no one had the courage to stand up and defend their own interests. Europe followed the United States more closely. It can be said that the populist forces in the West have gradually united.

What is a little surprising is that when the interest rate hike was at its most tense last year, the UK and Switzerland were hit by crises one after another. But at the critical moment, the US slowed down the pace of interest rate hikes in order to save Europe, and even conducted currency swaps with major central banks to cover Europe's financial risks.

From this perspective, Europe still has an important position in the United States' future global strategy and is a basic base that the United States must not give up.

From these three aspects, the United States has reached a point where it can only go all out and has no way out. Secondly, the United States seems to have made every effort to do this. If you ask what the United States will do if it fails, the only answer the United States can give now is that there is no such thing as failure.

In this situation, we really have no other choice. After the last financial war, we have been constantly eliminating risks in the past few years, and we have also made great changes internally.

【Three major differences in China】

When we faced the US financial tightening in 2015, objectively speaking, we were at an absolute disadvantage. Many people know that two things happened during the US financial tightening: the stock market crash in 2015 and the skyrocketing housing prices in 2016, after which the most stringent purchase restrictions were introduced in various places.

From the perspective of currency, there is a core here, that is, using other methods to lock up a large amount of liquidity. Then, relying on the huge scale of foreign exchange reserves, the pressure of capital outflow was resisted.

However, by 2022, our economic structure and the international environment have undergone some new changes. If we look at these changes from the perspective of international competition, we will find that there are three differences.

The first difference is that the degree of asset price bubble is very different compared to 2015.

In 2015, the overall housing prices in China were relatively reasonable. But since then, the national housing prices have experienced a round of rapid growth, and the housing prices in many popular cities have almost doubled. The reason why we were able to lock in liquidity in the real estate market at that time was mainly because the basic situation at that time was different from that of today.

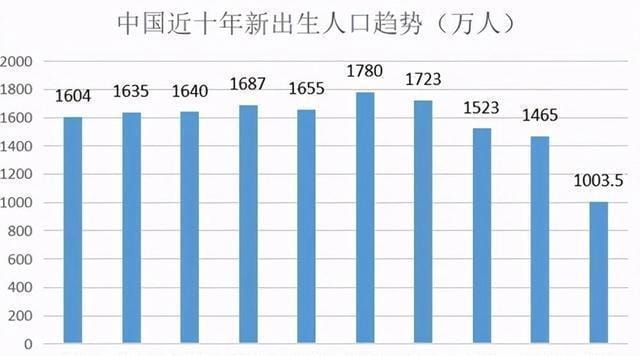

In 2015, the supply and demand fundamentals were still in short supply. At that time, the size of the newly married population and the newborn population were at a relatively high level in the past 10 years. The housing demand was at the end of the last round of population growth peak.

In the past two years, the number of newly married people has dropped below 8 million, and the number of newborns has dropped below 10 million. The scale of this rigid demand is absolute, and it is also shrinking rapidly. This is the biggest change in the fundamentals.

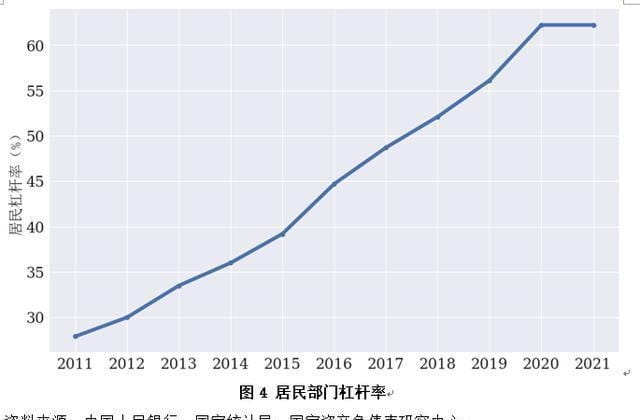

Another difference is in the economic foundation. In 2015, the leverage ratio of our household sector was quite low, less than 40%. However, after the sharp rise in housing prices, many families increased their leverage to buy houses. As a result, the leverage ratio of the household sector has now reached 62%, which is close to the international warning line of 65%. This means that the household sector does not have much room to increase its leverage.

Judging from the changes in the fundamentals of supply and demand and the fundamentals of the economic base, the real estate market can no longer be used as a way to resolve monetary and financial risks. On the contrary, because the degree of asset price bubbles has increased a lot, how to stabilize the level of domestic asset prices has become a key factor in balancing the exchange rate.

The second difference is that compared with 2015, the risks of the internal economic structure have been reduced a lot.

After the 2008 financial crisis, China and the United States launched a joint rescue. Our production capacity in all walks of life, especially traditional industries, expanded significantly, reaching its peak in 2013. But obviously, the United States later promoted the TPP and wanted to isolate us economically, so we had to carry out supply-side structural reforms since 2015.

The core of the supply-side reform is "three cuts, one reduction and one supplement". "Three cuts, one reduction and one supplement" refers to cutting overcapacity, reducing inventory, deleveraging, reducing costs and making up for shortcomings. This is the situation in the economic field, and there are corresponding actions in the social and political fields, one is poverty alleviation, and the other is anti-corruption.

The core purpose of these operations is to reduce economic structural risks in all aspects. As far as the current situation is concerned, after experiencing the trade conflict and technology sanctions of the United States in 2018, the fundamentals of our economic structure are still very solid.

The third difference is that compared with 2015, the risks in the external trade structure have been greatly reduced.

Since the United States promoted the TPP, we have been working hard to sign one-on-one free trade agreements with other countries. After 2015, our actions in trade, currency settlement and other areas have begun to accelerate.

In terms of economy and trade, we need to promote the comprehensive upgrade of the China-ASEAN Free Trade Area, establish RCEP cooperation, and promote the continuous expansion of trade and investment in countries along the Belt and Road. ASEAN has been our largest trading partner for three consecutive years, and the export volume of goods in the Belt and Road countries has also soared.

On this basis, we have promoted currency swaps in various places and increased the proportion of local currency settlement in bilateral trade. In terms of financial risks, our foreign trade structure has become more diversified. In recent years, the surplus income has continued to set new highs, stabilizing the scale of foreign exchange reserves. There is also a gradual consensus on promoting de-dollarization internationally.

From these aspects, compared with 2015, the risks in our economic, trade, social and other structures have been reduced a lot. The main risk is still the problem of high bubble in asset prices such as real estate. How to make it a soft landing and how to ensure the balance and stability of currency exchange rates and asset prices will still be very important in the future.

[Differences in this attack]

In the past seven years, both China and the United States have made some adjustments and changes. Generally speaking, the United States has stepped up its offensive preparations both internationally and domestically, while we have strengthened our defense both internationally and domestically. From a strategic perspective, although the transition from the United States attacking and our defense to a strategic stalemate has already occurred, the situation has not been fundamentally reversed.

There is a big influencing factor here, that is when and how the current round of interest rate hikes in the United States will end. I have said many times that once the US interest rate hike cycle ends, it is time for us to launch a strategic counterattack. This is because the current dominant position of the US dollar has not yet been completely ended.

Let's take a look at these two interest rate hike cycles. The US's offensive methods are actually very different. In the interest rate hike cycle that began at the end of 2015, the US rate hike was slow and uninspiring, with each rate hike being 25 basis points, and the interval between two rate hikes was particularly long. By the end of 2018, when the rate hike cycle ended, the highest interest rate was only 2.5% after three years of interest rate hikes.

The current round of interest rate hikes that began last year has already reached 5.5% in just over a year, with a rapid and large rate hike. The United States has not yet said that the rate hike cycle is coming to an end, but has only said that high interest rates may be maintained for a long time, and even does not rule out the possibility of a large rate hike in the future.

From this perspective, the United States is reckless in this round of financial warfare, just like crazy. Of course, from a strategic point of view, if this desperate attack fails, the consequences will be very tragic.

From a strategic perspective, we need to look at the core fundamentals from the perspectives of politics, economy, and social structure to see how the support is. In these areas, we really need to be more stable. Of course, if we look at the superficial details, we may come to a completely opposite view, mainly because everyone's focus is very different.

For the country, at this stage, should we put risk prevention first or development promotion first? This may be different from what I feel. When the United States is in the interest rate hike cycle, external bargaining is a matter of survival. In this case, it is likely that we can only slow down and put risk prevention as the top priority. After understanding this big background, we will have a general idea of how to make decisions and how to act in accordance with the situation.

#Meme浪潮持续,你看好哪一个? #美国大选如何影响加密产业? #BTC能否站稳6W6 #Canary提交莱特币ETF申请 #鄂B炒家