The Chinese Central Bank Digital Currency (CBDC) is a proposed digital legal tender centrally issued by the People's Bank of China (PBoC), backed 1:1 by fiat reserves (M0 supply), with manageable anonymity and encryption features.

Following Facebook’s recent Libra whitepaper release, the Chinese central bank accelerated its plans to launch its own digital currency amidst growing concerns about continued capital outflows that could weaken the renminbi (RMB).

Based on recent details provided by the central bank-related entities, this digital currency would be based on a “two-tier system” for issuance and redemptions. On the first layer, the PBoC would issue and redeem China’s CBDC via commercial banks. On the second layer, commercial banks would be responsible for re-distributing China’s CBDC to retail market participants. Yet, on this second layer, the use of blockchain remains undecided () as the PBoC still hasn’t drafted a clear technical roadmap for its digital currency.

Furthermore, China’s CBDC would adopt a "loosely-coupled" design, which would allow fund transfers without the need for a bank account.

Through the digitalization of the RMB, the PBoC aims to improve the effectiveness of its monetary policy, while mapping out a more comprehensive picture of all individuals and businesses across China. Further, another key purpose is to increase both the RMB’s turnover rate and its global reach (internationalization). However, concerns remain owing to potential risks and abuses of individual financial privacy.

This report explores existing discussions related to the creation of a sovereign digital currency from the People’s Bank of China (PBoC), along with its potential structure from operational, financial, and technical perspectives.

1. General situation

China is on its way to become the world's first major country to issue a sovereign digital currency, with top officials from the People's Bank of China1 announcing on August 10th 2019 at the latest China Finance 40 Forum that they were “close” to doing so. A heated debate ensued2 in China, following speeches by two of the top Chinese officials at the event.

One of these two officials, Mr. Mu Changchun, the Deputy Director of the PBOC’s Payment and Settlement Department, revealed the People’s Bank of China would soon be issuing its own Central Bank Digital Currency (CBDC), unveiling technical details such as the overall design structure of this digital currency.

A second speech was given by Mr. Sun Tianqi, Chief Accountant of China’s State Administration of Foreign Exchange, explaining that Facebook's Libra (by virtue of excluding the RMB) could have a major impact on China's foreign exchange management and cross-border capital flows, as well as affecting the RMB's internationalization.

These two speeches echoed the former governor of the PBoC Zhou Xiaochuan’s call last month3 that Libra posed a threat to China’s domestic payment systems and to the national currency. As a response, he advised China to “take precautions” in response to the threat posed by foreign corporate-backed digital currencies like Libra. As recently revealed, the PBoC had already set up a dedicated research team in 20144 to work on a “legal digital tender”5.

By issuing a digital currency, it is believed by some analysts that the PBoC could use its CBDC to internationalize the RMB6, especially in the midst of the current US-China trade war.

Despite the Chinese central bank having not released any formal document (i.e., white paper) related to the issue of a digital currency, this report intends to summarize (1) some of the key discussions in China by different public stakeholders and (2) various publicly available information, which has been released so far.

2. Description of China’s CDBC

2.1 Overview of the BIS’s money flower

The Bank for International Settlements (BIS), in its recent research paper related to central bank digital currencies, defined a model to characterize different types of digital money.

This model, referred to as the “Money Flower” (see chart 1), introduces four different sub-segments, mutually non-exclusive, which define the nature of money (such as bank deposits, digital tokens and cash) along four axes:

Token-based (or not): whether transactions occur directly between the payer and the payee or if there is a need for a central intermediary (e.g., clearing authority).

Central bank issued (or not): whether it is a public legal tender or a private currency.

Digital (or not): whether it is electronic form or physical form.

Widely accessible (or restricted): whether the currency is intended for everyone’s use or for specific institutions (“).

Chart 1 - BIS’s Money Flower

Sources: Bank for International Settlements (BIS), Binance Research.

Based on the definition by the Bank for International Settlements (BIS)7, the following three areas, represented above by dark grey-shaded areas, could potentially be considered as money to be covered within the scope of the CBDC:

1. Central Bank Accounts (General Purpose): This is a "general purpose", "account-based8" variant, i.e., an account at the central bank for the general public. It is widely available and primarily targeted in retail transactions (but also available for broader use-cases).

2. Central Bank Digital Tokens (General Purpose): A "general purpose", "token-based"9 variant, i.e., a type of "digital cash" issued by the central bank for the general public. This second variant has similar availability and functions as the first one but is distributed and transferred differently than within traditional banking networks.

3. Central Bank Digital Tokens (Wholesale Only): This third type is a "wholesale", "token-based" variant, i.e., a digital token with restricted access for wholesale settlements (e.g., interbank payments, or securities settlement).

Di Gang, Deputy Director of the PBoC’s Digital Currency Research Institute, mentioned that the digital currency under development would correspond to variants 1 & 2 under IMF’s Money Flower10.

As a result, the CBDC could potentially have two core structural forms, which would both remain within the General Purpose scope. It would be both central-bank issued and widely accessible.

In the next subsections, some key features of this proposed CBDC11 are highlighted in regards to these two definitions.

2.2 Operational structure

This subsection addresses some key elements about the issuance and redemption processes for the CBDC and the operating structure of the network.

2.2.1 Centralized issuance & management by the PBoC

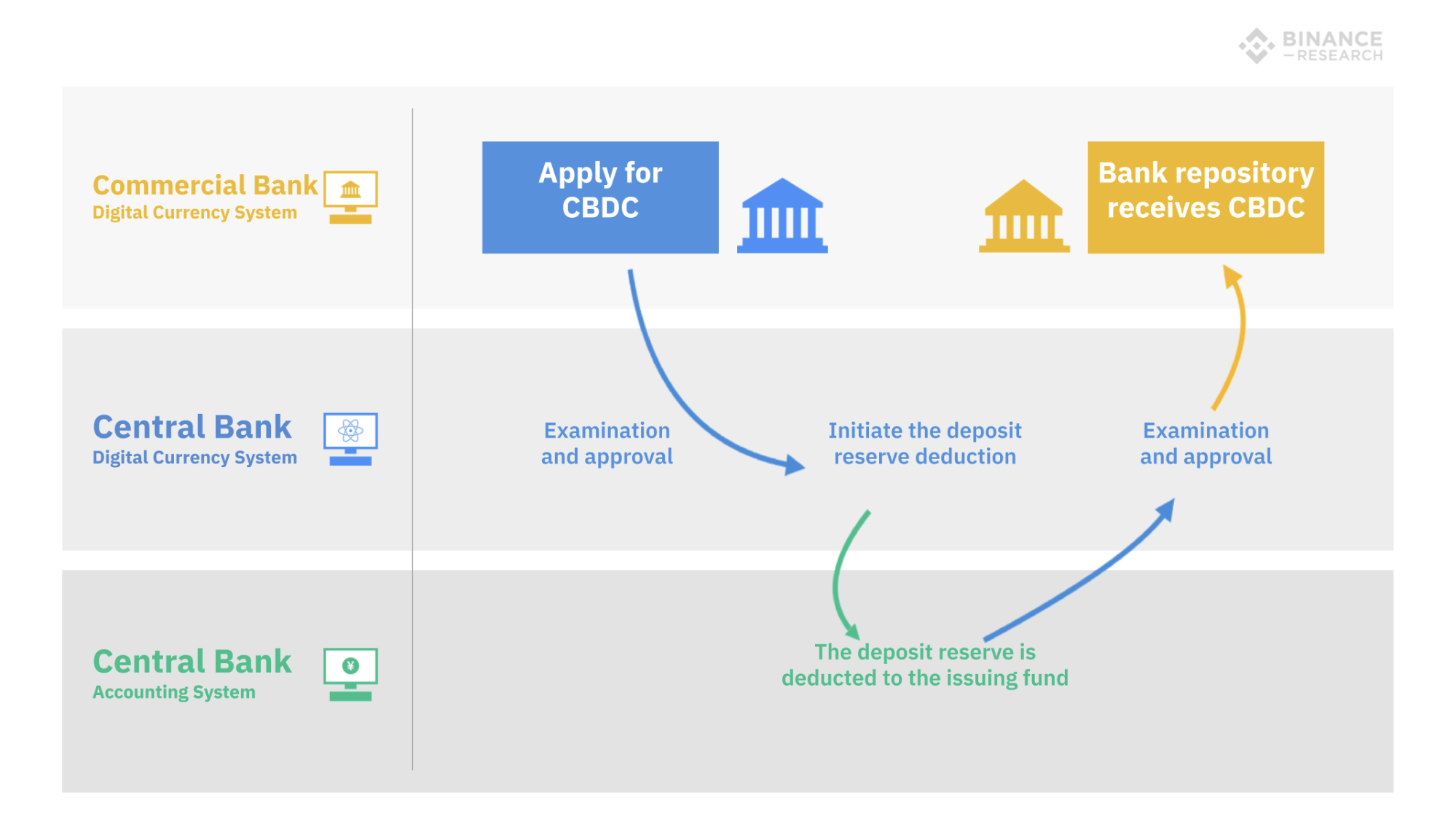

To ensure monetary sovereignty and effective transmission of monetary policy, the CBDC would be issued solely by the central bank, which will give the CBDC ultimately legal status as tender12. Unlike Libra or most cryptocurrencies, which are governed by distributed committees, the People’s Bank of China would have absolute control over its digital currency

Chart 2 - Issuance Process of PBoC’s CBDC

Sources: Digital Currency Research Institute of PBoC, Binance Research.

2.2.2 Two-tier operating structure

As discussed in the previous section (2.1), the CBDC would fall within two sub-segments of the BIS’ money flower as illustrated by its two-tier operational structure described in chart 3 below.

Chart 3 - Two-tier Prototype Operating System of PBoC’s CBDC

Sources: Digital Currency Research Institute of PBoC, Binance Research.

China’s CBDC is expected to be powered by a two-tier operating structure, represented by two distinct layers:

First layer: the first layer features direct interaction between commercial banks and the People’s Bank of China (PBoC). Namely, the PBoC would issue and redeem its CBDC only via commercial banks. Some of the expected institutions13 would include five commercial banks: China Construction Bank, the Industrial and Commercial Bank of China, the Bank of China, the Agricultural Bank of China. Interestingly, other partners would include Union Pay (Chinese banking association) and online payment service providers like Alibaba and Tencent.

Second layer: the Chinese CDBC would also be token-based (referring to the central grey part in the BIS’ money flower). Financial institutions like commercial banks, would also be responsible for distributing CBDCs to the general public as well as businesses, which would then circulate the CBDC. From the perspective of both individuals and businesses, the deposit and withdrawal processes would occur in a similar fashion as a normal interaction with their domestic commercial banks.

By adopting the two-tier system on its digital currency, the People’s Bank of China would achieve its goal of replacing paper money without subverting the existing monetary issuance and circulation system, which is also two-tier based (i.e., commercial banks are required to maintain capital above the required minimum reserve ratio at the PBoC).

The next subsection discusses the financial blueprint of this digital currency issued by the Chinese central bank.

2.3 Financial characteristics

This subsection focuses on the purpose of the CBDC initiative from the People’s Bank of China, the 1:1 pegging mechanism of the digital currency, and its interest-bearing characteristics.

2.3.1 China’s CBDC as a replacement for cash (M0 money supply14)

The People’s Bank of China plans to replace China’s M0 money supply with its CBDC. Several potential improvement areas were discussed as reasons to justify this move:

Retail payments: as it shares main properties and features of cash, China’s CBDC would meet both the needs of portability and anonymity (i.e., according to the PBoC).

Interbank clearing: a distributed inter-bank ledger system would make clearing more efficient for institutions.

Cross-border payments: the CBDC would enable increased speed and lower costs for cross-border payment, ultimately promoting the internationalization of the renminbi.

The PBoC also believes that the parts of the M1 & M2, which differ from the M0 money supply, have already been digitized. Hence, there would be no need to digitize these parts of the money supply again.

Other reasons to justify the adoption of the CBDC are:

Lower operating costs: in the existing cash-based system, issuance, operation and maintenance costs of paper currency and coins are relatively much higher.

Improved anti-money laundering policies and reduced illicit uses: as cash remains the easiest method to engage in illicit activities, the use of digital money could potentially lead to lower risks and threats from illicit activities. In particular, Mr. Mu (the Deputy Director of the PBOC’s Payment and Settlement Department) stated that paper money’s risk to be “used for money laundering and other illegal and criminal activities" was high.

In short, the PBoC considers, by design, China’s CBDC to be an upgraded version of the existing M0 supply with greater functionalities and increased opportunities to foster anti-money laundering and to monitor for potential illicit usages.

2.3.2 Full-reserve system

Instead of a "fractional-reserve" system used in the traditional banking system, the Chinese CBDC would require financial institutions to maintain a 100% reserve ratio15. As a result, the CBDC would not have any derivative deposit or money multipliers. As discussed in subsection 2.2 of this report, China’s CBDC would act solely as an intermediary between (1) commercial banks and the People’s Bank of China and (2) between commercial banks and businesses & individuals.

As China’s CBDC aims to replace M0, this digital currency would not be over-issued and follow the exact existing issuance process as cash with commercial banks required to maintain overnight collateral above the required reserve ratio requirements.

Hence, the existing monetary policy tools would not be challenged and this digital currency would not likely have any negative impact on the existing monetary policy run by the PBoC. Conversely, this CBDC might lead to a greater presence of central bank in China's overall financial system, hence leading to greater contribution of the PBoC in its role of allocating resources in the economy16.

2.3.3 Interest-bearing characteristics: no interest payments

As the Chinese CBDC targets to be a substitute for China’s M0 supply, CBDC-holders would not receive any interest from the central bank if it is not parked in any financial institutions. In this way, China’s CBDCs would not compete with commercial bank deposits, and would not have a noticeable impact on the existing economy in this regard.

Besides paper cash, the most liquid and least risky asset for retail users are bank deposits. Therefore, if China’s CBDC were to pay interest, it would raise additional issues, ranging beyond monetary transmission and implementation functions as the PBoC would compete against commercial banks. It would result in greater risk on the overall stability of China’s financial system17 since CBDCs would be less risky and more liquid than bank deposits as a cash-like asset.

2.4 Technical features

This subsection discusses in-depth some of the technical features, inferred from the early design proposals and research documents from the PBoC and other related research institutions.

2.4.1 Manageable anonymity mechanism

China’s CBDC will adopt a "loosely-coupled" design, allowing fund transfers without a bank account. Unlike "tight coupling18", the Chinese CBDC would be transferable between two parties, without the need for a bank account, unlike how traditional payments or fund transfers work in most countries19.

The end goal for the CBDC20 is to display a turnover rate as high as cash, while achieving “manageable anonymity”. In other words, in the first-layer network of the CBDC, real-name institutions are expected to be registered while the transfer in the second-layer network would be anonymous from the perspective of users. Officials from the PBoC believe that this would benefit “both the RMB’s circulation and internationalization”21.

2.4.2 The use of encryption algorithms

China’s CBDC would be stored in digital wallets in the form of digital ledgers verified by cryptography and consensus algorithms.

In Mr. Yao's 2018 paper22, private cryptocurrencies are criticized as displaying not enough information to express the real attributes of a currency. As a result, some of the missing elements have been added into China’s CBDC publicly-released design attributes.

Specifically, the proposed model of the prototyped CBDC is expressed as:

This attribute set includes the following information:= the user id, = amount of the money, = owner’s information, = the issuer’s information, = extendable, scalable attribute set. The basic process would be encrypt the information metadata, then perform a signature operation, and then receive the encrypted string for the CBDC output.

Regarding wallets, there is very little information about how digital wallets would operate. However, China’s CBDC is likely to be accessible on mobile devices, personal computers or physical IC cards, depending on what specific currency networks the Chinese CBDC would run on.

2.4.3 No preset technical roadmap, blockchain is an option

As mentioned above, the operational system of China's CDBC is a two-tier system, with the first layer of the network being a centralized distributed ledger .

However, it remains uncertain whether the second layer would also be based on a blockchain network. As the second layer management would be delegated to financial institutions, the Chinese CBDC could potentially run on multiple different networks at the same time.23

Undeniably, the two-layer network supporting the CBDC targets to achieve transaction performance of "at least 300,000 transactions per second"24. As of today, blockchains do not achieve performances as high as the target requirement. However, this transaction speed could potentially be achieved with the "off-chain relay, on-chain settlement" mechanism or through other scaling improvements such as sharding or side-chains.

2.4.4 Smart contract availability

The People’s Bank of China suggested that its CBDC could function with smart contracts, but would not run on contracts that provide functionality beyond that of “basic monetary requirements”. This is due to concerns that it may add additional value to the CBDC and “downgrade” this CBDC into some kind of security, consequently reducing its stability and usability, and adversely affecting the internationalization of the renminbi (RMB).

However, the definition of "basic monetary requirements” has not been disclosed yet, and little information has been provided by the central bank so far. Yao Qian, former head of PBoC's Digital Currency Research Department, in his 2017 paper25, emphasized that the central bank's digital currency should be programmable and extensible. In addition, if the digital currency also included automated and reliable execution thanks to smart contracts, which could pave “a new direction for the development of the legal digital currency”.

Yao Qian also mentioned that in a simulation test of a trading platform with blockchain based digital notes, the introduction of smart contracts for liquidity management “greatly improved” trading efficiency.

2.4.5 “One coin, two repositories and three centers”

Yao Qian, the former head of PBoC’s Digital Currency Research Institute, described in his 2018 paper that this central bank digital currency would be built on the following "one coin, two repositories, and three centers" approach. Specifically, there are several elements that need to be considered:

"One coin" refers to the Chinese CBDC itself: an encrypted digital string representing a specific amount guaranteed and signed by the PBoC.

“Two repositories" refer to the central bank's issuance database and the commercial bank's database, as well as the digital currency wallets used by individuals or organizations.

“Three centers" refer to authentication, registration, and big data analysis centers. An overview of these centers are as follows:

Authentication center: the PBoC would implement centralized management of financial institutions and end-user identity information26, which is the basic component of system security and an important module of the controllable anonymity design. However, in the early stages of the system, the PBoC may only authenticate and manage the identity of financial institutions. In the future, authentication support for end-users may be built based on technologies such as IBC (identification-based cryptography).

Registration center: it would record the identity of each unit of China’s CBDC and corresponding users, and complete the registration of China’s CBDC for the following functions: issuance, transfer and redemption.

Big data analysis center: it would serve several functions such as: preventing anti-money laundering, analyzing payment behavior analysis, monitoring real-time regulatory indicators, etc.

Chart 4 - Structure of the prototype system of PBoC’s CBDC

Sources: Digital Currency Research Institute of PBoC, Binance Research

2.4.6 Privacy and anonymity

The "three centers" are designed to guarantee that Chinese CBDC's transactions are anonymous from the user perspective, while also preventing money laundering, terrorist financing, and tax evasion.

Mu Changchu, the deputy director of the PBOC’s Payment and Settlement Department, in his speech on August 10th, stated that China’s CBDC aims to "strike a balance" between anonymity and the AML/CFT/ATA work”. China’s CBDC is less likely to be an instrument of illegal activities even if it were anonymous like cash, as both the PBoC and financial institutions on the second layer would have the ability to immediately freeze any CBDC or accounts if they were involved in suspicious transactions, helping deter illicit activity on the network.

According to Yao Qian's 2018 version of the prototype system, China's CBDC expression contains a user id and the owner information, and according to his description, every time a CBDC is transacted, it will generate a new CBDC string which includes the new owner’s identity.

Even if transactions would be anonymous at the user level, it would still remain possible to retrieve the entire history of transfers of each individual CBDC unit, hence providing it a variable fungibility status. It would be more fungible than most cryptocurrencies, like Ethereum and Bitcoin, at the user level as transaction history would not be retrievable.

However, unlike privacy coins, central authorities would be able to gather information. Eventually, identities would likely be tied to respective individual wallets, hence making it fully non-anonymous, unlike Bitcoin27.

3. Conclusion

The Chinese Central Bank Digital Currency (CBDC) is a proposed digital legal tender centrally issued by the People's Bank of China (PBoC), backed 1:1 by fiat reserves. It aims at replacing the M0 supply, through the digitization of cash and hence, would also rely on the credibility of the central bank. Some of its core features relate to manageable anonymity and encryption along with China’s CBDC not necessarily requiring a bank account (but may require KYC) to use the currency.

Built on a two-tier system, the Chinese CBDC would be distributed through two distinct layers: (1) between the central bank & commercial banks and (2) between commercial banks and individuals & businesses. While the first layer is to run on a permissioned blockchain system, it is not yet clear what technology will be used on the second layer network.

From the perspective of the People’s Bank of China, this digital currency would bring multiple benefits such as:

Ability to calculate more accurately some metrics such as inflation rate, and other macroeconomic figures

Increased possibilities to collect real-time data such as creation, bookkeeping and circulation of money, providing useful reference for monetary policy makers.

Help to prevent money laundering, terrorist financing, and tax evasion through the use of its Big Data Center.

Lower information asymmetries between financial institutions and regulators.

As a whole, the People’s Bank of China could potentially be more informed to conduct any monetary policy while gaining more comprehensive control over the entire spectrum of socio-economic activities.

Whereas this report intended to only describe expected characteristics of China’s Central Bank Digital Currency through a cryptocurrency research lens, this proposed digital currency system will not be a direct competitor of existing cryptocurrencies like Bitcoin or Monero.

Furthermore, compared to decentralized cryptocurrencies, a highly centralized one could negatively impact financial privacy for all individuals. Several pending questions remain such as the requirement to open wallets, whether a third party could freeze assets and under what specific circumstances.

Despite one of the end-goals from this digital currency initiative being to further internationalize the renminbi, it remains to be seen what legislation would apply on cross-border payments. Furthermore, it is unclear whether that individuals, based outside of China, would rely on the Chinese central bank to both maintain a consistent monetary policy and to protect their financial privacy.

References

BIS. Central bank digital currencies (March 2018). https://www.bis.org/cpmi/publ/d174.pdf

Coindesk. China Should Prepare Digital Yuan to Counter Facebook Libra: Ex-PBoC Chief (July 2019).https://www.coindesk.com/china-should-prepare-digital-yuan-to-counter-facebooks-libra-ex-pboc-chief

Di Gang (Deputy Director of PBoC’s Digital Currency Research Institute). Digital currency discrimination (September 2018). https://www.chainnews.com/articles/176343895374.htm

Fan Yifei (Deputy Governor of PBoC). Considerations on Central Bank Digital currency (January 2018)http://www.yicai.com/news/5395409.html

Mu Changchun (Deputy Director of PBoC’s Payment and Settlement Department). The Practice of Central Bank Legal Digital Currency (August 2019).https://www.chainnews.com/articles/761536251153.htm

Reuters. China's sovereign digital currency is 'almost ready': PBOC official (August 2019).https://www.reuters.com/article/us-china-cryptocurrency-cenbank/chinas-sovereign-digital-currency-is-almost-ready-pboc-official-idUSKCN1V20RD

Wang Xin (Head of PBoC’s Research Bureau). Strengthening the Confidence of Monetary Culture and Deepening the Research and Development of Central Bank Digital Currency (December 2018).http://kns.cnki.net//KXReader/Detail?TIMESTAMP=637013063616113750&DBCODE=CJFD&TABLEName=CJFDLAST2019&FileName=JRKJ201812008&RESULT=1&SIGN=juULi6RKxHMmYr1VuV%2fNPhEbf5Y%3d

Wang Yongli (former Deputy Governor of PBoC). What is the Essence of Currency? (June 2019).http://finance.sina.com.cn/zl/bank/2019-06-04/zl-ihvhiews6790929.shtml

Yao Qian (former head of PBoC’s Digital Currency Research Institute). Theoretical Logics and Technical Structure of CBDC (August 2017) (in Chinese)_

Yao Qian (former head of PBoC’s Digital Currency Research Institute). Experimental Research on Prototype System of Central Bank Digital Currency (June 2018) http://kns.cnki.net/kcms/detail/detail.aspx?filename=RJXB201809013&dbcode=CJFQ&dbname=CJFDLAST2018&v=

Yao Qian (General Manager of the China Securities Depository and Clearing Corporation). Economic Effect Analysis of Legal Digital Currency: Theory and Empirical Study (January 2019)http://kns.cnki.net/KCMS/detail/detail.aspx?dbcode=CJFQ&dbname=CJFDLAST2019& filename=GJJR201901012&v=MTIwMDBJaWZCZkxHNEg5ak1ybzlFWm9SOGVYMUx1eFlTN0RoMVQzcVRyV00xRnJDVVJMT2ZiK2RzRnl6a1Zyek8=

The People's Bank of China (PBoC) is China’s central bank. Throughout this report, it will be referred to the Chinese central bank, PBoC and the People’s Bank of China.↩

https://www.coindesk.com/chinas-central-bank-close-to-launching-official-digital-currency↩

https://www.coindesk.com/china-should-prepare-digital-yuan-to-counter-facebooks-libra-ex-pboc-chief↩

https://www.reuters.com/article/us-china-cryptocurrency-cenbank/chinas-sovereign-digital-currency-is-almost-ready-pboc-official-idUSKCN1V20RD↩

“法定数字货币” in Chinese↩

https://finance.sina.com.cn/blockchain/coin/2019-08-12/doc-ihytcitm8648461.shtml ↩

In account-based systems, the identity of each account holder is verified by the financial institutions, when money is exchanged. Hence, the verification work relies on the ability of these institutions to carry the burden and costs to do so.↩

Token-based money (or payment systems) rely on the ability of the payee to verify the validity of the payment object. With cash the worry is counterfeiting, while in the digital world the worry is whether the token or “coin” is genuine or not (electronic counterfeiting) and whether it has already been spent. (BIS)↩

PBoC also uses DC/EP (Digital Currency/Electronic Payment) to call its digital currency, but in keeping with general understanding, this report uses CBDC to refers to the Central Bank's Digital Currency.↩

Means the money can be paid in the discharge of a debt of any amount, legal action can be taken against a person who refuses to accept this money.↩

Reported by Forbes on August 27th 2019. There has been no official confirmation from the PBoC as of release. https://www.forbes.com/sites/michaeldelcastillo/2019/08/27/alibaba-tencent-five-others-to-recieve-first-chinese-government-cryptocurrency/↩

Notes and coins in circulation (outside the central bank and the vaults of depository institutions)↩

China’s required reserve ratio is at 11 % as of August 15th 2019.↩

This is discussed in the report “Central bank digital currencies” released in March 2018 by the BIS.↩

Wang Xin, head of the People's Bank of China's Research Bureau, mentioned in an earlier speech that the CBDC could be a floor for deposit rates. However, in his latest speech, Mu Changchun, the Deputy Director of the PBOC’s Payment and Settlement Department, made it clear that CBDC would not pay any interest.↩

Tight coupling refers to a system of components which are highly dependent on one another. Its opposite is loose coupling.↩

The most similar existing example is the transfer of digital money between two WeChat accounts.↩

https://www.chainnews.com/articles/761536251153.htm (in Chinese)↩

Both Wang Xin, Fan Yifei, Mu Changchun, Yao Qian, Zhou Xiaochuan have mentioned this on various occasions.↩

http://kns.cnki.net/kcms/detail/detail.aspx?filename=RJXB201809013&dbcode=CJFQ&dbname=CJFDLAST2018&v= ↩

Yao Qian, former head of PBoC's digital currency research department, in his 2018 paper, the prototype system he proposed was "a distributed ledger system jointly established by the central bank and commercial banks".↩

From Mu Changchun, the deputy director of the PBOC’s Payment and Settlement Department.↩

The commercial banks will be the first to record the end-user's identity, but as Fan Yifei, the deputy governor of PBoC, stated that the central bank's database will also kept all user's information, for lower the pressure of commercial banks' system, the synchronization of data could be done in an asynchronous way.↩

For instance, Bitcoin is pseudo-anonymous as a user identity can only be revealed at the fiat gateway level or if someone associates publicly to his wallet address.↩