As USD-backed stablecoins continue to see increased adoption and trading pair usage, their volume dominance over BTC-denominated pairs is higher than ever. However, from a trading environment perspective, there are few differentiations amongst the mid-cap stablecoins (i.e., PAX, TUSD and USDC).

The first four months of 2019 led to net inflows for most stablecoins; January saw the largest inflows, but the subsequent three months had more redemptions than deposits. Bucking this trend, PAX and USDC exhibited strong inflows of over USD 40 million respectively towards the end of April, potentially owing to the recent Tether turmoil.

Irrespective of its recent breaking of its dollar peg, Tether (USDT)’s use is continuing to shift from the Omni blockchain to other public chains like Ethereum and Tron. Meanwhile, Paxos (PAX) will soon be rolled out on the Ontology blockchain.

Furthermore, the expansion of non-USD stablecoins, illustrated by Trust Token’s new offerings (HKD, AUD, CAD, GBP, EUR), may lead to several key developments:

Additional channels for global remittance

Easier to hedge against fiat currency risk

Greater price efficiency for non-USD cryptocurrency exchanges

The development of blockchain FX exchanges, either on or off-chain

Eventually, stablecoin initiatives from various non-financial companies, i.e., Facebook and Samsung, might further the growth of the digital asset industry by introducing cryptocurrencies and blockchain technology to their large existing user bases.

The large majority of collateralized stablecoins are USD-pegged. However, many stablecoin-related projects are now rolling out additional products and services that may expand the use cases and reach of these coins beyond USD barriers. In this report, we examine the current state of stablecoin popularity, and what might be next on the stablecoin horizon.

1. Ever-increasing popularity in USD-collateralized stablecoins

1.1 Year-on-year volume breakdown comparison on Binance

Chart 1 - Comparison of 24h quote Asset volume between May 1st 2018 and May 1st 2019 on Binance

As discussed in our previous report about crypto-correlations, stablecoins are continually growing in popularity. Quote asset volumes driven by stablecoins on Binance (denoted as USD(S) in the figure above) have grown from just over one-third of all volume (35.78%) one year ago to over three-fifths (60.55% as of May 1st, 2019), eating into the market share of both BTC-denominated and ETH-denominated pairs. Interestingly, the share of volume in BNB pairs also doubled during the same time period.

1.2 Stablecoin pair additions on Binance over first 4 months of 2019

Part of the increase in volume from stablecoins can be attributed to the introduction of several stablecoin pairs with new quote assets and base assets.

Table 1 - Addition of new stablecoin pairs on Binance for existing assets over the first four months of 2019

Quote Asset | USDT | PAX | TUSD | USDC | USDS |

|---|---|---|---|---|---|

New Base Asset | WAVES, HOT, ZIL, ZRX, BAT, XMR, ZEC, IOST, DASH, OMG, THETA, ENJ, MITH, USDS | WAVES, BCHABC, LTC, NEO, BTT, ZEC, ADA, USDS | WAVES, BCHABC, LTC, BTT, ZEC, ADA, USDS | WAVES, BCHABC, NEO, LTC, BTT, ZEC, ADA, USDS | BTC, BNB |

excluding new base asset listings (e.g., initial pairs offered for BTT or FET)

Large cryptoassets such as NEO, Litecoin (LTC), Cardano (ADA) or Bitcoin Cash (BCHABC) received additional trading pairs against PAX, TUSD and USDC, complementing the previous addition of USDT pairs. On top of this, a dozen of large assets were listed against USDT which is expected to further reduce the percentage of the cryptoasset total trading activity from BTC pairs to stablecoin pairs.

1.3 Net inflows: more deposits than redemptions over the first four months of 2019

Table 2 - 2019 first 4-month redemptions & deposits for main USD-backed stablecoins

USDT1 | PAX | TUSD | USDC | USDS | GUSD | |

|---|---|---|---|---|---|---|

Redemptions | - | (155,469,012) | (67,750,435) | (395,289,454) | (3,014,519) | (97,462,832) |

Deposits | - | 173,879,681 | 70,800,456 | 437,262,481 | 7,215,884 | 54,299,444 |

Net inflows (outflows) | 975,370,119 | 18,410,669 | 3,050,021 | 41,973,026 | 4,201,365 | (43,163,389) |

Market Cap as of April 30th 2019 | 2,888,440,781 | 160,737,039 | 208,021,789 | 293,184,174 | 5,635,840 | 47,831,688 |

% Relative to initial Market Cap | +51,0 % | +12.9% | +1.5% | +16.7% | +292.9% | -47.4% |

Once again, USD Tether (USDT) saw the largest net inflow, with a total increase slightly below $1bn USD. Though Tether’s market cap is much bigger than the cumulative market capitalization of all five other stablecoins discussed in the table above, these inflows still represent an increase of around 50% of Tether's total supply, particularly notable in a period of turmoil for the company.

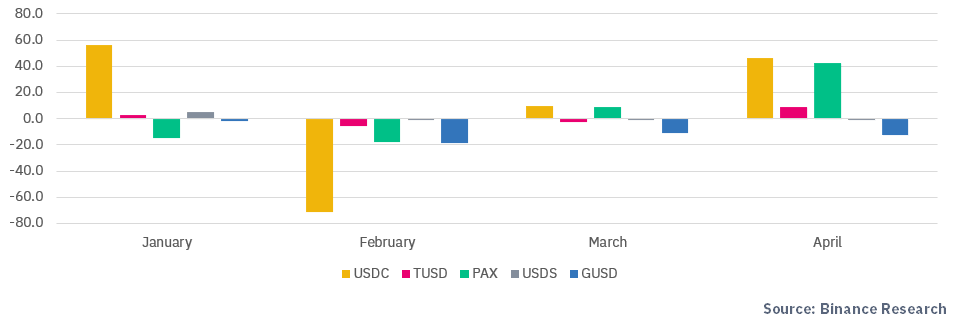

Chart 2 - Evolution of total monthly net inflows (USD million) in non-USDT stablecoins in 2019

Amongst the non-USDT stablecoins, USDC was the biggest gainer in circulating supply, seeing an inflow of nearly 60 million USD in January. While USDC saw the largest monthly net redemption amount in February, it rebounded with a slightly positive inflow in March. In April, both USDC and PAX saw minting of over 40 million tokens. Notably, GUSD was the only stablecoin not to have an inflow in any of the four months, displaying a continual net redemption trend. As a result, owing to its small market cap, Gemini Dollar lost nearly half of its market capitalization in the first four months of 2019.

2. Trading environment overview

2.1 Untethered stablecoins have small differences

We selected BTC, being the largest digital asset in the world by market capitalization, to act as the base currency for comparing the liquidity of each stablecoin on Binance: Tether (USDT), Paxos (PAX), TrueUSD (TUSD), USD Coin (USDC), and StableUSD(USDS).

Table 3 - Statistics about stablecoin trading pairs on Binance (over April 2019)

Average Spread (%) | Median Spread (%) | 95-pctile Spread (%) | 5-pctile Spread (%) | Average time between 2 fills | |

|---|---|---|---|---|---|

BTCUSDT | 0.02 | 0.02 | 0.05 | Inferior to 0.01 | 00:00.3 |

BTCPAX | 0.08 | 0.08 | 0.17 | 0.02 | 00:05.2 |

BTCTUSD | 0.11 | 0.1 | 0.21 | 0.03 | 00:08.1 |

BTCUSDC | 0.09 | 0.08 | 0.19 | 0.03 | 00:07.3 |

BTCUSDS | 0.26 | 0.23 | 0.47 | 0.13 | 02:33.1 |

Unsurprisingly, the BTC/USDT pair exhibits the lowest median and average spreads over April 2019. With USDT listed on so many other exchanges, one would expect a tight spread given the potential for cross-exchange arbitrage strategies. On top of this, the frequency of filled trades (measured by the distance in time between two consecutive trades) is extremely high for this pair, occurring at an average frequency of under 0.3 seconds.

What does this data reveal about the “untethered” trading landscape?

Paxos (PAX) and USD Coin (USDC) exhibit the lowest BTC median and average spreads, with both figures being below 0.09%. A close third is TUSD, with an average BTC spread of around 0.11% and a median spread around 0.10%. This slight gap between TUSD and PAX / USDC could be linked to the recent change of pair naming logic from “TUSD/BTC” to “BTC/TUSD” may have thrown off automated traders who failed to update the ticker accordingly.

StableUSD (USDS) lags behind the first three stablecoins, as the average time (on BTC/USDS) between two consecutives fills is above 2 minutes. The main explanation is that the supply is extremely small in comparison to the other stablecoins (around 5 million) and concentrated on a single exchange. As a result, cross-venue arbitrage opportunities are limited, ultimately resulting in lower volumes and higher spreads.

The average time between two fills is under 10 seconds for all stablecoins against BTC with the exception of StableUSD (USDS).

2.2 Tether volatility: low but recent spike in late April

Chart 3 - Kraken USDT/USD daily OHLC from January 1st 2019 to April 30th 2019

Over the past trading four months, there were three major phases & events in the price of Tether:

The price fluctuated around dollar parity (0.99-1.01) for the first three months of 2019.

Bitcoin rebounded on April 1st and USDT jumped to stabilize around 1.01.

Recent news from NY AG2 led to a large price drop in Tether with a brief bottom of 0.95 on April 26th. Since then, the price has rebounded to a median price bouncing between 0.98 and 0.99. Recent developments3 about Tether may lead to greater price volatility in the coming months. What are other expected developments in the stablecoin industry and their potential implications for the digital asset industry?

3. Axes of differentiation

3.1 Addition of new blockchains

3.1.1 Tether: OMNI is not the end-all-be-all

While Tether is “blockchain agnostic” and features an ERC-20 token, most of its supply runs on the OMNI layer, which is built on top of the Bitcoin blockchain. Recently, a partnership between Tether and Tron has made the news4, leading to potential expansion on yet another chain.

Regardless of the specific chain, the trend of Tether lessening its OMNI reliance marches on. As of April 30th, 400 million for Ethereum-based and 137 million for Tron-based tokens existed. In comparison, USD Tether running on the OMNI blockchain represents roughly 2.82 billion, or 80% of all the USDT in existence today.

Chart 4 - Breakdown of all USD Tether issued across blockchains5 as of April 30th 2019

This is expected to change, however, as large exchanges are now increasingly supporting deposits and withdrawals of Tether on alternative (i.e., non-OMNI) blockchains as illustrated below.

Table 4 - Exchanges supporting non-OMNI versions of USD Tether

Binance | Bitfinex | Huobi | OKEX | Gate.io | Poloniex | Bitfinex | Kucoin | |

|---|---|---|---|---|---|---|---|---|

Ethereum | no | yes | yes | yes | yes | yes | yes | yes |

Tron | no | yes | yes | yes | yes | yes | yes | yes |

Binance has both an ERC20 USDT and a TRC10 USDT wallet.

In contrast to USDT, EURT (EUR Tether) runs solely on the Ethereum blockchain, with a total supply slightly above EUR50 million.

Over time, the proportion of USDTs minted on Ethereum/Tron relative to total supply has grown to be much higher than before, as illustrated by the chart below from the end of 2018, when ERC-20 USDT marked just a small, small sliver of the entire USDT supply.

Chart 5 - Breakdown of all USD Tether issued across chains as of December 31st 2018

3.1.2 Ontology’s support of the PAX stablecoin

Ontology recently announced that it will partner with Paxos to issue a collateralized stablecoin based Ontology's OEP-4 token standard while keeping its existing ticker “PAX”.

For Ontology, this would allow greater participation of individuals and institutions into the Ontology decentralized ecosystem. Eventually the team would in order to make it easier to transact stable units with its technology.

For Paxos, it would enable the company to further differentiate from other stablecoin issuers such as Circle or TrustToken, and potentially to obtain a “stablecoin monopoly” for decentralized applications running on Ontology. This may be a recurring trend for many stablecoin issuers and chain pairs, leading to future pairing of specific blockchains with stablecoin issuers marking the end of blockchain agnosticism for these issuing companies.

USD 100 million worth of PAX tokens are reportedly going to be issued on the Ontology blockchain in May-June 2019. It remains to be seen which exchanges will also start accepting deposits and withdrawals of this token. However, the main goal of this partnership appeared to be aimed at in-dApp usage, rather than trading.

Chart 6 - To-be-issued Ontology-based PAX compared to existing Ethereum-based PAX (as of April 30th 2019)

3.2 Additional support of new collaterals: Trust Token’s expansion to a wide range of fiat currencies

TrustToken, the company behind TUSD, which launched in March 2018, announced consecutively in April 2019 that TrueGBP6 and TrueAUD7 tokens, along with future support of a wider range of fiat currencies, namely CAD & HKD (2019 Q2) and EUR (2019 Q3) in the roadmap.

What are the potential implications of the ever-increasing range of fiat collateralized stablecoin that are non-USD denominated?

Additional channels for global remittance: from a speed and cost perspective, these new stablecoins are likely to help transferring money worldwide, and users will continually demand a greater range of currencies beyond USD. For end users whose primary currency is not the US dollar, the currency risk will be mitigated.

Ability to hedge against fiat currency risk: fund managers or retail investors/traders, whose profit currency is not the US dollar, will be able to calculate their PnL in their local currency with the added ability to recognize their profits in a different currency with greater ease.

Greater price efficiency for non-USD fiat exchanges: new stablecoins can lead to broader opportunities for cross-exchange arbitrage, particularly between non-USD fiat exchanges. Exchanges where the primary quote currency is different from the US dollar (e.g., EUR: Kraken, Binance Jersey) could be more efficiently arbitraged with the introduction of these new stablecoins.

Creation of FX markets on the blockchain: if stablecoin providers such as TrustToken continue to develop new stablecoins that receive large subsequent inflows, it is possible that this added liquidity may ultimately result in added opportunities for more advanced exchange-related products. In particular, FX blockchain-based exchanges may be developed, where users could trade popular FX pairs such as EUR/USD or JPY/USD in a blockchain environment. These exchanges could be either:

centralized allowing the use of high leverage and margin trading.

decentralized such as an Ethereum-based DEX for stablecoins, addressing the counterparty risk problem.

3.3 Increasing participation of non-financial institutions: could Facebook Coin and Samsung Coin become future game changers?

3.3.1 Facebook Coin

Facebook is reportedly working on its own blockchain solution for a future stablecoin tentatively named “Facebook Coin” (also referred to as “Project Libra”).

This digital currency is expected to be integrated into Whatsapp, the popular messaging service previously acquired by Facebook, to allow users to transfer money to each other8.

More technical details on Project Libra are still unknown, including whether this digital currency would run on an existing blockchain or a new one built from scratch, and whether its blockchain would be public or private (such as an implementation of Quorum with the JPM Coin).

Regardless, Facebook has an entire ecosystem across its Facebook, Messenger, Whatsapp, and Instagram products that could integrate this future digital currency. With a user base in the billions, end use-cases could span from international remittances to payment for premium content (e.g., games) for individual users and services such as advertising campaigns, etc. for businesses.

The project is led by David Marcus (ex-Paypal president9) and, as noted by Barclays analyst Ross Sandler, has the potential to generate new income-generating sources for Facebook.10

Four core scenarios can be drawn for this chain/coin, based on two independent variables: whether the chain is public or private, and whether there is a central authority, a la Ripple, or not:

Private with a central authority: the blockchain would not be immutable by design (e.g., Facebook controlling the majority of the nodes) and would solely be used as an accounting system to avoid double payment issues.

Private with no central authority: the blockchain would be immutable but an insurance mechanism or a litigation system would exist to prevent fraud.

Public with a central authority: the blockchain would not be immutable but all transactions would be public.

Public with no central authority: the blockchain would be immutable with all transactions being public.

While it is difficult to predict what this project will ultimately result in, this blockchain is likely to be private (or partially private) with some degree of authority from Facebook itself. In a similar fashion to the JPM Coin, this project could constitute a stepping stone in mass-adoption for cryptocurrency and other digital assets while contributing to the “unbanking” of the payment industry.

3.3.2 Samsung Coin

On April 24th, Samsung was reportedly11 building its own blockchain on top of Ethereum. This announcement follows the hype about the Samsung Galaxy S10, the company’s flagship phone, which features an integrated Ethereum wallet, and also echoes the company’s focus on blockchain given its recent investments from the Korean company into several prominent blockchain-based companies such as Ledger12.

While “Samsung Coin” may not be a pegged currency (very few details have been provided at this stage), it remains a strong possibility that it will be a price-stable currency, as the stability would allow for easier integration across the entire ecosystem of Samsung services and devices.

Initial reports indicate that this blockchain could be a hybrid in structure, with potential private elements such as a private-public state option (similar to that to JP Morgan’s Quorum). However, the exact consensus mechanism and nature of the blockchain, i.e., “whether it would be a permissioned or permissionless network?”, remains unknown.

4.Conclusion

Unsurprisingly, collateralized stablecoins are continuing to gain popularity but major differences in stablecoins exist from a trading perspective. BTC markets are dominated by Tether with greater liquidity represented by lower spreads and higher volumes than other stablecoins.

Excluding StableUSD (USDS), all other stablecoins exhibit similar liquidity profiles but USD Coin (USDC) and Paxos (PAX) exhibited slightly lower spreads than TrueUSD (TUSD) in April 2019. Most of the stablecoins also received more deposits than withdrawals during the first four months of 2019, with recent large inflows in April for Paxos and USD Coin.

Competing for market share, these stablecoin providers are becoming increasingly innovative in their product offering:

Tether is seeing increased adoption of its Ethereum-based and Tron-based tokens.

TrustToken is planning to roll out several new stablecoins in 2019 in a wide variety of fiat currencies such as AUD, GBP, HKD and EUR.

Paxos has partnered with Ontology to expand its offerings on different blockchains, in a similar manner as Tether.

These may lead to long-term benefits such as additional channels for global remittance, greater price efficiency for non-USD cryptocurrency exchanges or the development of blockchain FX exchanges, either off or on-chain.

The digital asset industry is seeing wider interest from non-financial institutions and its future may be fueled by these large institutional players creating tradable assets running on public blockchains, hence championing the use of blockchain as the key technology for all digital wallets.

These non-financial companies (e.g., Facebook or Samsung) are likely to be less risk-averse than traditional financial companies, and have greater incentive to disrupt the payments industry, with the added ability to execute at a faster, scalable pace. As a result, these companies may help defining future key growth drivers for both the global payment and the digital asset industry.

Based on changes from the total assets displayed on the current balances from Tether’s website. Historical snapshot are saved here.↩

https://www.bloomberg.com/news/articles/2019-04-26/cryptocurrencies-lose-10-billion-on-tether-cover-up-allegations↩

https://www.bloomberg.com/news/articles/2019-04-30/tether-says-stablecoin-is-only-backed-74-by-cash-securities↩

All authorized Tethers were included. https://wallet.tether.to/transparency↩

https://www.coindesk.com/a16z-backed-trusttoken-launches-stablecoin-pegged-to-uk-pound↩

https://www.coindesk.com/trusttoken-launches-aud-backed-stablecoin-with-3-more-to-follow↩

https://www.cnbc.com/2018/12/21/facebook-reportedly-working-on-a-cryptocurrency-for-transfering-money-through-whatsapp-.html↩

https://www.bloomberg.com/news/articles/2019-05-08/facebook-s-blockchain-team-is-assembling-its-own-mini-paypal-mafia↩

https://www.cnbc.com/2019/03/11/facebooks-cryptocurrency-could-be-a-19b-revenue-opportunity-barclays-says.html↩

https://cointelegraph.com/news/report-samsung-planning-new-blockchain-mainnet-featuring-samsung-coin↩