Original title: Our Stride Thesis

Original author: James Ho, Partner at Modular Capital

Original translation: 1912212.eth, Foresight News

Editor's note: On February 2 this year, Stride, a Cosmos ecosystem liquidity pledge protocol, completed a $4 million strategic financing, led by DBA, with participation from 1confirmation, Road Capital, Modular Capital, Imperator, Chorus One, etc. This round of financing aims to promote the development of Stride in the Celestia ecosystem. It is worth mentioning that on the same day, Stride's total TVL exceeded $100 million, setting a record high.

text:

Stride is a Cosmos ecosystem staking protocol that currently accounts for more than 90% of the market share and has a TVL of over $60 million. It supports Cosmos chains, including ATOM (Cosmos Hub), OSMO (Osmosis), INJ (Injective), JUNO (Juno), etc.

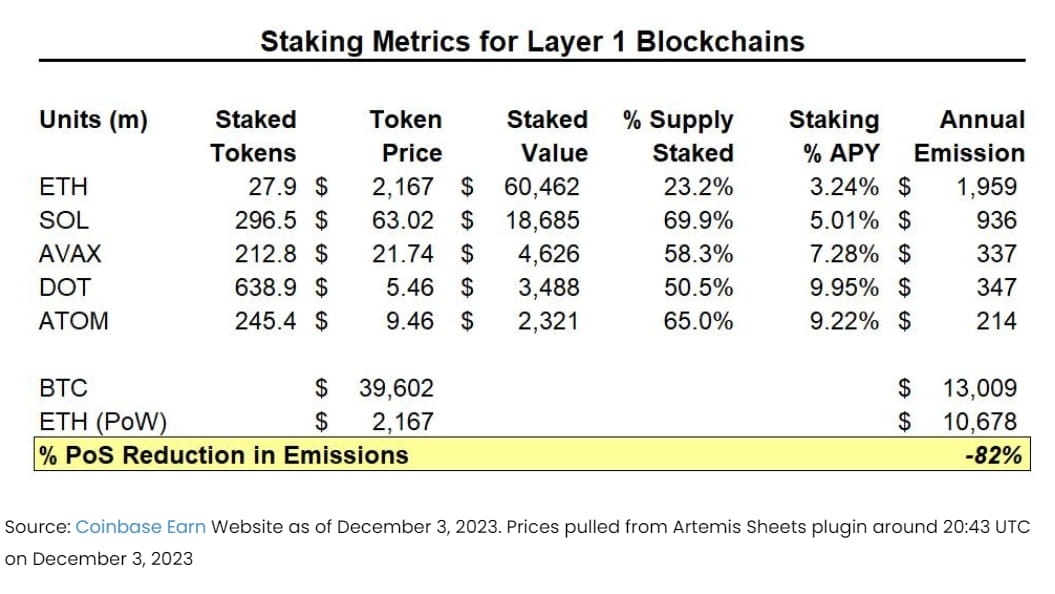

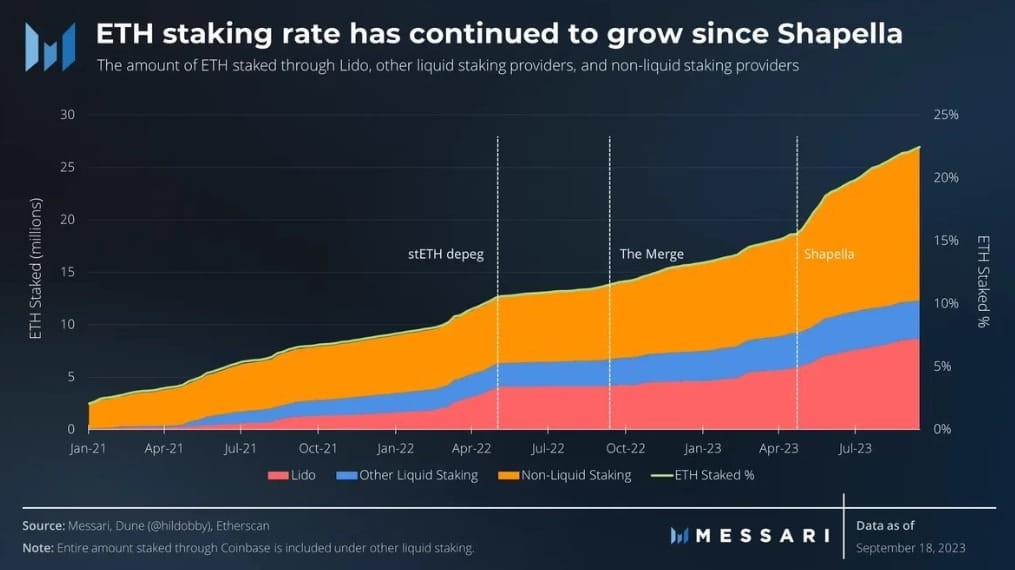

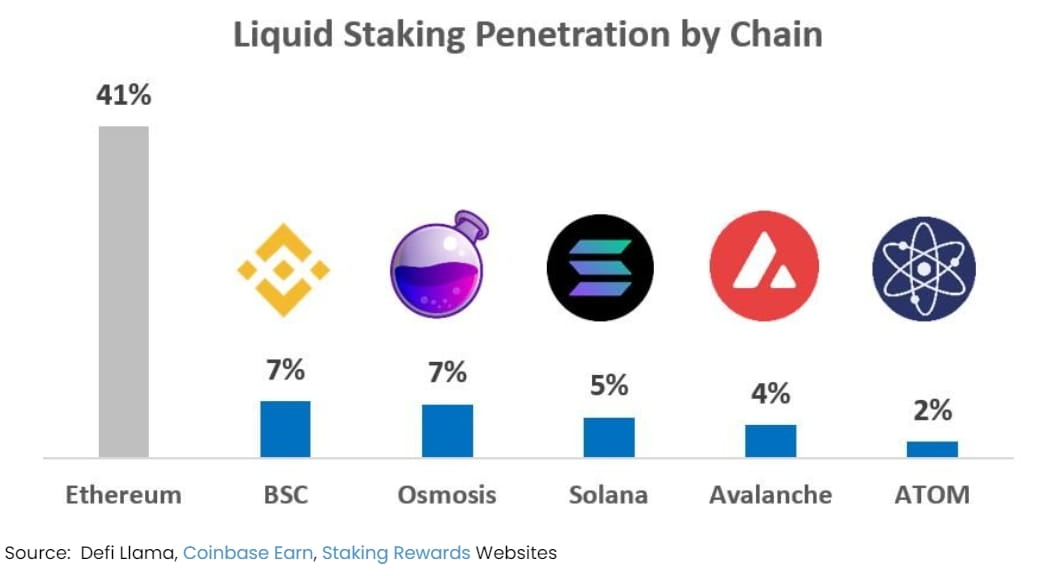

Staking is still in its early stages in the Cosmos ecosystem. 41% of ETH staked on Ethereum is done through staking service providers (Lido, Rocketpool, Frax, Coinbase, etc.). In contrast, only 2% of the total ATOM and 7% of the total OSMO are staked, which provides a broad opportunity for further development.

Liquidity Staking Tokens (LST) are very attractive to users because they can improve the capital efficiency of collateralized assets. By issuing collateralized tokens (stOSMO, stATOM), Stride allows users to use assets freely in DeFi while earning staking returns. In addition, most Cosmos chain collateralized assets have a 14-30 day redemption period, and users need to wait a long time to release the collateral. In Stride, LST allows users to sell their collateralized tokens immediately under certain market slippage.

Liquidity staking as a category has strong network effects and tends to be a winner-take-all situation. Due to Lido's deep liquidity for its stETH, Lido's share of LSTs on Ethereum is close to 80%, which in turn makes more users prefer to use Lido instead of competitors. Given Stride's 90% share of the Cosmos ecosystem and growing, we expect similar network effects to play out in Stride.

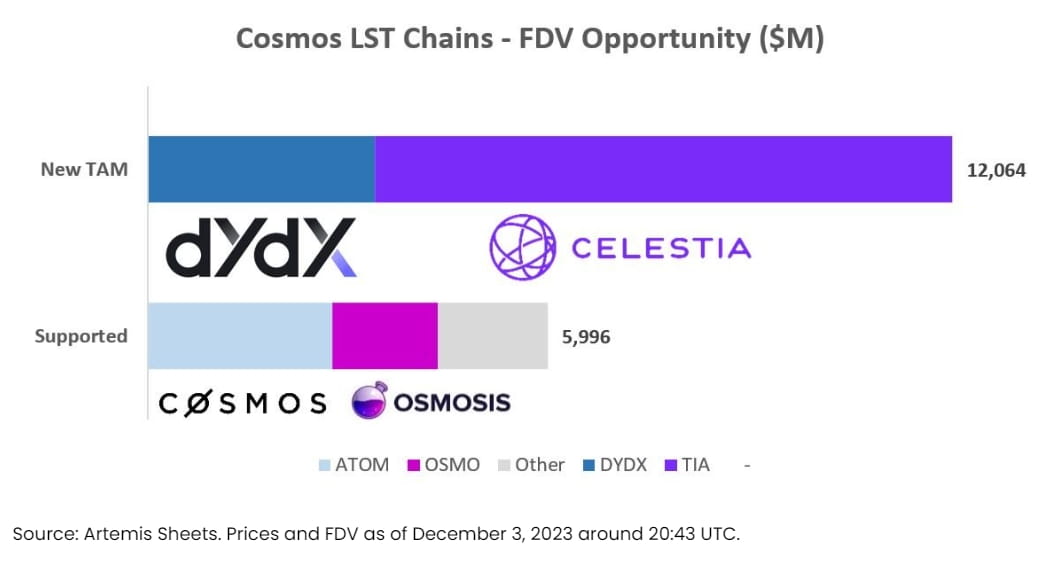

Stride intends to support liquidity staking pairs for new Cosmos chains such as Celestia (TIA) and dYdX (Editor's note: TIA and DYDX are now supported). The total market value of these chains combined exceeds $10 billion, which greatly expands Stride's market size in the Cosmos ecosystem.

As the Cosmos ecosystem market capitalization increases to $20-50 billion (currently $5-6 billion), Stride could generate $20-70 million in fee revenue. Assuming 15-30% staking penetration, and Stride continuing to maintain a 90% market share. Applying a 50x to this number, Stride could reach a market cap of $1-3 billion+.

PoS

Proof of Stake (PoS) is a consensus mechanism used to determine how transactions are processed and new blocks are created. Ethereum has historically used Proof of Work (PoW) to ensure the security of its chain, in which miners guess a random encrypted hexadecimal number by using computing resources such as GPUs and electricity. This is also the security model currently used by Bitcoin.

After years of planning, Ethereum completed the merger in September 2022, switching from PoW to PoS. There are many reasons why most public chains switch from PoW to PoS security and anti-sybil attack models, including:

Energy consumption: PoW ensures security by consuming real-world resources (computing resources and electricity). PoS, on the other hand, ensures security through the value of native network assets (ETH, SOL, AVAX, ATOM). This reduces the energy consumption of PoS networks by 99.9% compared to PoW networks.

· Network Consensus: PoW is secured through economic incentives. The network issues new tokens and rewards them to miners in exchange for consuming real-world resources (which cost money to buy). However, miners often immediately sell the newly issued tokens (e.g. BTC) to recover the costs of operating mining facilities. In PoS, the network is secured by the owners (those who hold and purchase the native network tokens). The idea is that this creates consistency among network owners, who are incentivized to ensure the security of the network.

· Emission reduction: Under a PoW network, $1 of emissions must be spent to gain $1 of security (in the form of real-world spending). This requires the network to have a significant amount of new issuance on an ongoing basis. Under PoS, stakers do not have large real-world spending, instead they only need a certain percentage of issuance (usually in the range of 3-10%) to compensate for the illiquidity of their staked assets. This means that the network spends $0.03-0.10 for $1 of economic security, which is a more economically sustainable long-term model. Ethereum has reduced the number of tokens issued each year to secure its network after transitioning to PoS by more than 80%.

Currently, almost all major public chains calculated by TVL use PoS to ensure their network security, including Ethereum, Solana, Avalanche, Polkadot, and Cosmos Hub.

Liquidity pledge concept

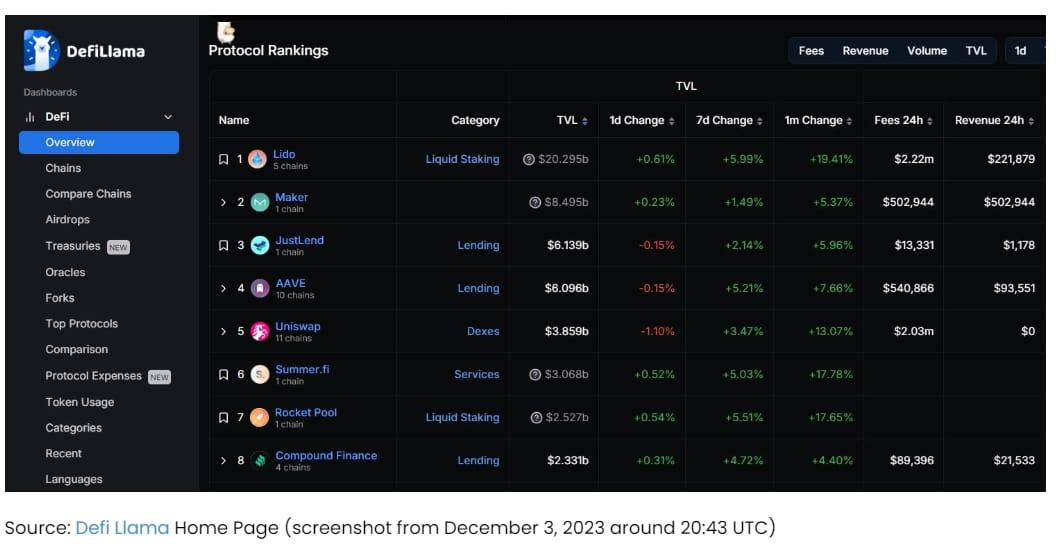

Liquidity staking is a very large category in the DeFi space, and the biggest success story is Lido. Lido has now become the number one protocol in the entire cryptocurrency space, with a total locked value (TVL) of over $20 billion, accounting for nearly a third of all staked Ethereum. Lido earns over $80 million in fees per year.

In simple terms, Lido places ETH into a smart contract and then distributes that ETH to a group of node operators to stake on behalf of the protocol. These node operators include Figment, Stakefish, Everstake, and Blockdaemon.

After users deposit ETH into the Lido protocol, they will receive stETH. stETH represents the ETH that users stake in the Lido protocol, including the value of the initial deposit and ongoing staking rewards. stETH has the following uses:

Lending: Users can deposit stETH into lending protocols like Aave if they want to use it as collateral to borrow assets such as the USDC stablecoin.

AMM liquidity: If users want to provide liquidity and earn fees, they can deposit stETH into trading protocols such as Uniswap, Curve, etc. Curve's wstETH/ETH pool earns 2% in fees per year, which is in addition to the 3-4% ETH staking income on Lido.

Yield hedging: Users can deposit stETH into Pendle (a yield DeFi native tool) to lock in their staking yield for a period of time.

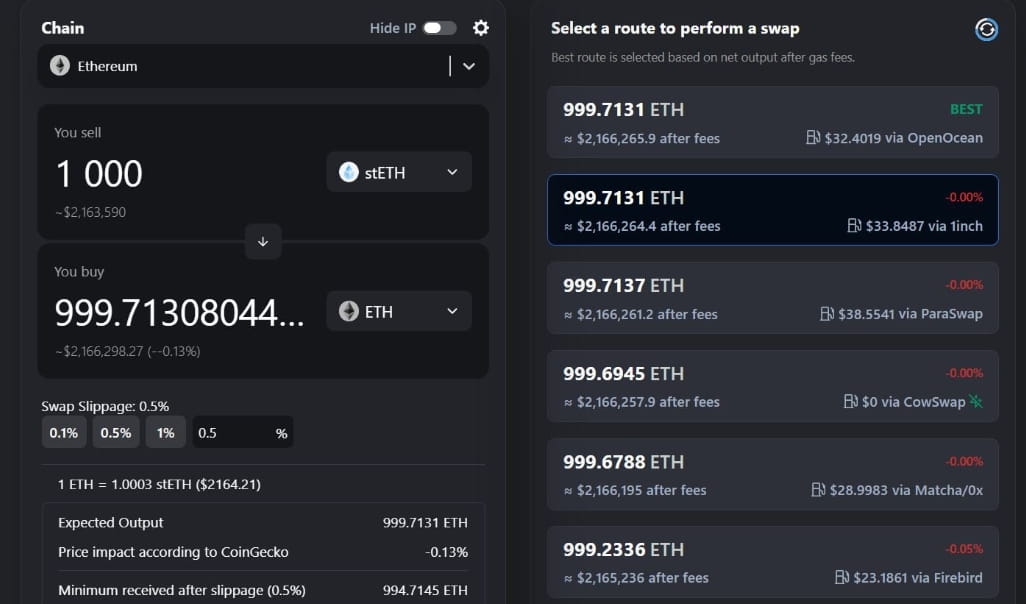

Sell on the open market: Usually users need to unstake ETH through Lido, which may take days to weeks depending on Ethereum's exit queue. If users don't want to wait, they can sell stETH on the open market. Selling 1,000 stETH (more than $2 million) will incur a slippage of about 10-15bp.

Like many other things in DeFi, any DeFi protocol that wants to support stETH can integrate and adopt stETH (just as Aave, Uniswap, Curve, Pendle have already done). Each protocol that supports stETH creates additional utility and demand for users of liquid staking.

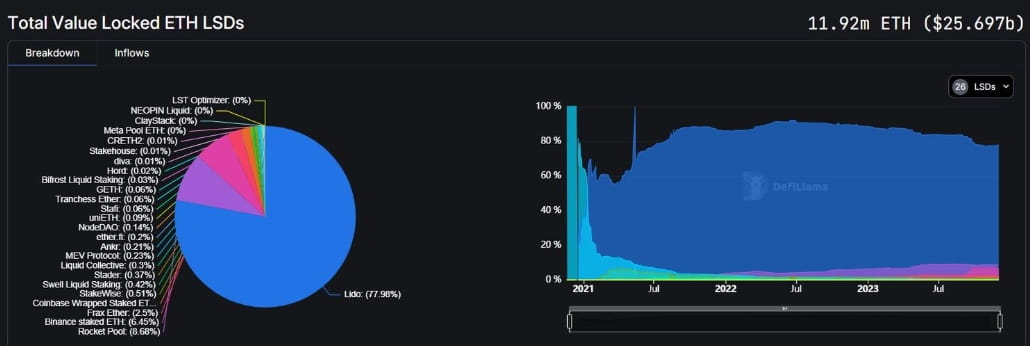

Lido has achieved a FDV of over $20 billion (top 35 tokens by market cap) by locking up over $20 billion in assets, earning over $80 million in annual fees (of which over $40 million belongs to Lido DAO). It is worth noting that the liquidity staking market often has a "winner takes all" situation. Lido holds nearly 80% of the LST market on Ethereum, while the second largest player, Rocket Pool, has staked nearly 10 times less ETH than Lido ($2 billion for Rocket Pool and $18 billion for Lido).

These network effects are driven by several factors:

Liquidity depth of Lido stETH vs. other LSTs: On Curve (the leading DEX for stable assets), the stETH/ETH pool has a TVL of $220M and a liquidity yield of 2% APY. In comparison, the rETH/ETH pool has a TVL of $8M. The increased liquidity depth of stETH means that stETH holders can exit their positions with less slippage and market impact than rETH holders, which is one of the key value propositions of any given LST.

Security and Lindy Effect: Users only receive a low annual yield (3-4%) on their staked assets. This means that security is important to the extent that the protocol is not hacked (e.g., incorrectly issuing and redeeming stETH to obtain ETH), and users value liquid staking protocols with the longest history of security.

DeFi Integration: The largest LSTs tend to have more integrations with other parts of the DeFi ecosystem (across lending, AMMs, yield protocols, derivatives collateralization, etc.), which adds utility to stETH pairs compared to other smaller LSTs. 36% of stETH is used in liquidity pools and lending in DeFi.

These network effects have solidified Lido’s dominance, which holds nearly a third of all staked ETH and has steadily increased its share over the past 2-3 years. As the percentage of staked ETH steadily increases, Lido continues to benefit. In fact, Lido’s dominance is so great that many have called for an examination of its systemic importance on Ethereum, including the implementation of Lido + stETH dual-token governance to check whether the Lido DAO is aligned with Ethereum/stETH holders.

Given the success of Lido (>$2 billion FDV protocol) and its strong network effects in the LST category, similar attempts have emerged in other L1 ecosystems including Solana (Marinade, Jito), Avalanche (BENQI), BNB Chain (Binance, Stader), and Cosmos Chain (Stride).

Liquidity staking penetration varies widely by ecosystem. Ethereum is currently the most mature ecosystem at 41%, while most other ecosystems are in the 2-7% range.

Unlike other major L1 ecosystems, the Cosmos ecosystem is designed as an "internet of blockchains". Cosmos provides an open source SDK (i.e., the Cosmos SDK) that developers can use to write and launch custom blockchains. The first of these chains is the Cosmos Hub (ATOM, $2.7 billion in circulation market capitalization). ATOM is designed to serve as the economic center of this cross-chain and connect/protect other chains in the Cosmos ecosystem.

Over time, many public chains have been launched in the Cosmos ecosystem with open source SDKs, including Osmosis (AMM), Injective (DeFi-focused public chain), Sei (DeFi-focused public chain), Celestia (data availability layer), dYdX (perpetual trading), Kujira (Cosmos DeFi), Terra (now defunct UST stablecoin), etc. Each of these chains has its own PoS blockchain, secured by their own validator set and consensus. This means that for each of these blockchains, there is a native token (OSMO, INJ, SEI, TIA, DYDX, KUJI, LUNA) that is used to secure the network - just like ETH, SOL, AVAX are used to secure their respective blockchains.

Most Cosmos chains are built using some version of BFT (Byzantine Fault Tolerance), where consensus is achieved when 2/3 of the nodes agree on the final state of a block. As a result, most chains rely on a delegated proof-of-stake model that places limits on the number of validators that can participate in consensus to still allow for fast block finalization times (in seconds). In contrast, Ethereum has no limit on the number of validators (approximately 880,000 validators as of December 3, 2023, with 32 ETH staked per validator), similarly requires 2/3 of validators to attest to block finalization, and results in block finalization times of up to 13 minutes.

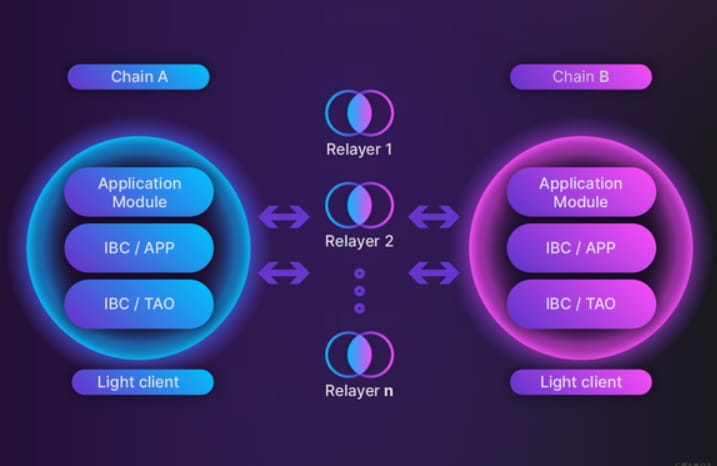

An important aspect of the Cosmos ecosystem is the existence of IBC (Inter-Blockchain Communication) as a standard for trustless bridging between Cosmos chains. IBC is a protocol that handles data transfer and authentication. By defining a standard that every chain built on Cosmos can implement, this allows cross-chain to be done without additional security assumptions, unlike other bridges such as those that rely on multi-signatures (Multichain), optimistic proofs (Synapse), or active validator sets (Axelar) when bridging across non-Cosmos chains. This ability to use IBC for trustless bridging is why Cosmos has been called the "Internet of Blockchains" that can communicate and interoperate with each other.

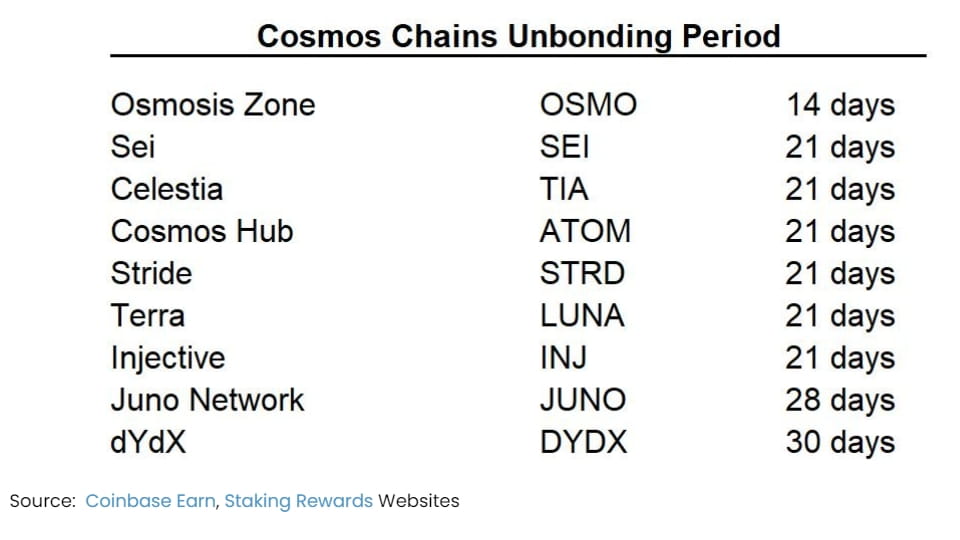

Like other PoS blockchains, the Cosmos chain also has an unlock period for staked tokens. The minimum is 14 days (Osmosis) and the maximum is 30 days (dYdX). Most Cosmos chains have an unlock period of 21 days. While assets are staked and secured on each Cosmos blockchain, they cannot be used in DeFi (lending, providing liquidity, hedging returns), and users must wait a long time if they choose to sell their assets.

About Stride

Stride is a rapidly emerging liquid staking protocol in the Cosmos ecosystem. The protocol was founded by Vishal Talasani, Aidan Salzmann, and Riley Edmunds in June 2022. They raised $6.7 million in seed funding from funds including North Island VC, Distributed Global, and Pantera Capital.

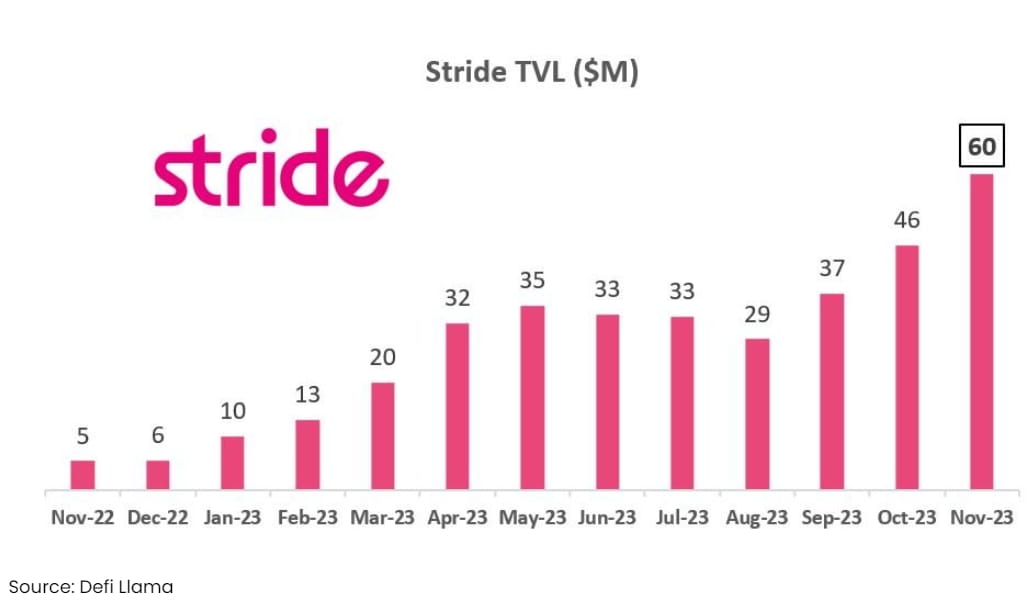

Stride’s protocol launched in September 2022 and has grown to over $60M in total locked value (TVL) over the past year, supporting all major Cosmos chains/tokens including ATOM, OSMO, INJ, JUNO, and soon Celestia and dYdX.

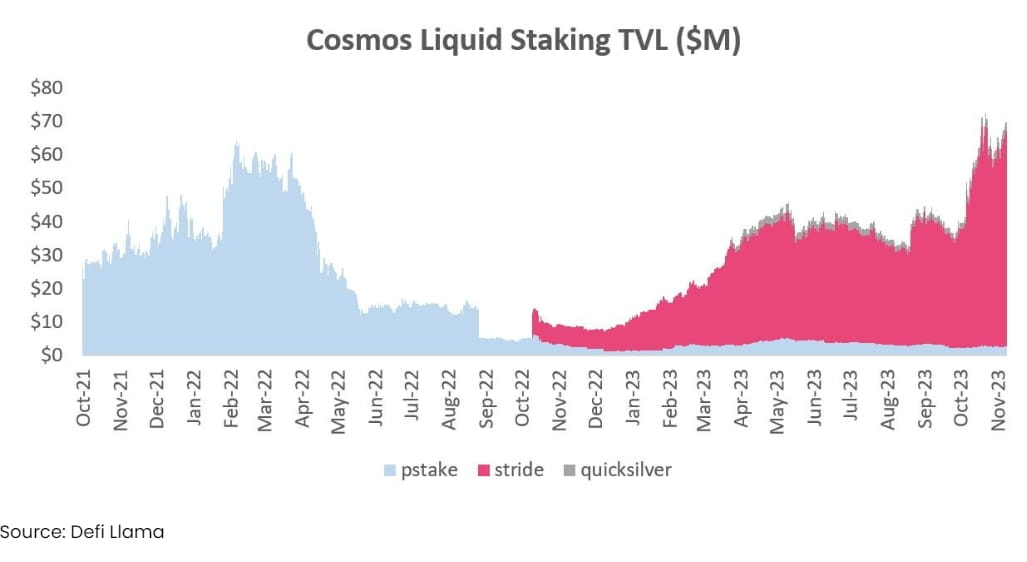

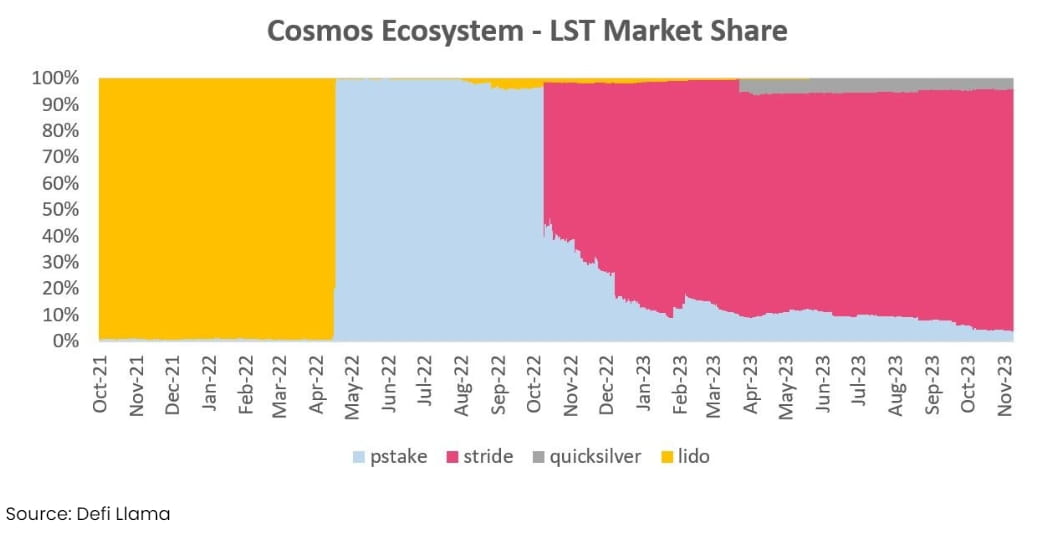

Cosmos has three major liquid staking participants - Stride, pStake, and Quicksilver.

pStake was the first mover, launching in February 2022 and quickly attracting $60 million in TVL through airdrops and support for OSMO (called stkOSMO). However, during the bear market and over the past 18 months, Stride has quickly risen and surpassed pStake in TVL.

Quicksilver is another emerging player but has been struggling in the $2 million to $3 million TVL range.

Currently, Stride dominates the liquid staking market (LST market) in the Cosmos ecosystem, with over 90% of the LST TVL share.

pStake and Quicksilver each hold a 4% share.

Note that Lido once owned ~100% of the liquid staked assets in the Cosmos ecosystem, and its LUNA LST had nearly $10 billion in TVL at its peak (April 6, 2022). However, on May 10, 2022, LUNA began a death spiral and trended towards 0 as its stablecoin UST decoupled and LUNA was minted infinitely. Lido subsequently closed support for Terra to focus on Ethereum, and today does not own any LST in the Cosmos ecosystem, nor has any known plans to do so.

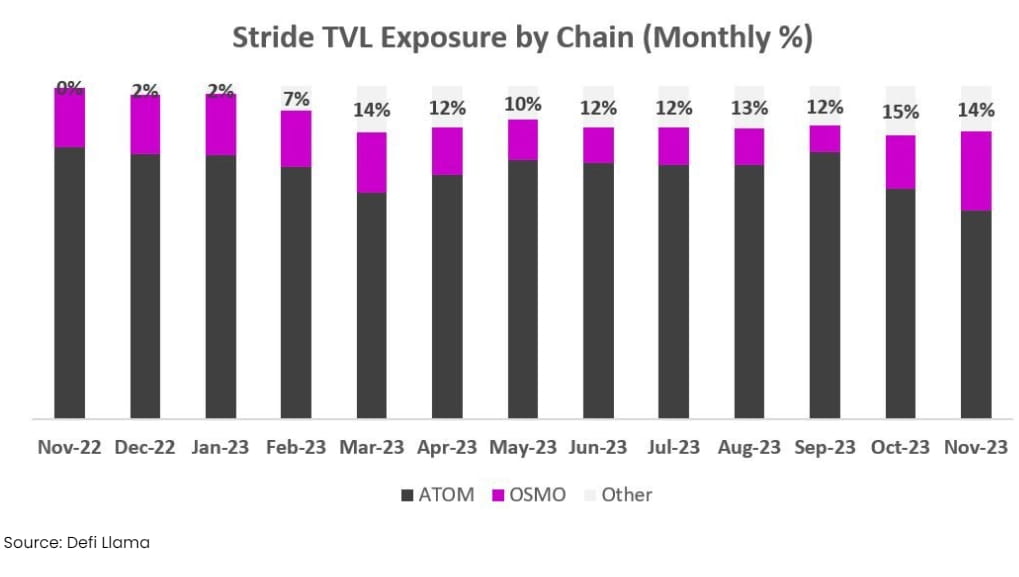

Staking penetration is still in its infancy in the Cosmos ecosystem, with ATOM at 2% and OSMO at 7%. Today, these two chains represent over 85% of Stride TVL. Compared to Ethereum’s 41% penetration (and still growing), this represents 5-20x additional opportunity for ATOM/OSMO before adding other supported Cosmos chains and new chain extensions (Celestia, dYdX).

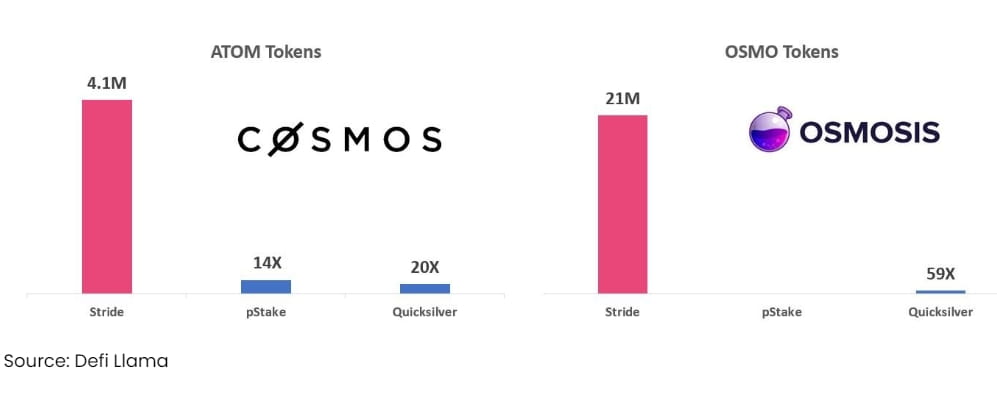

Stride holds 14-20x more ATOM than its two competitors (holding over 85% of liquid staked ATOM), and 59x more OSMO than Quicksilver (holding over 95% of liquid staked OSMO). This is a very impressive lead, and one we believe will be maintained over time.

Stride also has a share of over 95% on other LSTs including INJ, EVMOS and JUNO.

In our opinion, Stride wins for a number of reasons:

· Support for most chains — Stride supports 10 chains in the Cosmos ecosystem. Since its launch in February 2022, pStake only supports two asset pairs (ATOM and XPRT).

Ecosystem Alignment — Stride is tightly integrated with the Cosmos ecosystem. Starting July 19, 2023, Stride begins leveraging ATOM (Cosmos Hub) for economic security (which means that staked ATOM holders secure the Stride blockchain and handle block production). In return, Stride shares 15% of its issuance and protocol revenue with ATOM.

Stronger Economic Security - Using ATOM for consensus means that Stride has stronger economic security than pStake (circulating market value is less than $10 million). In addition, the Stride chain is very simple and does not have any non-LST products on its roadmap. This simplifies the security of the chain.

· Network Effects — As Stride reaches an inflection point for asset support in Cosmos, network effects are starting to kick in. The minimal code changes required to support new Cosmos chains by enabling IBC means that Stride’s scale and Lindy Effect make it the preferred and most secure partner for new Cosmos chains (Celestia, dYdX) to use for their LSTs.

· Deep AMM Liquidity – Stride’s liquidity in AMM pools is significantly deeper compared to competitors. Stride has over $17 million in stATOM liquidity on Osmosis, while pStake has less than $1 million in stkATOM liquidity. This is typically provided to the main chain via Protocol Owned Liquidity (POL), which reduces the incentive Stride needs to provide to scale a given LST pair. For example, Osmosis deployed $11 million worth of OSMO to the stOSMO liquidity pool, while Juno deployed $1.65 million worth of Juno to the stJUNO liquidity pool.

DeFi Integrations — Stride’s LST can now be used in a variety of Cosmos applications, including Umee ($6.5M TVL), Shade ($3M), Kujira ($1.5M), Mars ($1M), and more. These increase the utility and network effects of the Stride LST asset. Stride’s focus on LST, rather than competing with other DeFi protocols, also enables it to be more widely integrated.

Stride takes a 10% cut of the staking revenue it collects through the protocol. Of this, 8.5% goes to the Stride protocol (to stakers of STRD tokens) and 1.5% goes to ATOM/Cosmos Hub to provide economic security for the Stride blockchain.

There are important differences between Cosmos and Ethereum in terms of staking economics:

Validator Fees: Every 32 ETH staked on Ethereum requires the launch of a new validator node. Therefore, Lido takes a 10% cut (same as Stride), but must pay 5% to validators, with the Lido DAO retaining the remaining 5%. Since Cosmos runs on delegated PoS or an equivalent model where staking is simply delegated to existing large validators, there is no additional cost or fee sharing between Stride and validators. The result is higher margins, making Stride the more profitable liquidity staking protocol from a net fee perspective.

Staking yield: Cosmos chains typically launch with higher issuance and inflation rates. For example, ATOM has an annualized yield (APY) of 18%, OSMO has 9%, JUNO has 15%, and INJ has 15%. In comparison, Ethereum's current staking yield is 3-4%. This naturally tends to allow LST to capture a larger proportion of the economic benefits and makes LST a more attractive value-added service when deployed in DeFi protocols.

With TVL growing from $5 million to $60 million over the past year, and an average staking APY of 16%, Stride’s annualized revenue has grown to nearly $1 million.

We believe the following chains from the Cosmos ecosystem will provide growth and buying opportunities for Stride over the next 6-12 months. Stride has expressed its intention to support liquidity staking on dYdX and Celestia (via stDYDX and stTIA tokens).

dYdX ($3-4 billion FDV): dYdX is the largest decentralized derivatives exchange, with over $400 billion in trading volume and generating $100 million in annualized fees. dYdX has been working on a product upgrade (v4) to migrate its trading platform from the StarkEx chain to its custom Cosmos blockchain. Importantly, transaction fees will now accrue to staked DYDX token holders (with a 30-day unlock period). As the market penetration of decentralized perpetual contracts grows from 1-2% to 30% like spot markets, dYdX has the potential to become one of the largest public chains in the Cosmos ecosystem by FDV. On November 21, 2023, Stride announced the upcoming launch of stDYDX and issued 250,000 STRD to drive early adoption.

Celestia ($800-900 million FDV): Celestia is part of Ethereum’s modular scaling roadmap and is one of the leading Data Availability (DA) layers. They recently deployed to mainnet on October 31, 2023. Celestia is likely to grow as Ethereum and its L2 usage grows. Stride has published information to Celestia governance to start supporting LST (called stTIA).

Akash (over $400M FDV): Akash is a decentralized computing marketplace, most recently focused on GPUs. Since the GPU mainnet launch in September, Akash has scaled to ~200 GPUs, with an annualized GMV of ~$500K-$1M. Importantly, a portion of the 20% cut collected by Akash is distributed to Akash stakers, along with the annualized release volume.

· Noble (native USDC on Cosmos): Circle recently launched native USDC support on Cosmos through Noble, an application chain built specifically for native asset issuance. Currently, there are over $30 million in Noble USDC on Cosmos. Noble USDC issuance on Cosmos is likely to grow significantly as Cosmos sees an influx of demand from dYdX, Celestia, Akash, and others, which will spur activity on other Cosmos application chains such as Osmosis, which accounts for Stride's total locks A large portion of the contract volume (TVL).

In the long term, dYdX and Celestia provide Stride with an opportunity for over $10B in FDV compared to ~$6B on existing supported chains. We believe these could be a strong additional tailwind for Stride’s growth in addition to continued penetration of LST on existing chains (ATOM, OSMO, etc.).

In general, Stride intends to be a pioneer in new Cosmos chains. As long as IBC/Cosmos SDK remains attractive for developers to deploy application chains, Stride can continue to support, collaborate and benefit from the growth of new ecosystems.

Valuation and scenario analysis

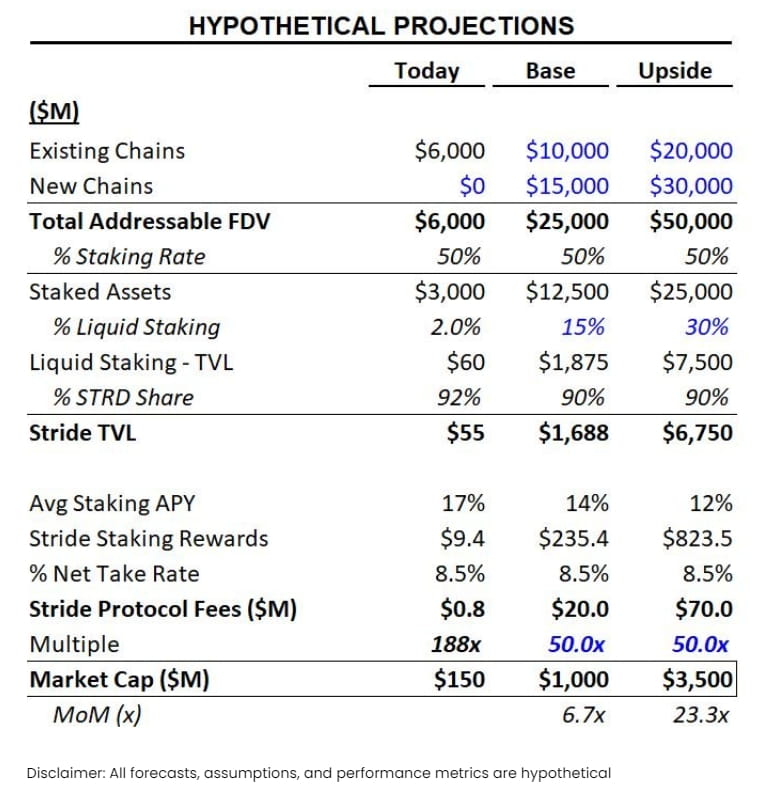

Below, we provide several scenarios for Stride's key drivers. In our base case:

Stride’s FDV Growth: We assume Stride’s FDV grows from $6 billion to $25 billion. Currently, Stride has $6 billion in FDV from existing chains (primarily ATOM, OSMO, and INJ). We assume this grows to $10 billion over a market cycle. Stride is developing support for dYdX and Celestia (TIA), which currently represent nearly $10 billion in FDV. As we are bullish on dYdX and Celestia, we assume their FDV will increase by 50% to $15 billion.

Staking ratio remains stable: Across the entire Cosmos chain, the staking ratio remains stable at 50%. For major existing chains such as OSMO and ATOM, there are no changes.

· Staking drive for dYdX and Celestia: dYdX’s new product will return its fees to token holders, which should drive staking rates comparable to other L1/Cosmos blockchains. Over 16 million dYdX tokens are currently staked. Celestia (TIA) requires a strong validator set to ensure the security of its data availability layer, which may similarly drive high staking rates.

· Liquidity staking penetration growth: On Ethereum, liquidity staking penetration accounts for 41% of all staked ETH (with LDOs accounting for >30% of this share). With a general increase in activity in the Cosmos ecosystem (covering DeFi, AMM, lending, perpetual contract trading, etc.), we believe that Liquidity Staking (LST) penetration can grow significantly from 2% to 15%, which is still far low At the level of Ethereum. Since Cosmos typically has longer unbonding times than other chains (21+ days), this should provide a greater boost for LST penetration growth.

Market share remains stable: LSTs often exhibit a winner-take-all effect, as seen with Lido in the Ethereum ecosystem. Since January 1, 2023, Stride’s market share has grown from 72% to 92%, and we expect it to continue to dominate this market.

Stride maintains its current fee rate: We believe Stride may demonstrate modest pricing power in the future, but do not assume this in our base case or bullish forecasts. Therefore, we assume Stride maintains its current fee rate of 8.5%. Based on the above assumptions and analysis, we can construct different financial forecasts and valuation models for Stride to assess its performance and potential under different market conditions.

Stride Investment Risks and Mitigations

In our investment in Stride, we are actively focusing on several key risks and have developed mitigation strategies accordingly.

· Exposure to the Cosmos ecosystem: Currently, over 85% of Stride’s total value locked (TVL) is tied to just two Cosmos chains - ATOM (63%) and OSMO (24%). This causes Stride’s performance to be tightly correlated with these two projects, as well as market cap/token performance. We believe this concentration risk will decrease over time as Stride gradually expands to support new chains with unique demand vectors. For example, dYdX’s usage is tied to perpetual trading markets, while Celestia is tied to data availability needs for Ethereum rollups, bringing more diversity to Stride’s ecosystem. Since the beginning of 2023, Stride’s share of non-ATOM/OSMO TVL has grown from 2% to 14%-15%.

Competition Risk: Although large-scale liquid staking tends to present a winner-takes-all market structure, the Cosmos LST market is still in its infancy with a penetration rate of only 2%. The Cosmos ecosystem has experienced several changes in dominant players (such as Lido, pStake), which have gradually lost market share as market conditions have changed (LUNA crash, crypto bear market). The risk of Stride failing to dominate liquid staking in the Cosmos ecosystem remains. Recently, new players like Milky Way are trying to compete with Celestia (TIA)'s LST pair.

· Osmosis’ Superfluid Staking: Osmosis launched Superfluid Staking in early 2022, allowing liquidity providers on the Osmosis DEX to collect OSMO staking rewards while providing AMM liquidity. While this is not exactly the same as a liquid staking protocol, it may serve as an alternative to Stride’s stOSMO (22% of TVL). Superfluid Staking only allows LPs to earn 75% of OSMO staking returns compared to holding stOSMO (after deducting Stride’s 10% fee), so we believe Stride offers a better product. Additionally, despite facing competition from Superfluid Staking over the past 12-18 months, Stride has been able to succeed in the OSMO ecosystem (8% liquid staking penetration, even higher than ATOM).

Special Thanks: Thanks to Vishal Talasani (Co-founder of Stride), Jeff Kuan (Axelar), Paul Veradittakit (Pantera Capital), and Cody Poh (Spartan Group) for their reviews and valuable feedback.

Original link