Original title: When the Yield Runs Out Original author: Prathik Desai, Token Dispatch Original translation: Chopper, Foresight News

Original author: Rhythm BlockBeats

Original source: https://www.thetokendispatch.com/p/when-the-yield-runs-out

Reprinted from: Mars Finance

In the financial world, so-called stability is often just an illusion. You bet on a seemingly bland financial product, thinking it can bring stable and reliable returns. It does indeed operate according to the script until the underlying fundamentals begin to shake. Such 'robust bets' are often more deceptive than speculative targets, after all, people initially expect the latter to be high risk, yet rarely anticipate that seemingly safe investments can also go wrong.

Such a scenario played out 75 years ago. In the 1940s, after the Great Depression and World War II, European banks accumulated a large number of dollar deposits. Depositors could hold dollars in non-U.S. banks to hedge against domestic currency depreciation risk. These deposits yielded considerable returns and also gave rise to some innovative operations. Some depositors, including U.S. companies, began to operate flexibly, storing dollars overseas to circumvent capital controls in their home country.

European banks fully embrace this, absorbing deposits and then lending at higher interest rates. A large amount of dollar deposits in Europe ultimately gave rise to the Eurodollar market: a parallel dollar system not regulated by the Federal Reserve. However, with the outbreak of the Cold War at the end of the 1940s, the situation began to spiral out of control. More and more people demanded to reclaim their dollars, but banks did not have enough physical dollars on hand, leading to the collapse of the entire system.

Today, a similar situation is emerging in the stablecoin market. The difference is that this time, digital dollar issuers seem to have learned from historical lessons.

In this article, I will analyze whether Ethena's strategy of shifting to the traditional stock market can save its stablecoin reserve strategy.

The origin of USDe

In early 2024, Ethena launched USDe, a unique synthetic stablecoin. USDe is pegged to the dollar, but the reserves do not hold real dollars. For every USDe issued equivalent to 1 dollar, the platform will hold cryptocurrencies like Bitcoin and Ethereum while shorting an equivalent amount of crypto futures.

These two positions hedge each other. If Bitcoin rises, the spot profit will be offset by the futures short loss, and vice versa. Ultimately, even if there are no real dollars in the account, USDe can always maintain a value of 1 dollar.

But why would users hold USDe instead of mature stablecoins like USDT or USDC? The answer is yield.

The incentive mechanism of USDe perfectly aligns with the operational logic of the crypto derivatives market. In a bull market, more traders bet on rising prices, and trading platforms charge a small continuous fee from longs, known as the funding rate, and pay it to the counterparty. Ethena collects this fee and distributes it to USDe holders as earnings.

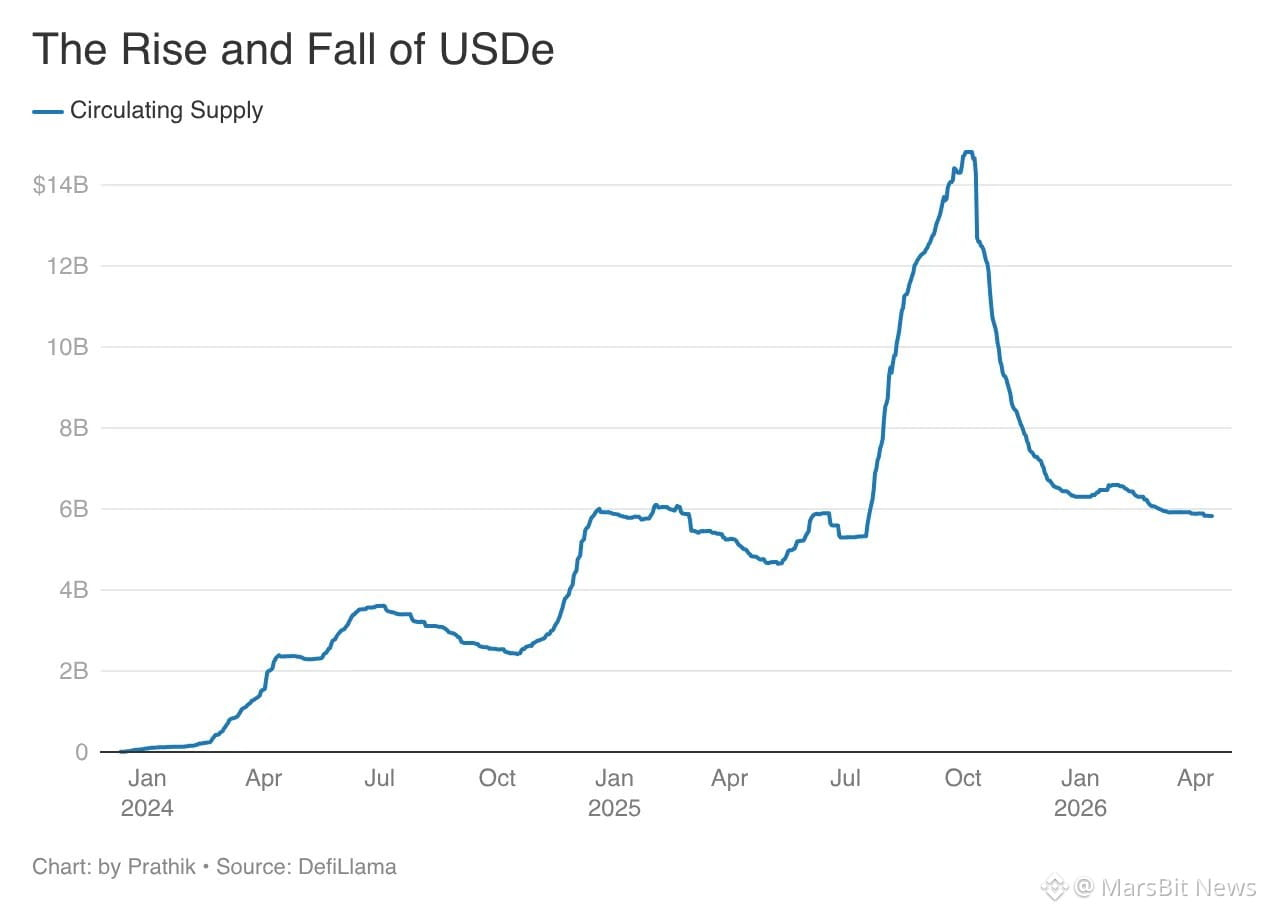

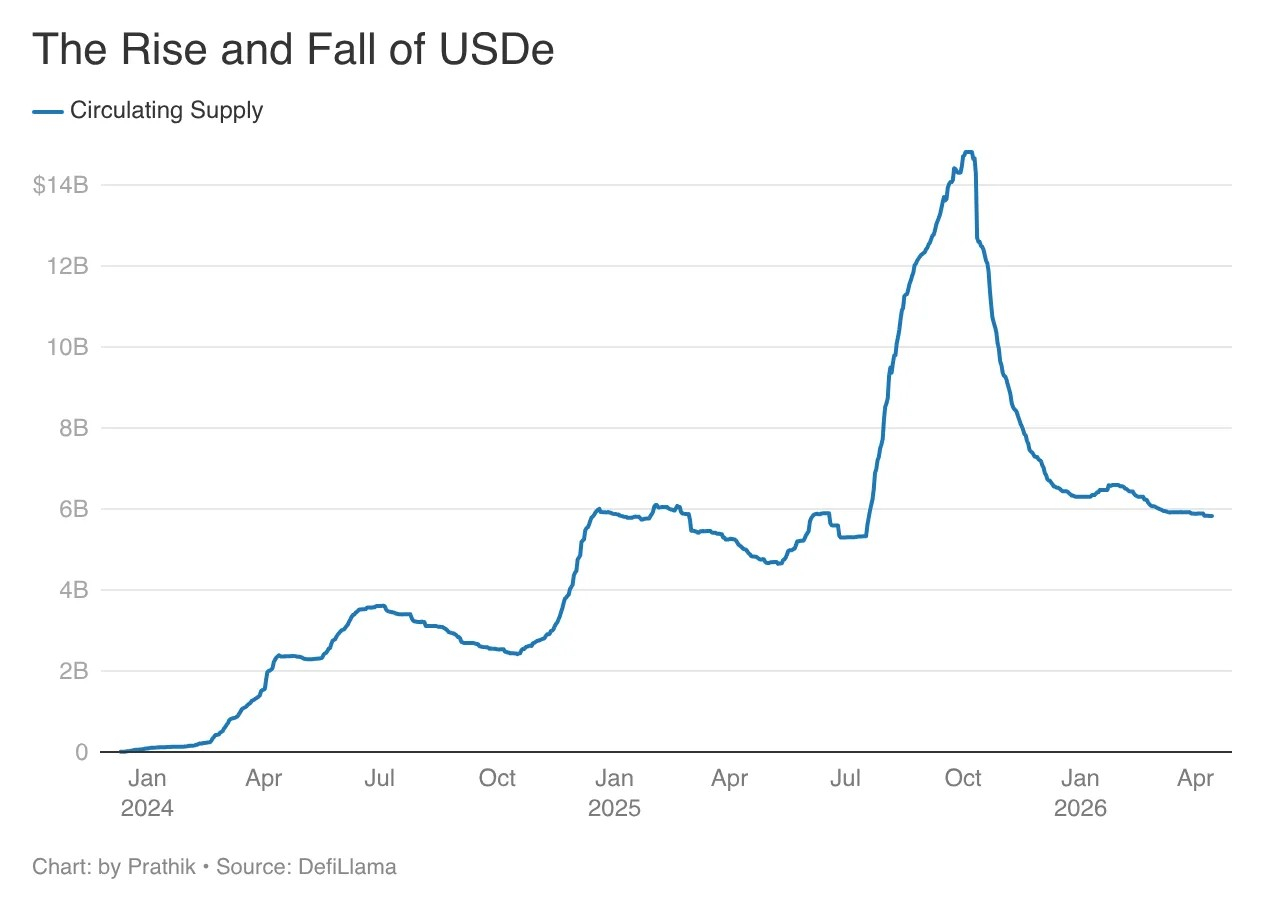

The annual yield peak of USDe once exceeded 20%. Within 18 months, the circulation of USDe grew sevenfold to approximately 15 billion dollars, setting the record for the fastest growth rate in stablecoin history.

However, this design heavily relies on the active state of the crypto market. In a bull market, it works well because Ethena, as a minority short seller, earns the funding fees from the majority long positions. But the market will always turn, and cracks will appear. On October 10 last year, during the largest liquidation in crypto history, over 19 billion dollars were wiped out, and USDe briefly lost its peg, dropping to 0.65 dollars on Binance.

In the five months since then, the circulation of USDe plummeted from about 15 billion dollars to less than 6 billion dollars.

The lesson learned too late

Over 9 billion dollars were redeemed. Perpetual futures once accounted for nearly 100% of reserves, but now only account for 11%. Ironically, all of this could have been avoided; Ethena should have had early warnings.

The signals are already evident: the market always operates cyclically, and the crypto field is no exception. The past 16 years have repeatedly proven that over-reliance on a single collateral closely tied to market trends (perpetual futures) is, in itself, a ticking time bomb.

Other stablecoin issuers have already begun to adjust. As the Federal Reserve cuts interest rates, the top two stablecoin issuers are replenishing reserve earnings. Tether is diversifying its reserves, increasing its gold holdings to a record level; USDC issuer Circle is building infrastructure revenue sources through its Layer 1 public chain Arc and full-stack internet payment system Circle Payments Network.

However, Ethena's actions were slow, and its founder Guy Young admitted on X that without timely remediation, the decline would have been even more severe.

Since October 10 last year, Ethena has been unprepared to respond to significant shifts in the market. Over the past few months, we have been building infrastructure to securely access other safe and scalable collateral sources, making the business more resilient during such cycles.

He also listed the measures that Ethena has begun to take to adapt to market changes.

Embracing solutions from traditional finance

Ethena will expand the range of collateral to include stock and commodity basis trading, over-collateralized institutional lending, bulk brokerage services, and a wider array of real-world assets (RWA).

Ethena was initially a crypto-native synthetic dollar, distinctly different from stablecoins like USDT and USDC that rely on real dollar or treasury reserves.

Now it has come full circle, re-entering the traditional financial system to continue paying yields to holders, and it is tapping into multiple sources of income.

In stock basis trading, Ethena buys the S&P 500 spot while shorting its futures to earn the spread, which is the same strategy it used in the early days with Bitcoin and Ethereum. This yield may be small, but it is predictable and unrelated to crypto market trends.

Similarly, Ethena can replicate the same strategy across multiple asset classes such as gold, silver, wheat, crude oil, commodities, stock indices, and credit markets. Each asset has price differences driven by supply and demand, allowing Ethena to execute delta-neutral arbitrage across all categories, earning interest rate spreads around the clock, completely unaffected by crypto market sentiment.

While this reduces dependence on the crypto market, it binds it to markets like stocks and commodities. Once the volatility of these markets surges and futures liquidity dries up, the strategy may also fail.

However, this pessimistic expectation is equivalent to betting that a highly diversified cross-asset investment portfolio will fail overall. While the possibility exists, it is small. The financial world is built on probabilities; diversification is not intended to ensure profitability during a market-wide downturn, but rather to reduce the probability and extent of losses.

For Ethena, diversifying investments into revenue sources unrelated to the crypto market can achieve the same effect. Even if one or two asset classes perform poorly, the overall yield is unlikely to be completely squeezed out.

Liquidity test

Ethena's diversification strategy is a reasonable solution to cope with market cycles. Spreading risks across stocks, commodities, credit, and crypto assets can make income streams more resilient. This may also be its only advantage compared to USDT and USDC, which rely on treasury bonds and offer almost no returns to holders.

However, the new strategy still faces tremendous resistance.

The liabilities of USDe are fully liquid, and holders can redeem at any time; however, the assets generating revenue do not have ideal liquidity during periods of stress. Stock basis positions require time to close out smoothly, institutional loans have fixed terms, and collateralized loan certificates often lack liquidity in volatile markets.

The mismatch between this highly liquid liability and imperfectly liquid assets will become a structural contradiction for all income-generating stablecoins, which cannot be completely resolved even with a diversification revenue strategy.

In a stable market, different assets will fluctuate based on different signals: inflation concerns push up gold prices, positive earnings uplift the stock market, geopolitical crises in oil-producing countries push up oil prices, and retail optimism boosts crypto funding rates.

But under extreme pressure, all logic will fail. The assumption of correlation between assets will collapse, and the advantages of diversification will vanish. The only common core of all assets is liquidity.

Once the market deteriorates comprehensively, everyone will choose to cash out.

Harry Markowitz won the Nobel Prize for his theory of risk reduction through diversification, but the 2008 financial crisis proved that modern portfolio theory has exceptions. Scholar Nassim Taleb also proposed the same view in 'The Black Swan': correlation is not a constant attribute of assets but a variable that changes with the market environment.

Despite such anomalies, it must be acknowledged: black swan events are inevitable and extremely rare, and almost no one can predict or control them. Cross-asset diversified portfolios are still likely to outperform concentrated positions relying on a single asset class. The 2008 monetary market crash is an example.

Over-collateralization is one of the means Ethena uses to respond to such risks. If borrowers collateralize assets exceeding the loan amount, theoretically, losses will be absorbed before affecting USDe holders. However, the over-collateralization rate is set based on historical volatility, and extreme stress events may exceed this range.

No strategy can be completely risk-free. What Ethena needs to do is convince investors that this new diversification strategy is more robust than the previous model that relied entirely on a single crypto market.