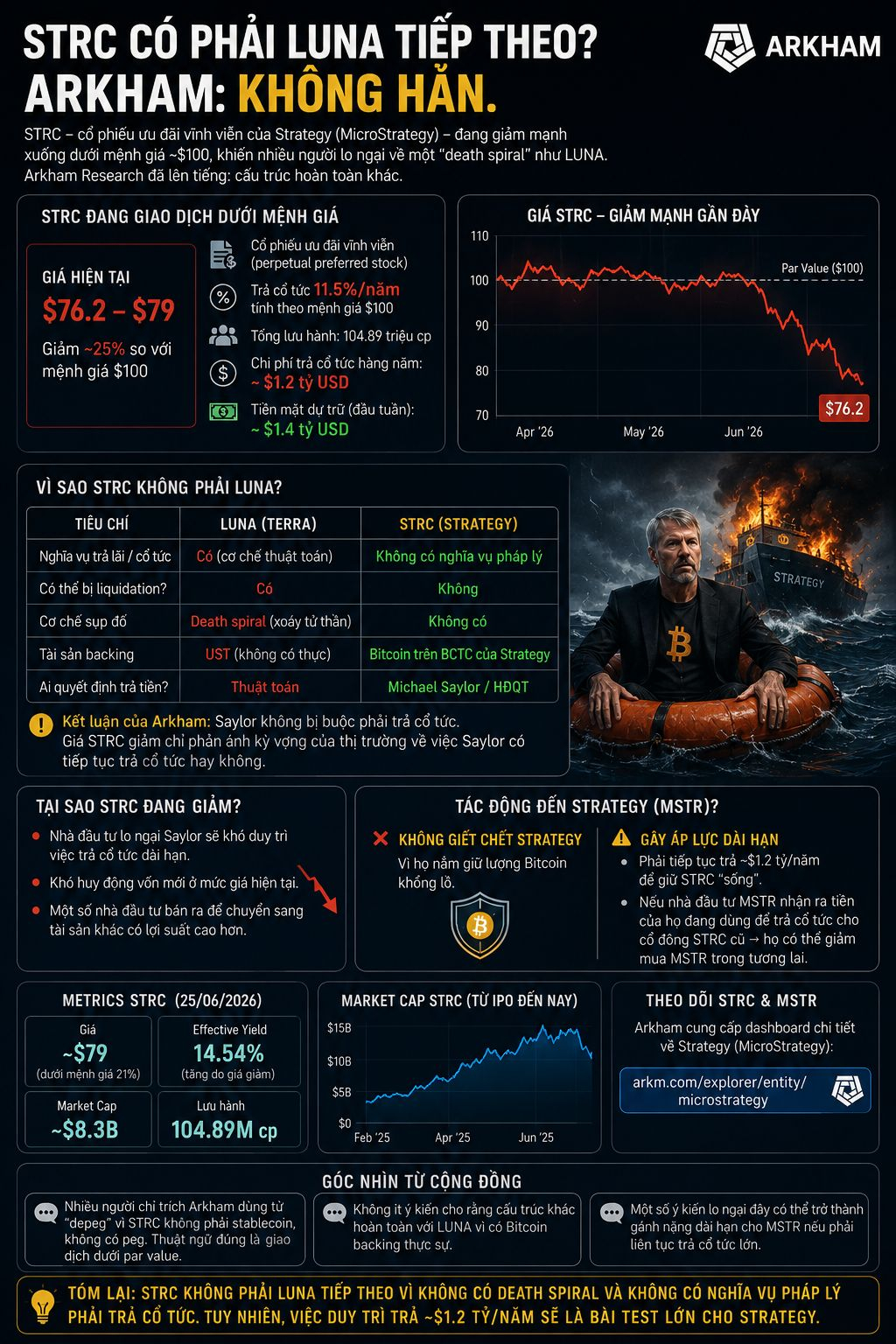

After STRC (Strategy Preferred Stock) fell sharply to about $76–79, nearly 25% below the $100 par value, many investors started asking whether this is a "second LUNA." Refer to Arkham’s arguments, folks:

=> In my view, the issue worth focusing on is not the "death spiral" capability, but the sustainability of the capital-raising model Michael Saylor is building.

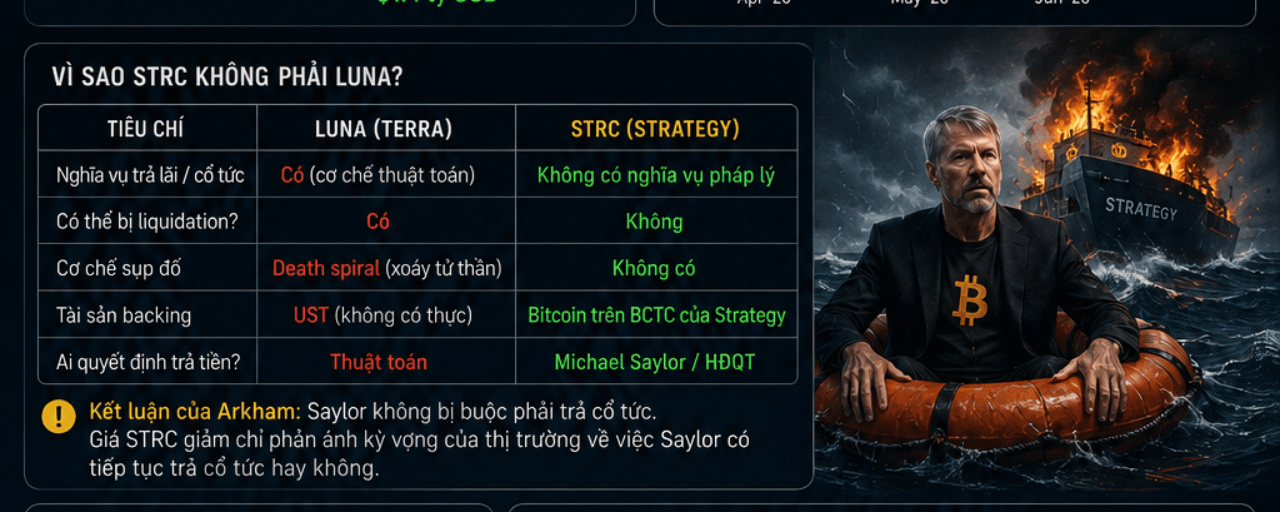

Why is STRC being compared to LUNA?

*The similarity that makes the market draw parallels is that both witnessed assets dropping sharply in a short time, raising concerns about the ability to sustain the financial model behind them.*

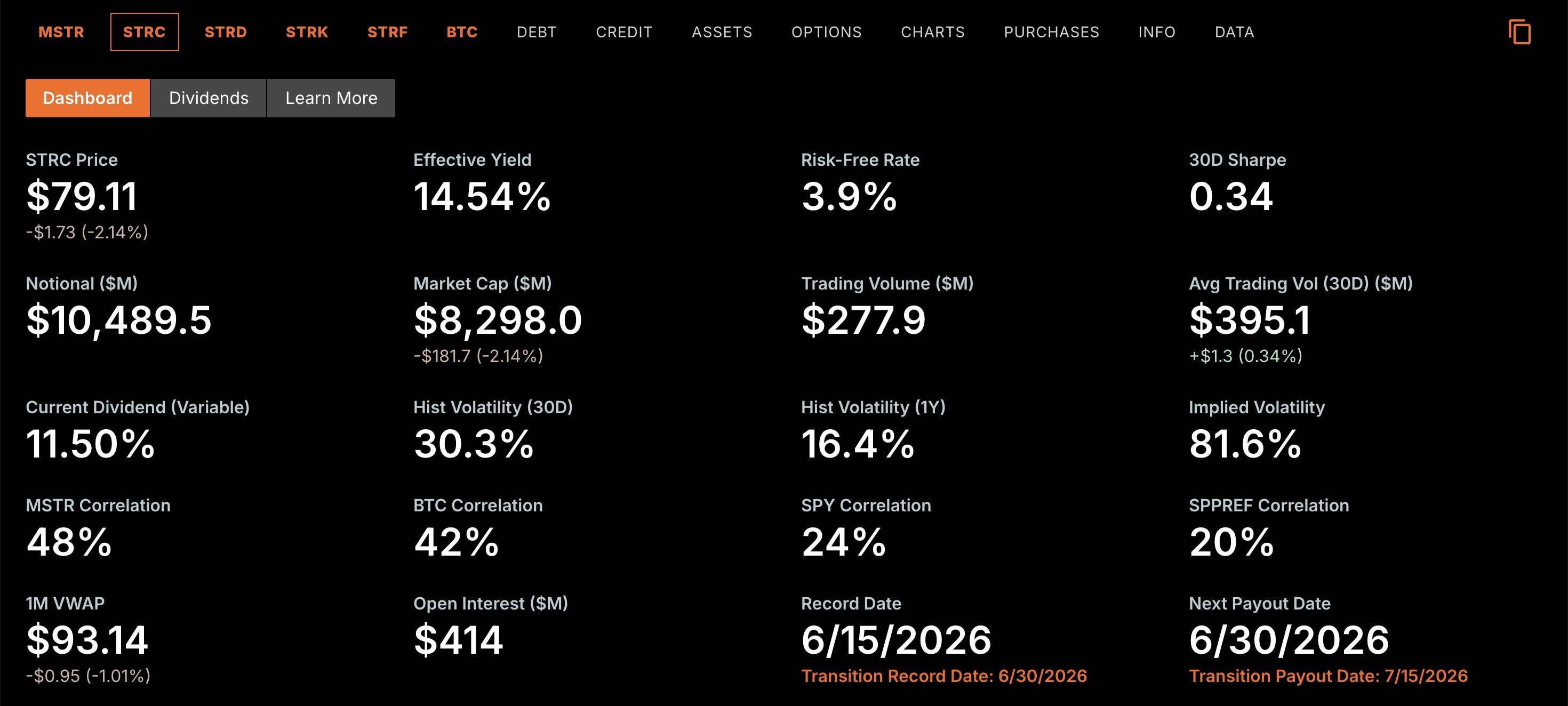

STRC is currently trading around $76–79, about 25% lower than the $100 par value.

But this is a Perpetual Preferred Stock (perpetual preferred share) issued by Strategy, paying a dividend of 11.5% per year based on par value.

The price drop reflects the market re-pricing risk, not the system entering a collapse spiral like Terra.

=> What worries the market isn’t that the price of STRC is dropping, but whether Strategy can continue to sustain this capital-raising model for many years to come.

Why isn’t STRC LUNA?

*The biggest difference lies in the operating mechanism.*

LUNA depends on an algorithmic mechanism to maintain the value of UST. When trust disappears, the system automatically creates a "death spiral" that causes both UST and LUNA to collapse.

STRC has no infinite token-minting mechanism. Strategy will not be liquidated if STRC’s price drops. More importantly, Strategy has no legal obligation to continue paying dividends if the company faces difficulties.

=> Whether to continue paying or to pause dividends entirely is decided by Michael Saylor and the Board of Directors. That’s why $STRC cannot get pulled into the death spiral like Terra.

Then why is STRC still dropping sharply?

*The main reason is that the market is re-pricing expectations about the sustainability of dividends in the future.*

*Currently, Strategy has:*

104.89 million STRC shares are outstanding.

The cost of paying dividends is about $1.2 billion per year.

About $1.4 billion in cash reserves (based on early-week figures).

=> These numbers have not yet put Strategy into a liquidity crisis.

*Some questions from the market:*

But if the capital markets become tougher going forward, will Strategy still be able to raise cheap capital?

If Bitcoin $BTC enters a prolonged down cycle, will the company still prioritize paying dividends?

If Strategy cuts dividends, will STRC still be valued like it is today?

=> In other words, STRC is falling not because Strategy becomes insolvent, but because the market is starting to reduce expectations about the long-term sustainability of this model.

Bitcoin is the biggest differentiator

*Strategy’s collateral assets are completely different from Terra*.

Terra operates based on trust in an algorithm and the stablecoin UST.

Meanwhile, Strategy holds a very large amount of Bitcoin on its balance sheet. A drop in STRC’s price doesn’t force Strategy to sell Bitcoin. There is also no mechanism that would cause STRC to be issued infinitely like LUNA used to be.

=> This is why Arkham thinks calling STRC the "next LUNA" is not accurate.

What is Strategy’s real risk?

Over the past several years, Michael Saylor has continuously used the strategy: Issue financial instruments => Raise capital => Buy more Bitcoin.

This model works extremely well when the market is willing to provide funding at low costs. But if STRC continues trading below par value, the cost of raising capital will rise, and issuing more similar products will become more difficult.

=> This is not a risk that would cause Strategy to go bankrupt, but it could reduce the effectiveness of the "Bitcoin buying machine" that Michael Saylor has built over the years.

Conclusion

In my view, comparing STRC with LUNA is not appropriate because the two models are fundamentally completely different. STRC has no death spiral mechanism, it isn’t automatically liquidated, and it is supported by the actual amount of Bitcoin held by Strategy on its balance sheet.

However, if STRC continues trading below par value, Strategy will have to raise capital at higher costs, thereby slowing down the Bitcoin accumulation strategy that Michael Saylor is pursuing.