Today I’ll continue talking about the US stock semiconductor sector. Don’t think there are many semiconductor companies—at present, there are only a handful of major players. Most of what I need to cover has already been discussed. At the beginning, when I first started talking about US stocks, it was dizzying—there were so many companies: how do you tell them apart, how do you analyze them? But by accumulating step by step, I’ve almost memorized most of the companies and the ways the semiconductor sector is categorized.

After I’ve finished going through the semiconductor companies in the next sections, I’ll also classify the leading players across these different semiconductor sub-sectors—so be sure to keep watching the program.

Yesterday I talked about KLAC, KLA Corporation—truly a fascinating company that has been making money long term. It belongs to the inspection stage, so in this track, I’m going to dig deeper into a few more companies.

1. Applied Materials (AMAT)

This company mainly sells “chip manufacturing machines,” with key directions including deposition, CMP, ion implantation, and other integrated equipment. Many people think chip manufacturing is mainly about lithography machines—like ASML. But there are many steps in chip manufacturing. Before lithography on the silicon wafer, you need to perform “deposition” operations.

It essentially “grows” various materials layer by layer on the surface of a silicon wafer, ultimately forming complex structures like transistors, interconnects, and insulating layers. You can think of it like building a building: you need to lay steel reinforcement bars and pour concrete on the foundation, and then repeat the process over and over to build the structure. In the AI era, there are more and more layers in GPUs, so you continuously build conductive layer and insulating layer materials on the surface of a silicon wafer. The operation precision is at the 0.1nm level, and currently, globally, there are not many companies that can do this. This is AMAT’s absolute core moat.

Besides deposition equipment—which is its most profitable business—it also supplies “ion implantation” equipment. Ion implantation installs conductive ions onto silicon. Since silicon isn’t a good conductor on its own, the equipment acts like a particle accelerator. The equipment cost ranges from a few million to tens of millions of dollars.

CMP (chemical mechanical polishing): after each deposition layer, you need to polish it—this is relatively easy to understand.

AMAT’s main customers include Micron, Hynix, Samsung, Nvidia, Intel, and other chip “makers.” So it’s almost an “all-in-one” company for the chip supply chain.

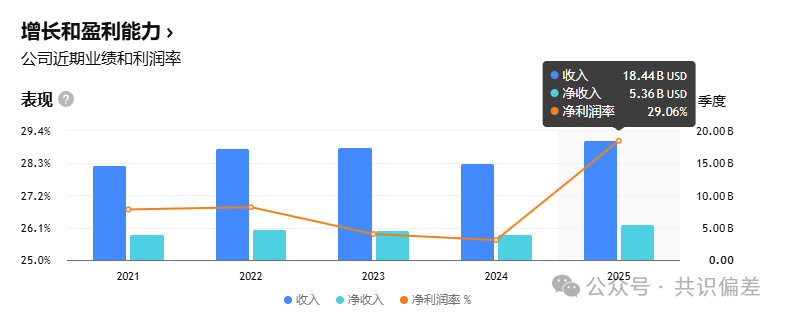

Current market capitalization is 574 billion RMB, with a P/E ratio of 65x. In recent years, its revenue has been very stable—about 28 billion RMB, net income of 7 billion RMB, and a net profit margin of 25%. Currently, the 2026 revenue forecast is 33 billion RMB. In 2026 Q1 and Q2, the reports show sequential growth of around 10%.

But the stock price is already at a new high. If you look at it from the monthly chart, it has been in a steady uptrend. From the 1977 low of 0.017, it’s now up 41,000 times. From 150 in June 2025, it’s also up 5x. So sometimes you don’t know until you look—U.S. stocks really are a “miraculous” place!

2. Lam Research

Lam Research (LRCX) is the world’s second-largest semiconductor equipment company (by revenue, it comes right after AMAT) and is also the absolute leader in global etching equipment.

Lam’s two most core businesses are:

- Plasma Etch

- Wafer Cleaning

Etching is the next step after AMAT deposition. After AMAT lays down and prepares the materials, lithography tools pattern the wafer, and then LRCX is responsible for removing all the unwanted areas.

Don’t think this is simple—it is extremely difficult, involving atomic-scale patterning at the nanometer level. The core technology is high aspect ratio etching (look it up on Baidu yourself). It’s also the kind of track where one piece of equipment sells for several million to tens of millions of dollars. It’s a market with a very deep moat.

LRCX currently has a market cap of 541.9 billion RMB, a P/E ratio of 77x. At present, the company’s revenue is also stable at 18 billion RMB, with net income of 5 billion RMB. The 2026 revenue forecast is 23 billion RMB, and 2027 is forecast at 30 billion RMB. The estimated growth rate for the next 4 years is 20%.

Currently, the LRCX stock price is also at a new high. Since the 1990 low of 0.07, it’s now at around 425—up 6,000 times. From 80 in June 2025 to now, it has risen about 5x.

Because of space limitations, I’ll cover two of the four semiconductor equipment leaders first. They are absolute leaders with non-substitutable positions. Over the long term, they are still very good.