Over the past six months (Aug 2025–Feb 2026), risk appetite in financial markets has reached historically elevated levels. However, this strength is uneven across asset classes. In U.S. equities, options markets show sustained bullish positioning, with call volumes significantly exceeding put demand and volatility remaining near historic lows. This environment reflects strong investor confidence and favorable liquidity conditions.

Recent CPI data has reinforced this backdrop. Headline CPI slowed to 2.4% year-over-year, down from 2.7%, while core CPI eased to 2.5%. Lower inflation reduces pressure on real yields and supports expectations of eventual monetary easing, creating a supportive macro environment for risk assets.

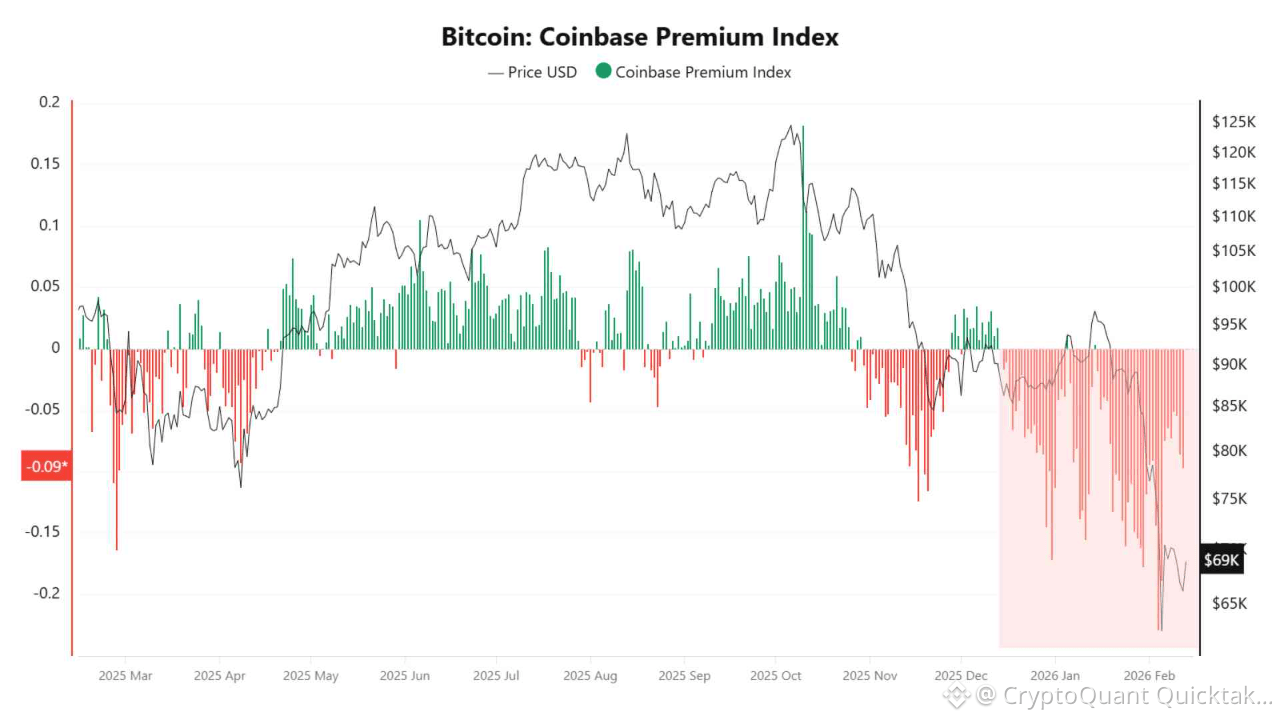

In contrast, Bitcoin’s structure remains less decisive. The Coinbase Premium Index, a proxy for U.S. spot demand, has remained in negative territory, indicating weaker institutional buying during recent price movements. Historically, sustained rallies tend to coincide with persistent positive premiums, reflecting active accumulation from U.S.-based investors.

ETF flows also remain inconsistent, alternating between inflows and outflows rather than forming a sustained accumulation trend. This suggests institutional capital has not yet fully re-engaged despite improving macro conditions.

Over the next 30 days, Bitcoin is best viewed as being in a recovery validation phase rather than a confirmed uptrend. Key signals to monitor include a sustained positive Coinbase Premium, consecutive ETF net inflows, and evidence of spot-driven demand rather than leverage-driven price movements.

Written by XWIN Research Japan