Written by: 0xLoki

Space has talked about a topic before: Will the Hong Kong SFC be like the US SEC, and go crazy in defining securities and then regulating, investigating, and fining them? The key to this question is that we cannot just look at what they say (organizational goals), but also what they do (actual behavior). There is a very simple way to answer this question: understand the business and personnel composition of the SEC and SFC.

SEC

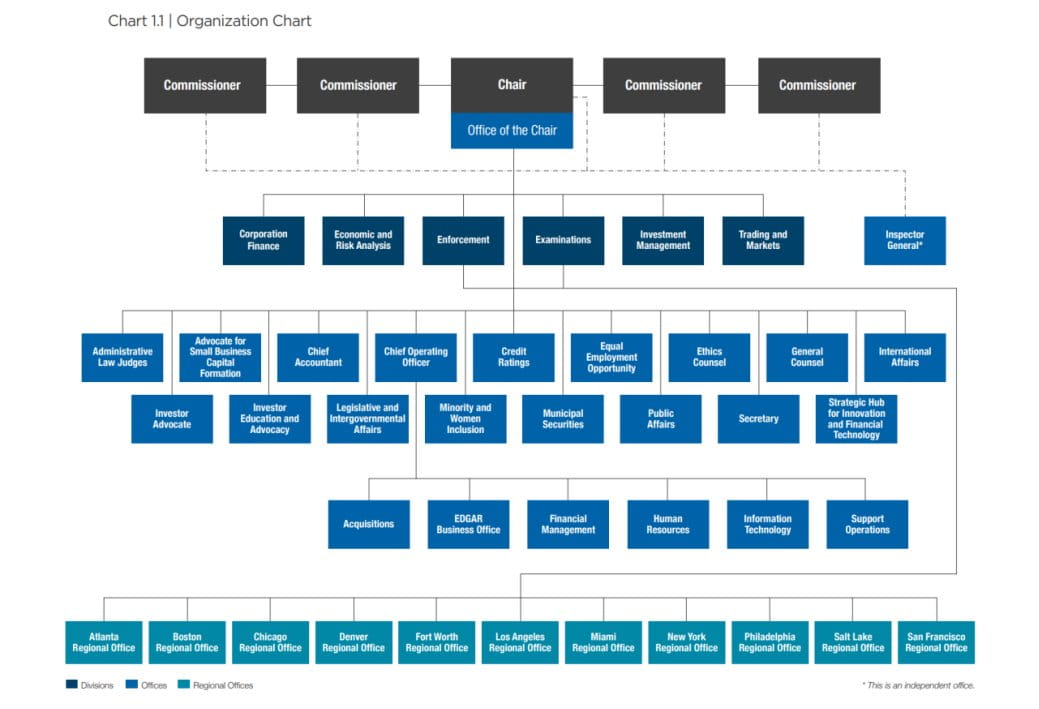

First, let’s take a look at the structure of the SEC. At the top is a committee consisting of the Chairman + 4 members, which consists of 6 departments + 1 Office of the Inspector General + 11 offices. In addition, there are 11 regional offices. It should be noted that these 11 regional offices need to report to both the Enforcement Department and the Examinations Department at the same time.

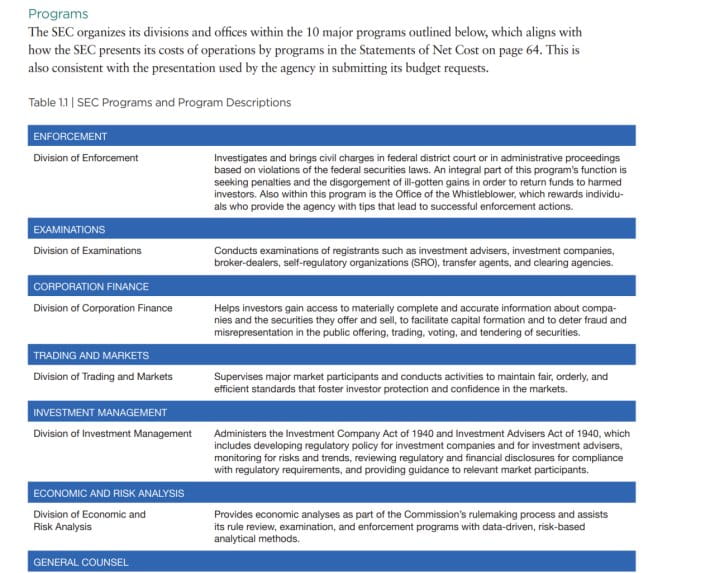

From the organizational structure, we can find that the Enforcement Department and the Examination Department seem to be the most important among all departments. In the following descriptions of each department, we can also see that the Enforcement Department and the Examination Department are also listed first and second.

In addition, there is a more convincing data: financial situation. The SEC’s funding sources are roughly composed of three parts:

1) Financial budget;

2) Securities trading fees and application fees;

3) Fines and confiscations.

The fines and confiscations are divided into two parts:

A. If there is a need to compensate the victims, the fines and confiscations will be used to compensate the victims + injected into the General Fund of the U.S. Treasury.

B. If there is no need to compensate the victims, the fines and confiscations will be allocated to the investor protection fund, whistleblowers (providers of investigative clues), and funding for investigations by the Office of the Inspector General.

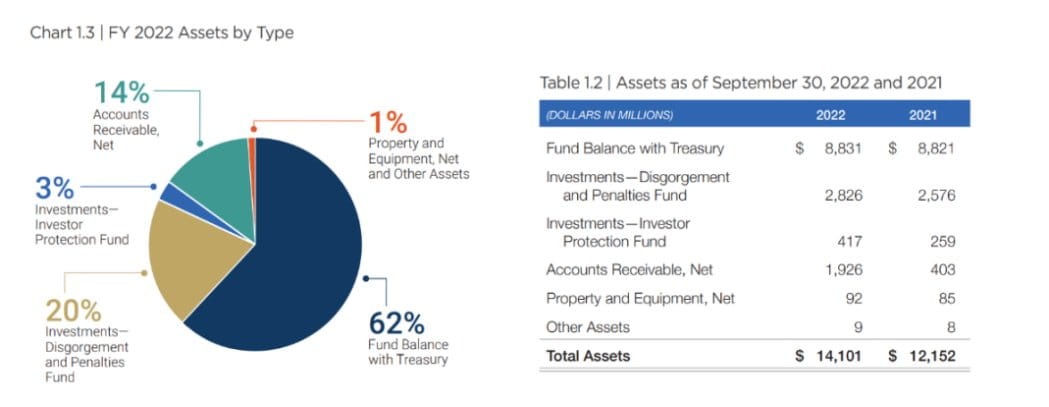

Next, let’s take a look at the SEC’s balance sheet. According to the annual report for fiscal year 2022, the SEC’s total assets increased from $12.2 billion to $14.1 billion, an increase of $1.9 billion. Among them, investment items increased by $400 million; accounts receivable increased by $1.5 billion. The vast majority of these two items are composed of fines and confiscations, and the investment items have also deducted expenses in the regulatory process.

In addition to fines and confiscations, the OMB approved a reserve fund budget of $50 million for the SEC in 2022, an investor protection fund budget of $390 million, SEC transaction fees of approximately $1.8 billion, and application fees of $640 million. It can be seen that fines and confiscations have become a kind of [pillar income].

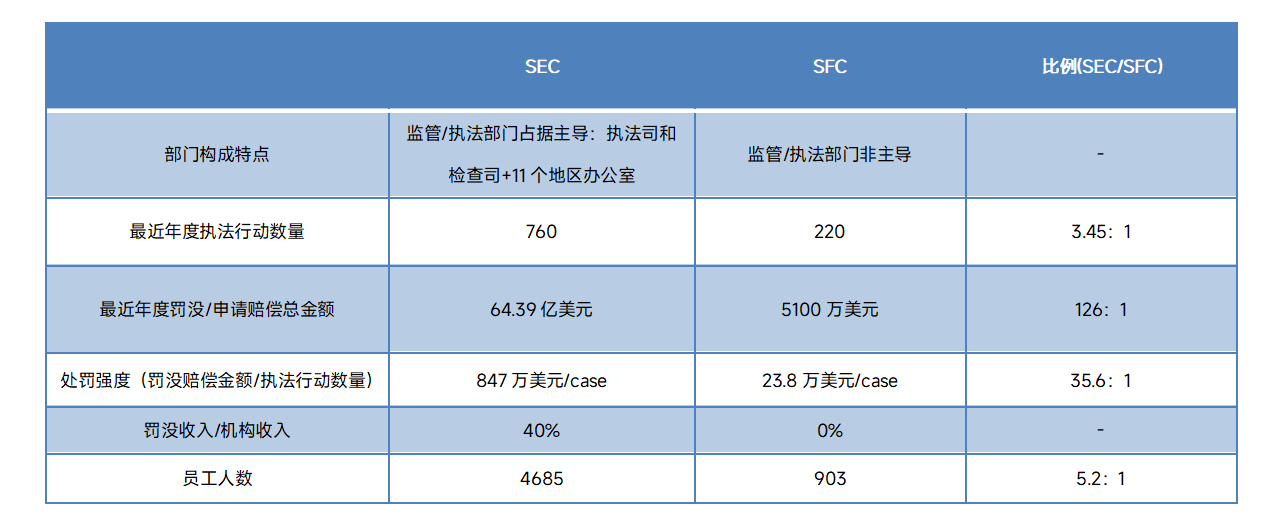

After looking at the income and then looking at the expenditure, you can see that the net expenditure of the Enforcement Division and the Inspection Division is the highest, totaling US$1.75 billion, accounting for 65% of the total expenditure. These expenditures were eventually converted into enforcement actions: According to another public article of the SEC, the SEC filed a total of 760 enforcement actions in fiscal year 2022, an increase of 9% over the previous year. This includes 462 new or "independent" enforcement actions.

These enforcement actions brought in a bounty of revenue: Total payments ordered totaled $6.439 billion, including civil penalties, disgorgement, and prejudgment interest, the highest in SEC history, up from $3.852 billion in fiscal 2021. Of the total amounts ordered, civil penalties amounted to $419.4 million, also a record high.

Under this system, the SEC has issued generous rewards to whistleblowers. In fiscal year 2022, the SEC issued approximately US$229 million in 103 awards, ranking second in history in terms of amount and number of awards. At the same time, the number of reports in fiscal year 2022 also ranked first in history, with the SEC receiving a total of 12,300 reports. Gensler's request at the hearing for the SEC to obtain resources to increase its staff from 4,685 to 5,139 also became reasonable.

To sum up, the SEC’s behavioral path is not difficult to understand. This is a post-enforcement. First, let as many people as possible come in and behave themselves, then investigate, collect evidence, prosecute and punish as much as possible. Therefore, it is not difficult to understand the SEC’s statement that [except BTC] are all securities. Expanding the law enforcement goal is the first step. Of course, whether to choose to enforce the law in the end and whether the prosecution is established depends on many factors.

SFC

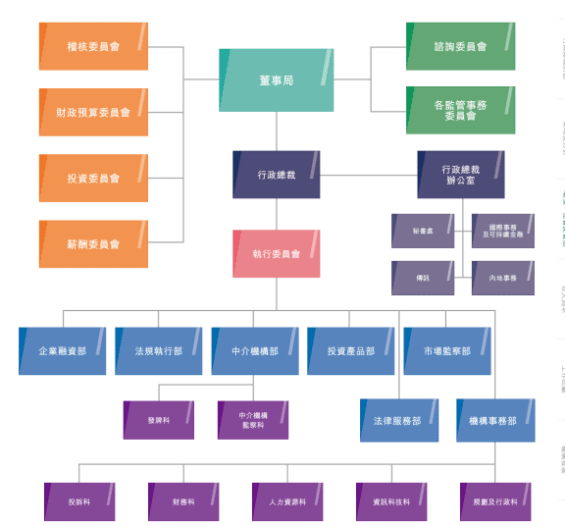

After talking about SEC, let’s look at SFC. The structure of the SFC is significantly different from that of the SEC. The only ones that may be involved in supervision are the Market Inspection Section and the Intermediary Supervision Section under the Intermediaries Department. In addition, the intermediary agency has also set up a [Licensing Section], which is inseparable from the familiar licensing system.

According to the SFC's 2021-2022 annual work summary, the SFC conducted a total of 220 case investigations, initiated 168 civil lawsuits, and imposed a total fine of HK$410.1 million on licensed institutions and individuals. In addition to law enforcement, another important data is that the SFC received 7,163 license applications that year; more than 38,000 license information reviews were processed through WING.

In the specific category of enforcement, although the SFC mentioned that [where appropriate, we will decisively take enforcement action against unlicensed platform operators. ], but from the perspective of law enforcement cases, illegal activities in the traditional financial field are still dominated by insider trading and market manipulation, corporate fraud and misconduct, intermediary negligence, improper internal control and other illegal activities.

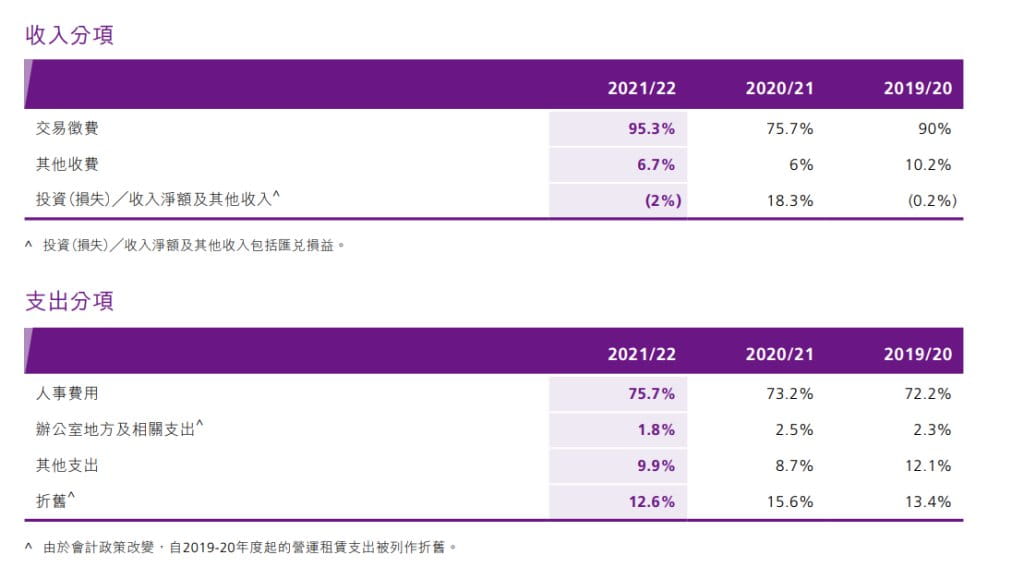

In terms of income and expenses, the composition of SFC is very simple. The total income of SFC in 2021-2022 is HK$2.247 billion, of which [transaction levy] accounts for 95.3%, other income is 6.7% (mainly levied from market participants), and penalty income It does not appear in SFC's revenue sharing. Of the expenditure, 75.7% was personnel expenses. According to the annual report data, SFC has a total of 913 employees as of 2022.

In addition, based on this data, it is not accurate to say that SFC makes money by issuing licenses. Market transactions contribute the vast majority of SFC’s revenue. According to the application fee/annual fee of HK$4,700-129,700 for each activity of licensed legal persons and the application fee of HK$1,790-5,370 for each activity of licensed representatives, the 3,231 licensed institutions and more than 40,000 licensed personnel do not contribute much revenue.

Judging from past data, the SFC does not have the same motivation as the SFC. On the other hand, the SFC does not have the same law enforcement capabilities as the SFC. The SFC has only 903 employees. These employees also need to deal with the complicated business of the Stock Exchange and the Futures Exchange, handle a large number of license applications, maintenance and inspections, and even have to [promote kindness and make the world a better place]. It is difficult to allocate so much manpower and material resources to carry out proactive law enforcement.

From the above data, we can see that the SFC does not have the same policy inclination as the SEC, and the SFC/SEC are essentially acting in accordance with the idea of [same business, same principles, same risks]; the SEC has a very strong regulatory inclination towards cryptocurrencies, but it also has the same inclination towards other financial institutions; and the SFC is unlikely to give cryptocurrencies special treatment.

In summary, I think it is very unlikely that the SFC will enforce the law on a large scale like the SEC. For entrepreneurs, as long as they do not clearly violate the current laws and regulations of Hong Kong, they do not need to worry about regulatory pressure. But I do not think that the [Hong Kong market] and [active licensing] are suitable for every project party. After all, application and maintenance also require considerable costs. Even without a license, many other Web3-related things can still be done in Hong Kong.

Although there is no need to worry about regulatory pressure like the SEC, I still want to say here that every participant who is eager to try should calmly ask themselves a question - do we really need a [license]?