After going through another round of bull and bear markets, the exchange landscape has also undergone a new round of reshuffle.

Although from a static perspective, the leading exchanges represented by Binance have occupied a large proportion of the market share, and the track structure seems to have become solidified, but if we take a longer-term view and combine it with the historical experience of track changes and even business development, there will always be up-and-coming companies that can accumulate momentum when they are insignificant, wait for the right opportunity, and then take advantage of the situation to overtake the former.

On this point, this was the case with Binance four or five years ago, Bybit which gained momentum by leveraging contract products, and FTX which was once at its peak.

TinyTrader: The “water carrier” behind the exchange

Recently, we contacted TinyTrader, a white label solution provider specializing in serving B-side customers such as exchanges, and had a chat with their co-founder and CEO Zo Liang.

As front-line practitioners who deal with institutional clients every day, Zo Liang and TinyTrader have intuitive perceptions and unique insights into the competitive status of the exchange track, the breakthrough opportunities for small and medium-sized exchanges, and the entry trends of traditional finance. Their views may also help to further deepen everyone's understanding of the development of the industry.

TinyTrader is positioned as a global trading infrastructure provider, providing a full set of white label solutions from front-end to back-end, from perpetual contracts to options contracts, from liquidity services to compliance support. To a certain extent, TinyTrader's business model is somewhat similar to MetaQuotes, a trading software developer in the traditional financial market, but unlike MetaQuotes, which is limited to a single market, TinyTrader's products and services can span the two major markets of traditional finance and Web3.

As the CEO of TinyTrader, Zo Liang has obtained multiple degrees in business management, marketing, financial accounting, and econometrics from Monash University. He has more than ten years of experience in technology, culture, and entrepreneurship, and has accumulated rich experience and resources in the traditional financial field. At the same time, Zo Liang has also been active in the field of venture capital and has a keen sense of the latest narratives in the venture capital field. Therefore, with the rise of the concept of Web3, he quickly captured the huge opportunities in the integration of traditional finance and Web3.

When talking about the reason for founding TinyTrader, Zo Liang said that part of the reason was that he saw the huge growth potential in the Web3 field, but at the same time he also found that the quality of the trading infrastructure in this market still had a lot of room for improvement. Therefore, he hopes to introduce some mature products in the traditional financial field into the Web3 market to provide better trading services for this market.

Zo Liang introduced that TinyTrader currently has six main product lines, as follows:

The first product line is TT0, a spot trading system to meet the most rigid and high-frequency needs of customers;

The second product line is TT1, the contract trading system. In addition to providing the most common perpetual contract services, TinyTrader can also provide CFD services that are less used in the industry.

The third product line is TT2, the options trading system, which is the first white label solution provider on the market to provide this service. Considering the huge incremental potential of the options market, TinyTrader also regards TT2 as its core product line.

The fourth product line is TT4, which focuses on adding fiat currency support to the matching engine and integrating cryptocurrency and foreign exchange trading systems.

The fifth product line is TTHub, which corresponds to the liquidity aggregation system.

The sixth product line is TTMarket, which aims to provide customers with other third-party services, such as payment, KYC, compliance, etc., so as to build a more complete application ecosystem.

It is worth mentioning that for each product, TinyTrader provides two service modes - development mode and full-stack mode. In the development mode, TinyTrader only provides a development toolkit, which customers can use to build their own systems. This mode is more suitable for customers with certain independent development capabilities; in the full-stack mode, TinyTrader provides a complete "one-stop" service, covering all system development work. Of course, the service fees of TinyTrader will vary depending on the mode.

Combining the product line, it is not difficult to find that although TinyTrader provides a full set of trading infrastructure, the derivatives business represented by contracts and options is still the focus of its products.

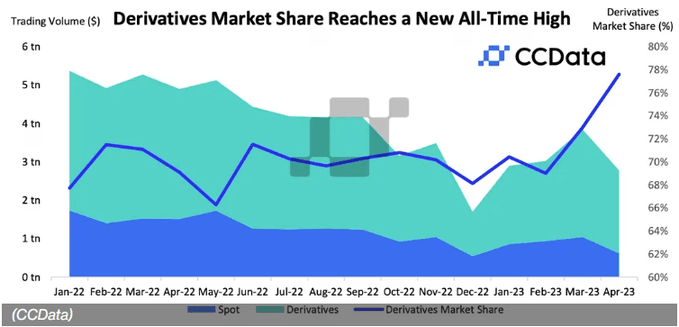

This is not difficult to understand. A recent report released by CCData shows that over the past three years, the proportion of spot trading volume and derivatives trading volume in the cryptocurrency market has undergone a disruptive change, and derivatives now occupy an absolute dominant position.

As of April this year, the proportion of derivatives trading volume has risen to a historical peak of 77.6%, compared with only 22.4% of spot trading volume. Whether from the current market structure or the trend of share changes, the importance of derivatives business to exchanges is self-evident.

From the internal structure of derivatives, the current market's main trading volume is concentrated on perpetual contracts, while the trading volume of CFDs and options-related products is still relatively small. The Block data shows that in May this year, the total trading volume of Bitcoin futures reached 743 billion US dollars, while the trading volume of Bitcoin options was only 19 billion US dollars, a difference of dozens of times.

Bitcoin futures trading volume, in trillions

Bitcoin options trading volume, only needs to be calculated in billions

In a report on derivatives released at the beginning of the year, top market maker Jump Crypto also pointed out that the trading volume of cryptocurrency options only accounts for 2% of the spot trading volume, but in the U.S. stock market this figure is as high as 70%, a difference of 35 times.

The structural imbalance means that although the current market competition surrounding perpetual contracts has entered a white-hot stage, the market competition surrounding new derivatives such as options is still in a very early stage, and there may still be opportunities for a group of new players to emerge in these areas.

Zo Liang added that, corresponding to each product line, TinyTrader's target customers mainly include five groups, among which the main customer groups are cryptocurrency exchanges and traditional foreign exchange brokers, but TinyTrader will also provide services to some game companies, market makers and other companies that want to enter the cryptocurrency industry.

For cryptocurrency exchanges (especially those with only spot business), Zo Liang pointed out that most of these customers are facing severe revenue and growth problems. It is difficult to guarantee continuous customer acquisition and positive profits by relying solely on spot business. In addition, due to differences in regulatory policies in various jurisdictions, most customers have certain compliance issues. The derivatives services and compliance support provided by TinyTrader can solve these two pain points.

As for traditional forex brokers, Zo Liang pointed out that most of these clients choose TinyTrader due to the diversification of their investment portfolios and businesses, especially after MT4 and MT5 encountered regulatory issues in the traditional financial field, many of these clients are facing greater revenue pressure. Due to the need to increase revenue, they also have the potential motivation to enter the Web3 market from the traditional stock, private equity, and foreign exchange industries.

Four major advantages build TinyTrader's moat

As the institution behind the institution, white label solution providers are somewhat unfamiliar to many people in the industry. Some readers may know that companies like Chainup and B2B roker are also providing similar services, but it is difficult to know the service differences and competitive situation between different service providers.

In this regard, Zo Liang stated that TinyTrader has four service advantages that other competitors cannot provide, and these advantages have become the moat that consolidates TinyTrader's market position.

The first advantage is that TinyTrader's services span the traditional financial and Web3 fields, and can provide a high-performance, low-latency transaction matching engine that supports both fiat currency and cryptocurrency. Its product model has been maturely tested in the traditional financial field and is relatively more trustworthy.

The second advantage is that TinyTrader focuses on derivative services and is the world's first white label solution provider that can provide a full range of services including perpetual contracts, CFDs, options, liquidity services, etc.

The third advantage is that TinyTrader is willing to help customers grow together. The reason for this is that TinyTrader can help customers make markets and provide risk control support; secondly, TinyTrader accepts a payment method of revenue sharing. Unlike other service providers who only accept one-time payments, TinyTrader's payment method means that it is willing to tie its own profits to those of its customers, which also indirectly demonstrates TinyTrader's confidence in the competitiveness of its own products.

The fourth advantage is that TinyTrader has a deployment efficiency far exceeding that of its competitors, and the core trading system can be launched in as fast as seven days. Zo Liang added that, in contrast, a well-known white label service provider in the industry takes at least two months to deploy.

From competition among exchanges to upgrading the financial world

In the conversation with Zo Liang, we repeatedly talked about the development of the exchange track and the role TinyTrader can play in this evolution. In his opinion, evaluating the development trend of the exchange track needs to be viewed from both internal and external directions.

Looking inward, although the top exchanges have shown a near-monopoly in the current stock market, there are actually many gaps under the shadow of the top exchanges - for example, the imperfect derivatives structure. In addition to perpetual contracts, there is still a relatively broad space for growth in contracts for difference and options. For another example, it is difficult for the top exchanges to use unified compliance standards to meet the regulatory requirements of different jurisdictions, which gives many regional exchanges the opportunity to counterattack in their "three-acre land" - these gaps are precisely the opportunities for small and medium-sized exchanges to break through.

Looking outward, more and more traditional financial players are entering the market with the support of service providers such as TinyTrader. On the one hand, this will inevitably intensify the competition in the entire exchange track, but at the same time, with the inherent resources of these new players, it may also indirectly bring new growth to the Web3 market.

In the following bull-bear cycle, the exchange track is bound to usher in new changes, but no one can predict when and who will be the breakthrough player. For small and medium-sized exchanges that are determined to catch up, all they can do is to improve their internal strength and wait for the opportunity, and this is exactly the value of white label service providers such as TinyTrader as "water delivery".

Looking into the more distant future, as the concept of Web3 matures further, TinyTrader also hopes to play a bridging role, bringing innovative concepts and technological achievements in the Web3 field back to the traditional financial field, improving the operation and settlement efficiency of the financial system, and thus contributing to the upgrade of the entire financial world.