This article briefly:

Despite a surge in savings rates, traditional savings accounts have declined, while Bitcoin wallets have surged.

· The evolving U.S. banking crisis led to changes in financial behavior, with $550 billion transferred from small to large banks.

Bitcoin’s growing popularity as a trusted investment and savings alternative marks a significant shift in global finance.

In an almost counterintuitive development, savings rates in the United States have reached their highest level in 15 years. Given the higher returns they now offer, one would normally expect such a move to encourage more deposits in savings accounts. However, an unexpected trend has been observed - despite the attractive interest rates, fewer Americans are choosing to keep their money in savings accounts.

The number of savings accounts has fallen despite rising interest rates. This surprising turn of events reflects a major shift in investor behavior and trust, away from traditional banking methods and towards alternative investing and savings channels.

Trust in traditional savings accounts declines

The shift away from savings accounts may be partly due to the increased scrutiny that traditional bank customers are experiencing. It has become common for even routine activity to be flagged as “suspicious,” which can lead to inconvenient account freezes.

This strict oversight, intended to deter illegal activity, is causing disruption to genuine account holders, sowing seeds of distrust.

"I didn't get any warning or red flags, and my bank account was shut down out of the blue," said former Chase customer Naafeh Dhillon.

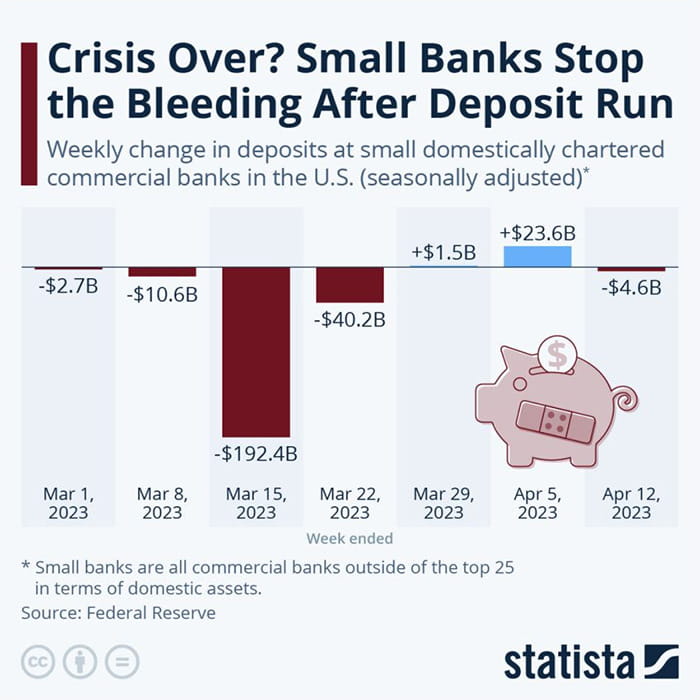

The plummeting trust in traditional savings accounts isn’t just the result of bank regulatory actions. The current banking crisis in the U.S., which has led to a massive cash withdrawal from financial institutions large and small, has compounded the problem.

JPMorgan Chase estimates that a massive $550 billion in deposits moved from small and regional banks to large banks and money market funds in the two weeks after the collapse of Silicon Valley Bank and Signature Bank.

"Market volatility always gets money moving. The biggest concern right now is: Is my money safe? How can I make it safer?" said Danielle Lucht, a financial adviser at Everwell Financial. People who have cash in simple savings accounts are taking advantage of the opportunity to move funds.

Smaller banks, in particular, have borne the brunt of the outflows because, unlike larger institutions, they are more vulnerable to financial distress in the event of large withdrawals due to their limited operating scale and capital reserves.

Despite the massive cash outflows, financial regulators insist the U.S. financial system remains sound. They point to high levels of capital reserves held by banks and the strength of the regulatory framework put in place after the 2008 financial crisis.

"The federal government took strong action to shore up public confidence in the banking system following the failure of two large regional banks. Since then, the situation has stabilized. Total deposit outflows have stabilized. The Federal Reserve's term funding programs for banks and the discount window are operating as intended. The United States banking system remains strong, as are our community banks. Liquidity and capital in the system are strong," said Treasury Secretary Janet Yellen.

However, the scale of the withdrawals highlights a deep-seated shift in public perception of the stability and trustworthiness of the traditional banking system.

In addition, external factors such as fluctuating inflation rates and socioeconomic shifts have also played a role. In particular, younger generations—Millennials and Generation Z—have proven to be more financially savvy, reducing their reliance on traditional savings mechanisms.

Amid all of these factors, an unexpected alternative is gaining ground – Bitcoin.

Rising Star: Bitcoin Wallets Surge

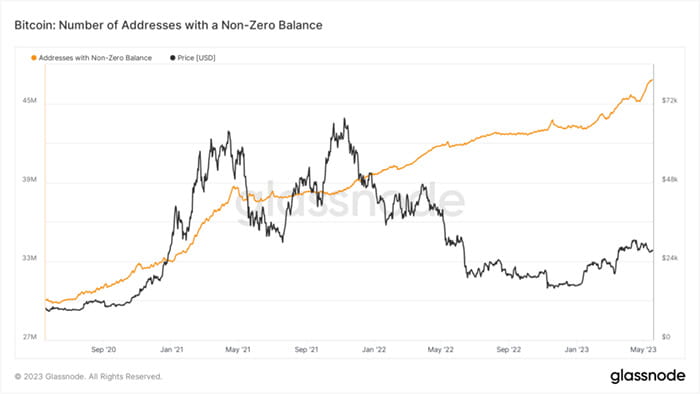

In contrast to the downturn in savings accounts, the number of non-zero Bitcoin addresses hit an all-time high. This growth shows that people are increasingly interested in cryptocurrencies despite the volatility of the market.

On-chain data from Glassnode shows a surge in the number of new Bitcoin wallets created each day. More importantly, there has been an increase in non-zero balance Bitcoin wallets, exceeding 48 million.

This upward trend indicates that people are increasingly accepting cryptocurrencies like Bitcoin as a viable investment and savings option.

More individuals and businesses are beginning to trust cryptocurrencies, increasing their use. Bitcoin's decentralized nature and high return potential have attracted those who are frustrated with the traditional banking system.

While the anonymity and independence offered by Bitcoin are appealing, another important aspect of its appeal is its scarcity. The 21 million BTC token cap instills a sense of exclusivity that adds to the digital currency’s appeal.

As more and more people strive to gain access to this limited resource, the value of Bitcoin continues to soar.

Additionally, Bitcoin provides a level of transparency that traditional financial systems cannot. The blockchain records all transactions, making them accessible to anyone, anywhere. This accessibility builds trust among users and fosters a sense of community.

Global financial scenario: Ripple effects of changing investor behavior

This shift is not limited to the United States. It is emblematic of a broader global trend. The global economic environment has been characterized by volatility, with corresponding fluctuations in traditional asset markets. Global investment flows have been redirected, causing fluctuations in the value of strong currencies such as the U.S. dollar.

Given these trends, Bitcoin appears to be on track to becoming a mainstream investment option. While still popular, traditional savings accounts are seeing a shift in user behavior. As this trend continues, banks must innovate to stay relevant in an increasingly digital financial environment.

As more individuals and businesses trust and understand cryptocurrencies, their adoption rate is likely to increase. As a result, global regulators may need to update their regulations to accommodate this new form of digital assets.

While the decline in savings accounts and the proliferation of Bitcoin wallets may seem contradictory, they are part of a broader shift in global financial behavior. How this shift will play out remains to be seen, but current trends suggest that digital currencies will play an important role in global finance in the future.