1. The current market consensus (Bloomberg survey median): Total CPI rose 0.20% month-on-month and 5.1% year-on-year; core CPI rose 0.40% month-on-month and 5.6% year-on-year. I expect total CPI to rise 0.24% month-on-month and core CPI to rise 0.35% month-on-month. In other words, it is expected that tonight's CPI data will most likely meet expectations.

2. The differences from the market consensus are:

1) According to consensus expectations, the total CPI is 0.2% month-on-month, which is significantly lower than the core CPI month-on-month 0.4%. The implicit meaning here is that CPI energy prices will have significant negative growth. Although I also estimate that CPI energy prices will be negative growth, but the negative The extent is not that great;

2) I still estimate that the growth rate of CPI rent will slow down significantly, and its contribution to the total CPI month-on-month will drop from 0.26% in February to 0.21%;

3) I read multiple seller reports that the CPI second-hand car price is estimated to have rebounded significantly. I also gave a positive increase, but the magnitude is still small, mainly because of the Manheim used car price index and the Black Book second-hand car price index. The car price index is 1-2 months ahead of the CPI for used cars. Now we need to look at the readings of these two indices from January to February.

3. If there are any areas that exceed expectations (I give it a probability of about 10%), I tend to think that the total CPI will increase by 0.3% month-on-month and the core CPI will increase by 0.3% month-on-month, that is, the total CPI will be higher than market expectations, and the core CPI will be lower than market expectations. The implicit logic here is that I think the market has overestimated the decline in CPI energy prices.

4. I think this number will most likely have a neutral or optimistic impact on the market. As for the next few months, I still clearly see inflation going down. In terms of operational strategy, I will continue to be bullish in April-June, and by the middle of the year, I tend to reduce my holdings in US stocks, including cryptocurrencies:

First, by the middle of the year, a considerable increase had already accumulated. Second, by the middle of the year, the total CPI had fallen to just over 3%, entering a bottleneck period. It would be extremely difficult to drop further to just over 2%. Third, the closer we get to the end of the year, the greater the probability of a recession. We are currently in the "late cycle", and this judgment is very clear. We will see this at that time, including looking at the first quarter report of U.S. stocks.

The most important thing is “wait and see” and “expect prices to rise until mid-year”.

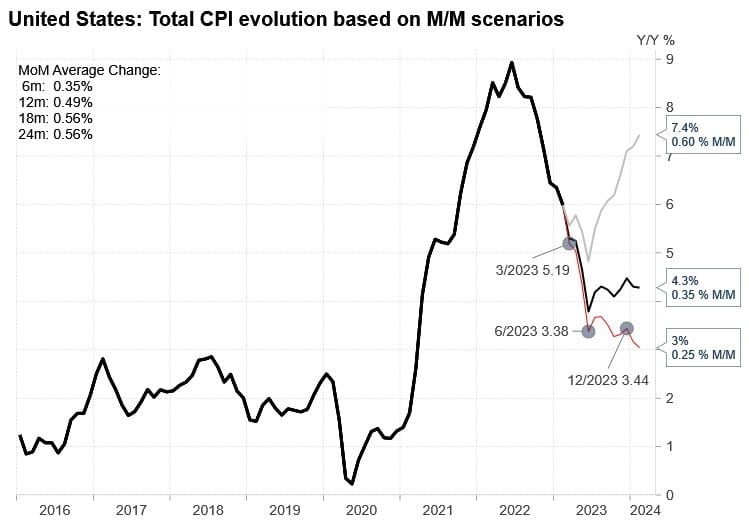

The downward trend of CPI can be divided into two stages:

1. Around the fourth quarter of last year, it was the first stage of rapid decline;

By the beginning of this year, the entire market was doubting the sustainability of the downward trend in inflation, which corresponded to the decline of the US stock market in February (economic data exceeded expectations, there was no recession, demand was strong, and inflation could not go down). This period was considered an expectation of downward inflation and a short bottleneck period;

2. We are about to enter the second stage of rapid downward inflation. The Headline CPI will increase from the current 6% to just over 5%, just over 4%, and just over 3% month by month in the coming months.

Although this chart is year-on-year and there is a base effect, it doesn’t matter as the base effect is also very important.

By the time the June CPI was released in mid-July, it had already reached just over 3%. It will be very difficult to get it to just over 2% going forward.

This is the core logic that I will continue to see in the next three months, but I tend to reduce my holdings after the middle of the year.