Written by: @Yinan_cycle

(This article first appeared in PANews: The RWA track that large organizations are laying out may be the beginning of the next round of narratives)

background

What is the original intention of encryption?

Is there short-term speculation through capital rotation games and inflationary rewards? Or improve the way society works by creating a more transparent, accessible and efficient global economy?

Everyone has their own opinion on this issue, but it’s undeniable that most of the crypto narrative right now is on-chain, with very few tangible real-world use cases that benefit ordinary consumers. With $867 trillion in traditional markets waiting to be disrupted by blockchain-based technologies, the opportunity to systematically improve the global economy is real.

Characteristics and current situation of decentralized finance

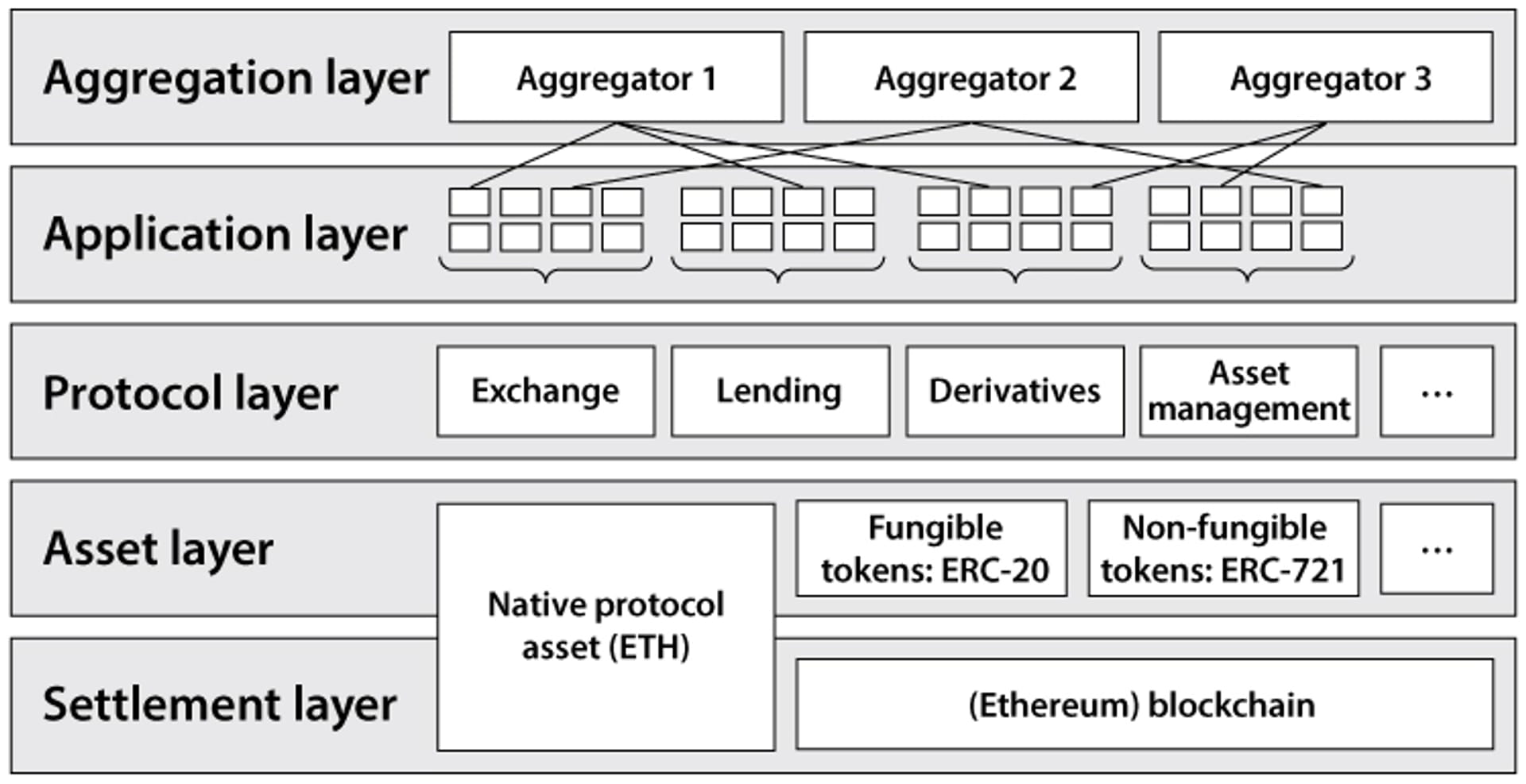

The initial application of blockchain is the creation and movement of tokens, and the emergence of DEFI has stimulated the potential of blockchain. Meanwhile DEFI applications benefit from the following properties:

Atomic Settlement: The combination of cryptography and decentralized consensus provides a strong final guarantee for economic transactions – reducing double-spend attacks and fraud in a tamper-proof manner, thereby increasing capital efficiency and reducing system risk.

Reduced costs: DeFi applications run more efficiently and autonomously because the need for intermediaries is minimized. This helps reduce the switching costs of moving funds across applications, creating an efficient market for application-level fees. Scaling technology also makes microtransactions feasible by reducing network-level fees.

Transparency: Public block explorers and data dashboards provide granular and clear insights into overall DeFi exposure and collateralization. Additionally, the source code of DeFi applications is open source and can be viewed by anyone.

Composability: Having a common settlement layer for running autonomous code enables permissionless composability between new and existing DeFi applications. Developers don’t have to worry about being de-platformed, further incentivizing collaboration.

User Control: Non-custodial asset management is enabled via private keys, allowing DeFi applications to interact with assets in a trust-minimized manner. Decentralized Autonomous Organizations (DAOs) also allow collective ownership of assets and applications.

Examples of decentralization include:

P2P payments (Lightning Network, Flexa)

Synthetic assets (Synthetix, Alchemix)

Spot trading (Uniswap, Curve)

Asset Management (Yearn, Beefy)

Loan market (Aave, Compound)

Insurance (Nexus Mutual, Unslashed)

Derivatives (GMX, dYdX)

Although DEFI does bring a lot of benefits, there is a major limiting factor that hinders the global promotion of DeFi: most of DeFi currently only constitutes a circular economy, which is almost the same as the existing global scale of traditional enterprises and services. There is no economic connection. Much of DeFi’s historical rapid growth has to do with the rise of the capital rotation game and unsustainable gains driven by inflationary token rewards. This is the equivalent of playing Minesweeper with a supercomputer: the potential is huge but not yet fully exploited.

The DEFI industry has flourished in the past two years, with TVL reaching its peak of 180 billion on December 2, 2021. However, with the occurrence of black swan events such as Luna and Ftx, and the advent of the bear market, DEFI's overall TVL has declined It has reached more than 57 billion, and due to the unsustainability of many protocols, the price of tokens has dropped by more than 90% from its high point, and the overall rate of return is also decreasing, gradually approaching the rate of return of traditional finance (TradFi).

Advantages and disadvantages of DeFi and TradFi

DeFi:

Transparency on the chain enables monitoring of fund movements

The composable smart contract can divide and isolate funds.

The flexibility and efficiency brought by models such as AMM automatic market makers

Lower the entry threshold for small and medium-sized investors and connect global markets

TradFi:

Investment access threshold is high and link market is limited

The access of intermediary institutions such as middlemen, background checks, and audits leads to increased marginal costs and reduced efficiency.

What is RWA

Refers to tangible assets that exist in the physical world. Examples include real estate, merchandise and art. Real-world assets are an important part of global financial value. The global real estate value in 2020 was US$326.5 trillion, while the market value of gold was US$12.39 trillion.

The financial economy is not static. From the use of clay tablets to track debts in the Babylonian Empire in 3000 BC to paper to digital, finance has been evolving. Despite this transformation, financial records still occur in isolated ledgers and are inefficient. DEFI's interoperability and decentralized liquidity provide opportunities for traditional assets.

The most popular RWA examples: Cash, metals (gold, silver, etc.), real estate, corporate debt, insurance, payroll and invoices, consumer goods, credit notes, royalties, etc.

The organization’s layout on the RWA track

Goldman Sachs launches digital asset platform for European Investment Bank’s €100 million blockchain bond.

Hamilton Lane's $2.1 billion flagship direct equity fund is now available for securitized investing through Polygon.

Siemens recently issued a €60 million digital bond on the public Polygon mainnet. The digital bond, which has a one-year maturity, was issued under the German Electronic Securities Act (eWpG) and was purchased by DekaBank, DZ Bank and Union Investment. By issuing bonds on a public blockchain, Siemens is able to eliminate the need for paper-based global certificates and central clearing, allowing bonds to be sold directly to investors without the need for banks as intermediaries.

Mitsui Company realizes asset management through digital securities, and the company provides stable operation of real estate and infrastructure investments to retail customers. The tokenization of these digital securities is done in partnership with LayerX and issued on a chain owned by SBI and Nomura Consortium.

The stable currency DAI issued by MakerDAO is the biggest manifestation of the adoption of RWA. Currently, the protocol has over $680 million worth of RWA-backed decentralized stablecoin DAI. By introducing RWA as collateral, MakerDAO is able to expand the amount of DAI issued to the market, strengthen its peg stability, and significantly increase protocol revenue (about 70% of revenue in December 2022 came from RWA).

Aave’s real-world assets are online.

Use cases of RWA track in DEFI

Stablecoin

Stablecoins are a perfect example of real-world assets being used successfully in DeFi, with three of the top seven crypto tokens by market capitalization being stablecoins (a total of $136 billion). Issuing companies like Circle maintain audited reserves of USD assets and mint USDC tokens for use across DeFi protocols.

synthetic tokens

Synthetic tokens represent another use case involving bridging RWA to DeFi. Synthetic tokens allow for on-chain trading of derivatives linked to currencies, stocks and commodities. At the height of the 2021 bull run, leading synthetic token trading platform Synthetix had $3 billion worth of assets locked in its protocol.

loan agreement

DeFi lending business models provide the most cost-effective way to pool and distribute funds among a large number of lenders and borrowers. It eliminates intermediaries and automates the flow of funds while providing users with relative anonymity.

Besides stablecoins, the most popular underlying asset class for RWAs is real estate. This is followed by climate-related fundamentals (such as carbon credits) and public bond/equity fundamentals. Secondly, the basics of emerging market credit (mainly corporate bonds), etc.

RWA related agreements

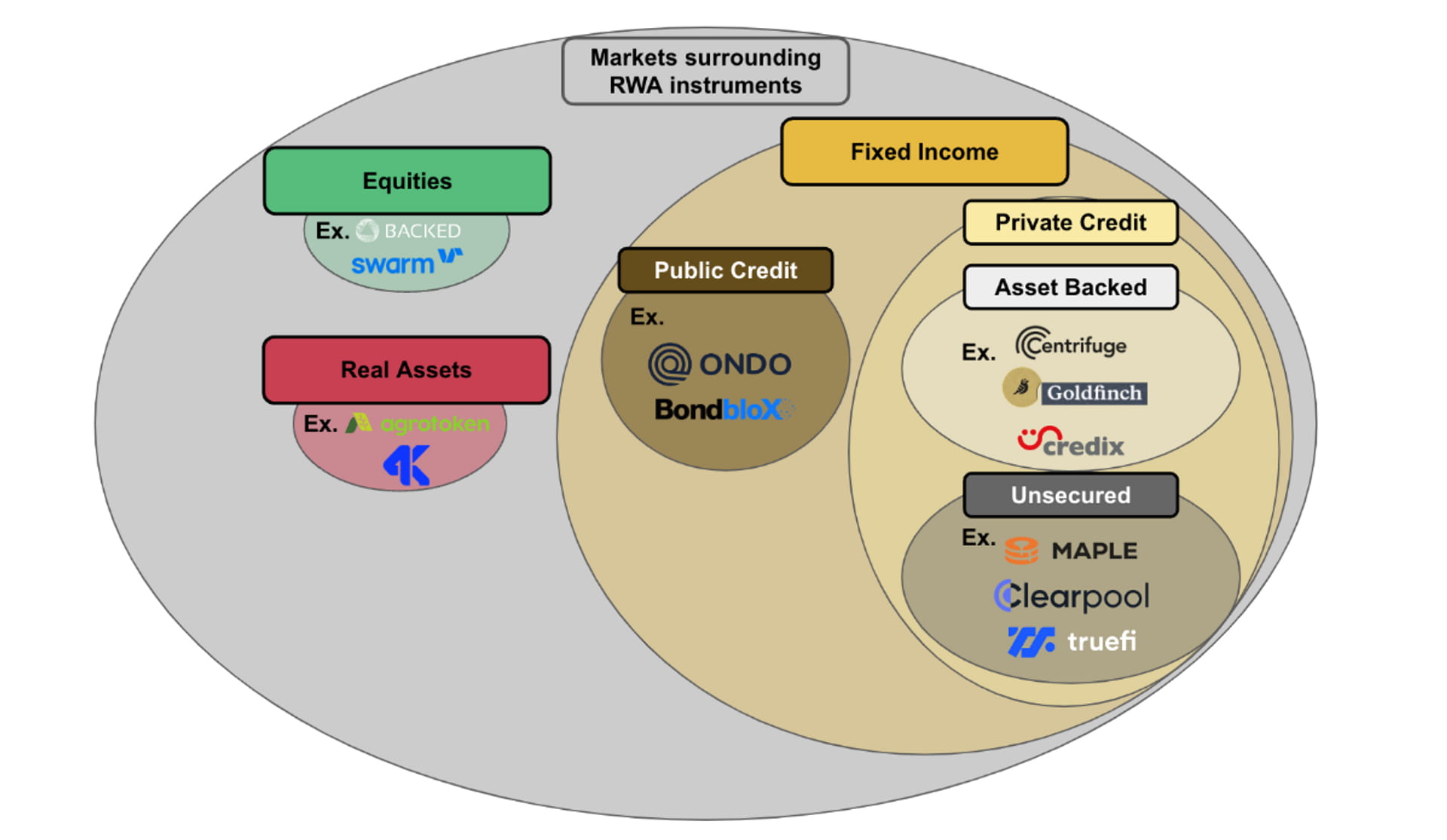

The classification of protocols on the RWA chain is mainly divided into two categories:

Stocks and real asset markets: Stocks and real asset markets are relatively small in the RWA space, and there are currently few protocols built in this space. One reason may be that stocks or real assets (such as commodities) are usually traded in the open market and are therefore highly regulated. In most jurisdictions, public stocks and real assets are only offered by registered and vetted exchanges. Another reason is that equity and real asset instruments often involve off-chain physical ownership of the underlying asset class. This adds a layer of operational complexity, as the equity/real asset agreement does not just facilitate a financial contract on paper, but in reality must store the equity/real asset and be able to transfer the equity/real asset in the event of redemption of ownership. Supports stock and real asset market protocols such as Backed Finance.

Fixed income: divided into public credit and private credit. Fixed income is the main market in the RWA space. Compared with equity or real asset markets, RWA-based fixed income markets are more active in terms of transaction flow, richer in terms of products, and more diverse in terms of market participation. Supports private credit protocols such as Centrifuge, Goldfinch or creditx.

List some RWA on-chain protocols

Backed Finance — a Switzerland-based tokenized RWA startup — recently launched its first product, bCSPX, which stands for tokenized S&P 500 ETF shares. Supported tokens can be freely transferred between wallets and support 24/7 capital market trading. Backed is one of the few protocols to offer public equity RWA, which requires registration under the Swiss DLT Act and must fully back each RWA asset with ownership of the underlying shares. In the event of a redemption, Backed Finance must sell the shares held by users and then coordinate whether they wish to be repaid in cash or cryptocurrency. On-chain equity alternatives that do not link to RWA include Synthetix.

Ondo Finance — a DeFi platform for tokenizing RWA — recently tokenized short-term U.S. Treasuries, investment-grade bonds, and high-yield corporate bonds. Ondo also launched Flux Finance, a DeFi lending protocol for borrowing permissionless stablecoins based on tokenized U.S. Treasuries.

Maple Finance — a blockchain-based credit marketplace with nearly $2 billion in loans issued — is planning to expand into accounts receivable financing, with a size of up to $100 million, and support U.S. Treasury and insurance refinancing.

Centrifuge (CFG) — an on-chain ecosystem for structured credit focused on securitizing and tokenizing previously illiquid debt, has raised $298 million in total assets. Its tokenized assets have been integrated across DeFi, including $220 million in risk-weighted assets on MakerDAO.

Goldfinch (GFI) — a decentralized credit protocol — has $101 million in active loan value. The platform allows for the creation of junior and senior tranches for assets focused on emerging markets, enabling fine-tuning of risk/reward profiles.

Blocksquare (BST)—It started working on BST as early as 2018 and has been an asset tokenization team for many years. Its product, Ocenpoint.fi, has US$45 million in real estate assets under management, an average APY of 4.9%, and 52 real estate projects located in 12 locations around the world. Formal RWA projects belong to the serious direction of tokenization.

As of now, credit protocols offer higher yields than most DeFi protocols. The APY provided by each agreement is as follows:

Maple Finance:8.31%

Centrifuge:9.31%

Goldfinch:8.31%

As of now, the default amounts of these agreements are as follows:

Maple Finance: $69.3 million

Centrifuge: $2.6 million

Goldfinch: Never faced a default

Future Trends

Layer1 public chain based on RWA

Currently, the most popular RWA protocols are deployed on permissionless layer 1 blockchains such as Ethereum and BNB. While there are some benefits to deploying to a permissionless blockchain, such as ease of development and crypto-native network effects, there are also operational and technical disadvantages.

Structurally, permissionless blockchains are public and not subject to any regulatory or permissioned logic. Many RWA protocols, particularly those that bring securities or credit-based assets to the blockchain, are subject to regulatory compliance and limit the use of their protocols to entities that have undergone rigorous KYC/KYB processes. The permissioned nature of these RWA protocols is structurally inconsistent with the public, free-floating access provided by permissionless blockchains. Therefore, current RWA protocols adopt a combination of soft and hard solutions to limit access to their platforms and comply with regulations (e.g. manual whitelisting of wallet addresses, restricted front-ends, token-gated account access).

Operationally, established token standards and transparency of permissionless blockchains may not be appropriate in the context of RWA protocols. A token standard on permissionless blockchains that allows the development and efficient operation of smart contracts for DeFi applications. However, these conventions can be restrictive and, operationally, often do not represent the characteristics of real-world assets. For example, if a corporate bond has a balloon payment at maturity and would be marked as RWA, then current marking standards may not capture the arbitrary payment logic of this type of asset.

Furthermore, by definition, all operations and transactions on a permissionless blockchain are transparent and can be reviewed on a public ledger. For some RWA markets, there may be some sensitive information that needs to be kept confidential. For example, if a property is to be represented as a RWA, the person selling the property or the person purchasing the property may not want to disclose the exact location due to privacy concerns. In response to structural and operational constraints, a custom Layer 1 is being developed to meet the unique, permissioned needs of the RWA protocol.

For example, Inatain Markets recently launched an Avalanche subnet designed specifically for on-chain issuance and trading of asset-backed securities. Another example is Provenance Blockchain, a layer 1 built for seamlessness and security.

Summarize

The exhaustion of DEFI narratives and the market for real assets. The characteristics of DEFI such as composability, transparency, low fees and high efficiency have brought more opportunities to the pain points of traditional real assets such as inefficiency and high cost. For example, it provides more possibilities for offline corporate loans, which were originally only available to groups in a certain region. After tokenization, it can be connected to the global market, allowing borrowers and lenders to provide matching transaction pools. Recently, with the crisis of trust caused by bank bankruptcy, the market value of gold tokenization has exceeded 1 billion US dollars, and the narrative of DEFI empowering offline assets may be coming.

Related Links

Chainlink blog: Tokenizing Real World Assets (RWA): Scaling DeFi to a global level

Blockworks: What are real-world assets? DeFi latest yield

Coingecko: Real World Assets (RWAs) in the crypto space and RWA tokens worth watching

RWA protocol data analysis website: https://app.rwa.xyz/#protocols

Binance RWA research report PDF: chrome-extension://bocbaocobfecmglnmeaeppambideimao/pdf/viewer.html?file=https%3A%2F%2Fresearch.binance.com%2Fstatic%2Fpdf%2Freal-world-asset-report.pdf