Source: https://twitter.com/thiccythot_/status/1643753971172151298?s=20

Author:Alex

Compiled by: TechFlow

Today's digital asset market has developed into a huge global industry, attracting more and more investors and institutions to participate. However, as the market continues to expand and the number of market participants increases, market stability and fairness have become an increasingly important issue.

Therefore, based on the recent Arbitrum incident, the author introduced the specific mechanisms of token market makers (MM) and the possibility of potential violations, and also put forward his personal opinion on the need for more disclosure of projects in this field.

Why do all current crypto projects have market maker (MM) transactions?

In the past, projects often promoted liquidity by providing tokens as incentives to on-chain pools, but now they provide incentives to complex market makers to provide liquidity on centralized exchanges (CEX).

This shift is intended to make price discovery more efficient and reduce costs for all parties involved.

On CEXs, price discovery is more efficient due to greater liquidity. Additionally, market makers are able to provide better bid and ask prices to buyers and sellers, making the market more attractive.

How do crypto projects incentivize market makers?

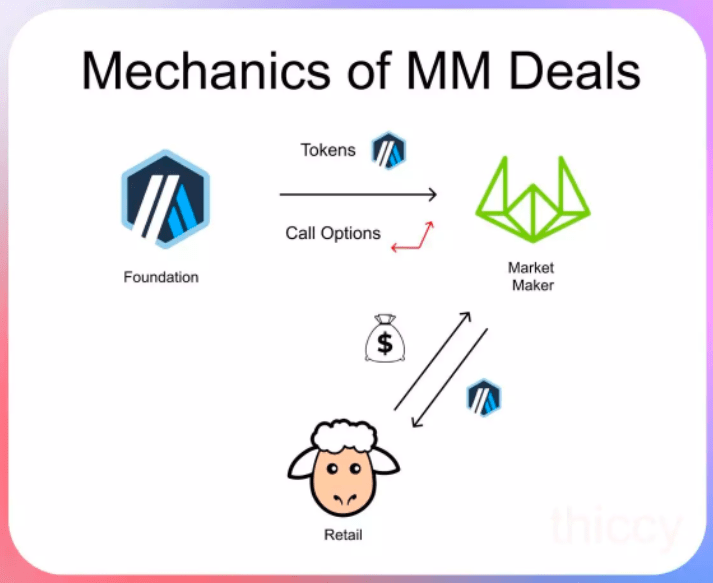

Typically, projects provide market makers with a one-year token loan, during which tokens are given with zero-cost subscription options. Specifically, projects lend tokens to market makers (usually 3-5) and require market makers to guarantee market size and spreads during the loan period.

Why do projects need to lend coins to market makers?

Market makers need token loans to ensure that they have enough inventory in their operations to cope with any excess buying demand that may arise.

At the same time, market makers need to conduct efficient borrowing operations in order to offset excess buy-side demand when necessary.

Token loans typically have zero or very low interest rates. While market makers need tokens to provide liquidity, they don’t want to incur huge borrowing costs.

Therefore, token lending is a common incentive mechanism that can provide market makers with the necessary tokens to support market liquidity while also reducing the cost burden of market makers.

Why give call options to market makers?

Market makers need to pay a price to provide liquidity services. Projects usually choose to use tokens instead of cash to pay this price because tokens are more liquid and operable.

However, in order to prevent market makers from immediately selling tokens and thus affecting the market price and the interests of investors, project owners usually give market makers subscription options to achieve incentive consistency. If the token price rises, market makers can get more benefits, and project owners can also benefit from the appreciation of tokens.

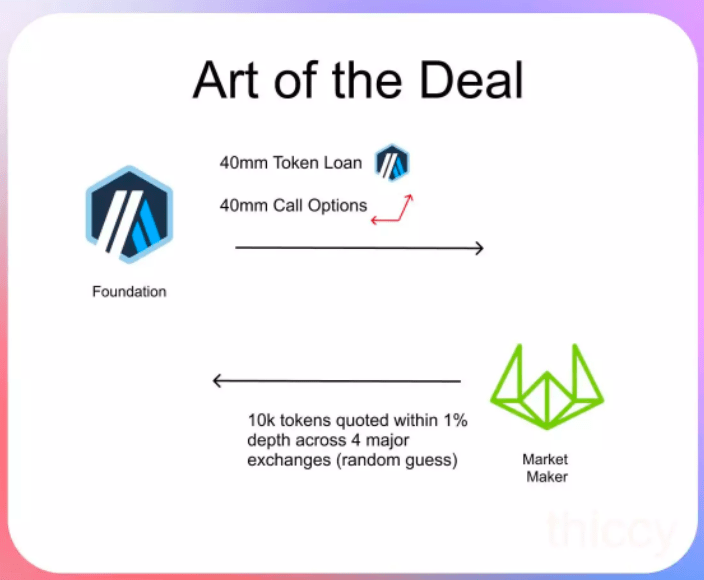

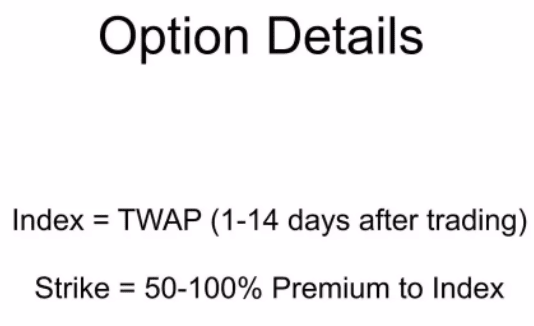

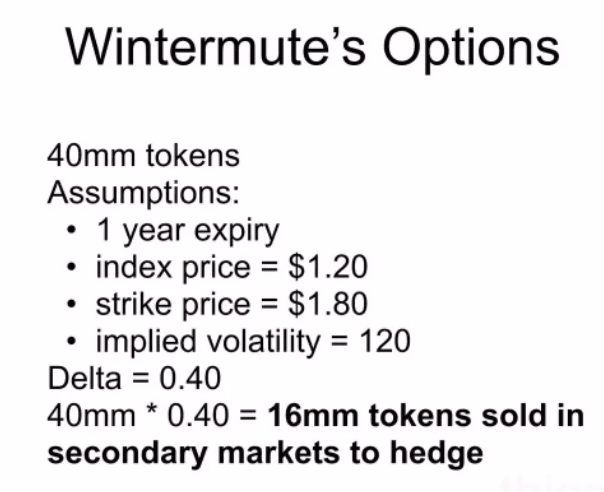

How to determine the strike price of a call option if the token has not yet started trading?

In this case, the project party will choose to set the strike price of the call option to a premium of 50% - 100% of the index price. Since the index price can usually be determined on the chain or in other markets, the strike price does not need to be known when the transaction is reached.

This method of setting the strike price of call options can provide market makers and project parties with a certain degree of flexibility and reduce trading risks. If the token price is higher than the strike price, the market maker can earn the difference profit and realize income. If the token price is lower than the strike price, the market maker can choose not to exercise the call option and give up the income.

The mechanisms associated with token market makers are not inherently malicious. The problem is that these mechanisms are often not disclosed to retail investors.

Therefore, this makes open market participants feel unfair. They may not be able to learn important information about token prices and liquidity, and thus suffer losses in transactions. If the project party or market maker clearly communicates this information to investors, the entire market can be more transparent and fair, thereby reducing investor losses and improving the confidence of market participants.

Let’s look at the recent Arbitrum incident.

In the filing, there is no mention of the trading terms and conditions of the token market makers, making it difficult for investors to understand the market makers’ actions and potential impact.

More importantly, the document also does not clearly state whether Wintermute (the market maker) is an investor in Arbitrum, which could lead to conflicts of interest and moral hazard.

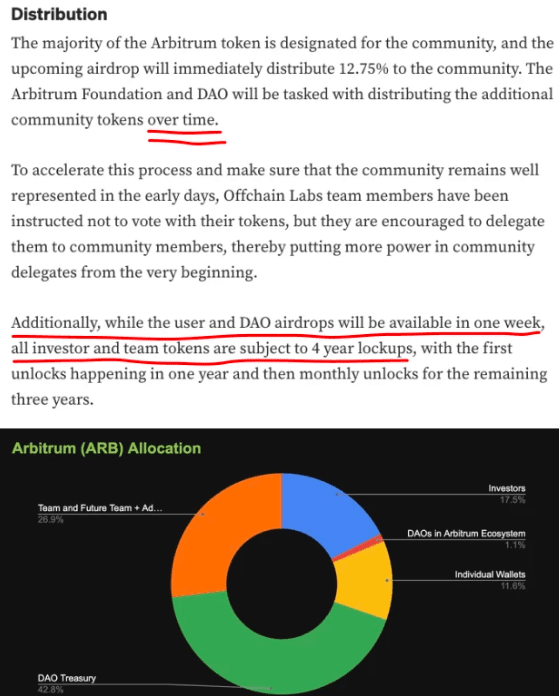

Retail investors made investment decisions based on the assumption that the 1.275 billion tokens mentioned in the document were the only supply on the secondary market. However, this was not the case, which led to some unexpected situations.

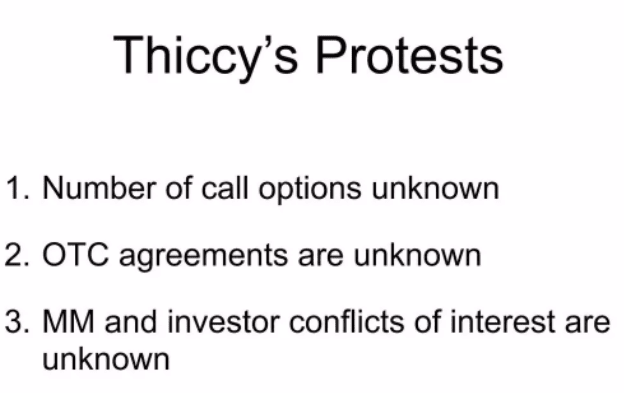

1. The number of call options is unknown

These call options essentially increase the circulating supply of the token and therefore cause the token price and liquidity to be affected.

In order to maintain market neutrality, market makers need to hedge the Delta of call options by selling tokens. In this process, market makers sell a large number of tokens, which actually increases the supply of tokens, but these data are not disclosed to investors in a timely manner.

It is reported that Wintermute (market maker) hedging transactions have added at least 16 million tokens to the secondary market, which is also one of the reasons for the unstable token supply and price fluctuations.

2. OTC transaction terms are unknown

Another concern is that the foundation sold $10 million worth of tokens through an over-the-counter transaction with Wintermute (a market maker).

However, these operations were not disclosed to retail investors before the transactions took place. In fact, investors did not learn of this information until after the transactions were completed.

At the same time, there is no mention in the original document whether the foundation has the right to sell tokens in such a short period of time.

3. Unclear positioning of investors and market makers

In the case of Arbitrum, it is unclear whether Wintermute (the market maker) was an investor in the project.

Especially for retail investors, it is very important to understand the relationship between investors and market makers. They should clearly understand the role of market makers in the market and the source of their profits in order to correctly assess the risks and opportunities in the market.

Here is a famous strategy from Alameda:

Retail investors were doubly hit by this incident, first by being forced to accept additional tokens being passed on to them without them being notified.

Arbitrum then tried to sneak in a fake decentralization plan, but was eventually uncovered, causing the token price to fall.

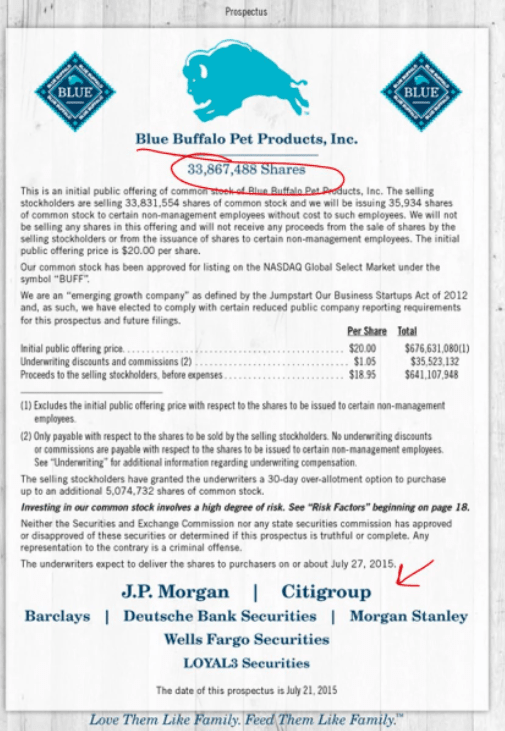

There is a reason why IPOs in Tradfi require the prospectus to clearly outline the following:

Number of shares issued;

Initial public offering price;

underwriters involved in the transaction;

Profits and dividends earned by underwriters.

This information is very important for investors as it provides comprehensive and transparent information about the company and its stock to help investors make informed investment decisions.

Of course, there is also a reason that insider trading laws exist. Participants who hold a large number of tokens or have insider information are required to publicly disclose their operations in the secondary market. This helps protect the fairness and transparency of the market.

However, in the cryptocurrency market, some non-compliant operations sometimes occur, such as releasing a large number of tokens into the market. These operations usually have an adverse impact on the market and cause damage to investors, which cannot be tolerated.

Transparency and fairness are very important for the development of the token market. The events of last week have caused great damage to the industry, and it also shows that there are some shortcomings and loopholes in the existing rules and mechanisms.

In the current token market, many investors and traders are facing problems of information asymmetry and market uncertainty. This situation not only affects the confidence and interests of investors, but also may hinder the development and innovation of the entire market.

Therefore, we need stricter supervision and more transparent market rules to promote market stability and reliability. Only by strengthening the transparency and fairness of the market can we attract more investors and participants to join this industry.

I believe we can build a social contract together that requires more transparent and open information and rules for future projects.

As investors and participants, we can take steps to achieve this goal. For example, we can avoid buying governance tokens that do not provide sufficient information and disclosures, or we can protect the fairness and transparency of the market by conducting more research, investigation and supervision of the market.

At the same time, token issuers and market makers also need to take responsibility and provide more information and disclosure to meet the needs of investors and the market. Only through cooperation and joint efforts can the token market be made safer, fairer and more reliable, thereby creating more opportunities and benefits for all market participants.