Yesterday (January 16), Federal Reserve official Waller made a speech. While acknowledging the prospect of a rate cut this year, he also downplayed market expectations for a rapid rate cut. He stated that policy formulation needs to be more cautious in the future to avoid excessive tightening. U.S. Treasury yields gradually strengthened during the day, with the ten-year yield returning to above 4%, at 4.06%, and the two-year yield now at 4.281%. The three major U.S. stock indices all closed lower, with the NASDAQ, S&P, and Dow Jones falling by 0.19%, 0.37%, and 0.62%, respectively.

Source: SignalPlus, Economic Calendar

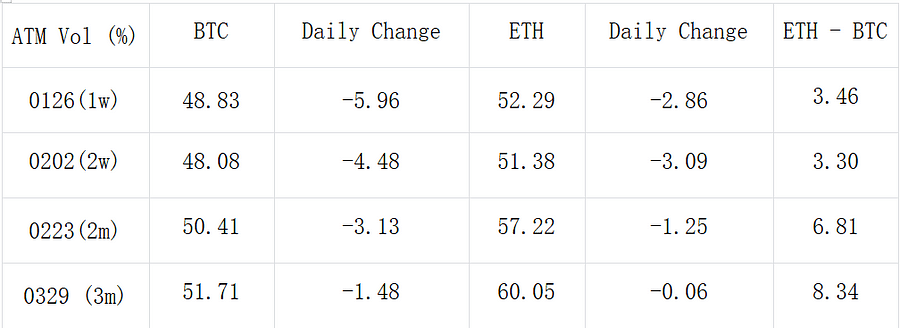

Source: Binance & TradingView

In the realm of digital currencies, the overall market situation remains the same, with BTC and ETH slightly rising to break through 43000 and 2600 respectively, before gradually giving back most of their gains. As a result, the implied volatility levels of both have been adjusted downwards again. The IV of BTC in the front end has returned to below 50% Vol, which is relatively low compared to the past three months. Although ETH has also experienced a slight decline, it has once again developed a Vol Premium of about 3 to 8% over BTC, overall being around the median of the past three months.

From a trading perspective, the Call Spread for 23FEB24 has once again gained favor in the market, represented by BTC 60000 vs 65000 and ETH 2700 vs 3200. Additionally, we’ve observed that under the current market conditions, which have persisted for over four days, the recent triangular bullish strategy has also attracted attention. For BTC, traders have reduced the cost of buying 2FEB Calls by selling 19JAN Calls, pushing the bet for volatility to occur to next week. Similarly, for ETH, there is a purchase of 2FEB Calls, but with a choice to sell further out 23FEB as a hedge.

Source: Deribit (As of 17JAN 08:00 UTC)

Source: SignalPlus

Source: SignalPlus

Source: Deribit Block Trade

Source: Deribit Block Trade