Produced by: OKLink Research Institute

作宇|Hedy Bi

One day before the news of the approval of the Bitcoin spot ETF application came out, SEC Chairman Gary Gensler tweeted on X to warn of the risks of virtual assets. It was this statement that made the market believe that the probability of approval of the Bitcoin spot ETF application increased, and the price of Bitcoin broke through the high of US$47,000 this morning.

Source: Bloomberg

Source: Bloomberg

Not only is the market sentiment so high, but applicants are also making adequate preparations. ARK Invest (ARK), an asset management company founded by Catherine Wood, will become the first Bitcoin spot ETF applicant to receive a final response from the SEC. At the end of last year, ARK sold all of its remaining GBTC positions and used half of the funds of about $100 million to purchase BITO, "possibly as a liquidity transition tool to maintain the beta value to Bitcoin" and include it in ARKW (ARK Next Generation Internet ETF) or ARKB (Ark 21Shares Bitcoin ETF, the Bitcoin spot ETF that ARK is applying for). All parties in the market are ready to go. If the US SEC approves the Bitcoin spot ETF, it also means that the 10-year protracted battle in which institutions have applied to the SEC for Bitcoin spot ETFs since 2013 but have been rejected is expected to end!

The United States will not give up its bargaining power from Wall Street easily. The passage of ETFs will bring about a superimposed effect of bargaining power.

If the threshold for spot ETFs is lowered, public funds, private funds and individual investors will be able to participate in the virtual asset market as easily as buying stocks on traditional stock exchanges, directly hold Bitcoin, and remove restrictions on compliance channels. The market effect brought by the amount of funds in the short term is only one aspect. The more critical thing is that the United States will enhance its bargaining power in the crypto market through ETFs and become the industry rule maker.

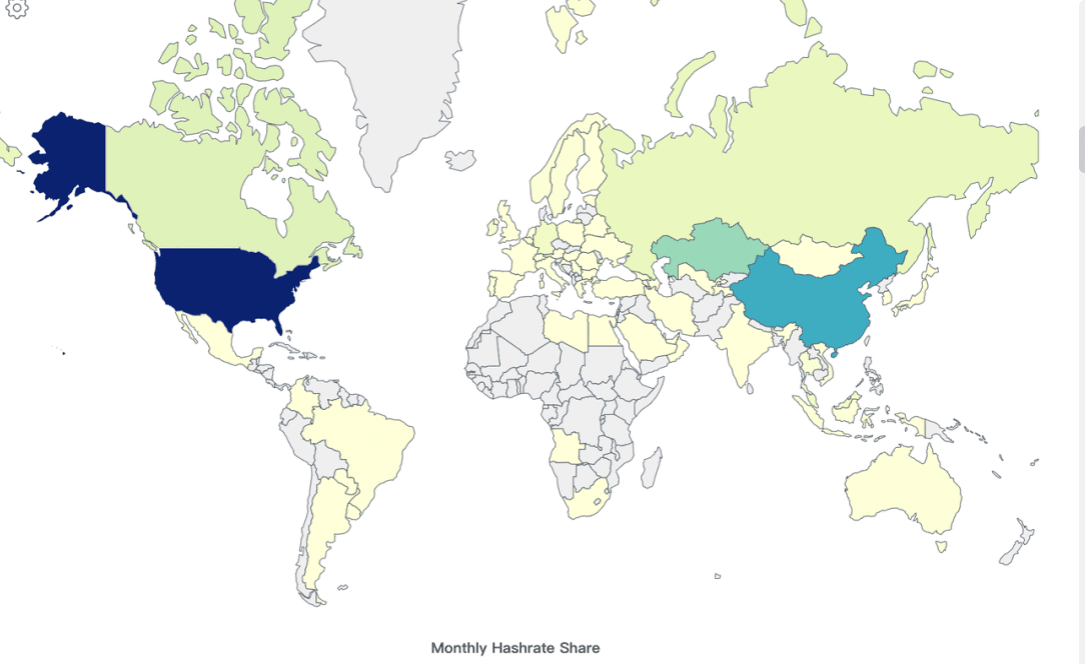

As the Bitcoin mining power has shifted from China to the United States, the United States’ Bitcoin computing power accounts for 40% of the world’s share, ranking first in the world. This means that the United States has already mastered its bargaining power on the supply side.

Figure: Global Bitcoin computing power source: worldpopulationreview.com

Figure: Global Bitcoin computing power source: worldpopulationreview.com

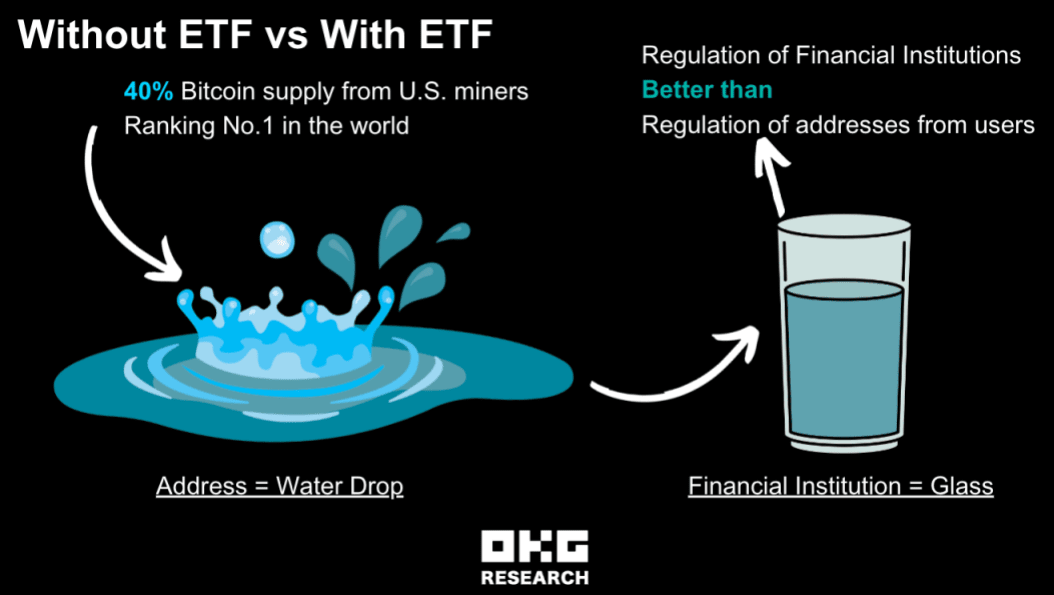

If the spot ETF is approved, it means that the position and transaction data of institutions will be disclosed, which will provide more market transparency for regulators and market participants. With this information, regulators can better supervise market activities and reduce the risk of market manipulation and fraud. As shown in the figure below, let's make an analogy. Although we know that "every drop of water" can be easily traced, tracked and verified on the chain, it is difficult for regulators to supervise "every drop of water". If we collect these water drops, put them in glass containers, and delegate such regulatory requirements to each "glass", regulators will be better able to formulate rules and manage.

For the United States, if the ETF is approved, it will establish the United States' position as the rule maker and market leader in the crypto market. Regardless of whether the Bitcoin spot ETF is approved or not, the United States will not easily give up this huge advantage.

Figure: OKG Research - ETF Compliance Channel vs. No ETF Compliance Channel

Figure: OKG Research - ETF Compliance Channel vs. No ETF Compliance Channel

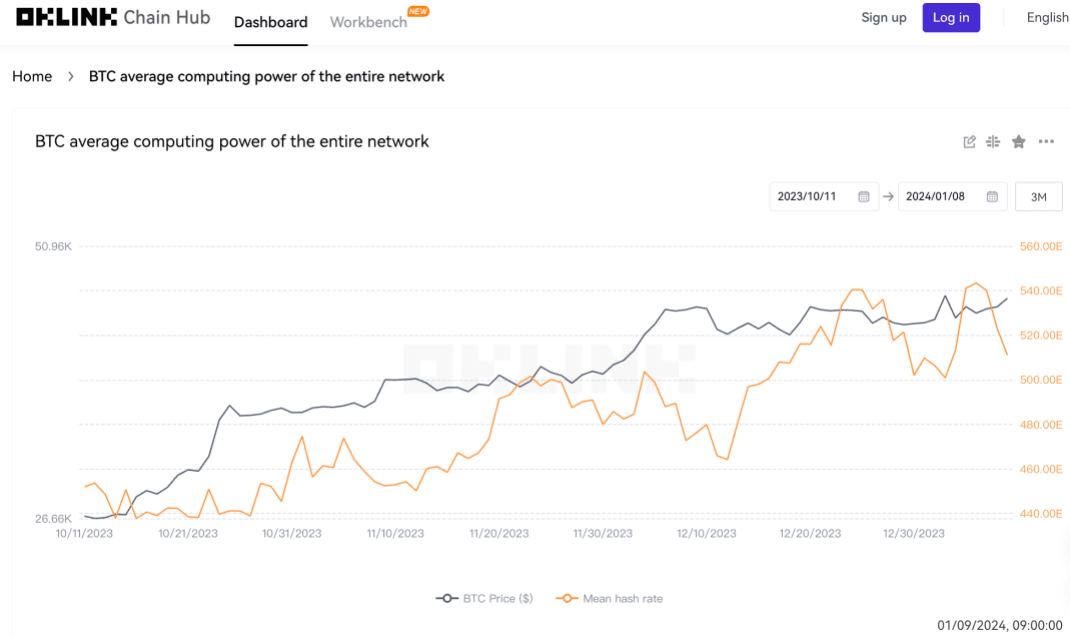

In addition, the expected approval of the Bitcoin spot ETF is also very obvious on the supply side: the competition among miners on the supply side is also very fierce and in full swing. According to OKLink data analysis, the hash rate has been increasing at an average growth rate of 5.17% in the past three months, compared with the monthly average growth rate of 1.76% in the same period last year, which shows that the competition among miners (supply side) is more intense.

Figure: Bitcoin computing power Source: OKLink

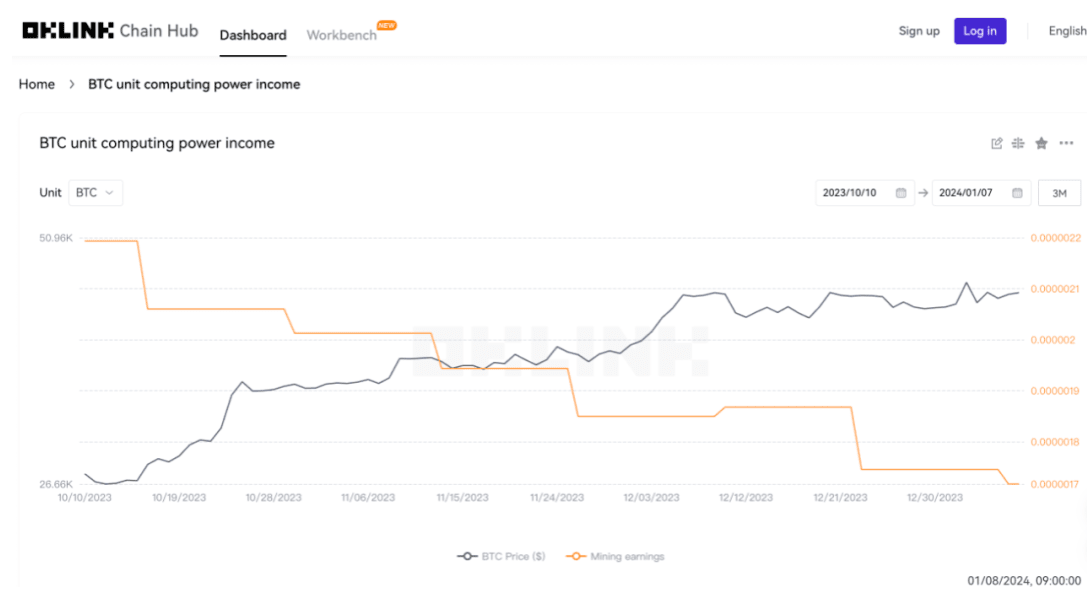

From the perspective of operating costs, OKLink data shows that the unit computing power income of miners has continued to decline at a rate of 8% in the past three months (Figure 2), while the monthly average growth rate during the same period is about 1.55%. The supply side is still selling to maintain operating costs despite the decline in unit income.

Figure: Bitcoin miners’ unit computing power income source: OKLink

New markets are ready to take off, and existing markets are more stable

Although the news of ETF has been long awaited in the market, the OKLink chain data shows that due to different time and risk preferences, new investors are more willing to endure the opportunity cost of waiting for the convenience of compliant channels and give up the potential profit of early ambush on the chain. However, the original market participants - long-term investors, Bitcoin supporters and institutional investors who have long been optimistic about Bitcoin still value the long-term value of Bitcoin.

Since some early bullish Bitcoin institutions have participated in other ways, such as ARK has sold all its remaining GBTC positions and injected BITO (Bitcoin Strategy ETF, BITO invests in Bitcoin futures, not Bitcoin), Grayscale is also seeking to convert GBTC into an ETF. They may be more focused on Bitcoin's fundamentals, technological development, and market demand, and are relatively less affected by short-term market fluctuations and ETF approval news.

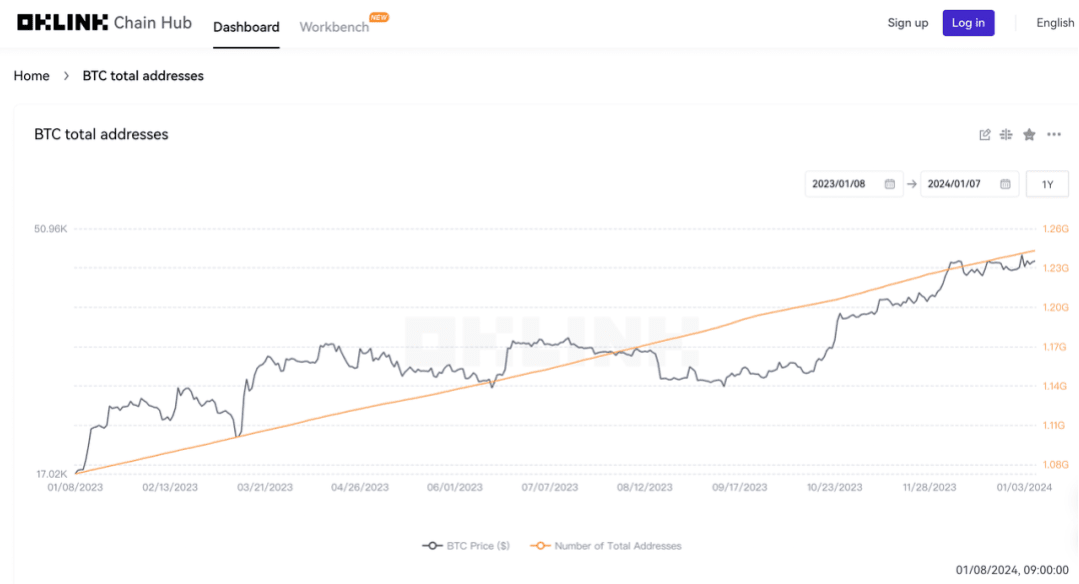

According to the data on OKLink, these news did not bring much excitement to the ecosystem on the chain. In the past three months (October 10 to January 7), the total number of addresses on the Bitcoin (BTC) chain has been rising in a straight line, with an average monthly growth rate of 1.16%. Compared with the same period last year, the growth rate is the same.

Figure: Total number of Bitcoin ecosystem addresses Source: OKLink

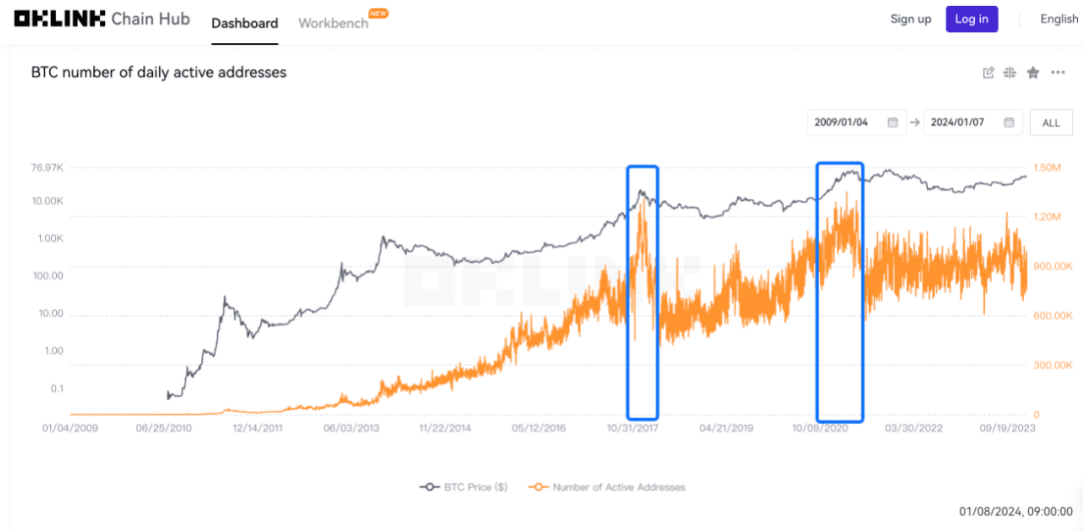

In addition, through observation of the number of active addresses, we found that the number of active addresses did not reach a high point when news about Bitcoin ETF broke out, but was relatively high in December 2017 and March 2021.

Figure: Number of Bitcoin daily active addresses Source: OKLink

The era of wild growth is gone

"You plan to start over?"

Even if the US BTC spot ETF is not approved, the market will not return to the "wild growth era". According to Coingecko, there are currently eight markets in the world that allow the operation of spot cryptocurrency ETFs, including Canada, Germany, Switzerland, and tax havens such as the Cayman Islands and Jersey. However, it did not arouse the same enthusiasm in the market as waiting for the approval of the US spot ETF, which once again proves the great impact of the superposition effect brought about by the US opening up the supply side and channels on the market.

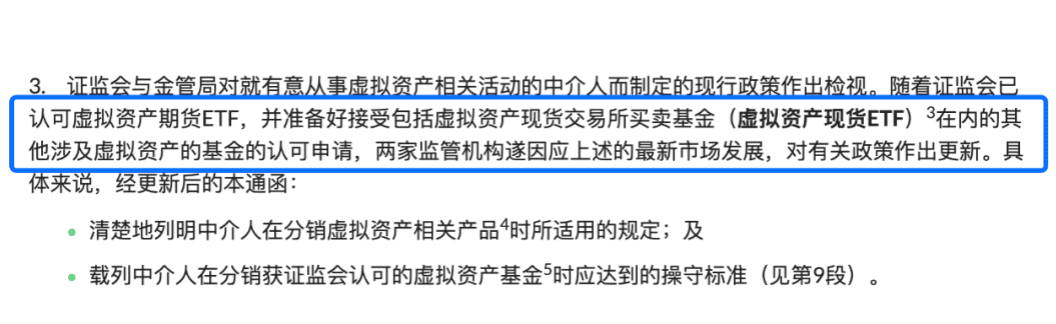

While the ETF plot in the United States is "confusing", Hong Kong, which has attracted much attention in 2023, has already taken that step. On December 22, 2023, the SFC issued several circulars in succession, stating that it is "ready to accept applications for recognition of virtual asset spot ETFs". Taking Hong Kong as an example, according to KPMG's 2023 Private Wealth Management Report, as of the end of 2022, the total asset management value of private banks and private wealth management in Hong Kong is HK$8965 billion. If 1% of the funds are transferred through the Bitcoin spot ETF, about US$11.6 billion will flow into the market.

According to OKLink Research Institute, several financial institutions are planning to issue Bitcoin spot ETFs in the first half of the year. Such a tens-billion-level competition will also force the US SEC to not easily reject the spot ETFs that are ready to go.

Comparing the differences between Hong Kong and the United States regarding Bitcoin spot ETFs, there are two points that deserve market attention:

In the circular on December 22, the Hong Kong SFC stated that it would support both cash and physical redemption modes to provide investors with more choices; the US SEC adopted a strategy of mandatory cash redemption, and the use of cash redemption is also to reduce the risk of market manipulation. Cash redemption is also a disguised control of AP, which will also squeeze its profit space for risk-free arbitrage. Because if AP attempts to manipulate market prices through operations in the primary and secondary markets, it may cause market instability. In addition, in the case of physical redemption, market makers can receive Bitcoin in exchange for ETF shares, improving tax efficiency. Financial institutions on the other side of the Pacific also hope to achieve multiple channels. According to CBNC, Fidelity and BlackRock have sought approval for cash and physical redemption to take care of investors who already hold Bitcoin but seek convenience in market transactions and taxation.

At present, the United States has submitted 8 Bitcoin ETF applications, which are planned to be traded on one of the three exchanges: Nasdaq, Cboe BZX, and NYSE Arca. Among them, the exchange with the largest proportion is Cboe BZX, accounting for 5/8 of the total number of applications. Unlike the trading venues applied by the US applicants, which are all trading platforms that have experience in trading other financial instruments, Hong Kong only stated in the circular on December 22 that the SFC and the HKMA listed the regulations and ethics that intermediaries need to meet when distributing ETFs. If the US BTC spot ETF is approved and traded on one of the three trading platforms according to the application materials, with such a case reference, the Hong Kong Exchange will be more motivated to consider providing a trading platform for the Bitcoin spot ETF issued by a Hong Kong company.

Figure: On December 22, SFC issued several circulars Source: SFC

Regardless of whether the US ETF is approved tomorrow, time has passed and the "Westworld"-like crypto market will never return. In 2024, the crypto market will surely be "flourishing".