Today we continue to talk about it in order of market value. It is the Rocket Pool of the staking track. I should have mentioned it when talking about LIDO before. I briefly talked about their comparison before. If you are interested, you can check out the previous program. .

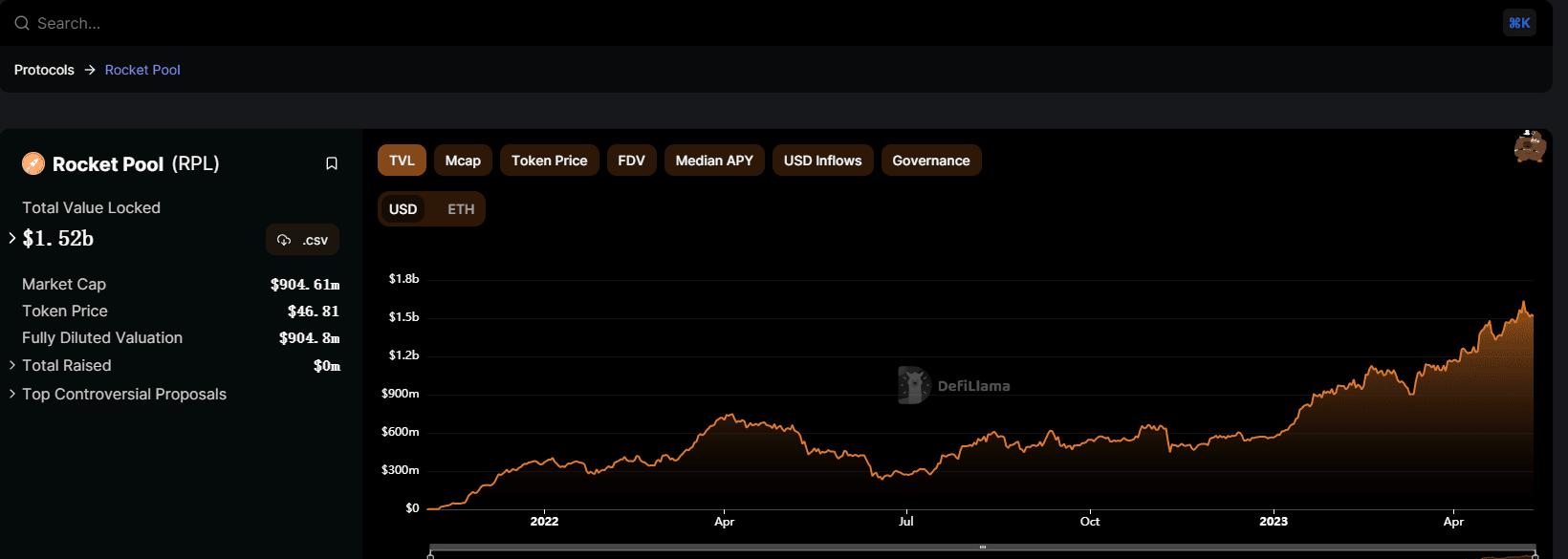

The current market value of Rocket Pool is US$900 million, ranking around 50th, and the No.1 decentralized pledge of Ethereum.

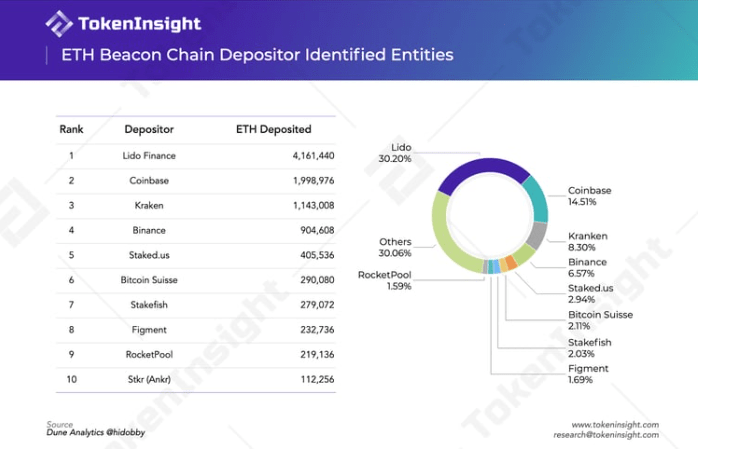

Compared to Lido Finance, Rocket Pool accounts for only a fraction of the $ETH liquidity staking market share, with less than 550,000 $ETH deposited into the protocol, compared to over 4 million $ETH deposited into Lido Finance. Rocket Pool distributes these $ETH to over 2500+ node operators, while Lido Finance distributes over 4 million $ETH to just 24 node operators. Rocket Pool is quietly working hard to help Ethereum achieve a more decentralized verification node distribution.

The importance of node operator decentralization to Ethereum

After Ethereum transitioned to the Proof-of-Stake blockchain, staking service providers such as Binance Stake and Coinbase Stake controlled a large portion of the staked $ETH. These large validators are responsible for validating new transactions and producing new blocks for Ethereum, and they can easily be pressured by outsiders to review certain transactions to comply with their respective regulatory requirements.

On the other hand, over 30% of pledged $ETH is through the largest liquid staking protocol, Lido Finance. Users deposit $ETH into Lido’s staking pool, and these deposited $ETH are then distributed to 24 whitelisted node operators. These node operators are selected by Lido DAO, and those who have obtained whitelist qualifications are mostly large-scale professional node operators such as P2P Validators, Stake.Fish, and Chorus One. Lido Finance holds over 90% of the market share in the liquid staking space and distributes all deposited $ETH to a select few professional node operators. This naturally raises concerns that the success of Lido Finance has brought about the centralization of Ethereum transaction verification power and may even potentially have an impact on Ethereum.

The vision of Ethereum is to have a decentralized and diverse portfolio of validator nodes around the world. However, the current situation is that the majority of staked $ETH is either staked through centralized exchanges or flows to a small number of professional node operators through Lido Finance. So this doesn't make sense.

Rocket Pool helps more people have the opportunity to become node operators

Liquid pledge service

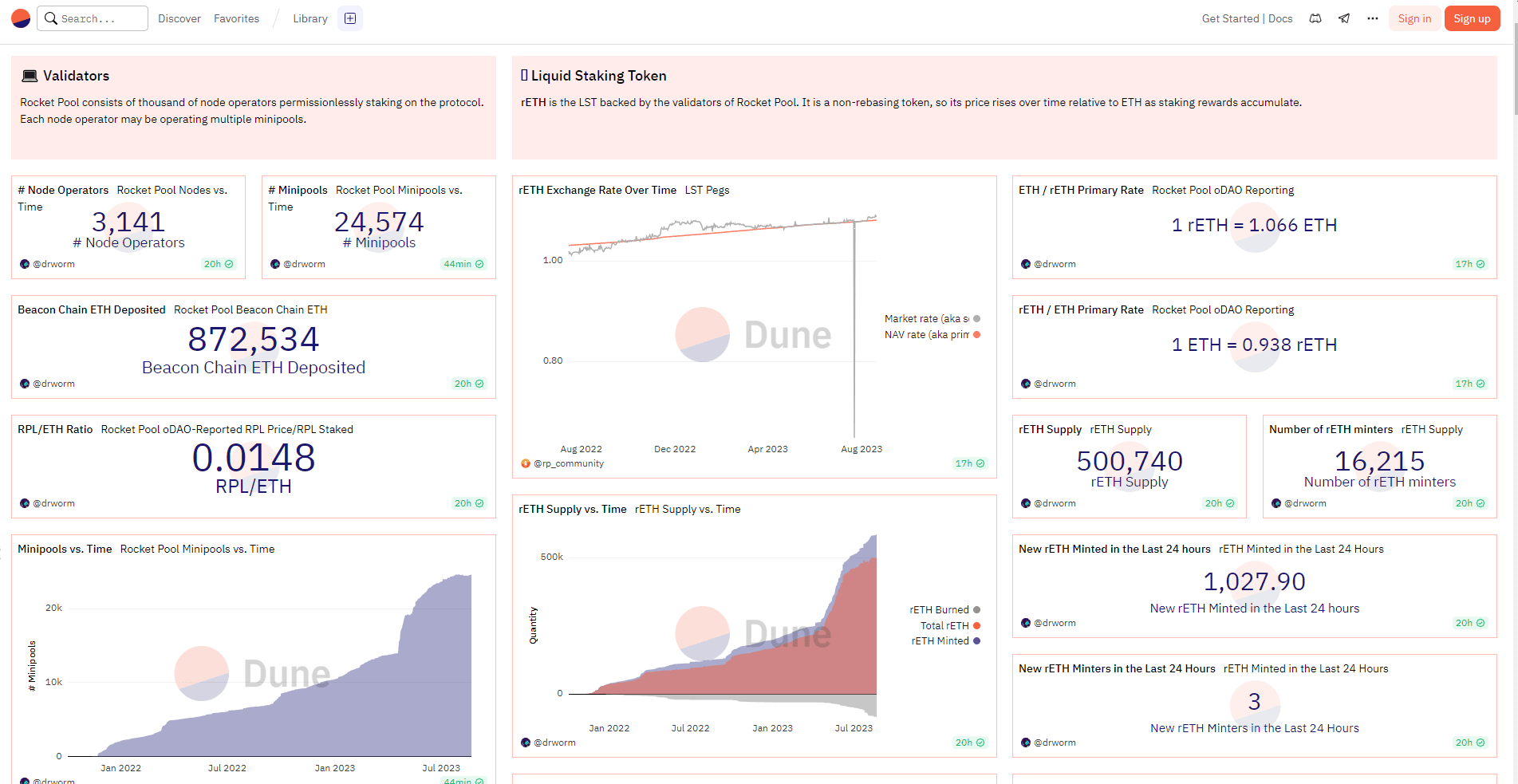

Like Lido Finance’s liquidity staking token stETH, Rocket Pool issues rETH, a token representing deposited assets. The main difference between the two is that rETH does not accumulate returns through additional issuance like stETH. When Ethereum successfully merges and opens the redemption of pledged $ETH, users can return rETH to the protocol and redeem the pledged $ETH and the corresponding share of $ETH rewards. Therefore, the value of rETH will increase over time, and the current secondary market price of rETH is approximately 1.023 $ETH.

Rocket Pool’s node operators are permissionless, while Lido Finance is only assigned to professional node operators. To help independent node operators, Rocket Pool has also developed smart node software to simplify the setup process of Ethereum nodes.

The Rocket Pool protocol is permissionless, instead leaving decisions to its token holders. Anyone can become a node operator in the network by creating a "minipool": for this, the node operator needs to deposit 16 ETH (half of the 32 ETH requirement stipulated in the Ethereum protocol) and the rest 16 ETH from user deposits. In addition, the "mini pool" operator will also need to stake at least 1.6 ETH (i.e. 10% of the 16 ETH they stake) of RPL tokens, which is used as a backstop for the protocol in the event of a large slashing incident on the validator node. Safety and security.

RPL is the governance token of the Rocket Pool protocol and can also be used to stake onto Rocket Pool nodes as a form of insurance. Specifically, these RPL tokens pledged by the "mini pool" operators will serve as collateral. When the node operator is severely punished or forfeited by the Ethereum protocol while performing verification duties, it will result in the node's pledge deposit being lost. When less than 16 ETH is available, these RPL collateral will be sold via auction for ETH, helping to compensate the Rocket Pool protocol for these lost ETH. In return for providing this security, the protocol will reward node operators with RPL tokens through token inflation built into the protocol. The more RPL tokens staked by node operators in Rocket Pool (the upper limit is 150% of the value of their staked ETH), the more RPL token rewards they can receive.

Rocket Pool’s model aligns interests between the protocol and node operators by requiring them to stake RPL tokens, and minimizes trust assumptions by automating the process of joining the network.

However, this comes at the cost of reduced scalability. Unlike Lido, which can continuously distribute an unlimited amount of ETH to validators at any time, Rocket Pool's growth is limited by the 16 ETH required to join the network and relies on the need to constantly have new node operators come online. .

If more independent validators join Rocket Pool, more $RPL will be staked as insurance, which will reduce the circulating supply of $RPL. Currently 34.55% of the total token supply in $RPL is staked for this purpose. At the same time, since the amount of $RPL that needs to be staked to become an independent validator is based on the value of $ETH, this means that if the price of $ETH increases but the price of $RPL does not change, then becoming an independent node operator requires staking more $ RPL, the $RPL circulating in the market will decrease faster.

The benefits of being an independent validator for Rocket Pool mainly come from two aspects, network verification rewards and $RPL rewards. Independent validators can earn 100% of the $ETH returns from half of the $ETH provided by themselves, 15% of the commission from the other half of the $ETH provided by the protocol, and $RPL rewards, 70% of the total $RPL supply will Used to reward these independent validators. According to Rocket Pool’s official statistics, the APR of verification rewards + commission income is approximately 4.81%, which is slightly higher than Ethereum’s staking income of 4.2%, and the APR of $RPL rewards is approximately 12.16%.

Therefore, two forces act together on the circulating supply of $RPL:

Incentive rewards for $RPL >> Increase in circulating supply

More independent validators and $ETH price increase >> Circulating supply decreases

The current TVL is US$1.5 billion, and it has been on an upward trend. In other words, decentralized Ethereum staking is becoming more and more popular.