by Alex Xu,Research Partner at Mint Ventures

Key Insights

This article delves into the ever-evolving landscape of Decentralized Exchanges (DEXs), particularly those deploying the ve(3,3) model. We aim to clarify the commercial prospects and challenges integral to this model, providing insights into the potential long-term path of DEXs.

As frontrunners in the DeFi race, DEXs and lending protocols have successfully attained a desirable Product-Market Fit. They boast a robust user base and trade volume, serving as the foundational pillars of the flourishing Value Internet metropolis.

Given their pivotal role, DEXs are continually at the heart of fierce competition and innovative advancement. Entities in this field aim to outshine their counterparts by rapidly enhancing their products, economic frameworks, and ecosystem alliances. Among myriad strategies in this field, the ve(3,3) model, introduced by Andre Cronje in early 2022, stands out.

This research delves into the ve(3,3) paradigm, serving as a crucible for critical inquiries:

Understanding ve(3,3): What constitutes the core elements of the ve(3,3) framework? What challenges is it engineered to overcome?

ve(3,3) In Practice: How have the standard-bearers of ve(3,3) performed in the DeFi arena? What enhancements have these trailblazers integrated into the foundational ve(3,3) blueprint, and how are they valued within the ecosystem?

Sustainability: Does ve(3,3) possess the resilience to establish a sustainable niche for future DEXs?

The subsequent report contains the author's perspective on the ve(3,3) model and the projects deploying it as of the publication date. Please be aware that the information presented may contain inaccuracies or biases and should not be used as an investment guide. We appreciate and encourage constructive criticism and corrections.

For a beneficial understanding of this article, a basic knowledge of the ve model and Curve, a project closely associated with it, would be advantageous. For a comprehensive understanding of Curve, you might refer to:

A Deep Dive into the Leading AMM Platform: Curve Finance

CRV under the attack of Uni V3: In-depth analysis of Curve’s business model, competition status, and current valuation

1. Defining the ve(3,3) Model and Its Value

The ve(3,3) model, rather than being a specific project, embodies a methodology for the construction and operation of Decentralized Exchanges (Dex) and liquidity protocols. The 've' stands for 'vote escrowed', which is derived from the veNomics proposed by Curve. The essence of this component is the fostering of an alignment of long-term interests between participants and the protocol, achieved through a staking-based voting mechanism.

The “(3,3)” component originates from the game theory of OlympusDAO, an interpretation of the Nash equilibrium theory. The basic principle is that OlympusDAO sells its native token, OHM, to users at a below-market price through bonds. In return, Olympus receives assets like USDC and ETH from its users, thereby establishing a value-supported treasury. The treasury then generates OHM to be disseminated through the Rebase mechanism to OHM stakers. In the event of increased market demand for OHM tokens, the treasury initiates a larger issuance of OHM tokens to stakers. This action catalyzes a virtuous cycle of high Annual Percentage Rate (APR) for stakers, contingent on a consistent increase in the OHM price. The underlying assumption here is that market participants will opt for continued staking rather than selling their OHM tokens. This phenomenon, known as 'Stake, Stake' or '(3,3)', motivates users to persistently partake in staking, hence enabling them to reap the benefits of continuous OHM token issuance while concurrently reducing the risk of token dilution.

If the intricacies of the (3,3) mechanism seem complex, it can be simplified as a strategic game model as follows:

A project is powered by its network effect. The larger the bilateral or multilateral scale of its user base and the involved funds, the more daunting the competitive barrier. As such, there's an ongoing imperative to broaden its scale to establish an unbeatable network effect barrier.

The project introduces a mechanism that incentivizes all token holders to collectively stake and reinvest their tokens (or undertake any other action that the protocol encourages). This concerted action enables the protocol to continually expand in size and strengthen its network effect until it establishes a robust competitive barrier capable of capturing monopoly profits within its sector. As a 'shareholder' of the project, a user's ownership value will naturally increase in line with the project's expansion in size and monopoly, as long as the user maintains their share of the total project tokens. This scenario culminates in a 'win-win' situation, enhancing the value of individual ownership while contributing to the project's growth.

The project sets forth a mechanism that encourages all token holders to collectively pledge and reinvest their tokens (or execute any other action that the protocol advocates). This unified action empowers the protocol to continuously expand in size and intensify its network effect until it forms a solid competitive barrier capable of securing monopoly profits in its domain. As a 'shareholder' in the project, a user's stake value will naturally escalate in conjunction with the project's growth in size and monopoly, provided the user retains their share of the total project tokens. This situation manifests in a 'win-win' outcome, bolstering the value of individual stakes while fueling the project's expansion.

The vulnerability of this mechanism becomes apparent when users choose to adopt opposing actions, such as unstaking and opting to sell their tokens in the market. Such an action could gradually create a ripple effect, leading to a decrease in token prices and mass exodus of users, thereby initiating a downward spiral that could result in project failure.

In the context of OHM's stablecoin project, the pursued network effect is that the larger the network of the stablecoin, with more use cases and users, the harder it becomes for subsequent players to compete. In the case of the Dex project represented by Solidly, the network effect pursued lies in the mutual amplification among Dex's Liquidity Providers (LP), veToken stakers, and traders. The larger its market share in trading, the more challenging it becomes for later entrants to catch up. Therefore, the primary objective of the (3,3) mechanism in the DeFi space is to aid projects in expanding their network effect and establishing competitive barriers at a specific phase of their development.

Additionally, the ve(3,3) Dex introduces novel strategies during the project's initial phase and the composability of governance credentials, augmenting the foundational ve model and (3,3). By integrating these design elements, it strives to establish a superior Dex model.

When considering the specific attributes of ve(3,3) category Dex projects, the following key features are notable:

1.Primarily, such projects adopt Curve's veNomics as their main framework, which implies:

The project not only operates as a Dex but also functions as a liquidity aggregator and liquidity marketplace. The project's equity tokens serve as the procurement currency for the platform's liquidity.

Equity tokens must be staked to gain governance rights and receive dividends from revenues (inclusive of fees and bribes). For stakeholders to derive value from the platform, they must commit to its long-term evolution.

There are two key points of distinction between ve(3,3) projects and Curve: one is that while Curve distributes all transaction fees from all pools to veToken stakers, ve(3,3) projects only allocate transaction fees from the pools voted on by the veToken stakers. On the other hand, the Liquidity Providers (LPs) of ve(3,3) projects receive only equity tokens as rewards for market making, while all transaction fees are directed to veToken stakers. Unlike Curve, which relies on an external platform (like Votium or Votemarket) for its bribe module, ve(3,3) projects integrate their own bribe module. This design allows for more straightforward short-term liquidity acquisition.

2.Learning from Olympus (3,3) game mechanism in the context of ve(3,3) projects suggests the following:

There is an encouragement for users to stake equity tokens in exchange for veTokens and for a proportional token incentive emission amongst veToken holders. This approach aims to prevent dilution of holders' token ratios, motivating users to stake actively.

An increase in staking ratio lessens the selling pressure on the token, thereby boosting the token price. This price increase results in a higher APR for market-making, attracting further liquidity, enhancing trading depth, and increasing trading volume, thereby creating a self-reinforcing business cycle.

3.During the initial phase or 'cold start', the first veTokens are typically airdropped to top projects in the ecosystem (usually referring to the underlying public blockchain), recognized for their business impact and influence. This strategy aims to attract the initial business audiences to its liquidity marketplace, much like an internet product issuing "free-try coupons" to its customers. Here, 'try' equates to the project's "liquidity buying service."

4.The staked voucher of the equity tokens have been changed from veToken to veNFT. Unlike veTokens, which are non-transferable, veNFTs can be transferred, allowing users to resell or restake their veTokens, thereby improving capital efficiency.

In essence, ve(3,3) projects represent an advancement of the Curve model, primarily targeting improvements in three key areas:

Enhanced User Incentives: These projects aim to increase users' inclination towards acquiring veTokens, thereby aligning the interests and actions of token holders more closely with the protocol.

Fee-Driven Incentives: The model operates on a principle where pool fees are allocated only to those who vote for a particular pool. This system indirectly incentivizes transaction volume, as better liquidity attracts more transactions, leading to an increase in fee generation.

Business-Oriented Strategy: ve(3,3) projects strive to provide an improved liquidity purchasing experience for token issuers while offering higher initial incentives to actively engage the business audience.

Hence, when assessing the performance of ve(3,3) projects, our analysis will center on these three critical elements.

2. Analysis of Prominent ve(3,3) Projects

The selection of specific ve(3,3) projects for this analysis takes into account a comprehensive range of factors such as the ranking of the blockchain on which the project is based, trading volume, bribe amount, and other indicators. The following projects, demonstrating superior business performance, have been selected for comparison and analysis: Velodrome on Optimism, Thena on BNBchain, Equalizer on Fantom, and Chronos, a recent entrant live on Arbitrum.

2.1 Velodrome: An Early Adopter of ve(3,3) and Leading Dex on Optimism

Velodrome is the most representative project forked from Solidly, and as such, it will be given a more in-depth introduction.

2.1.1 Project Overview and Unique Mechanisms

a. Mechanism Design

Velodrome, currently deployed solely on Ethereum's L2 network, Optimism, builds its product mechanism on Solidly's ve(3,3) framework with some notable alterations:

Bribes for the Liquidity Pool can only be claimed after the start of the subsequent epoch.

Velo token incentive distribution operates on a whitelist system. Currently, this whitelist is open for applications and does not follow an on-chain governance process. Conversely, Solidly's emission application is permissionless, meaning that token incentives can be routed towards pools that don't generate any transaction fees with voting power. Additionally, Velodrome has introduced an Emergency "Commissaire" with the power to terminate any gauge deemed detrimental to the wider ecosystem.

The emission reward rate for veToken holders has been reduced. Contrary to Solidly's guarantee of preserving the token proportion for veToken holders against dilution, the mechanism design of Solidly computes the emission reward for veTokens as (veVELO.totalSupply ÷ Token.totalSupply) × 0.5 × Total Emissions. On the other hand, Velo calculates the rewards for increasing issuance to veTokens as (veVELO.totalSupply ÷ VELO.totalSupply)³ × 0.5 × Total Emissions. Given a 50% staking rate for Velo, veVELO holders would receive 50% of the total emission under the traditional ve(3,3) model. However, under Velo's adjusted model, veVELO holders would receive only 12.5% of the total emission, which equates to a mere quarter of the traditional mode. This modification considerably weakens the (3,3) aspect of the ve(3,3) mechanism.

3% of Velo's emissions are transferred to the team's multi-sig wallet as operating costs, thus furnishing a budget for the long-term sustenance of the project.

They have removed the "boost" for LP emissions, a mechanism inherited from Curve that allowed the mining mechanism for LP to be accelerated based on the number of veTokens.

b. Team Information

The team behind Velodrome Finance had previously initiated veDAO, which was incubated by the Information Token, an anonymous blockchain research group. The core mandate of its inception was to secure governance rights for the Solidly ecosystem, as proposed by Andre Cronje. In early 2012, Cronje launched Solidly on Fantom, stating that the initial governance rights of Solidly (in the form of veNFT) would be distributed amongst the top 20 Fantom projects based on the proportion of their Total Value Locked (TVL). Upon its launch, veDAO attracted a peak TVL of nearly $2.6 billion.

However, soon after, Andre Cronje announced his departure, leading to the premature discontinuation of Solidly. Following these events, the veDAO team pivoted towards the Optimism ecosystem and subsequently developed Velodrome.

c. Milestones and Roadmaps

The forthcoming significant milestone for Velodrome is the unveiling of Velo 2.0, originally scheduled for the first quarter of 2023. As of early May 2023, the new version has yet to be launched. Upon inquiry in the official community regarding Velo 2.0's release timeline, a community ambassador indicated that audits have been finalized and the launch should occur in May.

Velo 2.0 comprises more robust features and is divided into five main sections:

Night Ride: Velodrome’s new frontend has been rebuilt from scratch to enhance user experience and deploy an enriched data dashboard. The UI/UX design emphasizes transparency.

Velodrome Relay: optimization of bribery fees around veToken staking delegation and other functions.

New features: LP customization (a basic function of concentrated liquidity), Pool customization (editable Pool function similar to Balancer), fee hierarchy, upgraded voting module (similar to Votium), veNFT trading, fragmentation, etc.

Technical upgrade: code library streamlining, auditing, risk control, etc.

Governance upgrade: veVELO can control the emission of VELO tokens via governance.

Given the extensive features that V2 will bring, it's possible that releasing all of them at once might pose challenges, and it seems more plausible that they'll be rolled out in stages. Furthermore, for 2023, the team has identified functionalities such as the Launchpad, automatic reinvestment of LPs, a complete concentrated liquidity function, portfolio pool (similar to Curve's MetaPool), and veNFT lending as key objectives.

2.1.2 Business Analysis

In evaluating Velodrome's business performance, I'll assess it from four perspectives: total value locked (TVL) and corresponding liquidity procurement costs, trading volume, bribe amount, and number of bribed projects, as well as the staking ratio of Velo.

As a spot Decentralized Exchange (Dex) with the ve(3,3) model combined with a liquidity procurement market, Velodrome's business model can be distilled into one sentence: it purchases and aggregates liquidity through its platform equity tokens (Velo), and then uses the procured liquidity to satisfy traders' needs (in exchange for transaction fees) and to sell to project developers (providing liquidity for their tokens).

Thus, by examining TVL and associated liquidity procurement expenses, trading volume and transaction fees, bribe amount, and number of bribed projects, we can gain a comprehensive understanding of the project's revenue, customers, and costs. The staking rate of Velo can be used as a measure of the effectiveness of the project's (3,3) mechanism.

a. TVL and Associated Liquidity-Purchasing Cost

According to the latest data from the renowned DeFi analytics platform, DefiLlama, Velodrome, a standout project in the DeFi ecosystem, exhibits a steady TVL of approximately $289 million as of May 4, 2023. Over the preceding months, the TVL of the project has demonstrated relative stability, varying between a range of $270 million and $320 million.

The most recent weekly liquidity emissions by Velodrome saw the distribution of 9,166,759 Velo tokens, each priced at $0.129. This leads to a cumulative value of roughly $1.18 million in weekly liquidity emissions.

This puts the total value of the weekly liquidity incentive at approximately $1.18 million. When evaluated against the TVL, this liquidity incentive equates to a proportion of about $244.64 for each dollar spent on weekly incentives. This implies that Velodrome can secure and sustain approximately $244.64 of liquidity for every dollar invested in incentives on a weekly basis. However, it's worth noting that the measure of liquidity encompasses more than just the sheer volume of assets. Factors such as the composition of these assets and the unique trading curve algorithm also come into play when considering the overall liquidity of the platform.

b.Trading Volume and Fee Revenues

As per the data available from Tokentermina, Velodrome has exhibited trading volumes fluctuating between $80 million and $300 million weekly for the last quarter. However, the trading volume usually falls within a more modest range of $100 million to $150 million in most weeks.

Weekly transaction fee revenues for Velodrome also vary, typically ranging from $25,000 to $100,000.

The primary contributor to Velodrome's fee revenues is predominantly non-stablecoin pairs, specifically Volatile AMM (vAMM) pools. Data dashboard constructed by community member @msilb7 indicates that vAMM pools are frequently in the top 5 contributors to Velodrome's fee revenues over the past week, accounting for 62.7% of the total trading fees.

However, when comparing the liquidity provider (LP) capital efficiency between Velodrome and Uniswap on Optimism, Velodrome appears less efficient. A significant divergence exists in the Volume/TVL ratio, with Uniswap V3 at 0.4, while Velodrome trails at 0.04, marking a tenfold difference.

This striking discrepancy can largely be attributed to Uniswap's concentrated liquidity mechanism. Though it requires more intricate management from LPs, it effectively captures a larger trading volume. This underscores the importance of concentrated liquidity as a primary focus for the forthcoming Velodrome 2.0 upgrade.

c. Bribe Revenues and Partnered Bribe Projects

During Velodrome's Epoch 49, the total bribe amount from the previous cycle was approximately $896,000.

Velodrome's bribe amounts have remained consistently above $300,000 for 15 successive weeks and have surpassed $500,000 over the past 12 weeks.

In comparison with Balancer, a well-established project that also employs the veModel and operates within both the Dex and liquidity markets, Velodrome's weekly bribe data outshines. Despite Balancer's higher TVL of $1.2 billion, its recent bribery amount on its main bribery platform, Hidden Hand, was $537,000. But with a governance cycle of 2 weeks, the weekly bribe amount comes to only $268,500.

Although Balancer‘s veToken participation rate on Hidden's vote on Hidden is below 30%, it's noteworthy to mention that Velodrome's significant bribe revenue indirectly indicates the benefits of the integrated ve(3,3) project, which includes the bribe module, in driving veToken governance and enhancing bribe amounts compared to conventional vemodel projects that adopt a modular service approach. On the partnerships front, according to Velodrome's data disclosed in February of this year, more than 53 different types of tokens have been distributed to veToken holders.

As of Velodrome's bribe data on April 26th, there were 248 active pools, with the top ten weekly bribes exceeding $13,000, and 49 pools had weekly bribes over $1,000.

The leading ten bribe contributors in Epoch47 originated from nine distinct projects, spreading across a diverse range of sectors, including lending and stablecoin protocols (Tangible, Inverse, Ethos, Sonne), derivatives (Kwenta), entertainment (Red), LSD (Rocket Pool), asset management (dHedge), and L2 infrastructure (Optimism).

Five out of the top ten DeFi protocols on Optimism ranked by TVL have initiated liquidity procurement on Velodrome. Meanwhile, the remaining five, which include three Dex sector competitors (Uniswap, BeethovenX, and Curve) and two other projects with sufficient liquidity and presence on major exchanges (Aave and Stargate), have shown recent interest. Specifically, Stargate has passed a community governance proposal to execute liquidity procurement on Velodrome.

Overall, Velodrome's liquidity procurement appears to have a diversified and healthy development, with a rich variety of sources.

d. Staking Ratio

Since its inception, Velodrome has seen a steady increase in Velo's staking ratio.

However, there's been a shift in this trend with the staking ratio peaking between February and March this year (Epoch 36), following which, it started to decline. Despite an overall rise in the total locked volume, the staking ratio of newly minted Velo tokens has significantly dropped. The current Velo staking ratio has dipped nearly 7%, dropping from its peak of 81.6% to 74.67%.

Several factors potentially contribute to the peak and subsequent decline in Velo's staking rate:

1.From late January 2023, the Velo token experienced a sustained price surge. Though Velodrome's transaction fees and bribe revenue also witnessed an increase during this time, the rate of this increase was markedly lower compared to the token's price surge. This led to a swift decrease in the APR of veVELO and a corresponding reduction in staking incentives.

2. Between February to April, the Velo token price displayed significant volatility with recurrent drastic fluctuations. This might have persuaded investors to hold the token for liquidity purposes, rather than staking it.

3. The "Tour de OP" program, initiated in November of the previous year, has been running for five months. This program, anticipated to last for 6-8 months, majorly focuses on leveraging Velodrome's 4 million OP reward to incentivize Velo staking. As the program nears its end, the OP incentives will stop, further decreasing the incentive for Velo staking. This might potentially trigger selling pressure.

4. A staking rate between 70% to 80% is considerably high. The cumulative marginal cost to maintain or increase the staking ratio is increasingly growing. For reference, Curve, employing a similar ve model, currently holds a staking rate of 38.8%.

2.1.3 Summary

Velodrome currently emerges as one of the most promising players in the ve(3,3) space. It holds the highest TVL among Optimism-based projects and boasts a transaction volume only surpassed by Uniswap on the same chain. The progress in its liquidity procurement activities has also been noteworthy, with the number, quality, and volume of its customers all positioning it at the top of the pile. However, the impressive rise in the token value since January coupled with significant volatility has driven the staking ratio to peak levels, which is now witnessing a decline. Additionally, the "Tour de OP" program, which provided OP rewards for staking, is nearing its end, implying a likely reduction in veVELO's mid-term staking ratio due to reduced incentives. Looking ahead, the concentrated liquidity brought about by the upcoming Velodrome 2.0 release could potentially boost the platform's capital efficiency, fee revenue, and its share of trading volume on Optimism. It's noteworthy that Velodrome's future largely intertwines with the trajectory of the Optimism community. The platform's growth ceiling is inextricably linked to the development of the Optimism ecosystem. Apart from Optimism serving as an L2 network, the potential inclusion of other L2 operators and applications into the Superchain L2 network based on Optimism Stack—currently Velodrome's mainstay—could significantly influence its development potential.

2.2 Thena: Pioneering ve(3,3) Project Implementing Concentrated Liquidity on BNBchain

Thena, having launched in January this year, currently holds the 9th position in terms of TVL on BNBchain. It was the first ve(3,3) Dex to incorporate the concentrated liquidity feature.

2.2.1 Project Overview and Unique Mechanisms

a. Mechanism Design

Thena, exclusively operating on BNBchain, represents an adaptation of the ve(3,3) model initially introduced by Velodrome, with a few significant modifications:

The platform features concentrated liquidity through its 'Fusion' function, which currently supports an auto-managed inter-marketing strategy based on this concentrated liquidity.

It offers rebase rewards for veTokens, with 30% of each period’s output (currently capped) being rewarded.

A referral system has been integrated, allowing referrers to share in the transaction fees generated by new users. New users brought in through referrals also receive rewards in the form of lottery tickets.

In its early stages, Thena utilized NFTs for fundraising. Now, staking these NFTs allows users to share between 10-20% of the agreement’s commission share.

The platform operates with elevated fee rates, with 0.02% applied to sAMM pools and 0.2% for vAMM pools. These are higher than Velodrome's rates of 0.01% and 0.05% respectively.

Like Velodrome, Thena uses the Gauge application licensing system. However, it eliminates the LP boost and allocates 2.5% (compared to Velodrome’s 3%) of the emission tokens to the project owner each period.

Fusion: Combining concentrated liquidity and Automation to Enhance Capital Efficiency and Reduce Participation Barriers

Apart from the core design mechanisms, the noteworthy addition to Thena is the Fusion feature, which was launched in April. This distinctive feature sets Thena apart from other ve(3,3) projects and serves as the foundation of Thena V2.

The main functions of Fusion are as follows:

The introduction of the Concentrated Liquidity Market Maker (CLMM) enables LPs to focus their funds within a specific price range for their market-making operations. This approach comes with several advantages, such as the concentration of capital within a custom price range. This concentration, in turn, ensures deeper liquidity and reduced slippage within the custom price range. As a result, LPs can capture a larger share of trading volumes and trading fees, thus improving their capital efficiency within that range. However, it's worth highlighting that this approach requires careful management. If the asset pairs offered by the LPs breach the set price range, they are converted into a single asset, and LPs can no longer capture fees, effectively reducing the capital efficiency to zero. This also implies an increased risk of impermanent loss. Hence, under the CLMM, market makers must possess advanced market-making skills, including the ability to forecast price trends, dynamically adjust market-making ranges, and devise appropriate strategies, to adequately navigate the landscape.

In an effort to lower the high market-making thresholds associated with concentrated liquidity mechanisms, automated LP management strategies have been introduced. The primary aim of these strategies is to alleviate two of the main market-making challenges:

1.The automatic adjustment of the LP market-making range: This helps to circumvent the issue of asset prices staying outside the market-making range for extended periods.

2.The provision of template-based market-making strategies: These strategies cater to five significant LP scenarios, making it easier for users with standard professional skills to swiftly identify an appropriate LP strategy. The five scenarios being catered for are as follows:

Source: Thena Medium Thena's Fusion feature introduces a dynamic fee structure, which automatically adjusts according to market volatility of the pool’s assets. During periods of high volatility, fees should be increased to compensate for potential losses faced by liquidity providers. Conversely, when trading volume is low and there is sufficient liquidity, fees should be reduced to encourage increased trading activity.

Overall, Fusion significantly contributes to Thena by reducing the complexities of market-making rooted in concentrated liquidity. That said, it's crucial to note that the challenges of market-making under this mechanism—such as the need for continual adjustments of the market-making ranges and, most importantly, price trend prediction—are not resolved by automated strategies and remain risks that users need to manage.

Moreover, the concentrated liquidity mechanism and Fusion's dynamic fee structure are furnished by Algebra Protocol's service, while automated LP management employs Gamma's service (note that LPs using Gamma's service don't have to pay fees, as Thena compensates Gamma with veTHE). This modular innovation approach has expedited Fusion's launch—while Velodrome's concentrated liquidity module is still in development, Fusion was able to go live more quickly. However, since Fusion's core services are derived from the amalgamation of three entities, it also brings additional external risk factors into play.

b. Team Information

The core team behind Thena operates under pseudonyms, without disclosing their real identities to the public. This team mainly hails from Liquid Driver, a project focused on yield aggregation and liquidity services on the Fantom blockchain. Liquid Driver had previously collaborated with other Fantom-based projects like SpookySwap, Scream, Hundred Finance, and RevenantFinance to form 0xDAO. This consortium aimed to accumulate liquidity, similar to veDAO's approach, and at its peak, they managed to attract $2 billion in liquidity. Moreover, they secured the largest share of veToken airdrops from Solidly.

However, the Liquid Driver project seems to have entered a period of stagnation, boasting a TVL of merely about $8 million and a token FDV of approximately $17 million. Given these circumstances, it's expected that the team has shifted its primary focus towards Thena. Despite the fact that the Thena team has yet to disclose any concrete information about its core members, several community members purport to "know who they are," suggesting that the team isn't entirely anonymous. According to some community members, the core team of Thena consists of 8 individuals, making it a relatively compact and agile unit.

c. Milestones and Roadmaps

2.2.2 Business Analysis

a. TVL and Associated Liquidity-Purchasing Cost

As of May 4th, 2023, Thena commands a Total Value Locked (TVL) of $81.41 million, as per DefiLlama data.

Similar to Velodrome, Thena incurs liquidity mining expenses, which primarily consist of THE token emissions to incentivize liquidity provision in its pools. Currently, in Epoch 17, Thena's total weekly emissions amount to 2,213,790 THE tokens. These calculations are based on the official documentation, which states an initial weekly emission of 2.6 million THE tokens and a subsequent weekly decay rate of 1%. Out of these total emissions, 67.5% are allocated towards liquidity incentives. With the current price of THE at $0.33, the liquidity mining incentives amount to 1,494,308 THE tokens, which, when multiplied by the token price, amounts to approximately $493,121 per week. By contrasting these weekly liquidity incentives with the TVL, an estimated liquidity-purchasing efficiency ratio is derived, indicating that Thena maintains about $165.1 of liquidity for each dollar spent on incentives per week.

b.Trading Volume and Fee Revenues

As per data from DefiLlama, Thena's weekly trading volume over the last quarter has fluctuated between $50 million to $200 million, with a majority of weeks seeing volumes within the range of $50 million to $100 million.

The weekly trading fee revenue for Thena has typically fallen between $40,000 to $100,000. Though Thena sees lower trading volumes than Velodrome, it is able to generate a higher aggregate transaction fee revenue owing to its higher fee rates for both vAMM and sAMM in its V1 iteration. In particular, Thena's vAMM imposes a fee rate of 0.2% (compared to Velodrome's 0.05%), while its sAMM fee rate is 0.04% (in contrast to Velodrome's 0.01%).

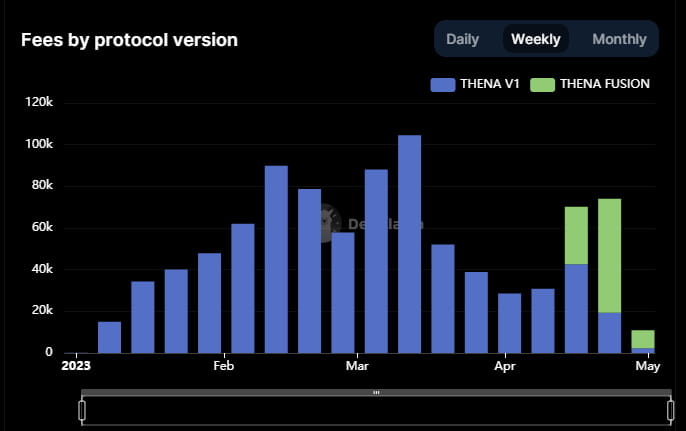

Notably, the launch of Fusion has prompted a significant increase in both trading volume and trading fees in line with Thena's overall business growth. Fusion-derived transaction fees have accounted for a substantial 73.8% of Thena's total, even while Thena's TVL has seen a decline. This trend underscores Fusion's capacity to attract trading volume and generate transaction fees, thanks to its concentrated liquidity provision and dynamic transaction fee model.

c. Bribe Revenues and Partnered Bribe Projects

Thena is in Epoch17. Owing to the recent introduction of Fusion, many external data dashboards are yet to incorporate Fusion's bribes into their analytics. However, the majority of weekly bribes from February to April ranged from $150,000 to $300,000. For a project that's been live for less than half a year, this revenue performance is quite remarkable.

Furthermore, according to Thena's official data, there are 146 active bribe pools (i.e., those with a bribe amount greater than zero), with 69 pools having weekly bribes exceeding $100, and 41 pools having over $1,000.

The top ten projects by bribe amounts this week are diverse, including stablecoin protocols (Tangible), a video streaming project (XCAD), liquid staking derivatives (Ankr, Pstake, Frax), derivatives and synthetic assets (Deus finance), and even a Ponzi project Dirt Dog (Libera). Among the top 15 DeFi projects on BNBchain, only Ankr (LSD), Radiant (lending), and Helio (stablecoin) currently have liquidity purchases at Thena, apart from Thena itself.

Excluding Thena's competing projects, Pancake and Biswap, the remaining projects – Venus, Alpaca, Chess, and Stargate – launched on Binance with robust liquidity.

In conclusion, Thena's liquidity market business has developed well, with a rather diversified customer base. Despite the sluggish growth and decline in the vitality of the BNBchain ecosystem, which is being gradually surpassed by ecosystems such as Arbitrum in terms of the number of high-quality projects, TVL, and other metrics in the past one to two years, it still maintains a high volume of active users and has attracted numerous new projects to deploy here. This forms the primary source of customers for Thena's liquidity market. However, given Binance’s centralized CEX, BNBchain's credibility is somewhat limited, leading to a plethora of projects with less refinement and innovation. Additionally, as Binance is the largest trading platform, it tends to overshadow the trading volume of BNBchain.

d. Staking Ratio

As of now, the staking ratio for THE stands at 61.83% and has been steadily increasing since its inception.

The primary driving force behind Thena's progressively rising staking ratio is its higher voting Annual Percentage Rate (APR) - with an average of 397%, far above most pools on Velodrome. This upswing is primarily influenced by two factors:

The lower token price of THE (attributable mainly to the sluggish progress of the BNBchain)

Intense competition among liquidity buyers, resulting in high bribe fees

Should these conditions persist, it's likely that Thena's staking ratio will continue its positive trajectory.

2.2.3 Summary

As the first ve(3,3) project on BNBchain, Thena has been operating effectively and currently ranks third among Dex projects on BNBchain (the top two projects have both received investments and support from Binance). We can point out several aspects where Thena has executed its strategies effectively:

Drawing on the lessons learned from Velodrome, Thena has capitalized on previous experiences to improve its own operations.

Thena has fostered innovation through partnerships with other projects, thereby accelerating the pace of product development. For instance, Thena has teamed up with the Algebra Protocol and Gamma to create a concentrated liquidity feature, collaborated with MUON to launch a referral commission function, and partnered with Open Ocean for trading routing.

Moreover, Thena's business metrics show that the adoption of the concentrated liquidity mechanism has had a substantial positive impact on its Dex operations. With the introduction of Fusion, both its trading volume and fees have seen significant month-over-month increases. This underlines the emerging trend towards concentrated liquidity adoption and hints at the potential opportunities in the service market (like Gamma) surrounding concentrated liquidity.

2.3 Equalizer: The only ve(3,3) project on Fantom

Equalizer, exclusively deployed on the Fantom network, ranks third in terms of Total Value Locked (TVL) among Dex projects on the network. However, it also boasts the smallest TVL and market capitalization among the ve(3,3) projects focused on in this article. This can be attributed both to the downturn in Fantom's ecosystem and to the intense competition on the network.

2.3.1 Project Overview and Unique Mechanisms

a. Mechanism Design

The mechanism of Equalizer is primarily inherited from Solidly, but with some distinct variations:

The rebase mechanism has been removed, meaning that ve users no longer receive emission tokens.

The maximum staking period for veTokens is 26 weeks.

The fee rates have been increased to 0.02% for the sAMM pool and 0.2% for the vAMM pool.

There has been no intentional airdrop of initial veToken governance rights to other projects.

The rebase feature was originally intended to be a key component of the ve(3,3) mechanism, with the expectation that it would enhance user propensity to stake. However, many subsequently successful ve(3,3) projects have substantially reduced the rebase rate. This is because these projects found that providing overly generous rebase rewards to existing ve token holders led to the solidification of governance rights. As a result, the cost and threshold for latecomer participants to acquire governance rights gradually rose, leading to many potential participants opting out. This eventually contributed to the ossification of the system. By adjusting the proportion of rebase rewards in the total emissions for ve token holders, projects can strike a balance between "incentivizing early adopters" and "ensuring fair competition opportunities for latecomers".

The decision to retain the Rebase mechanism, and the choice of the right retention ratio, should be influenced by the specific dynamics of the chain where the ve(3,3) is implemented.

In scenarios where a chain has a stable ecological landscape and existing leading projects are likely to remain dominant, ve(3,3) projects should aim to secure these "customer protocols" early. This can be achieved by providing them with ample ve governance rights and the right to purchase liquidity freely in the early stage via governance rights. However, in a chain where the competitive landscape is chaotic, and the actual "large customer protocols" have not yet been established, ve(3,3) projects should avoid allocating excessive benefits to early ve governance right holders. This ensures equal opportunities for later entrants to compete.

But there lies a dilemma: the leading projects on mainstream public chains, which are most likely already listed on exchanges and possess superior liquidity, will be less motivated to purchase liquidity on Dex. In the long term, newer projects will always constitute the primary clientele for liquidity purchases. Therefore, reducing or eliminating Rebase has become the favored choice for ve(3,3) projects.

b. Team Information

The background of the founder, Blake Hooper, is in marketing software and managed services. Most of the project's videos have been recorded by him. The team consists of a core of five members and operates with a lean staffing structure.

c. Milestones

Despite these advancements, Equalizer's product-level differentiation is limited compared to other ve(3,3) projects, with less notable capacity for innovation and delivery.

2.3.2 Business Analysis

a. TVL and Associated Liquidity-Purchasing Cost

Based on the data from Defillama, Equalizer has a Total Value Locked (TVL) of $26,320,000 as of May 4th, 2023. The weekly emissions of EQUAL tokens during the same period are 45,435. Given that the price of EQUAL is $3.45 on that day, the weekly liquidity incentive is calculated to be $156,842. Therefore, we get a value of 26,320,000 / 156,842 = 167.81$. This indicates that Equalizer can sustain liquidity worth $167.81 for every $1 spent on incentives per week.

b.Trading Volume and Fee Revenues

Over the last three months, Equalizer's weekly trading volume has varied between $30M and $120M according to DefiLlama data. However, trading volume has seen a decrease since the start of April, standing at only about $30 million in the last two weeks. The recent week's fee income was also low, around $30,000.

c. Bribe Revenues and Partnered Bribe Projects

Publicly accessible information regarding Equalizer's previous bribe amounts is not available. However, for the current period (Epoch 25), there are 73 Pools open for bribery, and 50 Pools have already received bribes. But as this period was in its early stages at the time of writing, the bribe amount is not particularly high, and thus the data is not very informative.

Still, based on a screenshot from the official announcement for Epoch 23, the total weekly bribe amount for the top 20 bribe pools was approximately $95,544. Given this information, the total bribe amount for all pools for that week would be around $100,000.

As for the top 10 bribery projects, they mainly consist of DeFi projects, including revenue aggregators, derivatives, lending platforms, and a domain project.

d. Staking Ratio

As of the time of this writing, Equalizer's token staking ratio stands at 71.55%. Following its launch, the staking ratio peaked at 94% but gradually fell to its current levels.

This downward trend in the staking ratio aligns with the official data on new token staking, which indicates that the ratio of new tokens staked per day is approximately 71%.

Based on previous data, the annual percentage rate (APR) for voting in pools with higher bribe volumes is primarily within the range of 80% to 150%.

2.3.3 Summary

While Equalizer's liquidity is significantly less than Velodrome and Thena, its revenue and bribe amounts are relatively impressive. Despite the significant decline in its total value locked (TVL) over the last month compared to its competitors, which is closely tied to a drop in its token price, there remains a strong correlation between token prices and liquidity.

However, it's worth noting that the Fantom ecosystem, where Equalizer operates, has experienced a period of underperformance. Despite the return of Andre Cronje as an advisor, Equalizer's performance within the Fantom ecosystem has been underwhelming. Even Andre Cronje's return has not managed to turn the tide, with Fantom’s TVL falling to tenth place in DeFi space. Over the past year, only Terra, which fell to zero, and Solana, which was affected by the SBF incident and the collapse of FTX, have suffered such a decline. The future for L1s like Fantom looks challenging, particularly with the rise of L2s such as Arbitrum, Optimism, and Base attracting developers, users, and funds. Even AC recently expressed subtle dissatisfaction on Twitter with the Fantom team's slow marketing actions, although this tweet has since been deleted.

👉due to word limit, please check the rest of this article in Unpacking ve(3,3) DEX Innovations: Analysis of Velodrome , Thena,Equalizer and Chronos (Part II)