Funding rates are periodic payments made to either long or short traders, calculated based on the difference between the perpetual contract prices and spot prices. When the market is bullish, the funding rate is positive and tends to rise over time. In these situations, traders long on a perpetual contract will pay a funding fee to traders on the opposing side. Conversely, the funding rate will be negative when the market is bearish, where traders short on a perpetual contract will pay a funding fee to long traders.

The funding rate is primarily used to force the convergence of prices between the perpetual contract and the underlying asset. Unlike traditional futures, perpetual contracts have no expiration date. Thus, traders can hold positions to perpetuity unless he gets liquidated. As a result, trading perpetual contracts are very similar to spot trading pairs. As such, crypto exchanges created a mechanism to ensure that perpetual contract prices correspond to the index. This is known as the funding rate.

Funding rates are calculated using the following formula:

Funding Amount = Nominal Value of Positions * Funding Rate

(Nominal Value of Positions = Mark Price * Size of a Contract)

Please note: Binance takes no fees from funding rate transfers as funding fees are transferred directly between traders.

Funding payments occur every 8 hours at 00:00 UTC, 08:00 UTC, and 16:00 UTC for all Binance Futures perpetual contracts. In the event of extreme market volatility, Binance reserves the right to update the funding interval of a perpetual contract that differs from the default 8-hour funding interval according to the funding interval adjustment rules mentioned in Section 8 ‘Adjustment of funding interval’ below. You are only liable for funding payments in either direction if you have open positions at the pre-specified funding times. If you do not have a position, you are not liable for any funding. If you close your position prior to the funding time, you will not pay or receive any funding.

There is a 15-second deviation in the actual funding fee transaction time. For example, when you open a position at 08:00:05 UTC, the funding fee could still apply (you’ll either pay or receive the funding fee).

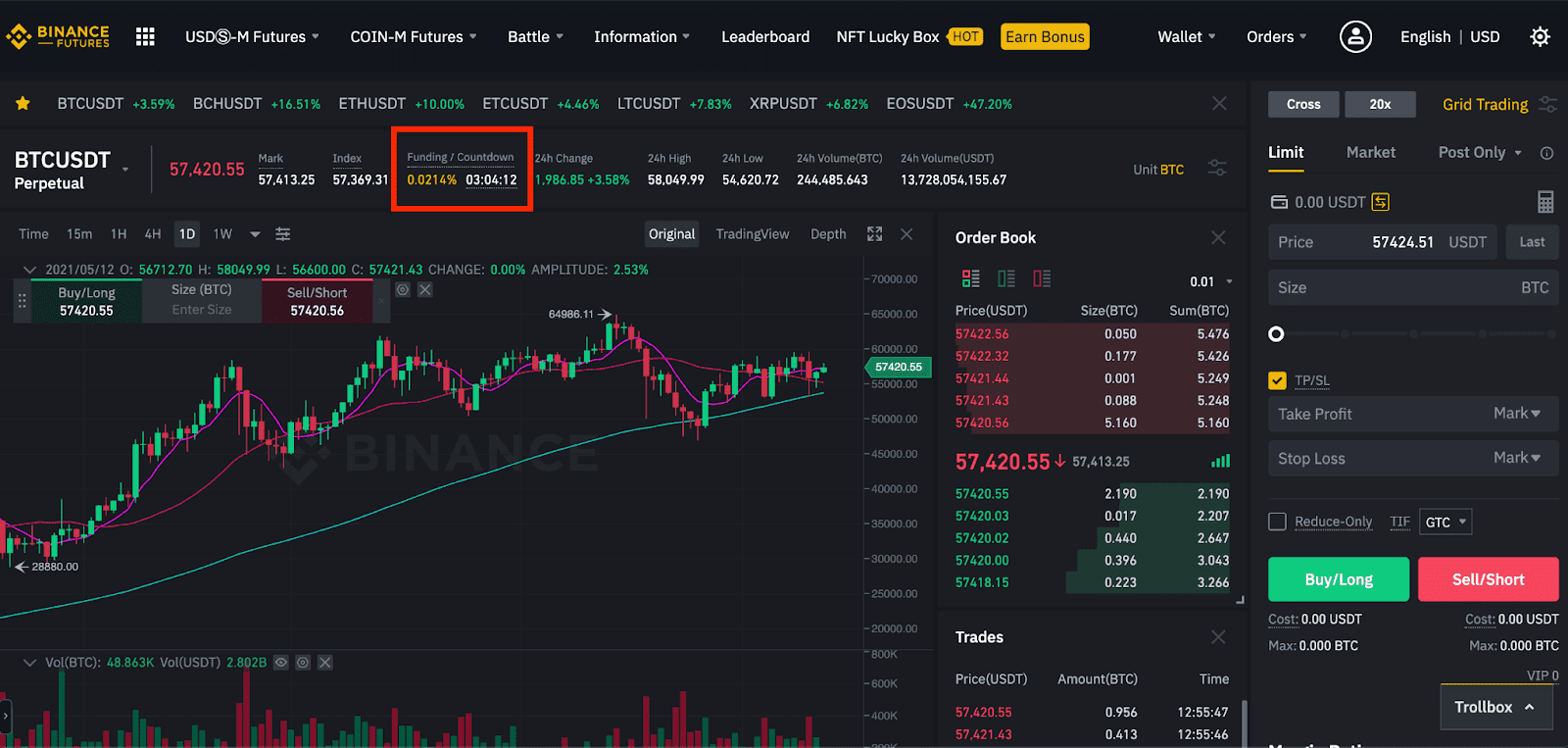

You can view the funding rates and the countdown timer to the next funding on the Binance Futures interface above the candlestick chart.

Please note: The funding rate here represents an estimation of the last 8 hours of the premium index. For example, at 09:00 UTC, the funding rate calculation uses the premium index dataset from 01:00 to 09:00 (rather than from 08:00 to 09:00).

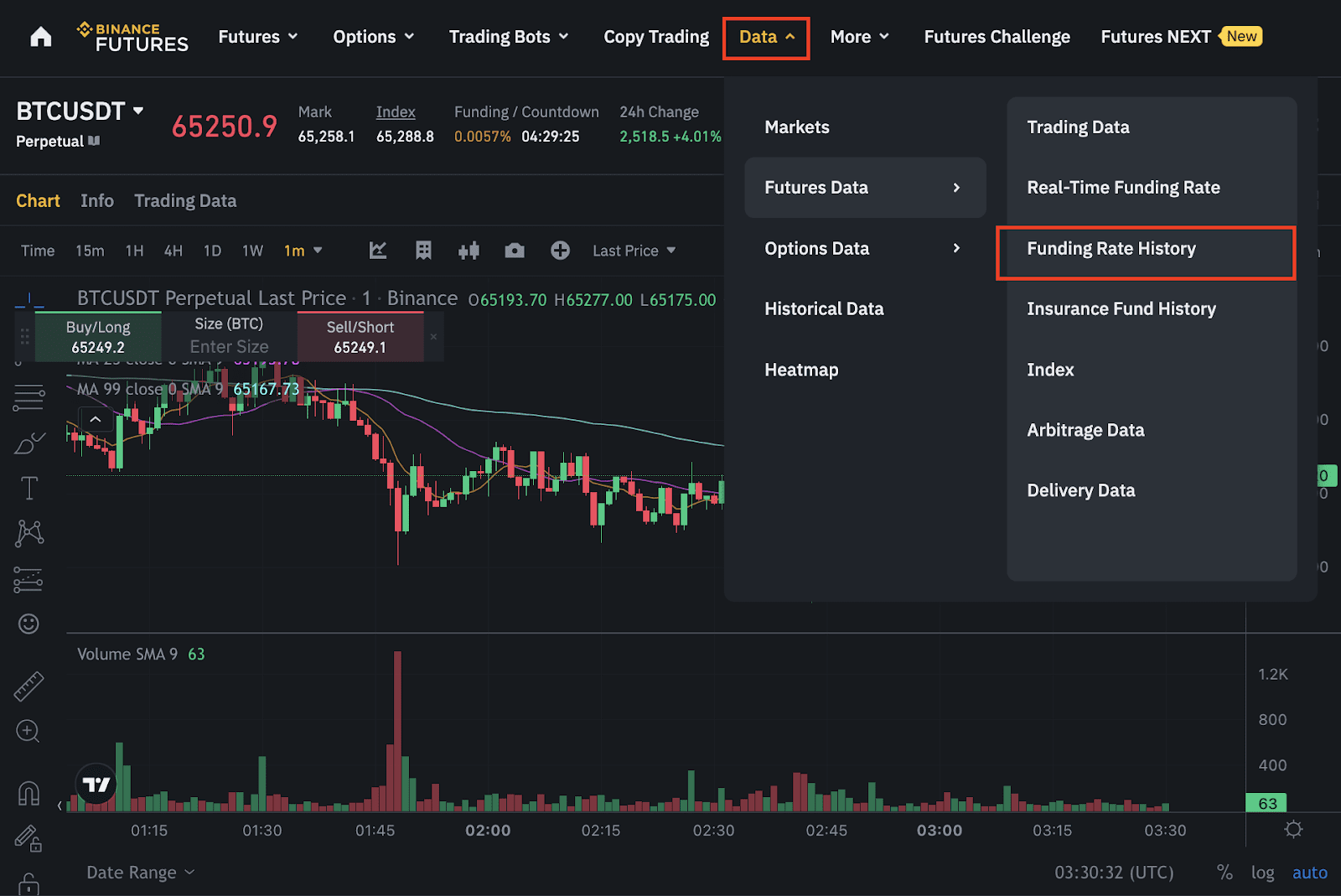

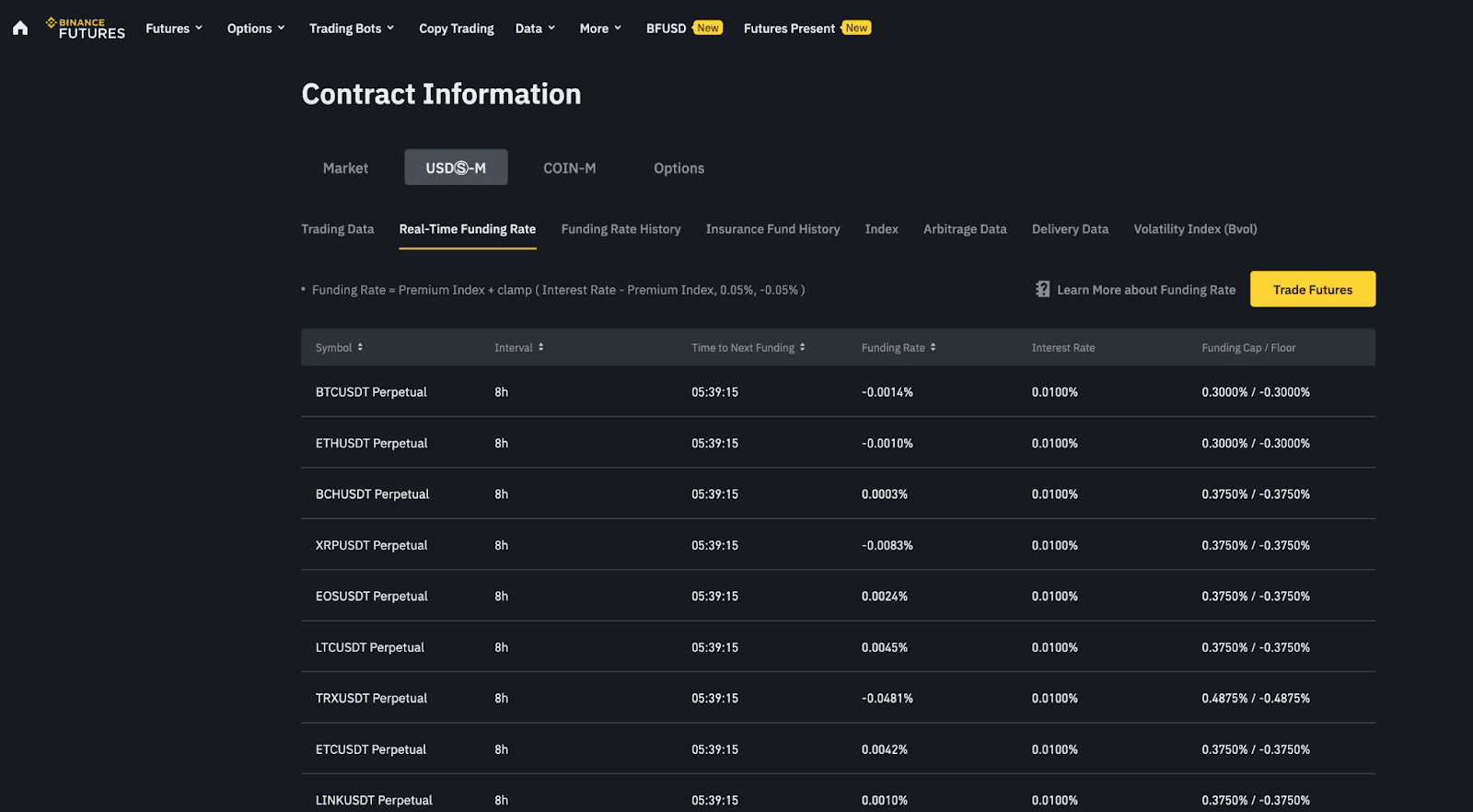

You can view the real-time and historical funding rates by clicking [Data] - [Futures Data], then select either [Real-Time Funding Rate] or [Funding Rate History].

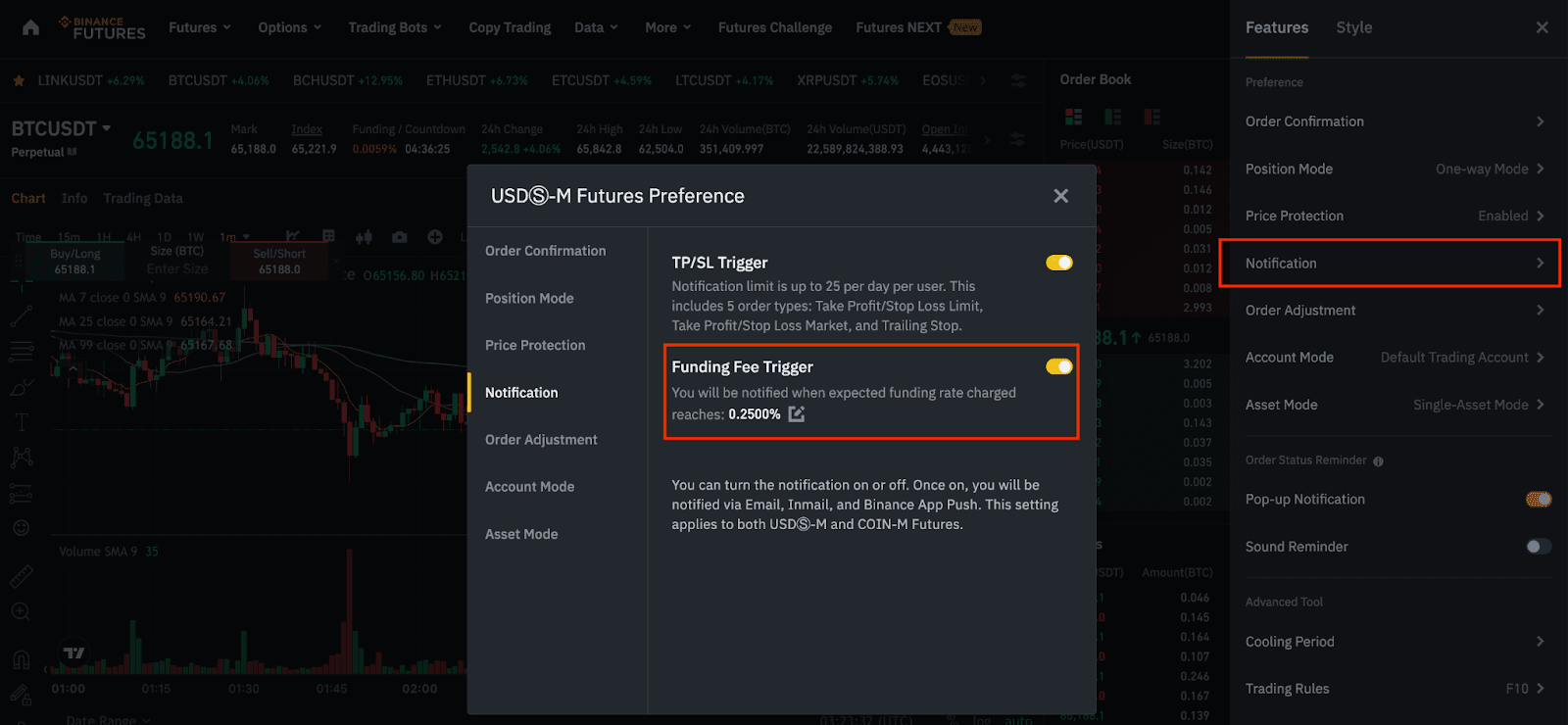

1. Go to the [USDⓈ-M Futures] trading interface and click the settings icon.

2. Go to the [Notification] tab to toggle on the [Funding Fee Trigger] button. You can also customize the funding rate charges percentage between 0.0001%-0.75%. Currently, it is defaulted to 0.25%, meaning you will be notified when the expected funding rate charges reach 0.25%.

Please note: You will be notified via email / in-app notification. This function serves as a risk warning and Binance cannot guarantee timely delivery. You agree that during your use of the service, under certain circumstances (including but not limited to personal network congestion and poor network environment), you may not be able to receive or receive delayed reminders. Binance reserves the right and has no obligation to deliver notifications.

There are two components to the funding rate: the interest rate and the premium. Binance uses a flat interest rate, with the assumption that holding cash equivalent returns a higher interest than BTC equivalent.

On Binance Futures, the interest rate is fixed at 0.03% daily by default (0.01% per funding interval since funding occurs every 8 hours). Please note that this doesn’t apply to certain contracts, such as ETHBTC, for which interest rate is set to 0%. Binance reserves the right to adjust the interest rate from time to time depending on market conditions.

There may be a significant difference in price between the perpetual contract and the Mark Price. On such occasions, a premium index will be used to enforce price convergence between the two markets. The premium index history can be viewed here. It is calculated separately for every contract:

Premium Index (P) = [Max(0, Impact Bid Price - Price Index ) - Max(0, Price Index - Impact Ask Price)] / Price Index

Impact Bid Price = The average fill price to execute the Impact Margin Notional on the Bid Price

Impact Ask Price = The average fill price to execute the Impact Margin Notional on the Ask Price

Impact Margin Notional (IMN) = 200 USDT / Initial margin rate at the maximum leverage level

For example, if the maximum leverage of BNBUSDT perpetual contract is 20x, and its corresponding initial margin rate is 5%, then the Impact Margin Notional (IMN) is 4,000 USDT (200 USDT / 5%), and the system will take an IMN of 4,000 USDT every minute in the order book to measure the average impact bid/ask price.

For more information, please visit Leverage and Margin of USDⓈ-M Futures.

Assume the following bid-side order book:

Level | Price | Base Quantity | Quote Notional Quantity | Accumulated Quote Notional Quantity |

1 | p1 | q1 | multiplier*p1*q1 | multiplier*p1*q1 |

2 | p2 | q2 | multiplier*p2*q2 | multiplier**p1*q1+multiplier*p2*q2 |

3 | p3 | q3 | multiplier*p3*q3 | multiplier**p1*q1+multiplier**p2*q2+multiplier*p3*q3 |

... | ... | ... | ... | ... |

n | pn | qn | multiplier*pn*qn | multiplier*∑pn*qn |

If multiplier *∑px*qx > IMN in Level x and multiplier * ∑px-1*qx-1 < IMN in Level x-1, then we can find the impact bid price from the Level x order book:

Impact Bid Price =IMN / [(IMN-multiplier *∑px-1*qx-1)/px+multiplier * ∑qx-1]

*IMN: Impact Margin Notional

To get the impact bid/ask price series, the system performs the above methodology over the order book snapshots in this funding period.

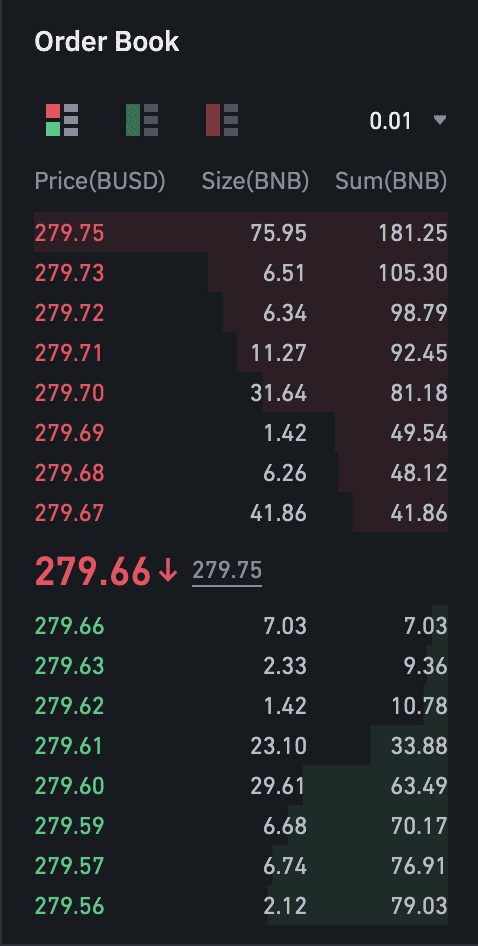

The ask order book is summarized as below:

Level | Price | Base Quantity | Quote Notional Quantity | Accumulated Quote Notional Quantity |

1 | 279.67 | 41.86 | (279.67 * 41.86) | 11,706.99 |

2 | 279.68 | 6.26 | (279.68 * 6.26) | (279.67 * 41.86) + (279.68 * 6.26) |

3 | 279.69 | 1.42 | (279.69 * 1.42) | …... |

4=x-1 | 279.70 | 31.64 | (279.7 * 31.64) | (279.67 * 41.86) + (279.68 * 6.26) + (279.69 * 1.42) + (279.7 * 31.64) = 22,704.65 < 25,000 USDT* |

5=x | 279.71 | 11.27 | (279.71 * 11.27) | (279.67 * 41.86) + (279.68 * 6.26) + (279.69 * 1.42) + (279.7 * 31.64) + (279.71 * 11.27) = 25,856.98 > 25,000 USDT* |

*Assume the maximum leverage of BNBUSDT perpetual contract is 125x and the contract default Impact Margin Notional is 25,000 USDT.

From the table above, we get the following figures:

Substituting into the formula:

Impact Ask Price = IMN / [(IMN-multiplier * ∑px-1 * qx-1)/px+multiplier * ∑qx-1]

= 25,000 / [(25,000 - 22,704.65) / 279.71 + 81.18]

= 279.69 USDT

Analysis:

Binance calculates the premium index every 5 seconds (12 premium index data points in a minute).

The number of data points used to calculate the funding rate n = 60/5 * 60 * hours of the funding interval

For example, the funding rate is calculated by taking the time-weighted average across all 5,760 premium index data points for the 8-hour funding interval.

Click to view the Premium Index History.

Premium index formula:

Premium Index (P) = [ Max(0, Impact Bid Price - Price Index ) - Max(0, Price Index - Impact Ask Price)] / Price Index

(Max(0,bpn-ipn)-Max(0,ipn-apn))/ipn

Sequence | Impact Bid Price | Impact Ask Price | Index Price | Premium Index |

1 | bp1 | ap1 | ip1 | (Max(0,bp1-ip1)-Max(0,ip1-ap1))/ip1 |

2 | bp2 | ap2 | ip2 | (Max(0,bp2-ip2)-Max(0,ip2-ap2))/ip2 |

... | ... | ... | ... | ... |

n | bpn | apn | ipn | (Max(0,bpn-ipn)-Max(0,ipn-apn))/ipn |

Case 1. For symbols of which the funding interval is greater than 1 hour, we use the premium index series in this funding period (from step 2), and substitute it to the average premium index formula:

Average Premium Index (P) = (1*Premium_Index_1 + 2*Premium_Index_2 + 3*Premium_Index_3 +···+ n*Premium_Index_n) / (1+2+3+···+n)

*Premium Index 1: the first premium index data point

n = 60/5 * 60 * 8 = 5,760 (Assume the funding interval is 8 hours)

Case 2. For symbols of which the funding interval is 1 hour, the average premium index is equally weighted.

Average premium index formula:

Average Premium Index (P) = (Premium_Index_1 + Premium_Index_2 + Premium_Index_3 +···+ Premium_Index_n) / n

n = 60/5 * 60 = 720

The funding rate is then calculated with this 8-Hour interest rate component and the 8-Hour premium component. A +/- 0.05% damper is also added. For example, the funding rates calculated from 00:00 - 08:00 are exchanged at 08:00.

The funding rate formula:

Funding Rate (F) = [Average Premium Index (P) + clamp (interest rate - Premium Index (P), 0.05%, -0.05%)] / (8 / N)

*Premium Index (P) here refers to the current average

*interest rate here refers to 8-Hour interest rate which is 0.01% for most symbols

*N is Funding Interval

Please note:

The function clamp (x, min, max) means that if (x < min), then x = min; if (x > max), then x = max; if max ≥ x ≥ min, then return x.

In other words, as long as the premium index is between -0.04% to 0.06%, the funding rate will equal 0.01% (the Interest Rate).

If (Interest Rate (I) - Premium Index (P)) is within +/-0.05% then F = P + (I - P) = I. In other words, the funding rate will be equal to the Interest Rate.

Example 1:

Time stamp: 2020-08-27 20:00:00 UTC

Price Index: 11,312.66USDT

Impact Bid Price: 11,316.83 USDT

Impact Ask Price: 11,317.66 USDT

Premium Index(P) = Max(0, Impact Bid Price − Price Index ) − Max(0, Price Index − Impact Ask Price) / Price Index

=Max(0, 11,316.83 - 11,312.66) - Max(0,11,312.66 - 11317.66) / 11,312.66

= (4.17 - 0) / 11,312.66

= 0.0369%

Please note: This example is within the funding period 16:00 - 24:00 (UTC), the actual premium index at 20:00 (UTC) needs to be taken from the time-weighted average across all indices to the 16:00 - 20:00 (UTC) funding period.

Example 2:

Time stamp: 2020-08-28 08:00:00 UTC

Mark Price: 11,329.52

This is the end of the funding period 00:00 - 08:00 (UTC), 8 hours = 480 minutes, so the 8-hours weighted average Premium Index (P) = 0.0429%.

Average Premium Index = (1*Premium_Index_1+2*Premium_Index_2+3*Premium_Index_3+···+ n*Premium_index_n)/(1+2+3+···+n)

Premium_Index_1: the first premium index data point

Funding Rate (F) = Premium Index (P) + clamp(interest rate - Premium Index (P), 0.05%, -0.05%)

= 0.0429% + Clamp(0.01% - 0.0429%,0.05%, -0.05%)

= 0.0429% + (-0.0329%)

= 0.0100%

Floor = -0.75 * Maintenance Margin Ratio

Cap = 0.75 * Maintenance Margin Ratio

Capped Funding Rate = clamp(Funding Rate, Floor, Cap)

*Funding Rate (from Step 4)

The funding rate of each contract is calculated based on its corresponding "initial margin ratio" and "maintenance margin ratio" at the maximum leverage level. For initial margin ratio and maintenance margin ratio, please refer to Leverage and Margin of USDT Futures Contracts for more details.

For example: To calculate the floor and cap of ADAUSDT perpetual contract, the corresponding "initial margin ratio" and "maintenance margin ratio" in the table at the maximum leverage level 75x are 1.3% and 0.65% respectively.

**In the event of extreme market conditions, Binance reserves the right to adjust the funding rate cap and floor parameters.

In the event of extreme market volatility, Binance reserves the right to update the funding rate floor and cap (with adjusted values respectively capped at -1 for floor and 1 for cap), as well as the funding interval of a perpetual contract that differs from the default 8-hour funding interval. You can visit the real-time funding rate and funding rate history pages to find out the latest funding interval and funding rate cap / floor.

Please note: Funding fees (if any) will be deducted from the available balance in your Futures Account. If your account balance is insufficient, the funding fees (if any) will be deducted from your position margin, which may affect your liquidation price. Please manage your positions accordingly to avoid any liquidation risks.

Effective from 2025-05-02 08:00 (UTC), Binance Futures will adjust the settlement frequency from every eight hours or every four hours to every one hour when the previous funding rate settlement of USDⓈ-M perpetual contracts reaches the funding rate cap/floor.

Taking USDⓈ-M BTCUSDT perpetual contract as an example, the funding rate cap/floor of USDⓈ-M BTCUSDT perpetual contract is +0.3% / -0.3% and the default funding rate settlement frequency of USDⓈ-M BTCUSDT perpetual contract is every eight hours.

USDⓈ-M BTCUSDT perpetual contract funding rate at 2025-04-22 at 08:00 (UTC) reaches -0.3%, the next funding rate settlement will be adjusted from every eight hours to every one hour. The new funding rate settlement frequency will start from 2025-04-22 at 09:00 (UTC).

The new funding rate settlement frequency for USDⓈ-M BTCUSDT perpetual contract will be as follows:

Time | Max Funding Rate |

2025-04-22 08:00 (UTC) | +0.3% / -0.3% |

2025-04-22 09:00 (UTC) | +0.3% / -0.3% |

2025-04-22 10:00 (UTC) | +0.3% / -0.3% |

2025-04-22 11:00 (UTC) | +0.3% / -0.3% |

… |

USDⓈ-M BTCUSDT perpetual contract funding rate at 2025-04-22 at 07:45 (UTC) reaches -0.3%. However, at the funding rate settlement time at 2025-04-22 08:00 (UTC), the funding rate is -0.25%. No adjustment will be made on funding rate settlement frequency because the funding rate did not reach the funding rate cap/floor at the funding rate settlement time.

Important Notes: