In 2022, Ethereum MEV revenue exceeded US$300 million, and a robot spent only US$2,057 to arbitrage approximately US$3.2 million from two Uniswap pools.

Written by: EigenPhi

Compiled by: Peng SUN, Foresight News

* Note: The clearing transaction statistics calculated in this report cover the period from May to December 2022, while the statistics for other types cover the whole year of 2022.

1. A new perspective on MEV

Currently, most reports and articles on the topic of MEV revolve around the introduction of concepts and how to introduce orders into the MEV market. Issues of concern include but are not limited to the fairness of the MEV market, the negative externalities brought by MEV, and the centralization risks or censorship issues related to mechanism design. These are the directions that many blockchain protocol and application layer builders are working hard to address.

In addition, Amber Group and Forbes also wrote articles introducing a large number of long-tail MEV cases, the inside story of the gold-digging strategy of the famous MEV searcher Nathan Worsley, and Wintermute and Alameda Research, two quantitative institutions that run MEV strategies. Their articles have raised the concept of "Payment for Order Flow", which seems to be a big trend that developers are working on, including Cowswap, 1inch Fusion model and Flashbots' MEV-Share. Mainstream financial institutions have also begun to pay attention to the MEV field. For example, Nasdaq's News and Insights column forwarded CoinDesk's article on how JIT robots and MEV promote DeFi. Of course, there are also a small number of people who pay attention to the regulation of the MEV market.

In fact, in addition to the general attention paid to the operation of the MEV macro market mechanism, we believe that there is also a micro issue that deserves attention: as a representative, MEV transactions mean that liquidity data has unprecedented opportunities and challenges.

As early as May 2022, in a series of events triggered by the UST-LUNA circuit breaker, financial institutions engaged in crypto business have been targeted by users and publicly disclosed their balances. This situation is not common in traditional finance, because the transparency and openness of blockchain ledgers allow anyone to obtain transaction data for free. Through on-chain transactions, we can obtain historical price information and liquidity data generated and updated in real time. Of course, the transparency of liquidity data can also help crypto financial institutions establish real-time risk control mechanisms based on liquidity and realize crises earlier.

This report aims to encourage users to pay attention to the value and risks of existing liquidity data in order to better protect assets or design better protocols to protect users.

II. Overview of the MEV Market in 2022

MEV is the truest manifestation of DeFi market liquidity. In 2022, MEV robots generated at least $307 million in revenue on Ethereum. Therefore, this section will provide an overview of the MEV market in 2022.

1. MEV trading opportunities increased throughout the year

In 2022, the number of MEV transactions increased over time. Arbitrage bots traded the most frequently, accounting for 68.3% of the market, and sandwich attacks were about 30.6%. The chances of liquidation transactions were much smaller than the other two MEV types, and although their statistical range was from May to December, this difference was not significant. Therefore, compared with traditional arbitrage transactions, liquidation opportunities are more likely to depend on violent market fluctuations.

Meanwhile, the total number of monthly MEVs is trending upward, reflecting the steadily increasing opportunities for MEV seekers in the market.

2. Market share and trends of different MEV types

The MEV income that searchers can generate from the market comes from three different types, namely arbitrage gains from narrowing price differences between markets, sandwich attack gains from front-running user transactions, and liquidation gains from exploiting the difference between debt and collateral value during market fluctuations.

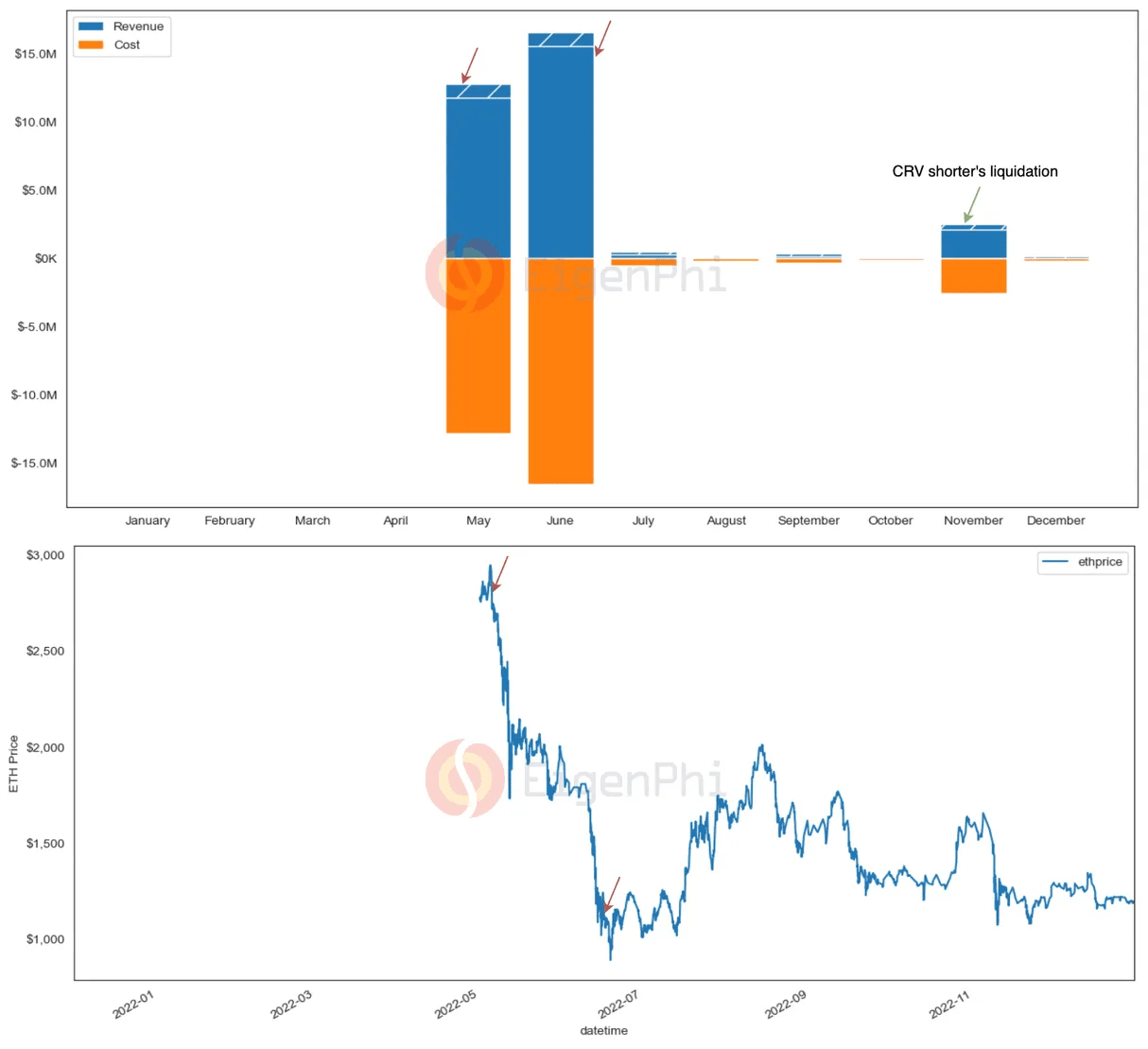

The following is an overview of the revenue, costs and profits of MEV transactions. (Note: liquidation data starts from May)

Mainstream MEV robots generated at least $307 million in revenue in 2022, of which MEV seekers received $145 million in total revenue from arbitrage trading, accounting for more than 47.5% of the total revenue, and $128 million from sandwich attacks, accounting for about 41.7%. Although the two have similar revenues, sandwich MEV has significantly higher costs and lower profits than arbitrage trading. Arbitrage seekers generated $75 million in profits, while sandwich attacks only generated $26 million in profits. Starting in May 2022, clearing transactions had a total revenue of $33 million and a cost of $16 million, and the clearing robot ultimately generated more than $16 million in profits from the market. In fact, sandwich attackers paid costs to block builders and validators that accounted for nearly 79% of their revenue. As can be seen from the figure below, compared with arbitrage trading, sandwich trading has a higher monthly "cost-to-income ratio", with an average of 0.78 for sandwich trading and 0.49 for arbitrage trading.

In general, the revenue generated by arbitrage seekers is relatively high in January, May, June and November, and stable in the rest of the months. Except for November, the revenue of sandwich robots showed a downward trend in the third and fourth quarters. Among the monthly revenues generated by liquidation transactions, the revenues in May, June and November are significantly higher than other months, because the sharp drop in ETH in May and June and the CRV short squeeze event led to liquidation opportunities.

3. MEV Robot

The chart below shows that a large number of bots generate negative profits, 68% of arbitrage bots generate positive profits, 67% of sandwich bots, and 51% of liquidation bots.

As for the life cycle of MEV robots, a large proportion are one-time robots, and long-term robots account for a smaller proportion. Seekers can use one-time robots for testing, and once a viable strategy is determined, the robot will be transferred to a new address to execute the strategy for a long time. On average, the life cycle of arbitrage robots tends to be shorter than that of sandwich and liquidation robots.

In addition, this article also ranks the top 10 most profitable robots according to the profit of MEV robots and their percentage of the total profit of all robots. The data shows that the top 10 arbitrage robots account for about 51.3% of the profits, the top 10 sandwich robots account for 74.8% of the profits, and the top 10 liquidation robots account for as much as 90.2% of the profits.

Liquidation bots are highly competitive, with the top two liquidation bots accounting for more than 53% of profits, dominating the market, and other liquidation bots must find ways to surpass these top bot strategies to gain market share. Interestingly, the most profitable arbitrage bot, 0xbad, performs fewer trades because he created the most profitable single arbitrage trade, which generated more than $3 million in profits through a single atomic trade during the Nomad cross-chain bridge vulnerability in August, indicating that strategy is extremely important for MEV.

4. MEV before and after The Merge

In 2022, a total of $133.8 million in MEV value was distributed to miners or block builders who were responsible for collecting transactions and building blocks. The MEV values paid for arbitrage transactions, sandwich attacks, and liquidation transactions were $45.8 million, $73.9 million, and $14.1 million, respectively. Among them, sandwich attacks contributed more than half of the MEV to miners or block builders and were their main source of incentives. After the Ethereum merger, the percentage of MEV contribution from sandwich transactions also increased.

In the first 100 days of the Ethereum merger, Ethermine and F2Pool accounted for 31.46% and 13.91% of MEV revenue respectively. After the merger, the top two block builder addresses extracted more than half of the MEV, accounting for 30.4% and 29.41% respectively. Although changes in the off-chain auction market for block space affect the distribution of MEV, the oligopoly pattern remains unchanged.

(V) Transaction volume calibration involving MEV

In 2022, the total MEV trading volume in which Sandwich robots participated was $287 billion, accounting for 87.5%, which is significantly higher than the arbitrage trading volume. Similarly, Sandwich trading volume always dominates the total MEV trading volume in each month. Perhaps because the collapse of FTX caused a large number of users to flock to DEX to exchange assets, the growth of Sandwich trading was particularly obvious in November.

Uniswap V3 is the most popular protocol for arbitrage bots and sandwich bots, with a total trading volume of $72.8 billion. Compared with arbitrage trading volume, Uniswap V3's sandwich trading volume is an order of magnitude higher. For protocols such as DODO and Uniswap V3, sandwich trading volume accounts for almost half of the total trading volume, which is worth considering for users.

6. Comparison of MEV Market on Ethereum and BNB Chain

As for different blockchain platforms, MEV opportunities on BNB Chain are much more cost-effective than Ethereum, as the average cost-to-revenue ratio (CRR) of arbitrage bots on BNB Chain is significantly lower than that of Ethereum. In 2022, the total revenue generated by arbitrage seekers from BNB Chain was $95 million, lower than Ethereum's $145 million arbitrage revenue, but the total profit generated by BNB Chain seekers was $90 million, higher than Ethereum's $75 million.

Arbitrage bots on BNB Chain do not face as much competition compared to Ethereum. The top 10 arbitrage bots generate 25% of the profits on BNB Chain, which is lower than Ethereum’s 51.3%. Therefore, the opportunities for arbitrage bots on BNB Chain are fairer than those on Ethereum. Newcomers are more likely to find a friendly environment to explore BNB Chain.

3. Current status and prospects of MEV market

Based on the above data analysis, this section will reveal the current main trends and new opportunities of MEV in the future.

1. Current situation: MEV infrastructure

The most critical infrastructure of the MEV market is the auction market, which ensures that the transactions of MEV robots are packaged on the blockchain. In order to achieve a fairer MEV market (at least this is the vision of Flashbots), this auction market began to be subdivided from the original Dark Forest (Mempool) to the off-chain professional auction market provided by relayers represented by Flashbots' MEV-geth.

After the merger, the Ethereum Foundation began implementing the pre-PBS scheme. In the PBS scheme, block builders such as Flashbots and builder0x69 bid for the right to build the next block, and validators propose the block with the highest bid. This approach effectively subdivides the process of packaging MEV transactions into two auction markets, one opened by block builders for MEV robots to bid for block space, and the other opened by validators for builders to bid for the right to build the next block. Block builders and validators can also be routed through third-party relayers such as MEV-boost to achieve data privacy and maintain fairness. The degree of competition in the two auction markets will affect the distribution of revenue for MEV robots.

Centralization vs. decentralization. As shown in the chart from mevwath.info, OFAC-compliant blockchains are in a fierce battle with non-OFAC-compliant blockchains.

Financial engineering infrastructure is often overlooked by the market. In the future, MEV robots will tend to provide more high-end and professional financial engineering services for the DeFi ecosystem, and they need to rely on data services and financial derivatives to enhance their performance.

Flash loans are a typical financial tool popular with MEV robots.

2. Discussion: Outlook for new opportunities in 2023

In 2022, there is a strong trend of increasing opportunities for MEV robots to extract value from DeFi protocols. Arbitrage trading remains the dominant type of MEV market, accounting for the majority of revenue and profit. Moreover, arbitrage robots trade most frequently in most months, and pay a smaller proportion of revenue to rent seekers than sandwich robots. A comparison of the total number of independent robot addresses also shows that arbitrage robots are more diverse, suggesting that there may be other thresholds for sandwich robots and liquidation robots.

A new MEV bot called JIT has seen an increase in trading opportunities over the past few months. As JIT bots provide a large amount of centralized liquidity, there seems to be a trend of more and more independent exchange users who can benefit from JIT activities. Slippage data from actual exchange trading and simulations also confirms this. Compared with other kinds of active liquidity management strategies, JIT bots are trying to provide liquidity in an innovative and more capital-efficient way. It is worth considering that related parties such as AMM protocol designers directly provide similar functions, which can connect exchange users and liquidity providers in a new way, while improving user experience and increasing liquidity providers' income.

In addition to these mainstream MEV robots, another off-chain MEV market is open in some DEXs and aggregators. Users' trading orders are transmitted directly to the routers created by these protocols in the form of dark pool orders or limit orders. Seekers can access these invisible orders to the memory pool under a set of auction rules and extract value by providing optimized settlement services. The Payment for Order Flow business seems to be a big trend that developers are working on, including Cowswap, 1inch Fusion model, and Flashbots' MEV-Share. Although this model was controversial when it was adopted by Robinhood very early, there is currently no clear regulatory policy.

If users are rewarded for providing information, Payment for Order Flow is actually a kind of MEV democratization. MEV democratization is a topic often discussed in the community. Another suggestion is to distribute part of the validator's MEV income to the Ethereum community through liquidity staking, although this has not yet been achieved given the current interest rates of liquidity staking platforms such as Lido Finance. The booming MEV market has also attracted developers of DeFi protocols to think about how to use MEV to improve customer experience and protect customer interests.

IV. MEV transactions worth watching in 2022

1. The Beauty of Arbitrage

On August 1, 2022, the arbitrage robot 0xbaDc made a profit of $3.197 million from a single space arbitrage between two Uniswap WETH/WBTC pools, spending $2,057 to run a large exchange transaction in reverse in the Nomad cross-chain bridge vulnerability.

2. Diversified Sandwich Trading

Sandwich attack patterns are becoming increasingly sophisticated, with a sandwich attack involving 56 victims in 2022, as well as sandwich attacks when adding/removing liquidity.

56-transaction sandwich attack: On Uniswap V2, there were 56 transactions in a block that exchanged WETH for MEME, and the sandwich bot attacked them all together. This shows that the sandwich bot does not necessarily attack only one transaction, and splitting a large order into multiple small orders does not guarantee that the trader can escape the fate of being attacked.

Sandwich attacks on adding/removing liquidity: Sandwich bots do not necessarily attack exchange transactions on DEXs, adding and removing liquidity can also be attacked. In past studies, sandwich attacks on adding liquidity can be seen as risk-free arbitrage on the change in slippage before and after adding liquidity to the pool. The attacked liquidity provider and other liquidity providers may bear losses. Similarly, removing liquidity can also be attacked, and liquidity providers may also bear similar losses. Therefore, liquidity providers should set checkpoints carefully and be aware that sandwich attacks will profit from their losses.

3. The Dilemma of the Leveraged Sandwich

In some skilled sandwiches, flash loans provide the funds needed for leverage, and traders only need to invest a small portion of their funds in front-running transactions, thereby pushing up the transaction price for the victim and prolonging potential gains. However, the downside of this is that the risk of the sandwich robot will also increase. In particular, if the front-running transaction is packaged successfully, but the corresponding back-run transaction is not successful, the sandwich robot will lose money. Sandwich robots using this strategy may need to pay higher MEV costs to prioritize transactions.

4. Long-tail MEV transactions

MEV types may not be limited to arbitrage, liquidation, sandwich or JIT, and the multi-attack in 2022 can also be classified as long-tail MEV.

In the Abracadabra arbitrage incident, the attacker exploited the price cache design of the protocol and used the update mechanism of the protocol's price oracle to complete the arbitrage. In the Mongo Squeeze and CRV short-queeze incidents, the attacker manipulated the market liquidity and created bad debts on the corresponding lending vaults. In the Ankr attack incident, the attacker used the stolen private key of the Ankr deployer to attack the token issuance mechanism and successfully obtained benefits.

At the same time, the large capital flows that accompany transactions often provide opportunities for traditional MEV robots, and large exchanges within AMMs also bring important arbitrage opportunities. As mentioned above, months involving major risk events are often accompanied by higher overall arbitrage profits. In addition, the huge price changes associated with the liquidity manipulation of CRV shorts provide more opportunities for liquidation robots. For example, during the CRV short squeeze event, a liquidation robot implemented a profitable liquidation strategy during the drastic changes in CRV prices, earning more than $1 million in revenue.

5. MEV Robot and DeFi Ecosystem

Since the concept of MEV became popular, most people's first impression of it is negative. MEV incentivizes miners to rent-seek to obtain a large amount of revenue from packaging transactions, and PGA competition between MEV robots increases the average transaction fee level of Ethereum. More importantly, MEV may also threaten the security and decentralization of the blockchain protocol itself. MEV robots can extract value by monitoring pending transactions and front-running transactions or sandwich attacks, which is a negative externality that many protocol developers try to mitigate.

But one must face the fact that MEV is fundamental due to the nature of blockchain protocols in achieving openness and transparency. From the perspective of DeFi protocols, MEV robots can also provide multiple values. The most common arbitrage robots detect price differences between DEX or CEX and make profits by buying low and selling high. Their calculation of price deviations in liquidity pools improves the efficiency of market price discovery. Liquidation robots monitor the health ratio of collateralized loans and initiate liquidations when the value of collateral dives, which helps the deleveraging process, especially during market fluctuations.

In the future, just like the JIT robots and statistical arbitrage market makers that have appeared in this market, there will be more different robots that are proficient in calculations, profit from data analysis and financial engineering, and are an important part of the smooth automation of the DeFi system.

On the other hand, the interaction between MEV robots and other participants in the DeFi protocol has also become more complex and important. As revealed by the alternative sandwich robots and JIT robots, the victims of sandwich robots are not necessarily just exchange users, but also liquidity providers. Due to the existence of sandwich robots, exchange users will not necessarily bear more slippage losses, but may benefit from the slippage discount brought by JIT robots.

In 2022, EigenPhi conducted an in-depth analysis of the impact of MEV on the two major DEX protocols Uniswap V3 and Curve. On Uniswap V3, the revenue scale of mainstream MEV robots accounts for 25% of the liquidity provider's revenue. On Curve, MEV trading volume accounts for 20% of the total trading volume on most days.

According to EigenPhi analysis, in 2022, arbitrage and sandwich bots contributed a total of $328 billion in trading volume to DEX, accounting for approximately 49% of the total trading volume of $666 billion generated on DEX that year.

In summary, we can see that MEV robots have become an integral part of the DeFi community that cannot be ignored. Understanding the transaction relationship between MEV robots and other entities can help stakeholders better understand the long-term impact of MEV on AMM.