Old players of options often hear that some institutions use the Gamma scalping strategy but do not understand why. I also used the chat GPT that comes with SP to look up the definition of the strategy. At the same time, the following article will try to explain the Gamma scalping strategy and its applicable scenarios by combining theory and practical examples.

1. Introduction to Gamma

1. Delta Introduction

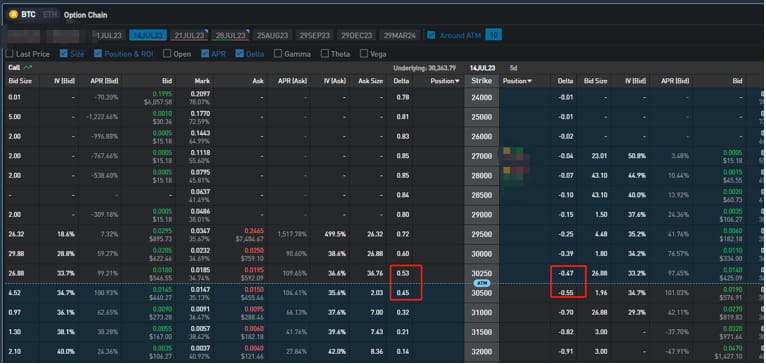

Those who have learned the Greek letters of options know that delta is the first-order derivative of the option premium with respect to the price. And delta has some obvious characteristics. For example, for options expiring on the 14th of this month, the absolute value of delta for at-the-money options is about 0.5. Due to the direction and probability properties of delta, many institutional investors will deliberately adjust their investment portfolios to be delta-neutral.

2. Gamma Introduction

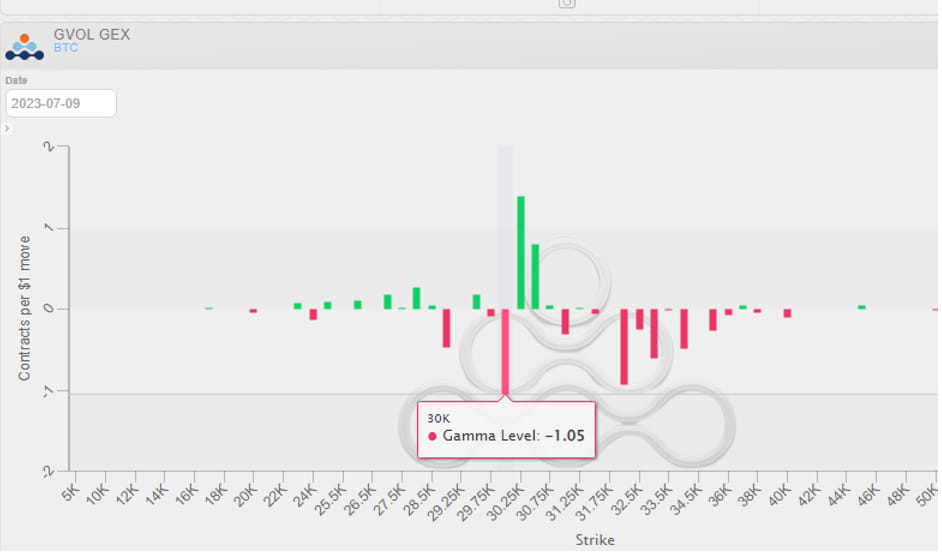

In mathematical terms, Gamma is the second-order partial derivative of option prices. If you are not clear about Greek letters, you can look up my options column, which has a special description of Greek letters. You can also check out the introductory course of the Options Academy, where I gave a special explanation. The main description is the price sensitivity of Delta to underlying assets such as Bitcoin. Gamma is the largest near at-the-money options. At this time, smaller changes in Bitcoin prices will cause larger delta changes, thereby driving Gamma to jump more, while the Gamma of OTM and ITM options are both normally distributed and close to 0. Because the Gamma of sell options is negative, some people always believe that the Gex value of the maximum -Gamma is the maximum pain point, which is actually a fallacy (for example, the description of 3W as the maximum pain point in the figure below).

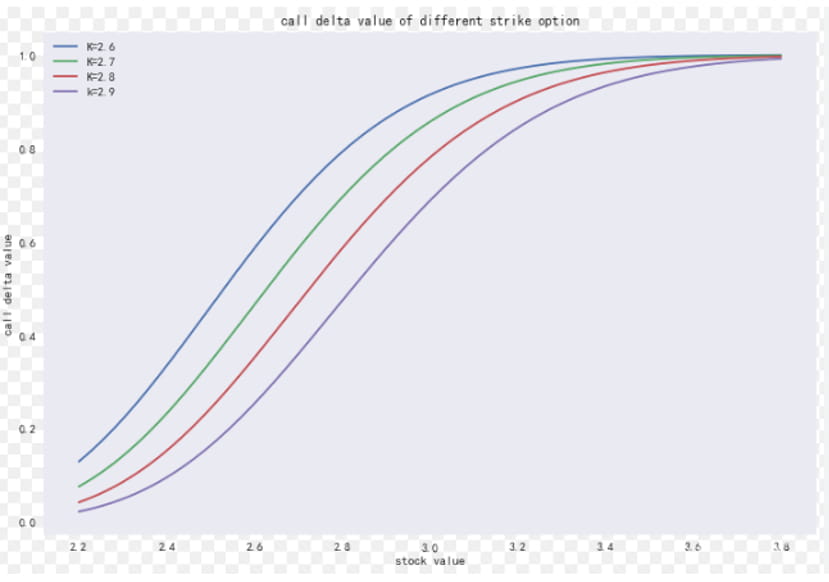

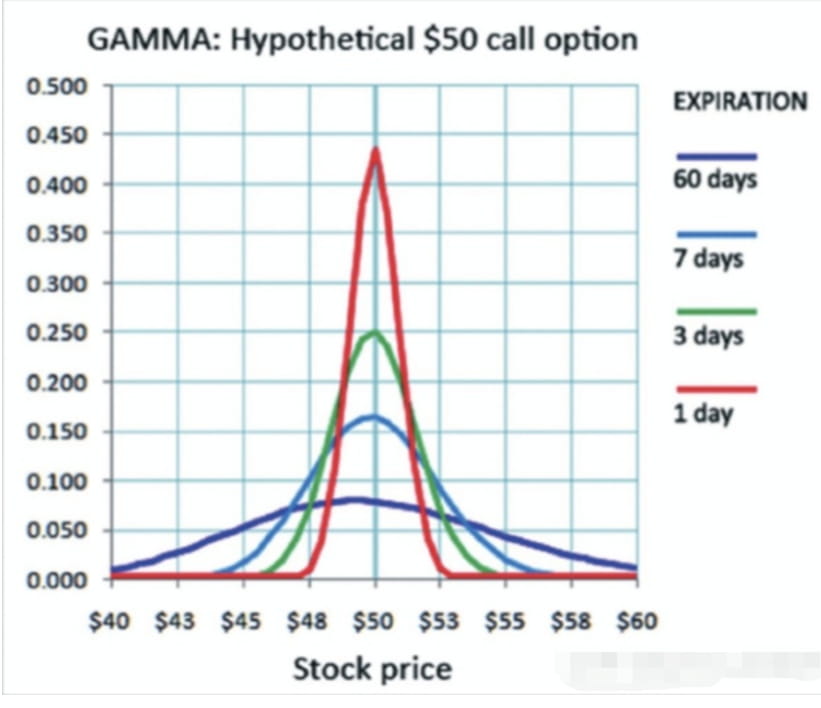

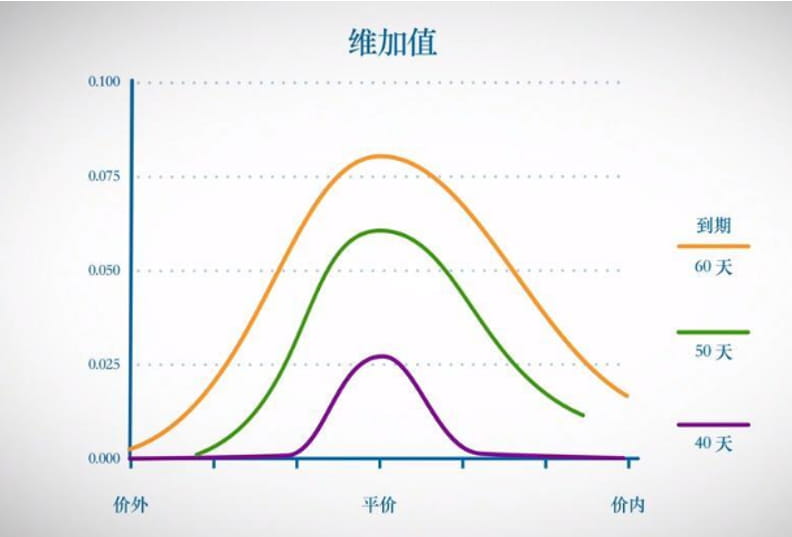

The following figure shows the difference in Gamma of options contracts with different expiration dates. To put it simply and crudely, the shorter the period, the greater the impact of Gamma, while vega is just the opposite. (Comparing the two figures, you will have a deeper understanding of Greek letters)

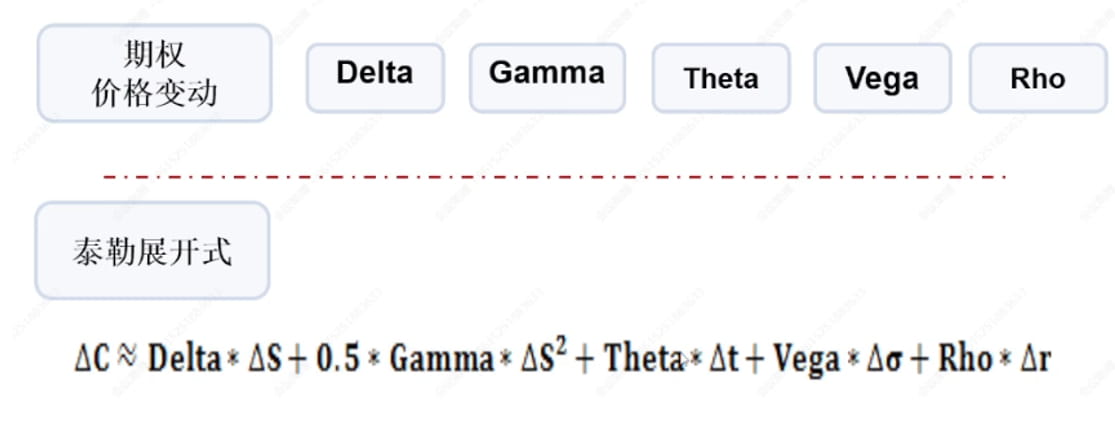

2. Taylor expansion and Gamma Scalping strategy principle

1. Important Taylor expansion of option price changes

I guess you guys will complain after reading this. Am I taking a college math class? Don’t worry. If you don’t understand math or understand the principles of some complex strategies, how can you apply them? If you want to keep it simple, then open a long or short position at 125 times the futures price. Lol.

2. Gamma Scalping Strategy Principle

To define the Gamma Scalping strategy in one sentence, it is actually a strategy to obtain Gamma returns by keeping delta neutral through hedging.

A careful observation of the Taylor expansion in the figure above shows that the interest rate rho is constant in the short and medium term, and the fifth term is equal to 0. If IV is assumed to be flat in the short term, the fourth term is equal to 0. Since delta neutral hedging is done, the first term is also 0. The key is to look at price changes, Gamma and theta determine the pnl of the overall combination. If it is a buy strategy, it is necessary to observe whether the Gamma gain can exceed the theta loss.

In actual operation, using big pie spot and options and buying strangles are common Gamma Scalping strategies. (Just keep delta neutral)

3. How to apply

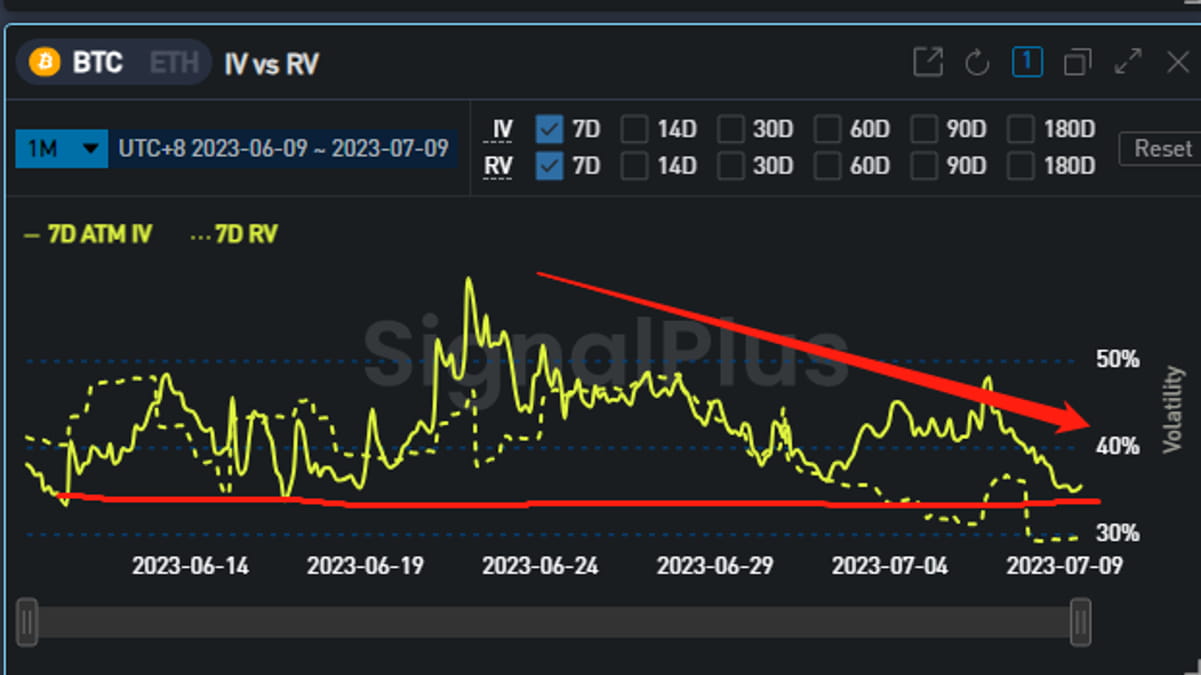

For example, taking the current IV of Bitcoin as an example, it has reached the lowest value in nearly a month.

Delta-neutral strategy through buying straddles

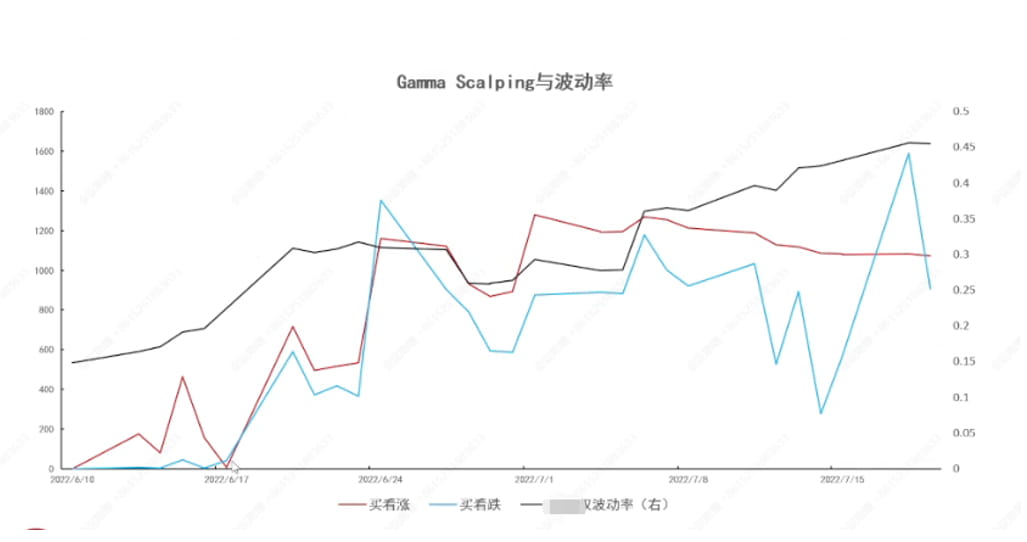

The following figure shows the combination of buy call and buy put with IV. In fact, it can be clearly seen that after delta hedging, the prediction of IV is still the core of the transaction.

Short-term long gamma returns are higher, and vega generally contributes positive returns.

Conclusion

The various Greek letters of options are the main measure of option return risk; the gamma scalping strategy is to maintain delta neutrality through a combination of options or options and big bitcoin spots, and to achieve profits when the gamma gains exceed the theta losses in the long term; at the same time, we have also found through observation that while long gamma gains profits, vega also plays a supporting role. In addition, when selling options to hedge short gamma, the strategy returns can be increased when IV is high.

To sum it up in one sentence, its essence is to be neutral through the target delta, not affected by price, and mainly adopt a strategy of buying low and selling high through volatility. The core here is still the judgment of IV.