Author: Will Owens, Research Analyst at Galaxy Digital; Translated by: Jinse Finance xiaozou

In July, Galaxy Research pointed out that the effectiveness of the Digital Asset Treasury (DAT) model depends on the maintenance of the company's equity premium. At that time, the trading price of these stocks exhibited a significant premium compared to the net asset value (NAV) of their underlying Bitcoin (or other cryptocurrencies), which was supported by a value appreciation cycle between price, issuance, and asset accumulation.

The Bitcoin treasury model is essentially a liquidity derivative. It is only effective when the company's stock trades at a premium relative to its Bitcoin net asset value. Once these premiums disappear, the entire growth flywheel will reverse.

The core warning from Galaxy Research's July report on Bitcoin treasury companies and the broader DAT report is: once premiums narrow, stock issuance shifts from value-adding to dilutive, this reflexive cycle can stagnate. And this situation has now become a reality.

Bitcoin has fallen from a high of about $126,000 in October to a low of about $80,000 (and has rebounded to around $92,000 at the time of writing), severely impacting trading of high-beta treasury assets. The macro context has increasingly shifted to a risk-averse mode: inflows into cryptocurrency exchange-traded funds (ETFs) have slowed, and speculative enthusiasm in the public market has weakened. As Galaxy Research noted in October, the deleveraging event on October 11 triggered a significant wave of forced selling, clearing leverage from the system and leading to a significant deterioration in liquidity conditions entering the fourth quarter.

For treasury companies whose stocks previously served as leveraged cryptocurrency trading tools, the impact of the market shift is particularly severe. Financial engineering that once amplified upward gains now similarly exacerbates downward risks.

Note: This report discusses only Bitcoin DAT. Companies investing in ETH or SOL can obtain returns through staking or DeFi lending in addition to capital appreciation, and thus require separate analysis.

Key Points of This Article

The equity valuation of DAT companies was significantly higher than their net asset value in the summer, and has now fallen, currently usually below their underlying asset value.

Bitcoin treasury stocks have significantly retreated from their 2025 highs, performing far worse than Bitcoin itself.

Most Bitcoin treasury companies hold Bitcoin that is currently in an unrealized loss state, and unrealized losses are starting to materialize.

Galaxy Research's prediction in July that 'premium contraction will break this reflexive cycle' has been validated.

The high beta characteristic of DAT stocks relative to BTC amplifies returns during upswings, but during downturns, the premium has collapsed, and issuance has become value-eroding.

1. Analytical Methods

In this article, we use market capitalization rather than the more traditional enterprise value to calculate the equity premium relative to the net asset value (NAV) of Bitcoin. Enterprise value is the standard method for evaluating operating companies, but Bitcoin treasury companies primarily operate as asset-holding tools, with their valuations driven by the Bitcoin exposure per share, rather than cash flow.

Therefore, the market capitalization provides a more direct and economically substantive reference point for comparing equity value with the net asset value of Bitcoin. The premiums or discounts derived from the enterprise value calculation method (commonly used to calculate net asset value multiples, i.e., mNAV) may differ from this.

This analysis focuses on MicroStrategy (MSTR), Metaplanet (3350.T), Semler Scientific (SMLR), and Nakamoto (NAKA), as they each represent different types within the Bitcoin treasury company sector. MicroStrategy is the world's largest corporate holder of Bitcoin, receiving the most market attention and having the longest track record. Metaplanet is the most proactive in accumulating Bitcoin and the most transparent in information disclosure. Semler Scientific entered the layout relatively early and initiated a Bitcoin purchasing plan last year. Nakamoto helps observe how new entrants position themselves in Bitcoin accumulation in the later stages of this cycle.

2. Current Situation

The deleveraging event on October 11 marked a turning point. The forced liquidation of centralized and on-chain perpetual contract positions led to a sharp reduction in open contracts, tightening liquidity conditions in the cryptocurrency market. As risk appetite weakened and the depth of the spot market deteriorated, this wave of deleveraging quickly spread throughout the entire cryptocurrency market. Galaxy Research's analysis of this event can be found in 'A Comprehensive Analysis of the Largest Flash Crash in Crypto History.'

For DATs (Digital Asset Treasury Companies), the feedback loop is directly manifested as:

Bitcoin price decline;

Net asset value per Bitcoin declines;

Equity premium relative to net asset value shrinks;

The ability to achieve value addition through stock issuance weakens.

The previous mechanism that supported companies to issue stocks at prices above net asset value and purchase Bitcoin has now completely reversed. As stock prices fall below net asset value, investors begin to question whether some companies will ultimately need to sell their Bitcoin.

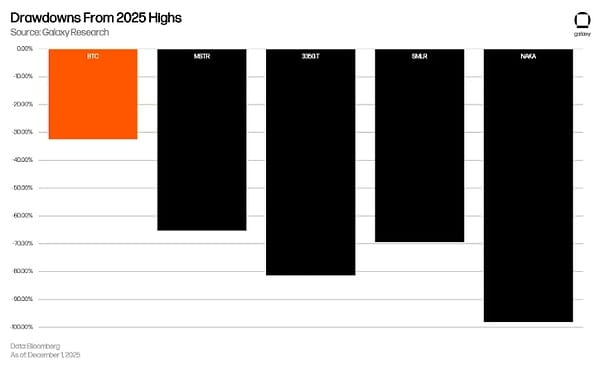

The chart below shows the price pullback magnitude of four Bitcoin treasury companies: MicroStrategy (MSTR), Metaplanet (3350.T), Semler Scientific (SMLR), and Kindly MD, which now trades under the NAKA code after merging with Nakamoto Holdings. The widespread and significant pullback is shocking, with NAKA's price drop exceeding 98%. This price trend is quite similar to the crash scenarios commonly seen in the Meme coin market.

It is also worth noting that the magnitude of these pullbacks is particularly extreme compared to Bitcoin's own decline. Bitcoin has fallen about 30% from its peak. In the volatile cryptocurrency market, such fluctuations are normal. But as Galaxy Research pointed out in the summer, these treasury companies are essentially leveraged investment tools for Bitcoin exposure. When the underlying asset BTC falls by x%, investors should expect that the stock price of Bitcoin treasury companies will fall by x+y%.

DAT stocks essentially combine operational leverage, financial leverage, and issuance leverage. This triple leverage effect can bring excess returns during an uptrend, but it will also result in more severe underperformance during a downturn.

Unrealized profit and loss

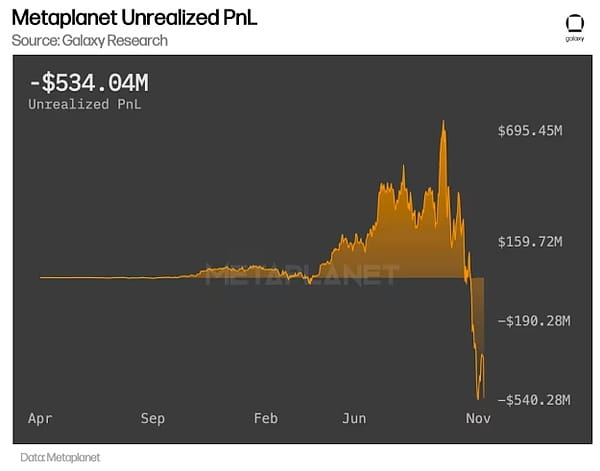

The unrealized profit and loss data on the Metaplanet dashboard clearly illustrates how quickly the situation has changed. The company had over $600 million in unrealized profits at the beginning of October, but as of December 1, it has turned into about $530 million in unrealized losses.

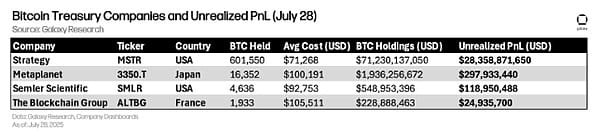

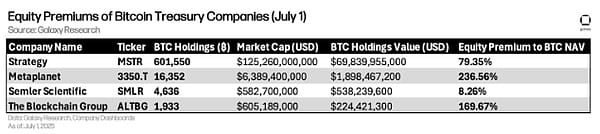

The table below is sourced from Galaxy Research's July 2025 report, showing the unrealized profit and loss situation of Bitcoin treasury companies as of July 28.

When the price of Bitcoin approached $118,000, the unrealized profit and loss status of various companies was good. Now, the trading price of Bitcoin has dropped to about $92,000 (as of the writing of this article), and its average holding cost is no longer optimistic. Both Metaplanet and Nakamoto's average Bitcoin cost exceed $107,000, indicating that their unrealized profit and loss have fallen into significant losses.

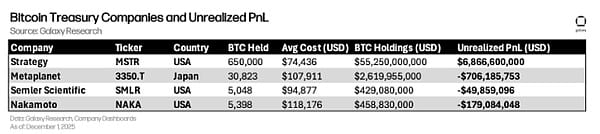

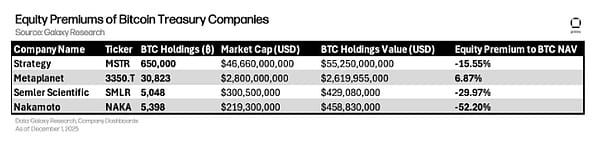

The table below shows the updated unrealized profit and loss data as of December 1. (Note: We replaced ALTBG with the more relevant NAKA.)

This chart is based on a Bitcoin price of $85,000.

Compared to the net asset value of Bitcoin, the equity premium

Since July, the equity premium relative to net asset value (NAV) has significantly shrunk, whereas at that time the premium level was significantly high.

In this section, we calculate the equity premium based on the current market capitalization (number of shares × share price) relative to the net asset value of Bitcoin.

The chart below shows the premium levels of MicroStrategy (MSTR), Metaplanet (3350.T), and Semler Scientific (SMLR) relative to Bitcoin's net asset value since the beginning of 2025. The continuous narrowing of premiums in the three companies clearly indicates that once Bitcoin weakens and risk appetite fades, the issuance premium quickly dissipates.

This chart does not include NAKA, as this company only began accumulating most of its Bitcoin holdings since August, making early data non-comparable to other companies.

The chart below compares the premium level at the time of the July report release, when Metaplanet's stock price was 236% of its net asset value (NAV).

This is the updated chart (we have again replaced ALTBG with NAKA).

3. Where do we go from here

The initial phase of Bitcoin treasury investment seems to have come to an end. This model has not mysteriously failed but has reached the natural boundary conditions pointed out in Galaxy Research's July report. When stock prices trade near or below Bitcoin's net asset value, issuing stocks turns from a growth engine into value erosion. This is the reality currently facing the market.

Looking ahead, based on the health of each company's balance sheet and financing capability, three reasonable scenarios may emerge (and may manifest simultaneously in different companies):

Premiums continue to narrow (baseline scenario)

As long as the cryptocurrency market remains weak, most DATs are likely to trade at par or at a negative premium. In this scenario:

The core indicator to determine whether issuance adds value or dilutes it is—the amount of BTC held per share will stagnate or decline;

Compared to spot BTC, DAT stocks will exhibit a leveraged downside effect, rather than upward momentum.

Investors should not expect the situation of 'stock beta > BTC beta' to reoccur in early 2025 unless risk appetite fully rebounds and BTC reaches new highs.

Selective survival and industry consolidation

This pullback serves as a stress test for balance sheets. The companies with the least flexibility include:

The company that issued the most stocks when premiums were highest;

The company that bought the most Bitcoin at the cycle peak;

Companies that use their Bitcoin holdings as collateral for debt stacking.

Continuous discounts combined with huge unrealized losses are likely to trigger actual solvency and governance pressures. Potential restructuring is expected, and stronger participants (including MicroStrategy) will be in a favorable position to acquire weaker companies at a discount or directly eliminate them based on their financial strength.

In other words, treasury companies are about to enter a phase of survival of the fittest.

MicroStrategy's recent announcement of establishing a cash reserve of $1.44 billion exemplifies this trend. For years, MicroStrategy has relied almost entirely on its Bitcoin reserves and capital market financing to manage liquidity. However, as the issuance environment changes, the company has now built a substantial dollar reserve (raised through immediate equity sales) to cover at least 12 months of dividend and interest payment obligations.

This move marks a significant evolution of the DAT model. The signal that MicroStrategy conveys to the market is that it is prepared to cope with the continued narrowing of premiums and the weak phase of Bitcoin prices. In addition to pure Bitcoin accumulation, liquidity management is increasingly becoming a strategic focus.

Next cycle DAT selection

In principle, the investment model of treasury companies has not vanished. If (or when) Bitcoin eventually reaches new highs, some of these companies are likely to regain moderate equity premiums and restart the issuance flywheel. But the threshold is clearly higher now. Boards and management teams will be judged based on how they respond to this first true stress test: Did they over-issue at price peaks? Did they retain flexible options? How did they handle market downturns? Are their shareholders willing to participate again?

The key is that these companies are no longer simply 'Bitcoin leveraged bullish instruments', but more like path-dependent tools—where their returns highly depend on issuance strategies and timing of entry.

It is worth reiterating a passage from Galaxy Research's July report: 'The DAT company model is vulnerable to shocks from premium collapse, regulatory changes, and capital market turmoil. Companies overly reliant on PIPE financing or excessive leverage may encounter severe pullbacks under adverse market conditions.'