Newton Protocol is trying to solve a problem the market has spent years pretending it can postpone.

Automated systems are getting closer to the point where they can move real money with very little human involvement. They can scan markets, shift positions, compare yields, react to price changes and execute instructions faster than any person sitting behind a screen.

That part is easy to sell.

The harder part is what happens when the system is wrong.

I have watched enough crypto projects build around perfect conditions to know how this usually goes. The demo works. The dashboard looks clean. The agent follows the script. Then the market gets violent, the data arrives late, one permission is too broad, and suddenly everyone discovers that “autonomous” also means nobody stopped it in time.

Newton Protocol is built around that uncomfortable gap.

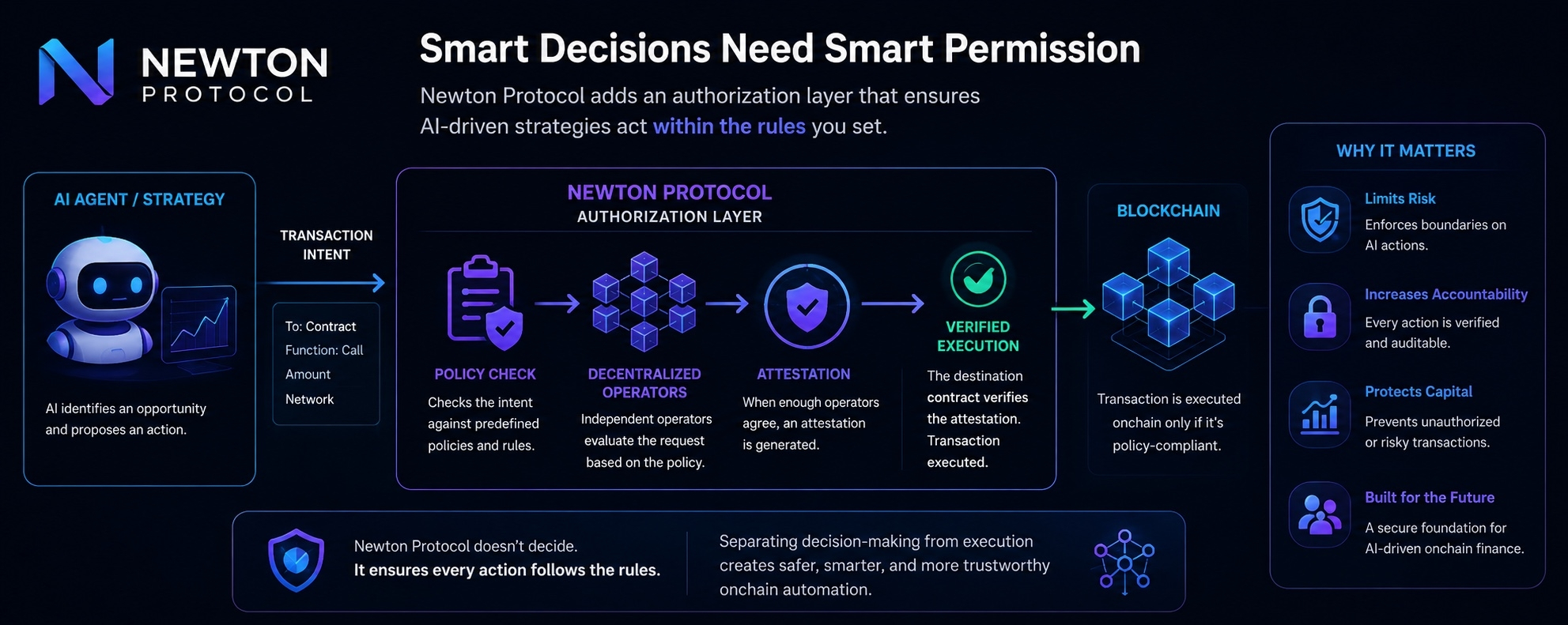

Its role is not to decide whether a trade is smart. It is not there to predict the market, generate the best strategy or turn an average model into a profitable one. The project is trying to control what happens after an automated system decides it wants to act.

That sounds less exciting than AI-powered trading.

Good.

The industry has enough excitement. Most of it gets recycled every cycle anyway.

Newton is attempting to create an authorization layer between a proposed transaction and final execution. An agent can request an action, but the request still has to satisfy a set of rules before the transaction is allowed to move forward.

That distinction matters more than it first appears.

A system may identify a lending opportunity with a high return. It may also fail to notice that the position would push the portfolio beyond its exposure limit. It could interact with a contract that has not been approved, move too much capital at once or make a decision using information that was accurate ten minutes ago and dangerous now.

The model may still think the trade makes sense.

The owner may not.

Newton separates the ability to suggest an action from the authority to execute it. I consider that one of the few sensible ways to approach automated finance. Not because it makes the machine smarter, but because it assumes the machine will eventually do something stupid.

That assumption is realistic.

The rules can be simple. A wallet may not move more than a fixed amount in one transaction. An automated strategy may only interact with approved contracts. A larger transfer may require an extra approval. A position may be blocked when liquidity drops, exposure rises too far or market conditions fall outside an acceptable range.

None of this sounds glamorous. It is mostly limits, checks and friction.

Friction has become a dirty word in crypto because every project wants to promise instant execution and invisible complexity. But when software can move money, some friction is useful. Sometimes the extra step is the only thing standing between a bad instruction and a permanent loss.

The important part is where the restriction sits.

Most automated systems already have rules inside the application. Developers can tell an agent not to spend above a limit or prevent certain actions from appearing in the interface. That works until it does not. Applications get compromised. Instructions are misunderstood. Access controls are configured badly. New transaction paths appear. Someone assumes another part of the system is checking.

This is the grind of real infrastructure. Security rarely fails because nobody wrote a rule. It fails because the rule existed in the wrong place.

Newton wants the policy to become part of the authorization process itself. If the transaction does not meet the required conditions, it should not receive the approval needed for execution.

The agent can still make a bad recommendation. The system simply refuses to turn every bad recommendation into an onchain fact.

I like the logic. I am less interested in the pitch.

Crypto has seen plenty of projects describe themselves as the missing layer between users and risk. Most eventually become another token attached to a thin product, a few integrations and a long list of future use cases. Newton will have to prove it is not recycling that pattern with different language.

Its early focus on managed onchain capital makes more sense than launching with a broad promise to secure everything.

Managed strategies already have rules. They have allocation limits, approved markets, liquidity requirements and risk boundaries. At least, they are supposed to. The problem is that many of those rules live in documents, internal processes or monitoring systems that react after the fact.

A manager may promise not to allocate beyond a certain limit. That is not the same as being technically unable to cross it.

Newton can potentially turn those promises into transaction conditions.

A strategy could be prevented from entering an unapproved market. It could be stopped from increasing exposure beyond a set threshold. It might have to maintain a certain level of liquidity before moving more capital. If conditions deteriorate, the transaction simply does not pass.

That is more useful than another risk dashboard telling everyone what already happened.

Still, this is where I start looking for the moment the design breaks.

A policy is only as good as the person who wrote it. If the rule is badly designed, too broad or based on the wrong assumption, the system can enforce nonsense with perfect consistency.

That is not a minor detail.

People often treat enforcement as if it guarantees safety. It does not. Enforcement guarantees obedience to the rule. Whether the rule deserves to be obeyed is a separate problem.

The same issue appears with data.

A policy may depend on prices, liquidity, wallet behavior, exposure levels or risk information. If those inputs are delayed or wrong, the authorization result can still be wrong. Several operators may agree because they all received the same broken information.

Consensus does not turn bad data into truth.

It only confirms that everyone processed the same noise.

Newton can show that a rule was applied. It cannot guarantee that the rule was wise, that the input was clean or that the market had not already moved by the time the answer arrived.

That does not make the project useless. It just puts it back in the real world, where systems are built from layers of assumptions and someone eventually has to admit which ones still require trust.

The operator structure is supposed to reduce the chance that one party can approve an invalid transaction on its own. Multiple participants evaluate the request, and enough of them must agree before the transaction receives a valid authorization.

Reasonable.

But I am watching the failure modes, not the happy path.

What happens when the operators disagree? What happens when they cannot access the required data? What happens when the system is under load, the market is collapsing and every second matters? A secure design may choose to block the transaction when it cannot confidently approve it.

That protects the funds.

It may also freeze a legitimate action at the worst possible time.

This is the old security-versus-availability argument, except now it sits directly in the path of capital movement. A system that fails open is barely a security system. A system that fails closed can become a bottleneck. The right answer depends on what is being protected, how quickly the transaction must happen and what emergency options remain when the authorization layer is unavailable.

There will not be one clean answer.

That is where the real engineering begins, after the marketing page runs out.

Privacy brings another layer of friction. Transaction policies may involve internal limits, sensitive account information or details that a fund does not want exposed publicly. Some parts of the process can remain away from the public chain, with only the final authorization being recorded.

Fine. But who sees the private information during evaluation? How much do operators need to know? How long is the data retained? Can a user verify the decision without revealing more than necessary?

These questions will matter if Newton wants serious capital rather than experimental usage.

Institutions do not become comfortable because a protocol uses cryptography. They want to know exactly where information moves, who can access it and what happens when something goes wrong. They have spent too long dealing with operational failures to accept vague answers about decentralization.

Newton’s developer marketplace could become useful, although marketplaces in crypto often turn into graveyards of half-maintained tools.

The idea is that developers create reusable policy components. One may handle transaction limits. Another may monitor portfolio exposure. Others could check unusual wallet behavior, risk conditions or compliance requirements.

Applications could combine these pieces instead of building every control from scratch.

That saves time. It also spreads dependency.

A well-designed policy can improve security across many applications. A flawed one can quietly reproduce the same mistake everywhere it is used. The more successful a reusable component becomes, the larger the damage if its assumptions turn out to be wrong.

I would care less about how many policies are listed and more about how many are still maintained six months later.

Who audits them?

Who updates them when market structure changes?

Who notices that a threshold designed during calm conditions no longer makes sense during a liquidity crisis?

This is where most developer ecosystems begin to decay. The launch attracts contributors. The repository grows. Activity looks healthy. Then attention moves elsewhere, dependencies age and users keep relying on tools nobody is properly watching.

Newton will need to fight that slow decline, not just attract builders at the start.

The NEWT token sits underneath the economic design. It is expected to support operator participation, rewards, fees, disputes and governance.

I have read that sentence in one form or another across more projects than I can count.

The words are easy. The demand is harder.

A token can be assigned five utilities and still remain economically unnecessary. The only question that matters is whether real activity forces people to use it. Are applications paying for authorization? Are operators putting meaningful value at risk? Does the token secure something that users actually depend on, or is it present because the protocol needed a token-shaped business model?

The market will eventually answer that without sentiment.

Usage either appears or it does not.

I would watch the amount of capital operating under Newton-enforced rules. I would watch how many evaluations are completed, how often the system blocks transactions and whether those blocked transactions represent genuine risk prevention rather than configuration errors.

The rejection rate may tell us more than raw volume.

Most networks celebrate every processed transaction. Newton should probably care about the ones it refuses. If a strategy attempts to exceed its mandate and the system stops it, that is evidence of a real function. If almost nothing is ever rejected, I would start wondering whether the policies are too weak, the use cases are too limited or the layer is mostly decorative.

There is also the question of cost.

Every extra check adds delay, complexity and operational overhead. Users tolerate that when the protection is obvious. They do not tolerate it when the system feels like another toll booth placed in front of something that already worked.

Newton has to make the friction worth carrying.

That means preventing losses, enforcing mandates and reducing the amount of trust placed in managers or automated systems. Not in theory. In live conditions, with real capital, during the kind of market disorder that exposes every shortcut.

I do not think Newton needs to make autonomous finance safe in some absolute sense. That is too clean a goal for a messy system. It needs to make authority narrower, mistakes less expensive and rules harder to ignore.

There is a market for that. I am fairly sure of it.

I am less sure whether users will accept another layer in the transaction path, whether developers will write policies carefully enough and whether the token economy will become necessary rather than merely available.

The project is aiming at a real problem. That already puts it ahead of much of the noise.

Now it has to survive contact with the thing every crypto design eventually meets: people using it under pressure.