I've spent the past week tracking two regulatory storylines that are converging in a way I haven't seen before. On one side of the Atlantic, the EU is proposing to ban all crypto transactions with Russia-based service providers. On the other, the U.S. CLARITY Act, the most ambitious crypto market structure bill in years, is stuck because Wall Street and crypto firms can't agree on whether stablecoins should pay yield.

Both matter enormously. Together, they're shaping what crypto compliance, exchange operations, and stablecoin economics will look like for years.

The EU's Blanket Ban

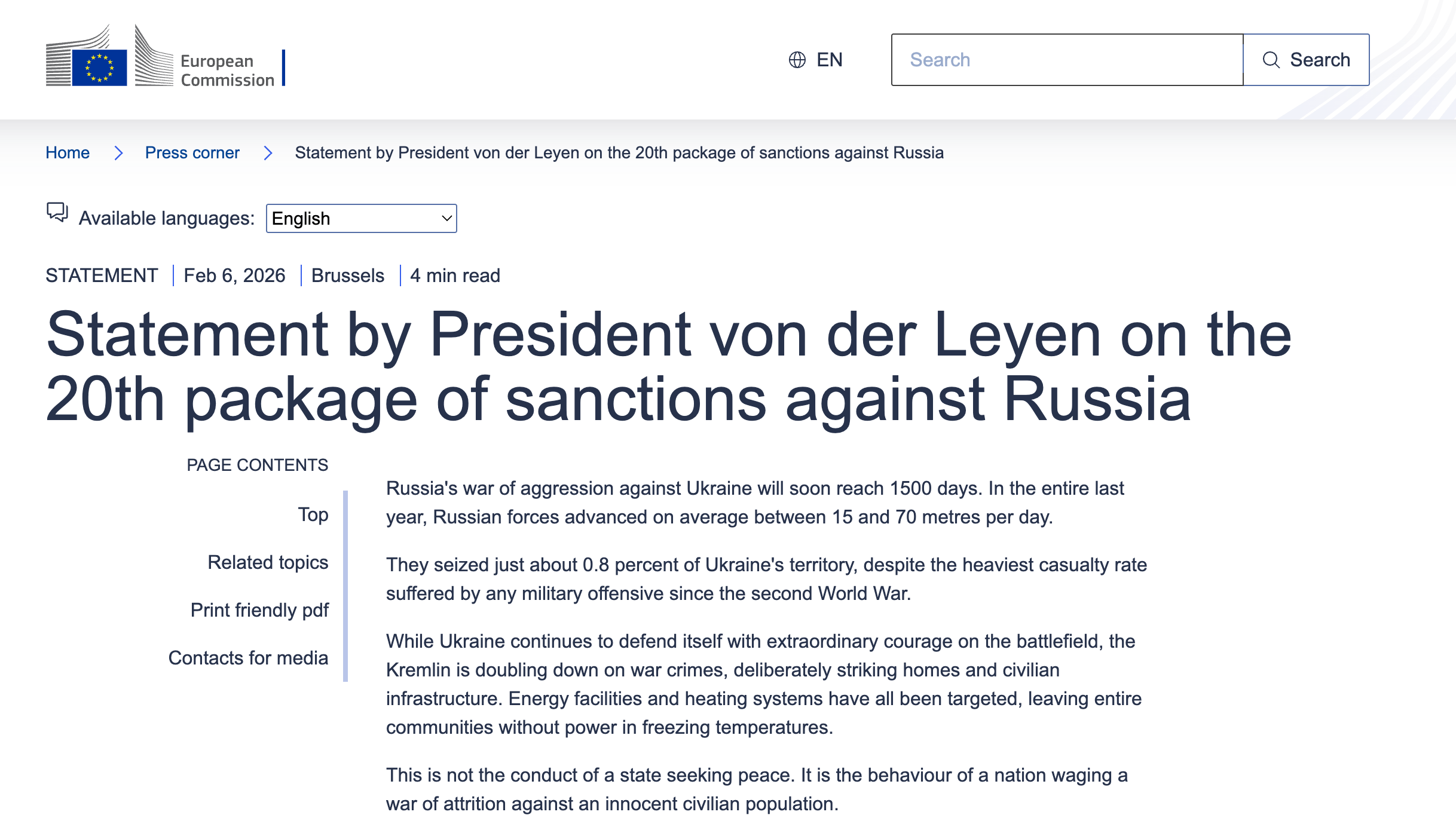

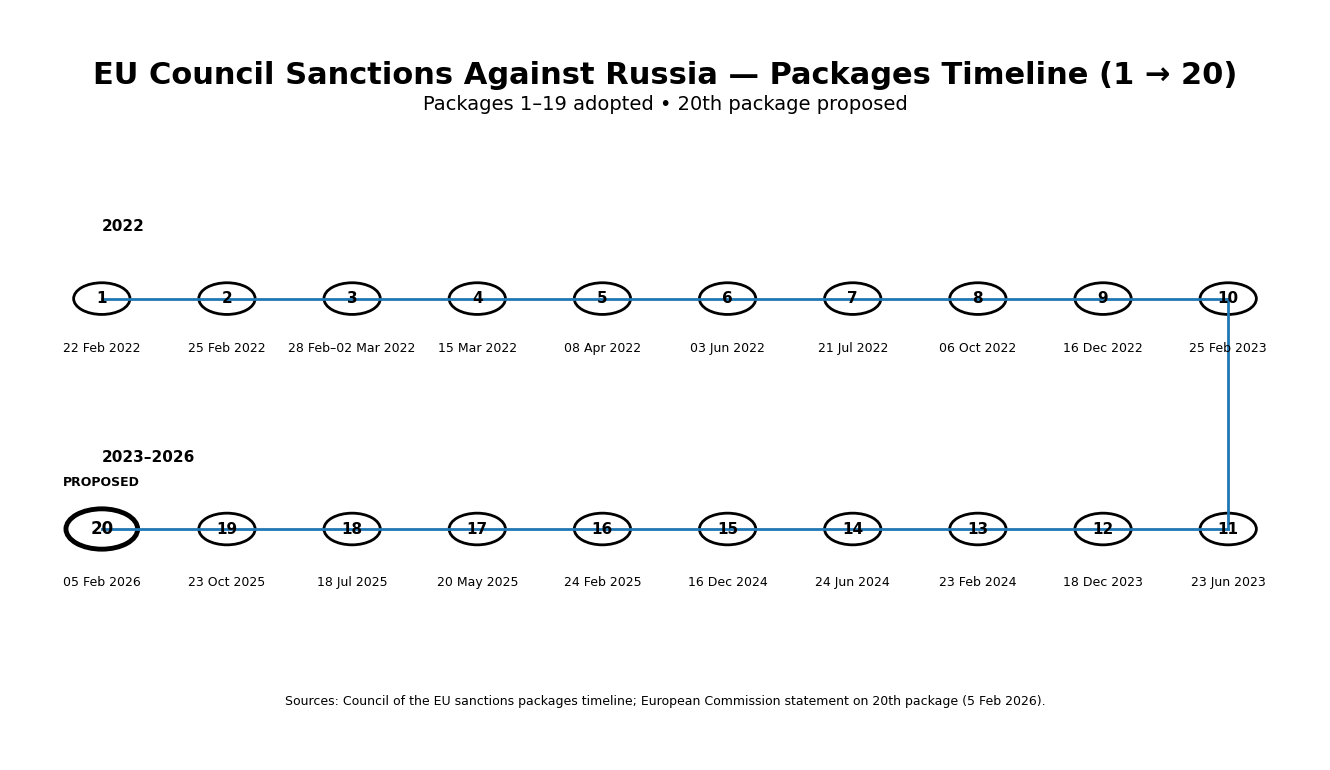

On February 6, Commission President von der Leyen unveiled the 20th sanctions package against Russia. The crypto piece is the sharpest yet: instead of listing individual platforms, a strategy that just spawned replacements like Grinex and the A7 network, Brussels wants to prohibit EU entities from engaging with any crypto service provider established in Russia. The digital ruble is also targeted, as is the A7A5 stablecoin, which processed $100 billion in cumulative volume despite being sanctioned by both the U.S. and EU last year.

I find the rationale compelling. An internal Commission document, widely reported by the Financial Times and Kyiv Post, essentially admits the whack-a-mole approach failed. But enforceability is another question. Analysts I've followed, including Global Ledger's Lex Fisun, point out that sanctioned stablecoin holders can swap into globally traded assets through decentralized liquidity pools, and distinguishing those funds from legitimate activity is, in his words, a technical impossibility. The real burden falls on centralized, MiCA-regulated exchanges and custodians, who now face screening by counterparty jurisdiction rather than just sanctions lists.

Adoption requires unanimity from all 27 member states by the target date of February 24. At least three countries have raised objections. I'm watching that vote closely.

The CLARITY Act and the Yield Fight

In Washington, the picture is different but equally consequential. The CLARITY Act passed the House in mid-2025, but the Senate version has ballooned to 278 pages with over 100 amendments. The markup was postponed in January, and two White House meetings, on February 2 and February 10, ended without a deal.

The core dispute is stablecoin yield. Banks, led by JPMorgan, Goldman, and Citi, circulated a one-page document demanding a total ban on any rewards or incentives for stablecoin holders. Their argument: yield-bearing stablecoins could drain trillions from bank deposits. The crypto side, represented by the Digital Chamber, Coinbase, and Ripple, countered on February 13 with a compromise, concede on passive idle yield but preserve rewards tied to liquidity provision and ecosystem participation.

Treasury Secretary Bessent weighed in on CNBC the same day, urging Congress to pass the bill this spring and warning the bipartisan coalition could collapse before November's midterms. I take that timeline seriously. If this slips past August recess, the legislative window effectively closes.

What I'm Watching

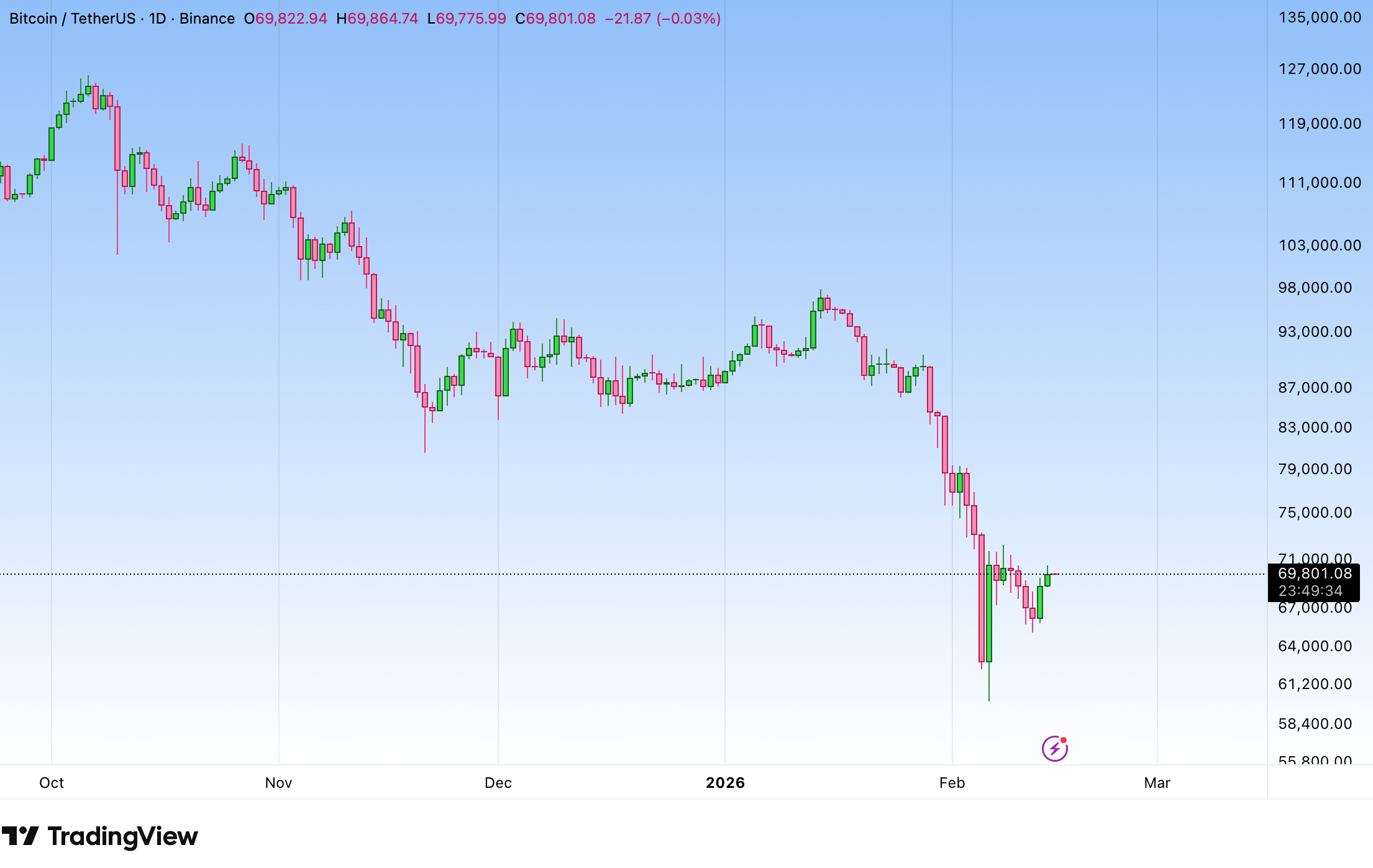

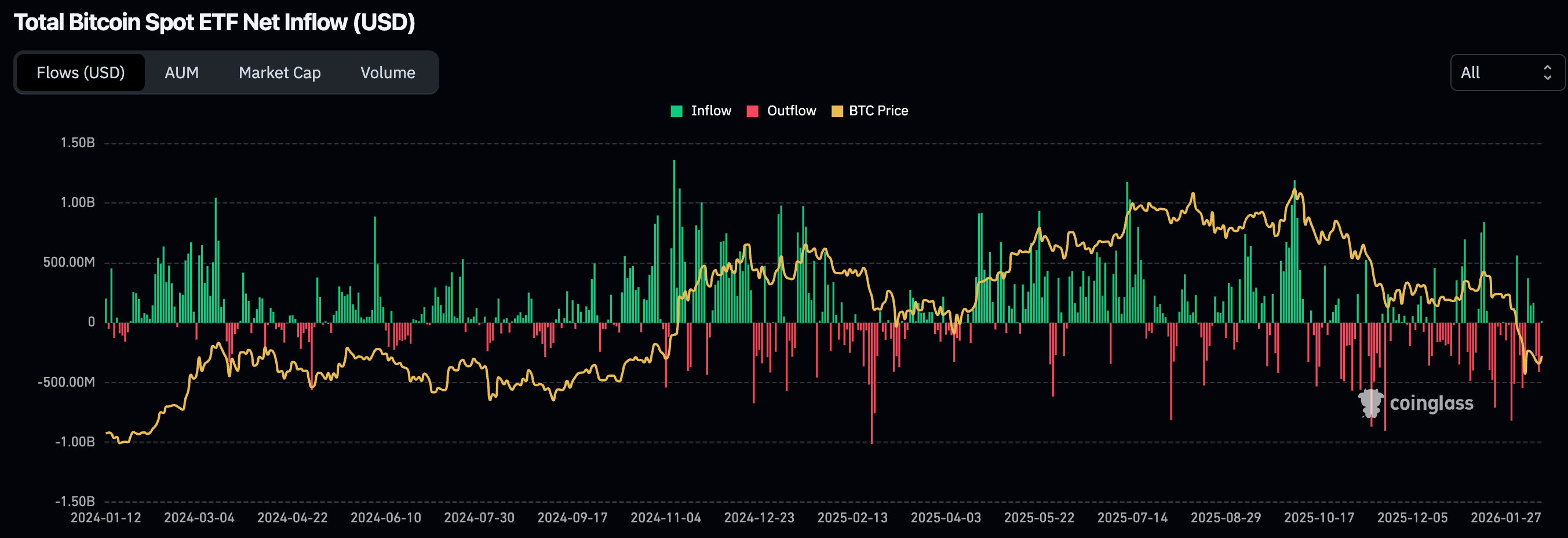

The ETF picture adds context. Spot BTC ETFs have posted four straight weeks of net outflows, with roughly $360 million leaving in the week ending February 14. BTC is trading around $67,000, down 25% year-to-date and nearly 50% from its October high. Yet total BTC held in ETFs has only dipped about 7%, suggesting core holders remain. The market is stressed but not structurally broken.

For me, the next ten days are critical. The EU unanimity vote, the White House's end-of-February deadline for compromise language, and whether Senate Banking schedules a markup will determine whether these two regulatory tracks advance or stall. I don't have predictions, but I do think the outcomes will set the template for how the West regulates crypto going forward.