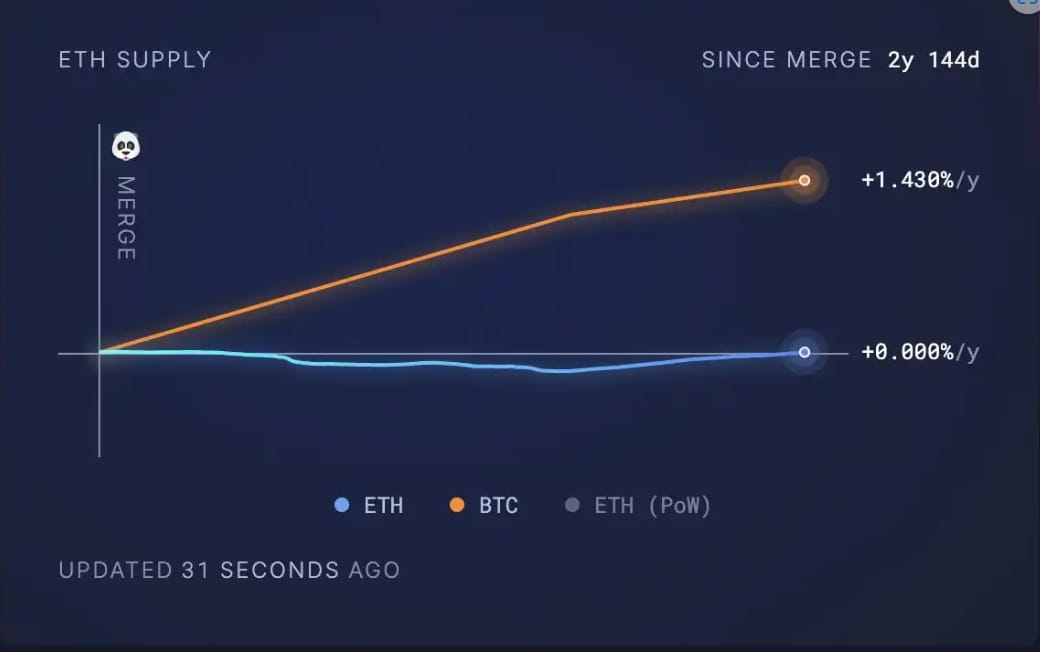

Author: Justin Drake, Ethereum Foundation researcher. Original text compiled by: Felix, PANews. The current ETH supply is growing at 0.5% per year. This is 1% of the issuance minus 0.5% of the destruction each year. To achieve excess returns again, either the issuance needs to decrease or the destruction needs to increase. Personally, I believe both will occur. ETH vs BTC

Before delving into Ethereum's issuance and destruction, let's briefly introduce ETH and BTC. The internet-native currency is a huge opportunity, valued at trillions of dollars. Currency premiums rarely accumulate on a large scale. You need a truly attractive asset with outstanding properties for societal coordination. At first glance, currency is a zero-sum game. In the internet age, gold is ready to be demonetized. Only two candidate currencies can replace it and win the internet currency battle—BTC and ETH. No other currency can compete. I believe the decisive factors are credible neutrality, security, and scarcity. Since Ethereum's merge, ETH has become scarcer than BTC. Notably, BTC's supply has increased by 666,000, valued at $66 billion, while ETH's supply has remained stable. Today, BTC's supply grows by 0.83% annually, which is 66% faster than ETH. For those looking to the future, ETH's supply will decrease again. Scarcity is important, but ultimately, the internet currency battle may be resolved by security. Ironically, the famous cap of 21 million BTC is the culprit. BTC's issuance will drop to zero—this is Bitcoin's strongest social contract. After several halvings, the issuance will become insignificant. Here is a data point: over the past 7 days, only 1% of miners' income came from Bitcoin transaction fees, while 99% came from Bitcoin issuance. Despite undergoing 4 halvings, the issuance has decreased 16 times, yet people have spent 15 years searching for Bitcoin's transactional utility, and the situation remains the same. I believe the Bitcoin blockchain is outdated. To sustainably carry out a 51% attack on Bitcoin, it would require about $10 billion and 10GW of power. For nation-states, this cost is trivial. Regarding power, Texas can produce 80GW. The security ratio of BTC is 200 to 1, which is a $2 trillion asset backed by $10 billion in economic security. Any shortable instruments related to BTC mining would incentivize a 51% attack. Bitcoin mining stocks worth $20 billion—these stocks would immediately create a 'nuclear explosion'. BTC's open contracts total $40 billion—direct short exposure. Not to mention the potential short exposure generated through $100 billion in ETFs and $100 billion in MSTR.

Scarcity is important, but ultimately, the internet currency battle may be resolved by security. Ironically, the famous cap of 21 million BTC is the culprit. BTC's issuance will drop to zero—this is Bitcoin's strongest social contract. After several halvings, the issuance will become insignificant. Here is a data point: over the past 7 days, only 1% of miners' income came from Bitcoin transaction fees, while 99% came from Bitcoin issuance. Despite undergoing 4 halvings, the issuance has decreased 16 times, yet people have spent 15 years searching for Bitcoin's transactional utility, and the situation remains the same. I believe the Bitcoin blockchain is outdated. To sustainably carry out a 51% attack on Bitcoin, it would require about $10 billion and 10GW of power. For nation-states, this cost is trivial. Regarding power, Texas can produce 80GW. The security ratio of BTC is 200 to 1, which is a $2 trillion asset backed by $10 billion in economic security. Any shortable instruments related to BTC mining would incentivize a 51% attack. Bitcoin mining stocks worth $20 billion—these stocks would immediately create a 'nuclear explosion'. BTC's open contracts total $40 billion—direct short exposure. Not to mention the potential short exposure generated through $100 billion in ETFs and $100 billion in MSTR.

Can Bitcoin somehow self-repair before it's too late? Bitcoin is a manifestation of blockchain rigidity. Can it have a 1% tail issuance per year? Maybe Bitcoin can switch to PoS and rely on minimal fees? PoS is blasphemy. Perhaps Bitcoin can switch to another PoW algorithm? No, that nuclear option is futile. Maybe Bitcoin can have large blocks and sell data availability on a large scale? Well, a holy war once broke out over small blocks. If you've read this far and understand the above, congratulations. Even today, few realize the long-term implications of Bitcoin PoW and its impact on BTC assets. This is an opportunity for early execution, but it requires patience. The timeframe is not 1 month, or even 1 year—but 10 years. Speaking of long-term frameworks, Lummis's proposal to lock BTC for 20 years seems a bit crazy—by then, Bitcoin will be obsolete. Worse, if the U.S. holds trillions of BTC, it would directly incentivize America's enemies to launch a 51% attack. Contrary to popular belief, Bitcoin has no resistance against nation-states—countries like Russia can easily launch a 51% attack.

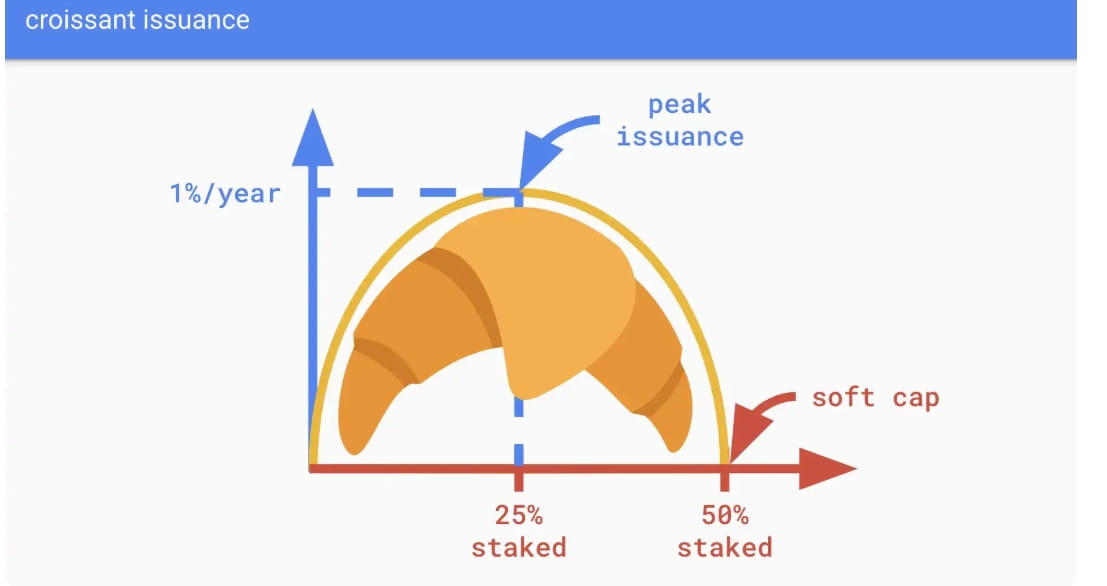

Back to ETH. The current issuance curve is a trap. Unfortunately, just like Bitcoin's issuance, Ethereum's issuance design is also flawed. It guarantees a 2% tail APR even if 100% of ETH is staked. Since staking costs are far below 2%, every rational ETH holder is incentivized to stake. When most ETH is staked, losses will occur: → ETH substitution: Liquid staking tokens like stETH and cbETH replace original ETH as collateral. This injects systemic risks into DeFi (custodial risk, slashing risk, governance risk, smart contract risk). This substitution also undermines ETH's role as a unit of account and triggers further repercussions on currency premiums. → Actual profits and tax rates: Actual profits, which are earnings adjusted for supply growth, decrease as ETH staking increases. When 100% of ETH is staked, all ETH holders are equally diluted. Worse, income tax is levied based on nominal gains. If no stakers enjoy positive real profits while all ETH holders bear billions of dollars in selling pressure each year, it would be a tragedy. I believe the issuance curve should be driven by competition among stakers to discover a fair issuance rate—not arbitrarily setting a lower limit of 2%. This means that as ETH staking increases, the issuance curve must ultimately decline and return to zero. My personal recommendation is 'Croissant Issuance'.

'Croissant Issuance' is a simple semi-oval with two parameters: → Soft cap: The staking ratio when issuance goes to zero. A 50% staking soft cap feels credible, neutral, and pragmatic. → Peak issuance: The theoretical maximum issuance that ETH holders bear. An arbitrary integer (e.g., 1% per year) would suffice, as the ultimate interest rate will be determined by the market. Ethereum Foundation researchers have been studying issuance for years—personally, I believe the current curve is broken and needs change, which is a rough consensus. Guiding the social layer to change issuance is not easy. For champions, this is an opportunity to address this situation and coordinate changes to the mainnet in the coming years.

I believe that a sustainable way to destroy a large amount of ETH is to expand data availability. Having 10 million TPS with a transaction fee of $0.001 is more profitable than having 100 TPS with a transaction fee of $100. I wouldn't be surprised if we see hundreds of ETH blobs destroyed daily this year, and then this destruction might suddenly plummet again due to peer data availability (DAS) in the Fusaka fork. Yes, the blobs introduced by EIP-4844 somewhat reduce the total destruction amount, which is a natural phenomenon of supply and demand. When the demand for DA catches up with supply, blobs are expected to be destroyed in large numbers. In a few months, the Pectra hard fork will double the number of blobs. The short-term goal is growth, and significant growth is expected.

In the coming years, the supply and demand will continuously play a game of cat and mouse until the full Danksharding deployment is completed. If we see hundreds of ETH blobs destroyed daily this year, and then this destruction suddenly collapses again due to peer DAS in the Fusaka fork, I would not be surprised. Looking to the future, this is about building infrastructure for the coming decades and centuries. The fundamentals will become apparent in the coming years. Whether it's Bitcoin security, ETH issuance, or ETH destruction, patience and confidence are essential.

Article

EF Researcher: The Current ETH Issuance Curve is a Trap and Should Adopt the 'Croissant Issuance' Model

--