Original | Odaily Planet Daily

Author | Nanzhi

The wave of migration to the chain

During the 2022 bear market, DeFi protocols led by GMX brought the "Real Yield" narrative to the market, providing a sustainable, stable, and high-capacity way to earn income. After the FTX crash, the importance of decentralization and transparency has received more and more attention. Perpetual contract derivatives exchanges (Perp DEX) have occupied an increasing market share, and the corresponding protocol revenue and user revenue have also expanded. The trend of migration from CeFi to DeFi has become unstoppable.

Among Perp DEX, GMX occupies a significant leading position. In the past year, GMX protocol revenue was US$132 million, ranking ninth among all projects and ranking first in the derivatives DEX track.

GMX Ecosystem

GMX is a DeFi protocol on Arbitrum that allows liquidity providers (LPs) to deposit funds and provide leverage to perpetual contract traders, who then conduct on-chain transactions using the funds they provide.

Traders: In GMX V1, traders need to pay transaction fees and lending fees, while V2 adds funding rates and price impact fees.

Liquidity Provider (LP): Compared to traders, the other party participating in the agreement is called a liquidity provider. LP invests a series of tokens to provide liquidity for traders and earns income from their transaction fees. The liquidity it provides is GLP in V1 and GM tokens in V2.

Simply put, for the expected value of a trader's profit and loss (EV), assuming that the profit and loss and the winning rate are both 50-50, the average EV of the trader's profit and loss is zero. If the handling fee is taken into account, the EV of the trader's counterparty in the zero-sum game is positive. Although some traders can make a lot of profit, after expanding the scope to all traders, the ones who can really make continuous profits are still their counterparties - liquidity providers.

GLP, the “Money Printing Machine” that Crosses Bull and Bear Markets

GLP is a product consisting of a basket of tokens, including non-stablecoins such as ETH and BTC, accounting for about 60%, and stablecoins including USDC, USDT, etc., accounting for 40%.

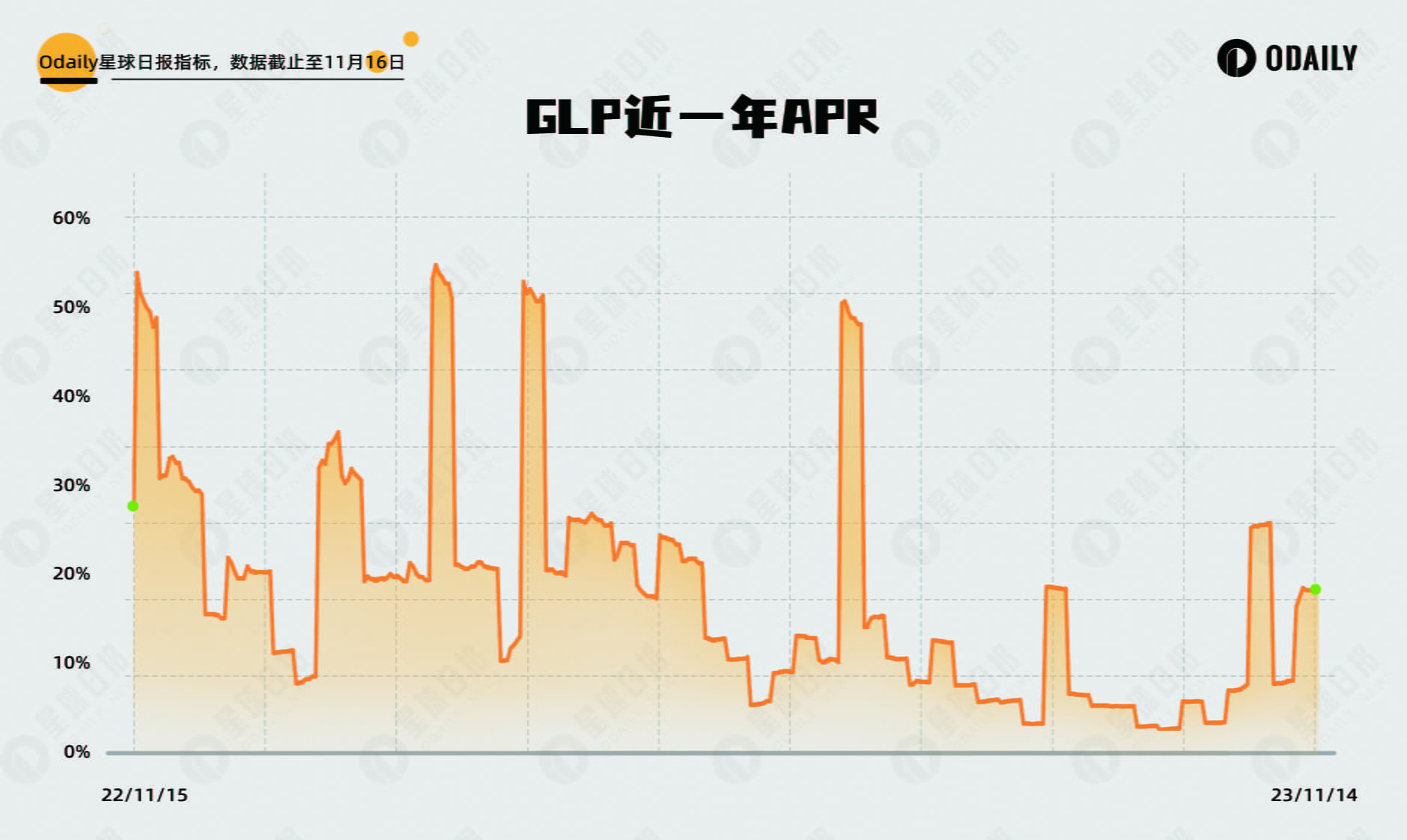

Continuous income: GLP's APR data for the past year is shown in the figure below. Even during the bear market, it continues to generate cash flow income for GLP holders. Its average annualized APR is 18%. Whether compared with the 4.6% of the 10-year US Treasury bond or the 4% of the ETH POS pledge income, the income from GLP is relatively considerable and stable.

Stable underlying assets: As mentioned above, stable currency assets account for 40% of GLP, while among non-stable assets, BTC accounts for 30% and ETH accounts for 26.8%, forming a stable underlying asset portfolio. The price of the past year is shown in the figure below. On the one hand, the overall asset trend is upward without a significant retracement. On the other hand, as it is heading towards a bull market, BTC, as the pioneer of the bull market, has the possibility of continuing to rise.

However, GLP will face counterparty risk caused by the imbalance of open interest (OI) and the problem of too few trading products. GMX launched the V2 version in August this year, using GM tokens as a liquidity pool to achieve independent risk control and expand trading assets. For LP, they can also choose risk exposure based on risk preference/return expectations.

Vaultka Product Matrix

After GMX opened up a simple and stable profit model for the market, a series of GMX-based Perp DEX competitors have emerged in the market, including well-known protocols such as Gains Network, MUX Protocol, HMX, etc. Faced with a variety of similar products, investors have generated many demands, including compounding and improving GMX's returns, and further control of its stability. Vaultka came into being. Through comprehensive horizontal expansion and deep vertical division, it has created a comprehensive and rich derivative strategy matrix for Perp DEX. Its TVL increased by 3 times last month to more than 10 million US dollars:

Horizontal system: covers Arbitrum’s popular Perp DEX protocol, and will soon launch index products to meet investors’ needs for protocols with different characteristics.

Vertical system: Provide a series of products with different risk preferences, and further segment investors under each product to meet multi-level risk preference needs.

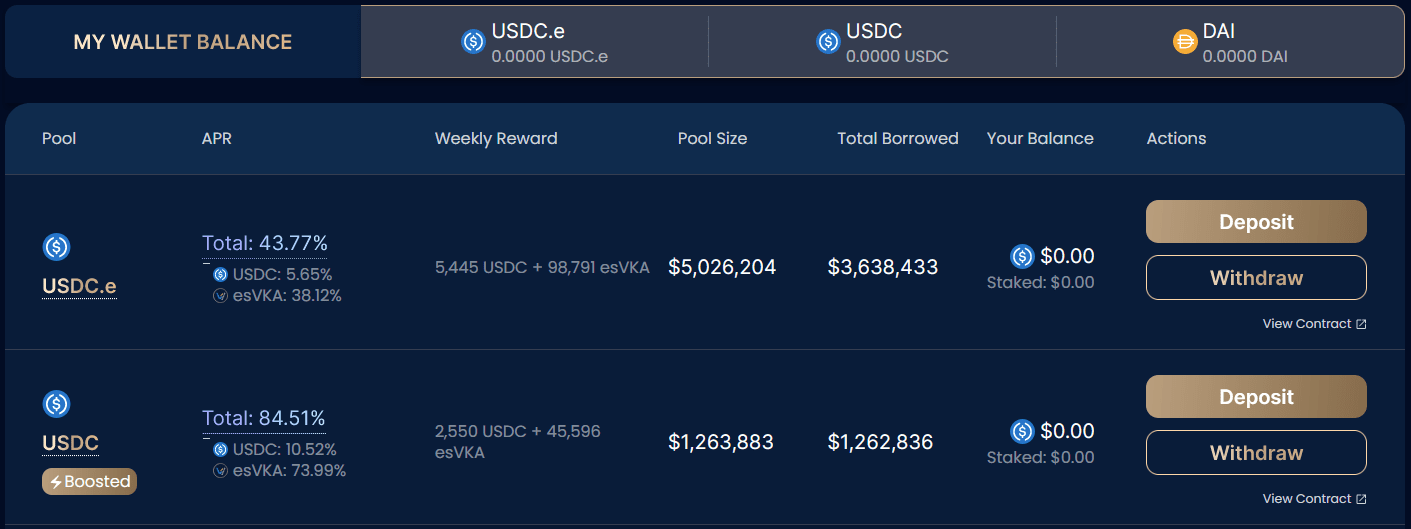

GLP/GM Strategy Vault

As mentioned above, liquidity providers will continue to profit from traders' transactions, with the average APR of representative GLP reaching 18% over the past year, while the maximum drawdown of GLP is approximately 7%.

Leverage Strategy

When the bull and bear markets switch, users hope to improve the profitability of their underlying assets. At the same time, with the Federal Reserve's cessation of interest rate hikes and expectations of rate cuts, expectations for rising risk assets increase, and investors' requirements for risk interest rates will further increase.

Vaultka's GLP/GM leverage strategy meets the needs of investors:

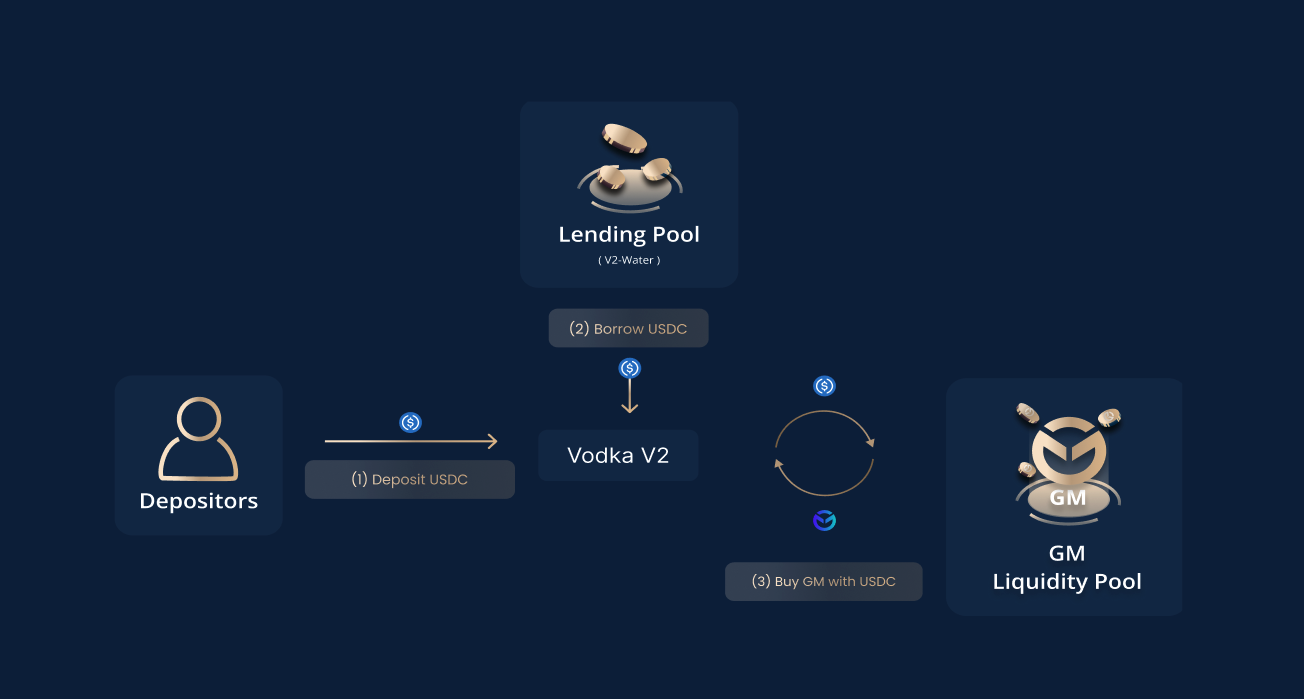

Users can use stablecoins such as USDC and USDT as investment capital. The protocol will lend assets from the Lending module based on the leverage selected by the user, and then mint GLP or GM. The protocol will regularly collect the income share of GLP/GM for Vaultka users to collect at any time.

Vaultka's Lending module adopts a revenue-sharing model. Users do not pay floating loan interest rates but share the underlying protocol revenue in proportion, achieving a win-win situation for both borrowers and lenders. It also designs an isolated lending pool to ensure the safety of lenders' funds.

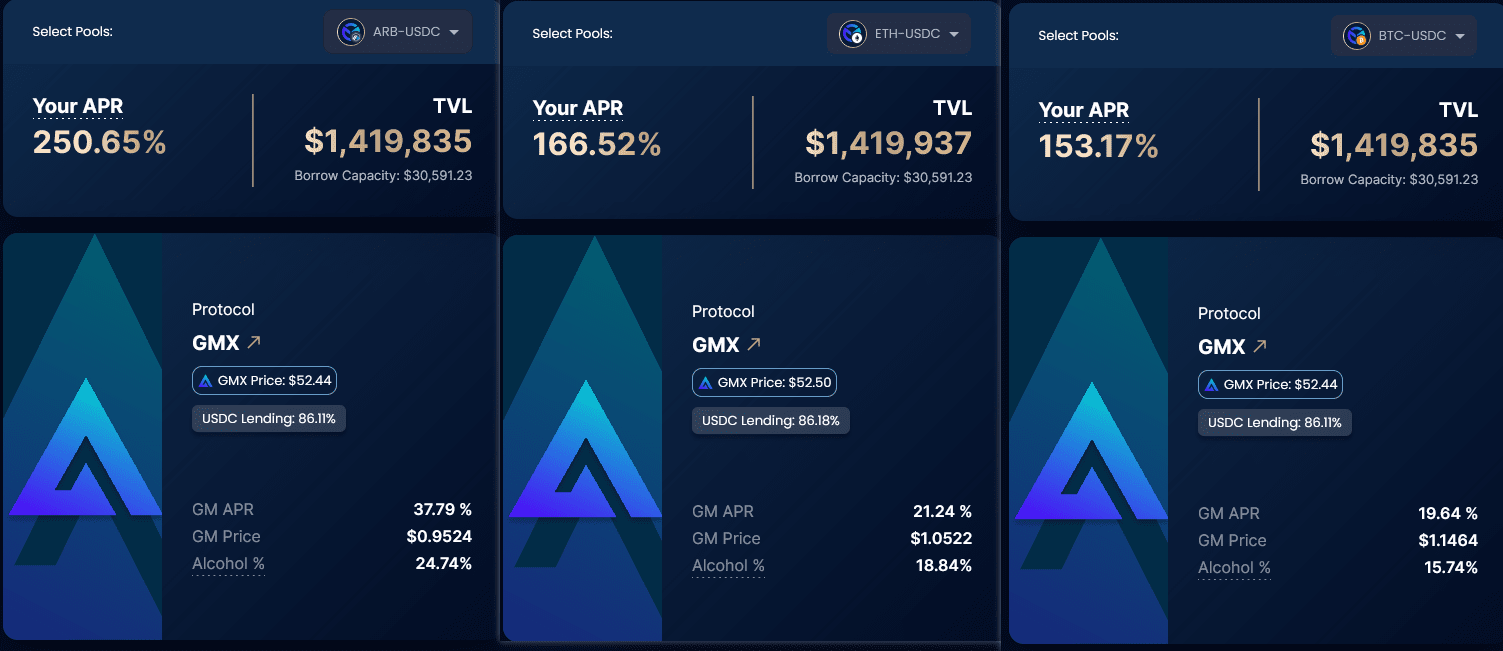

The user's rate of return is directly related to the leverage multiple. As of November 14, data from Vaultka's official website showed that under a 10x multiplier, the APRs of the three GM pools, ARB, ETH, and BTC, were 250%, 166%, and 153%, respectively, while the corresponding APR of GLP also reached 108%.

Judging from the GLP price review data over the past year, the leverage multiples provided by Vaultka have a certain safety margin. Investors can choose the multiples based on their expectations for the future market and risk preferences to meet risk-rate requirements and help improve both underlying assets and yields.

Market Neutral Strategy

As part of its vertical product system, Vaultka also provides investors with market neutral strategies, uses leveraged funds to hedge risks, and provides investment channels for conservative investors.

As mentioned above, GLP/GM are both composed of non-stable currencies, which is the first layer of "underlying asset volatility risk" faced by users. On the other hand, as the counterparty of the trader, users will also face "counterparty risk" brought about by unbalanced open positions (OI).

In response to this, Vaultka provides a hedging-based GLP neutral strategy, which hedges by shorting BTC and ETH according to the corresponding weights in GLP through reputable lending protocols. Vaultka determines the dynamic rebalancing point based on the long/short positions of GMX traders through continuous backtesting and simulation to further stabilize the equity value of the product and meet the needs of low-risk investment.

In addition, Vaultka recently disclosed the GM leverage neutral strategy for ETH and ARB, which eliminates the "underlying asset volatility risk" through a leveraged borrowing dual-currency + hedging combination structure. Regardless of how the prices of ETH and ARB change, it does not affect the value of the investment portfolio. Under a robust structure, users' profitability is continuously amplified.

Lending Module-Profit Sharing

In other leveraged strategy protocols, users often have a pain point - the borrowing interest rate fluctuates greatly and is difficult to predict, causing leverage to fail frequently:

Such agreements usually adopt a bi-curve interest rate model, where the interest rate rises at a low rate before the loan utilization rate (UR) critical point, and then rises sharply after breaking through the critical point.

In the case of GLP/GM’s “APR>Loan Rate”, users will usually continue to increase leverage, causing UR to rise rapidly, thereby increasing “APR

The above situation makes leverage unprofitable, and users begin to reduce leverage. After the data reverses, they start to leverage again, and this process continues to cycle according to the APR of GLP. The returns fluctuate repeatedly and are difficult to predict.

In response to this, Vaultka has designed a profit-sharing model in the Lending module to solve this problem. Strategy vault users pay lenders not a floating interest rate, but a bi-fold profit-sharing. There will be no fluctuation in lending rates at the APR critical point, so that the leverage of the strategy vault is profitable under all URs, releasing the potential of leveraged investment.

On the other hand, the parameters of this model have been pre-set and are positively correlated with the user's leverage multiple. Users can calculate the leverage cost they need to pay more clearly, which reduces the cost of the game and helps to clarify the cost considerations under different risk preferences.

In summary, the Lending module designed by Vaultka allows GLP/GM leveraged investors to focus only on the investment targets and strategies themselves, and assists in the decision-making, use and profitability of leverage strategies.

So far, Vaultka has created four strategy products vertically to fully meet the needs of users in segmented markets: ① Risk aversion - Lending lenders, ② Risk-free preference - GLP neutral strategy, ③ Low-risk investment - leverage neutral strategy, ④ Free choice - leverage strategy.

Other Strategies Vault

Horizontally, Vaultka also covers multiple Arbitrum popular protocols, providing users with optional leverage strategies:

HLP: HLP is the liquidity provider of HMX. After users deposit their assets into GMX to mint GLP, they deposit GLP into HMX as a liquidity provider and enjoy the dual transaction fee income of GMX and HMX. HLP has similar characteristics to GLP, with continuous profitability and low drawdown. Its price is shown in the figure below.

VLP: VLP is the liquidity provider of Vela Exchange and can only be minted through USDC. It can be considered a Delta-neutral product. Due to its single-asset characteristics, the liquidation scenario is controllable and the risk-bearing capacity is easy to predict.

gDAI: gDAI is the liquidity provider of Gains Network. Users use DAI as collateral on the platform and then mint gDAI. gDAI has the characteristic of eternal appreciation and is also a neutral product.

The above-mentioned multiple strategy products have different asset characteristics and yields. By fully covering and linking the Vaultka Lending module, users can freely choose according to their individual investment needs.

Lending module detailed explanation

In its lending module, Vaultka adopts a revenue sharing model and a revenue prepayment model. The former enables lenders to increase their capital returns based on market conditions, while the latter ensures the stability and predictability of returns.

Revenue Sharing Model

As mentioned earlier, the revenue sharing model solves the problem of leverage effectiveness for borrowers, and for lenders, this model also brings many advantages:

Income scalability: Under this model, the higher the leverage used by the borrower, the higher the share rate (30% for 2x leverage, 37.5% for 5x leverage, and linear increase in the middle), and the higher the actual capital efficiency and yield of the lender. And the increase in the APR of the underlying protocol will also be fed back to the lender's income.

Trading volume under the expectation of market rising will lead to an increase in APR and an increase in borrower confidence, further promoting an increase in leverage amount and leverage ratio, thereby achieving a triple increase in returns.

Zero lending interest: Borrowers enjoy zero lending interest, and reward sharing will only be triggered when closing a position generates positive returns.

Asset security: Lenders’ positions are protected with no downside risk, and losses will be borne by reserve and leverage users.

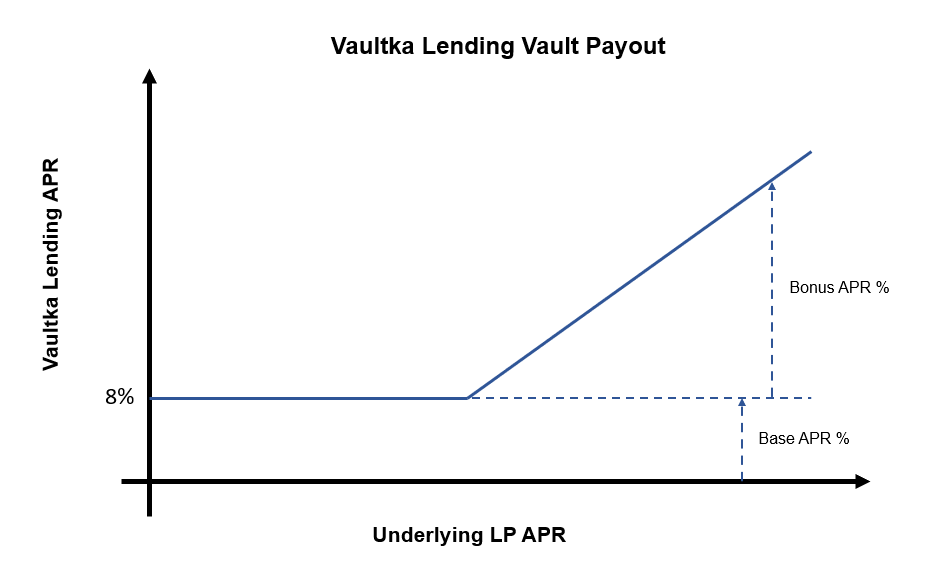

Revenue Prepayment Model

Vaultka divides the lender's income into a base reward (Base Reward) and an additional reward (Bonus Reward). The base reward is calculated from the total income of the previous quarter, and the additional reward is calculated by adjusting the total income of the previous week.

The model ensures that lenders can predict future returns with certainty, and that the rewards received by lenders will never fall below the specified expected amount, but will only increase.

In addition to the above features, Vaultka provides unique Lending vaults tailored for each specific strategic vault, effectively isolating and managing the risks associated with each individual vault. It also allocates esVKA rewards to lenders, allowing them to develop and gain benefits together with the platform.

Token Economics

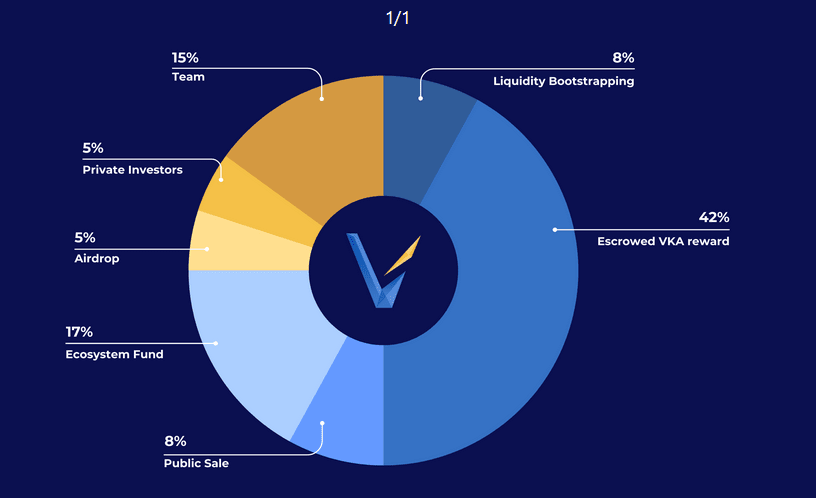

On October 19, the Vaultka platform token $VKA TGE was completed, raising 2,583 ETH, which is 7.9 times the initial target.

The total number of VKA tokens is 100 million, of which 13% are for private and public sales, 5% for airdrops, 15% for the team, and the remaining 67% are used for various ecological development purposes. The distribution details are as follows:

Token Use Cases

The VKA token has multiple use cases, including:

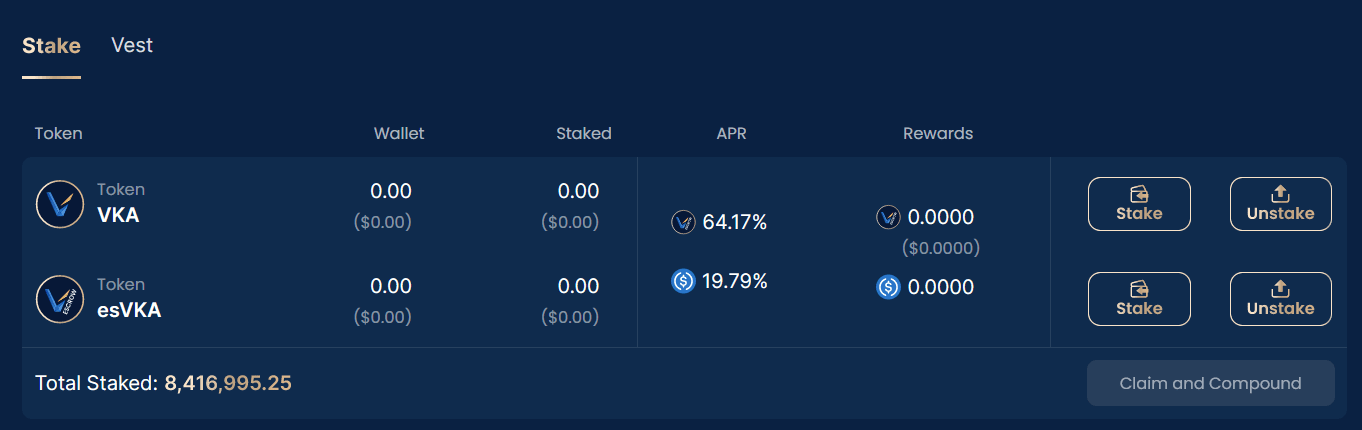

Reward boost: Staking VKA can earn 2.5 times the reward of esVKA released. The boost reward each user receives will be based on the weighted ratio of their deposit to the total liquidity weight of the pool, and the total amount of esVKA issued to the Vault.

Protocol Fee Sharing: By staking VKA or esVKA, stakers receive 60% of protocol revenue, including a 15% strategic Vault management fee and a 0.2% withdrawal fee. esVELA and esHMX will also be distributed as fees. esToken will be vested and collected by Vaultka from the underlying protocol every two weeks. In addition, stakers are eligible for additional allocations of esVKA.

Revenue Voting Rights: Weekly VKA stakers can also participate in Vault emission distribution and obtain bribery fees from the protocol.

In addition, Vaultka will repurchase and destroy VKA through protocol revenue, and the reduced portion of esVKA released in advance will also be destroyed.

esVKA

As shown in the token economics, 42% of the tokens will be emitted in the form of esVKA. esVKA staking enjoys the same benefits as VKA staking, including 2.5 times the release reward, protocol fee sharing, revenue voting rights, etc. Users can also choose to convert their esVKA to VKA, which is divided into 1 year of full release or 90 days of early release (the amount is reduced by 50%)

The bull market is coming, it’s time to snowball

Vaultka's product matrix is still developing. In subsequent planning, Vaultka will further expand its system, launch the Cocktail series (comprehensive investment in LP and governance tokens), and incorporate more protocols and tokens to provide investors with comprehensive, easy-to-decision and easy-to-operate products.

Compared with traditional derivatives markets, the trading volume of the Perp DEX market is still small. As its official statement said, Vaultka firmly believes in the potential of the Perp DEX market and will actively participate in and promote the growth of this rapidly expanding market. With its comprehensive and in-depth product system, it will roll a continuous cash flow snowball on the long slope of Perp DEX.