The slow-motion collapse of the world's largest asset class is accelerating. New data confirms that China's property downturn has shifted from a correction to a structural crisis that rivals the severity of the 2008 crash. With prices falling across the vast majority of cities and sales volume evaporating, the Chinese housing market is now approaching its 6th consecutive year of decline, leaving policymakers scrambling and investors trapped.

❍ Prices Fall in 62 of 70 Cities

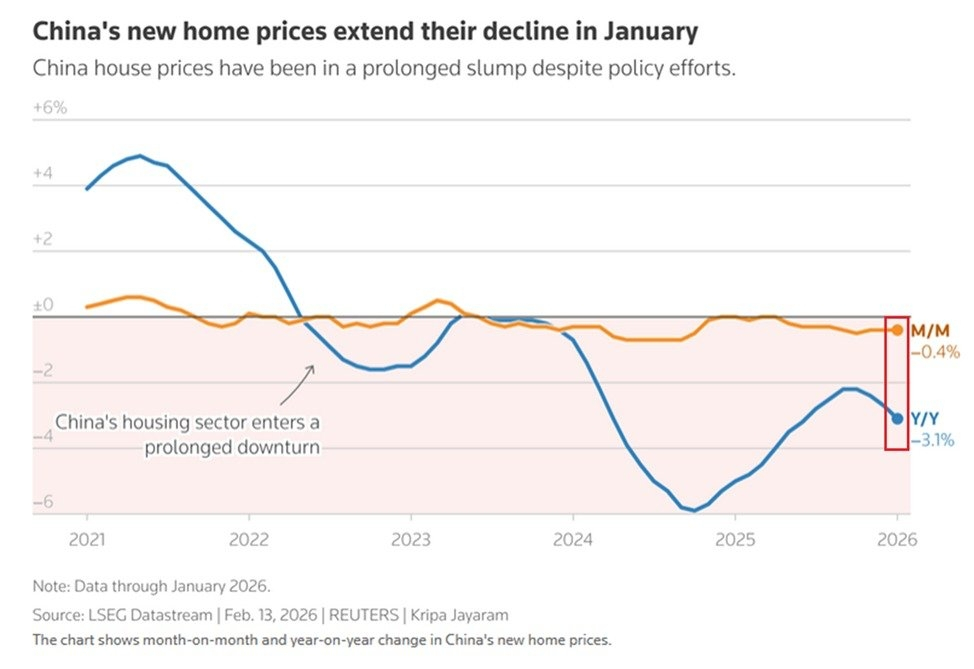

The latest data from the National Bureau of Statistics paints a picture of a broad-based capitulation.

-3.1% YoY: New home prices fell -3.1% year-over-year in January, marking the steepest annual decline in 7 months.

Widespread Pain: The damage is not localized. Of the 70 major cities surveyed, 62 posted price declines, up from 58 in December.

Historic Streak: This extends a brutal trend where home prices have now fallen in 43 of the last 46 months, the worst streak on record.

❍ Tier-One Cities Lead the Resale Crash

While new home prices are managed somewhat by government price floors, the resale market—which reflects true supply and demand—is free-falling.

-7.6% Plunge: In China's tier-one economic hubs (Beijing, Shanghai, Shenzhen, Guangzhou), resale home prices plunged -7.6% year-over-year.

Smaller Cities: The situation is equally dire in smaller cities, where resale prices dropped by over -6.0%.

❍ 2026 Outlook: Another Double-Digit Drop

Forward-looking indicators suggest the bleeding will continue throughout 2026.

Sales Forecast: Primary property sales are projected to fall another -10% to -14% in 2026.

Oversupply: The primary driver remains massive oversupply. With millions of unfinished or unsold homes sitting empty, developers are forced to slash prices to generate liquidity, creating a deflationary spiral that keeps buyers on the sidelines.

Some Random Thoughts 💭

This data dismantles the hope for a "V-shaped" recovery. When prices in tier-one cities—historically the "safe havens" of Chinese wealth—are crashing by nearly 8% a year, the psychological damage to the Chinese consumer is immense. Real estate accounts for roughly 70% of Chinese household wealth. A decline of this magnitude is a massive negative wealth shock that explains why consumer confidence and spending are so depressed. We are witnessing the deflation of the largest credit bubble in history, and "buying the dip" has been a losing trade for half a decade.