One of the most revealing metrics in DeFi isn’t TVL alone — it’s what people actually use the chain for.

This Aave V3 comparison tells a very clear story.

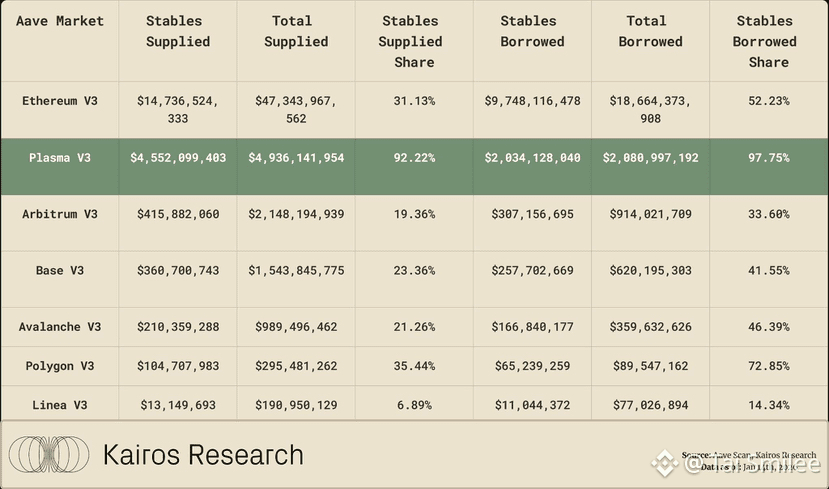

On Plasma V3, over 92% of supplied assets are stablecoins, and an even more striking 97.75% of borrowed assets are stables. That’s not a coincidence, and it’s not speculative behavior.

It signals intent.

Most chains still show a mixed profile: volatile assets supplied for yield, stables borrowed for leverage, and liquidity that disappears the moment incentives fade. Plasma looks different. The market composition suggests users are treating stablecoins as working capital, not casino chips.

In practical terms, this means:

• Liquidity is there to be used, not farmed.

• Borrowing demand is tied to payments, settlement, and cash flow, not short-term leverage.

• Capital efficiency matters more than token narratives.

What’s interesting is that Plasma achieves this without relying on aggressive incentives. The stablecoin dominance appears organic, driven by low fees, fast settlement, and growing off-chain integrations rather than yield chasing.

Compared to Ethereum, Arbitrum, or Base, Plasma’s Aave market looks less like a DeFi playground and more like a financial utility layer.

And that distinction matters.

If stablecoins are ever going to function as real money — not just onchain collateral — they need environments where borrowing and supplying reflect real economic activity. Plasma is quietly shaping itself into exactly that kind of environment.

Sometimes, the strongest signal isn’t growth. It’s composition.