Good morning and welcome to SignalPlus special edition.

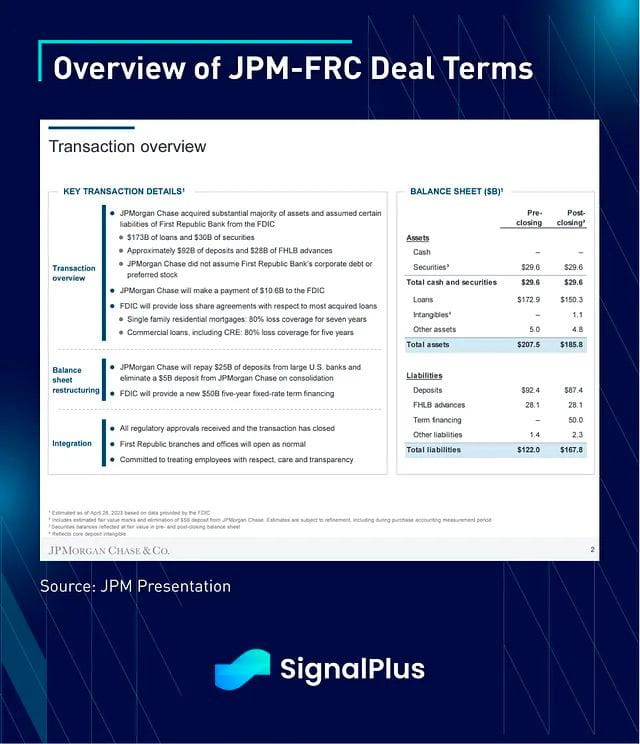

While much of Asia had embarked on its golden week holidays, First Republic Bank was the latest US bank to have gone under and acquired by JPMorgan with the blessing of US regulators. It was yet another masterclass in financial engineering, where FRC’s $92bln of deposits and $173bln of customer loans will be assumed by JPM, marking the 2nd largest US bank failure in history. Furthermore, JPM will also be making a payment of $10.6bln to the FIDC, as well as repaying $25bln of deposits to the consortium of US banks that had supported FRC back in March. JPM will also be borrowing a $50bln loan from FDIC to carry on the transaction. However, similar to SVB’s recapitalization, most of FRC’s corporate debt, preferred stock, and equity holders will be completely wiped out as part of this deal, showing once again that the ‘bailouts’ of 2023 look nothing like the kind we saw post GFC.

In bullet points:

JPM (and other TBTF banks) is now the de-facto "buyer of last resort" for the US banking system

G-SIB reserves are effectively nationalized assets as a (very) strong layer of defense against banking contagion

Policymakers are trying very hard to avoid the optics of any taxpayer bailouts for bad actors

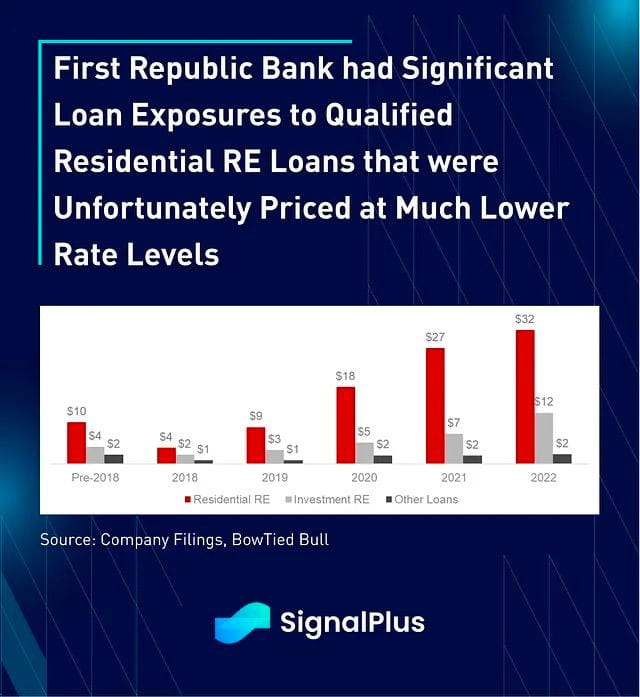

Unlike the SVB debacle, where losses stemmed from unrecognized HTM losses on their MBS asset holdings, FRC's demise came on the back of issuing low-rate and interest-only mortgages to high-quality borrowers

There were no issues with loan creditworthiness or markdowns; problems arose due to gross mismanagement of interest rate risks from poor loan originations

Shareholders and debt-holders are new bag-holders getting zero'ed out for the benefit of uninsured savers and new M&A buyers

Fed (and FDIC) balance sheets are being used selectively as bridge loans to buy time, not outright injections into companies' capital stack

Policymakers have been successful in containing any systemic contagion thus far, with FRC's weekend sale literally registering no impact on risk assets, with US equities making new local highs since NY open

Credit loan availability to the economy will likely continue to suffer as the TBTF (too-big-to-fail) mega-banks get even bigger with their share of total deposits

Regulators' post-GFC alphabet-soup of regulatory ratios (SLR, LCR, NSFR, etc) have completely failed to detect the problems with bank balance sheets this time around - expect a slew of new banking regulatory measures focused on policing interest rate duration mismatches as a post-mortem

Finally, we remind readers once again that we are no longer operating in the era of QE bailouts - witness the weakness in Gold/Bitcoin and other safe-haven assets at the moment

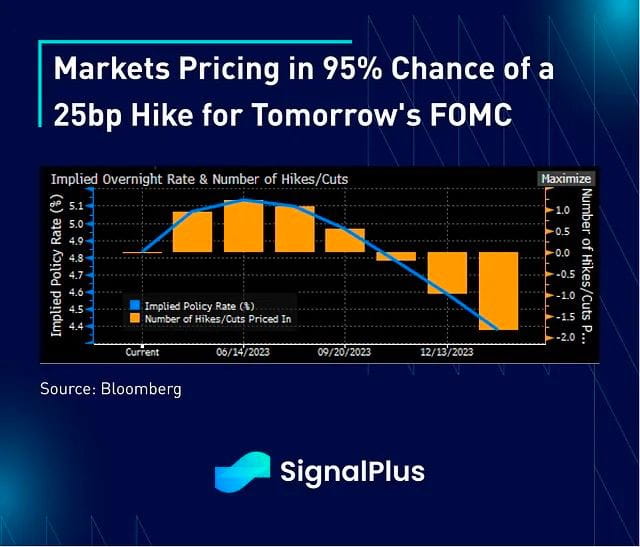

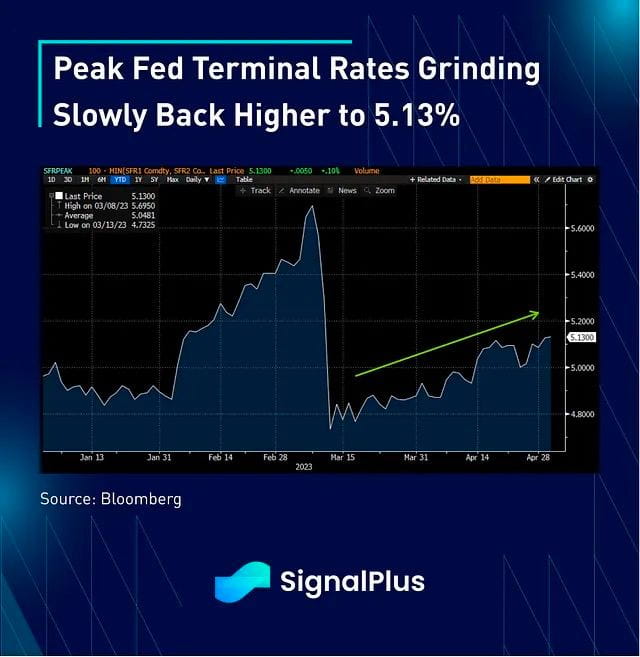

Data-wise, US manufacturing increased by 0.8 points to 47.1 in April, slightly better than expectations with most components in positive territory. Prices paid jumped 4 points to 53.2, with similar pricing pressures seen in the US S&P Global manufacturing PMI, where the report noted subdued client demand "due to inflationary pressures". The reflationary headline pushed interest rates higher all session, with bond yields higher by around 13-15bp across the curve. May hiking odds are back to 95% while June odds have risen to ~30%, and peak terminal rates are slowly grinding back above 5.13% after dropping to as low as 4.80% in mid-March.

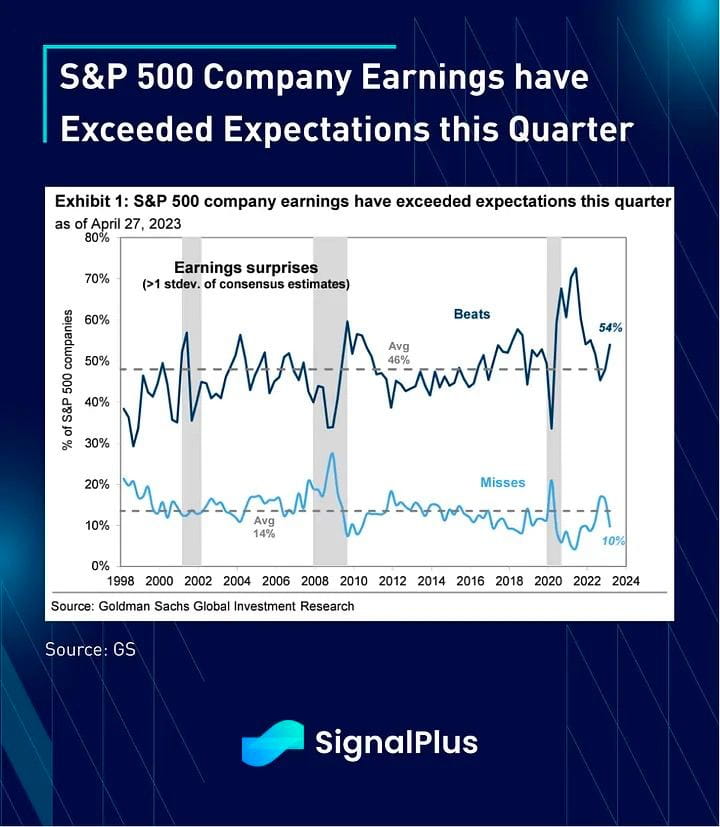

Over in equities, despite the popular adage of "sell in May and go away", stocks have performed remarkably well over the past 2 trading sessions thanks to the quick resolution of the FRC problem and a continued strong run of Q1 earnings. According to data from GS, with 64% of the S&P 500 market cap having reported as of Friday, 54% of firms have beaten EPS expectations by more than one standard deviation, well above the long-term average of 46%. Furthermore, with the blackout window expiring, 75% of S&P 500 companies will be eligible to restart their stock buyback program next week, adding more fuel to the upside just as most traders remain under-positioned in risk assets.

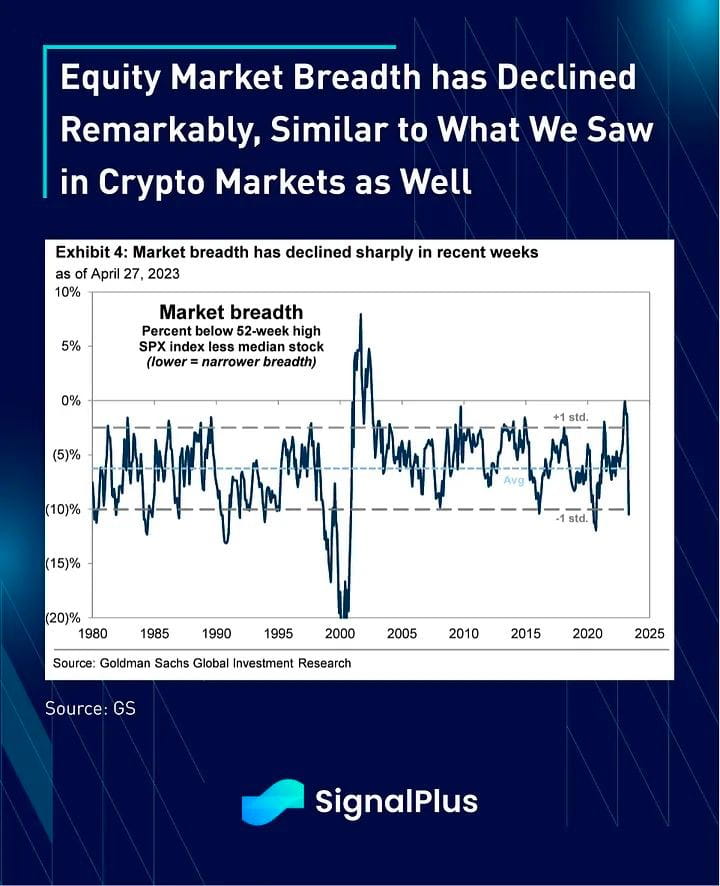

With that being said, market breadth and liquidity have dropped substantially in recent weeks, similar to the deterioration in trading conditions we saw with crypto YTD. Despite a profoundly lower VIX and positive risk-on sentiment, equity prices are increasingly vulnerable to sharp moves either way, with FOMC on Wednesday the obvious catalyst for the next potential move.

While year-over-year earnings estimates are still negative for the S&P, in particular with growth and cyclical names, all of this is more than offset by a massive growth multiple expansion, as markets widely expect an easier Fed going forward on top of declining inflation expectations. Equity valuations have turned a lot more expensive, and there's certainly a lot riding on Chairman Powell to strike a fine balance on the messaging front to keep the soft-landing narrative going.

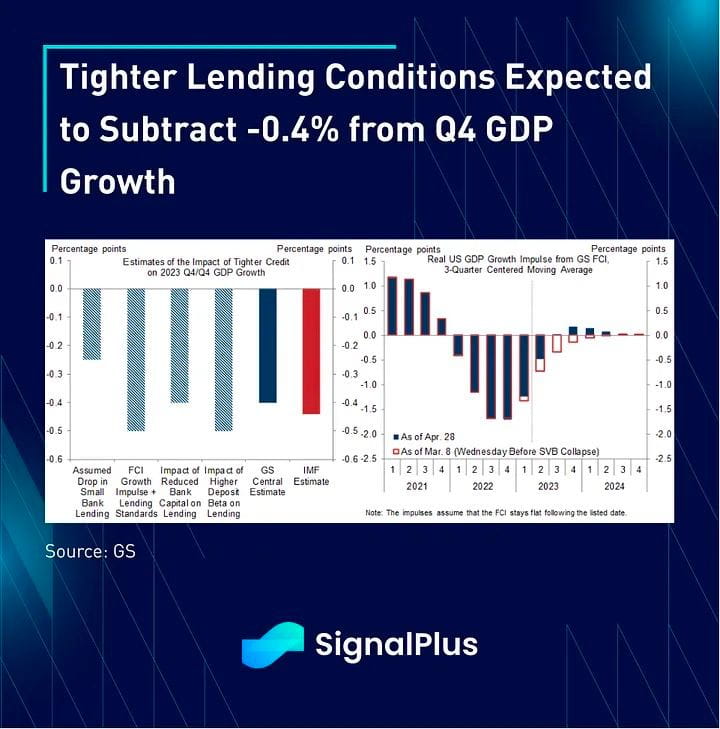

The FOMC will likely deliver a widely expected 25bp hike to 5.25% at the May meeting, though the market focus will be on revision to the forward guidance in its statement. Markets are fully expecting the Fed to suggest that they will be pausing in June, while trying to offset that pivot with a verbal, hawkish bias. The Fed is also expected to cite the recent banking stress and tightening credit conditions as the main drivers supporting a June pause, with the economy possibly falling into a mild recession by the 2H of this year. Numerically, Wall Street expects tighter credit conditions to be a -0.4% drag on Q4 GDP, or equivalent to roughly 1.5 rate hikes as a proxy. As usual, the Q&A will be key in deciphering the nuances of Powell's messaging, though we shouldn't be surprised that a significant portion of the session might be dominated by debt-ceiling discussions this time around.

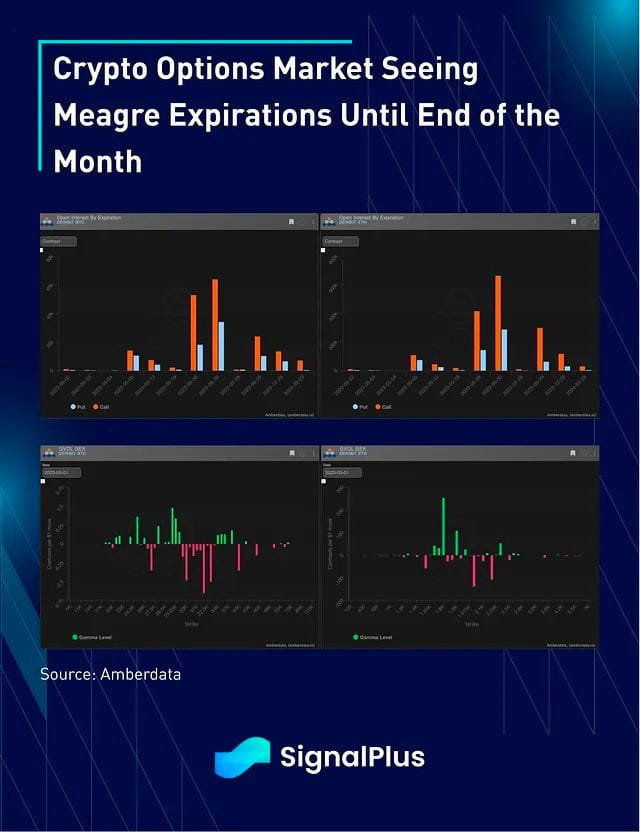

Crypto prices have traded very poorly in the last 72 hours, with BTC failing back towards the $28k area and ETH back to $1.8k. The resolution of the FRC situation has not led to another expansion of the Fed balance as many observers had anticipated as a continuation of the post-GFC playbook, and gold has also been stuck beneath the $2k resistance over the past 8 weeks. Option markets have little in the way of expiration until the end of May, with estimated GEX profiles relatively tame around the current strikes. In addition, vol demand remains relatively muted with a very flat term structure despite a small rebound in IV.

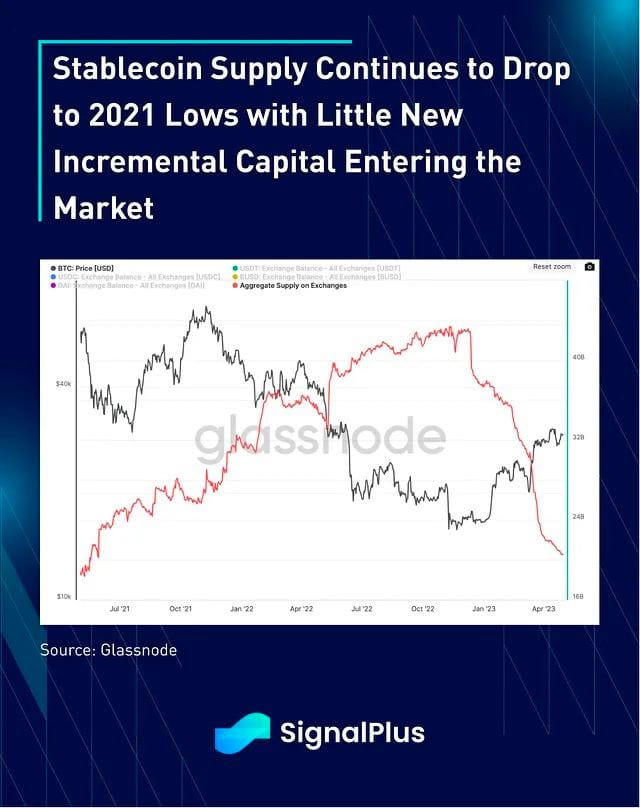

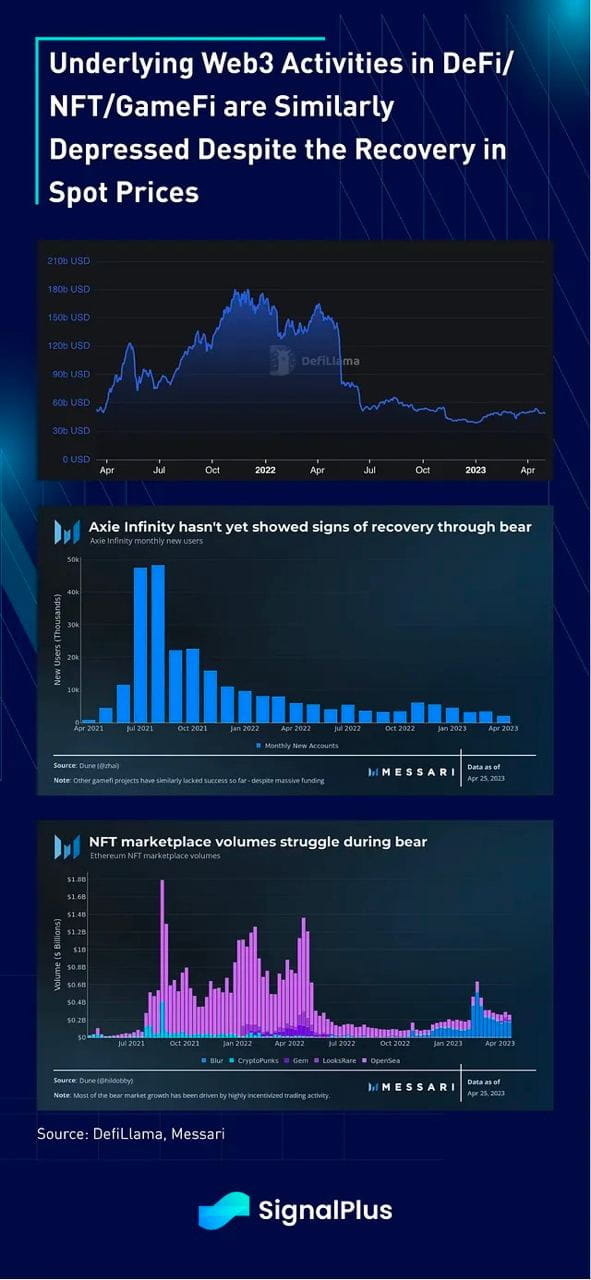

Activity wise, stablecoin balances on CeFi exchanges continue to dwindle with little new incremental capital entering the ecosystem. Furthermore, user activity on DeFi/NFTs/GameFi remain heavily depressed despite the recovery in spot prices, reinforcing our cautious view on crypto prices in the near future.