Algorithmic and automated cryptocurrency trading is a discipline at the crossroads of mathematics, computer science, technical market analysis and the structure of each cryptocurrency.

Like any science, half formal, half experimental, it necessitates a healthy dose of intuition and reflection, as well as techniques of proof and confirmation through market confrontation.

However, the market does not evolve without constraints: most trading platforms charge fees on each trade, and any trading algorithm must consider these fees when calculating performances to ensure that the sum of these fees does not impede the performance algorithm's progress.

There are 2 methods of validating an automated trading algorithm: the backtest and the live execution on an exchange such as Binance.

Backtesting is the general method for seeing how well a strategy or model would have done ex-post. Backtesting assesses the viability of a trading strategy by discovering how it would play out using historical data. The underlying theory is that any strategy that worked well in the past is likely to work well in the future, and conversely, any strategy that performed poorly in the past is likely to perform poorly in the future. Obviously, the conditions that trigger a buy or a sell at time t, in the backtest, only consider the data that precede t, that is to say the data that was already available, as if the algorithm had been run in real market conditions. My backtest was built using 4 years of reconstituted historical data. It gives a relevant period that reflects a variety of market conditions to backtest intraday trading strategies.

A trading algorithm is built from one or more market indicators on a well defined timeframe. A major obstacle to the choice of small timeframes, 1H, 2H and 4H, is the impact of fees on a trade frequency (turnover) that exceeds 1 trade per day or so : the progress of a well thought-out algorithm can be erased by the sum of the fees if the trade frequency is too high.

A revolution in the specification of trading algorithms is taking place, since some platforms, including Binance, offer Bitcoin trading without fees : because high frequency trading is now possible in the crypto-currency world.

I have focused all of my efforts and research on defining high frequency Bitcoin trading strategies on 1H to 4H timeframes.

After several months of intensive research, this metamorphosis of my research has paid off with the emergence of high-performance, low-risk automated trading strategies on BTC.

I sought to place myself in a different research paradigm than trend-following strategies. Indeed, trend following is more suited to time scales that allow for the development of relatively clear trends, i.e., higher time scales, including 8H and 12H, as well as daily, 3 days, and weekly scales.

It was not easy to get rid of the habits of thought and the methodological reflexes that are well established. But one of the major axes of research is creativity and adaptation to new market styles.

A new research paradigm has emerged through hard work : high frequency trading strategies on BTC 0 fees, which no longer exploit BTC trends, but its volatility, whether bullish or bearish, and this in Long Only.

I have succeeded in designing high-frequency algorithms that no longer depend on the direction of Bitcoin, but only on its quasi-chaotic short-term variations. Non-trend dependent strategies have emerged.

What makes this a revolution is that these strategies tend to do away with the natural rhythm of alternating bull and bear cycles, replacing them with a rhythm of alternating clear upswings and less pronounced upswings during phases of very low Bitcoin volatility.

The result is impressive : the backtest graph of my new strategies no longer reflects the alternation of classic bull and bear cycles : in a bear market, the algorithm gains just as much as in a bull market, provided that Bitcoin keeps its local volatility high enough.

These results required a radical change in the way we think about trading and approach market indicators.

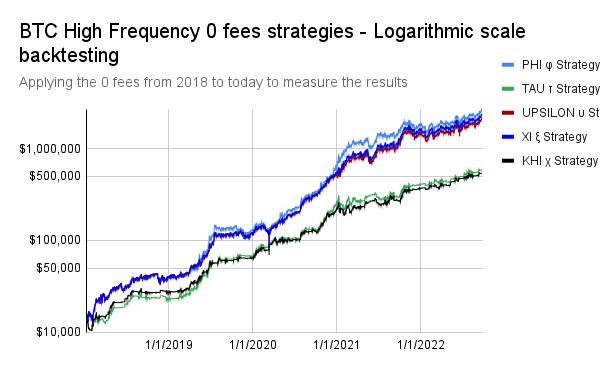

For example, the PHI φ strategy, here backtesting in logarithmic scale, applying the 0 fees from 2018 to today to measure the results of this strategy, has the characteristics we mentioned earlier :

1. high frequency trading on BTC 0 fees : 3.21 trades per day on average

2. Long Only

3. Progression independent of BTC trends : bull and bear markets are "erased" by the results of the strategy.

The risks, measured by the maximum drawdown - a drawdown is a peak-to-trough decline during a specific period for an investment, trading account, or fund; a drawdown is usually quoted as the percentage between the peak and the subsequent trough - are drastically reduced here : it is -30.10% maximum over the whole execution, from 2018 to today.

Another of my results, the KHI χ Strategy, in addition to the 3 features already mentioned on the PHI φ Strategy, has a consistently low maximum drawdown of -29.24%.

Furthermore, this strategy reflects the principle of decorrelation of my high frequency 0 fees strategies to Bitcoin trends in an even more spectacular way : Bitcoin's bull and bear markets are no longer even readable from the algorithm's progression alone.

I can say that it is now possible to break free from the very volatile cycles of the Bitcoin market, with the conceptual revolution that the switch to 0 fee trading offers.

Time, rhythm, scale, in automated trading, is a key factor that can radically change the way we understand market movements.

The notion of fractal in mathematics, especially in geometry, shows that in certain structures, any scale, no matter how small, is isomorphic (i.e. identical in structure) to the higher scales of that same structure. This phenomenon can be observed in the market: at small scales, micro trends appear, with a structure identical to the trends of the higher structures. Nevertheless, their short duration is such that a well thought-out algorithm is able to capture them statistically, which transforms the set of these small-scale bullish micro-trends into a progression whose slope is relatively stable.

Strictly speaking, these micro trends are not trends, but chaotic movements of identical direction. High frequency trading is able to "predict" them statistically, not on any scale, but on certain specific scales and with its own well defined tools.

A revolution is underway, and we are only at the beginning of these profound changes in algorithmic trading.

I will tell you in other articles about the implications and developments of high frequency trading, which is now becoming the core of my research.