Every financial system in history has wrestled with the same fundamental tension. Wealth accumulates in assets. Life demands cash. And the distance between those two things has always cost someone something, whether it's time, fees, taxes, opportunity, or the position itself. Traditional finance built an entire industry around bridging that gap: mortgages, margin accounts, securities-backed lending, repo markets. For centuries, the wealthy have known that you don't sell your assets to fund your life. You borrow against them. The returns keep compounding. The collateral keeps appreciating. The loan gets repaid on your terms.

For most of crypto's short history, that same logic simply didn't apply. You had assets, or you had liquidity. Rarely both at once. The infrastructure to do what any private bank would do for a high-net-worth client, namely let you access the value of what you owned without forcing you to sell it, either didn't exist, was limited to a narrow set of acceptable assets, or came wrapped in so much complexity and counterparty risk that it defeated the purpose. Vanar Chain is building the system that was always supposed to exist. And it's building it in a way the industry hasn't seen before.

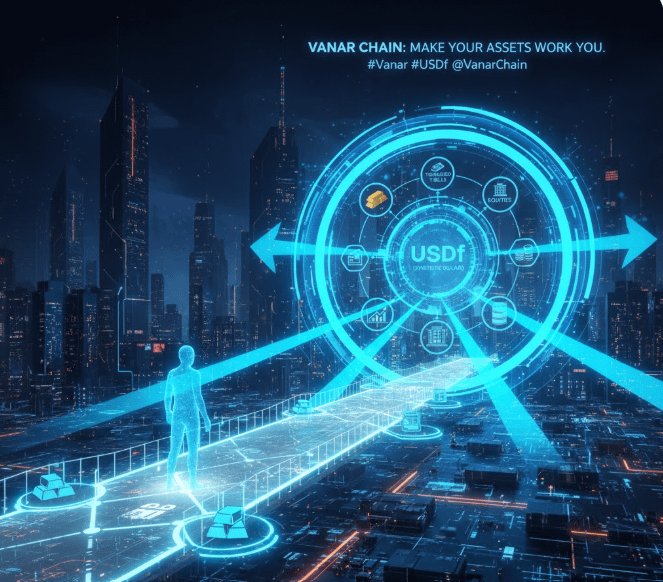

Vanar Chain is positioning itself as the first universal collateralization infrastructure in the blockchain space. That phrase deserves unpacking, because "universal" is doing a lot of work there, and it's precisely the word that sets this apart from everything that came before. The existing collateral frameworks in DeFi were built on exclusivity. They accepted a handful of blue-chip tokens, set rigid parameters around what counted as legitimate collateral, and drew a firm line between the on-chain world and everything outside it. The architecture was elegant in its simplicity and deeply limited in its ambition. Vanar Chain's thesis is that this limitation is not a feature. It's a failure of imagination.

The protocol is designed to accept a genuinely broad spectrum of liquid assets, including conventional digital tokens and tokenized real-world assets, as collateral for issuing USDf, an overcollateralized synthetic dollar built to give users stable, accessible on-chain liquidity without forcing them to give up the underlying positions that generated their wealth in the first place. The mechanism is straightforward in principle and extraordinarily difficult to execute at scale: deposit your assets, receive USDf, retain full exposure to what you deposited. When you're done, repay the synthetic dollar and reclaim your collateral. Your assets never left. They just worked harder while you were gone.

To understand why this matters so much right now, you have to appreciate what the asset landscape looks like in 2025, because it looks nothing like it did when the first DeFi protocols were sketching their collateral whitelists on whiteboards. Tokenized US Treasuries have crossed billions in on-chain circulation. Tokenized money market funds are generating real, auditable yield for on-chain holders. Tokenized real estate, private credit, and commodities are moving from pilot programs into genuine market infrastructure. BlackRock, Franklin Templeton, and a growing roster of traditional asset managers have committed real resources to the tokenization thesis, and their products are landing on-chain with increasing regularity.

The result is a world where the on-chain economy is no longer a closed loop of native crypto assets trading volatility back and forth. It is becoming a genuine mirror of the broader financial system, with real yield, real collateral quality, and real institutional participation. The old DeFi infrastructure wasn't built for this world. It was built for a world of ten tokens and one use case. Vanar Chain is building for the world that actually exists.

Consider the position of someone holding a meaningful allocation in tokenized Treasury bills. They are earning real yield on a low-risk asset. They have chosen, deliberately and thoughtfully, to hold that position rather than deploy it elsewhere. But they also exist in an economy where opportunities arise, expenses occur, and liquidity needs don't pause because your portfolio is locked up in a T-bill wrapper. Without Vanar Chain's infrastructure, their options are limited: liquidate the position, forfeit the yield, and reenter later at whatever price prevails, or simply miss the opportunity entirely. With it, they post the T-bill as collateral, receive USDf against its value, and deploy that liquidity wherever it's needed. The T-bill keeps earning. The position stays intact. The user moves forward.

Multiply that use case across every asset class that tokenization is now bringing on-chain and you begin to understand the scale of what's at stake. Every tokenized asset that exists without a productive collateral layer underneath it is, in economic terms, dead capital. It sits there, holding value, generating whatever yield it generates in isolation, but unable to participate in the broader liquidity ecosystem that turns static holdings into dynamic financial infrastructure. Vanar Chain's entire architecture is a direct assault on that deadness. It is, at its core, a machine for converting idle assets into productive ones, without destroying the underlying position in the process.

The issuance of USDf through overcollateralization is the mechanism that makes this work, and the overcollateralization piece is not incidental. The history of synthetic dollars and algorithmic stablecoins is a graveyard of projects that either underestimated the importance of genuine collateral backing or built elaborate game-theoretic scaffolding that collapsed the moment market conditions stopped cooperating. Terra's UST implosion in 2022 is the most dramatic example, but it isn't the only one. The market learned, expensively and publicly, that a synthetic dollar is only as trustworthy as what stands behind it. USDf's architecture takes that lesson seriously. Every dollar of USDf issued has more than a dollar of real asset value sitting beneath it. The buffer isn't symbolic. It's the foundation of the entire trust model.

What makes Vanar Chain's approach genuinely novel isn't just the overcollateralization, which MakerDAO has been doing with DAI for years, but the diversity of the collateral pool it's designed to support. A synthetic dollar backed exclusively by ETH is a different product from one backed by a diversified pool of tokenized Treasuries, money market instruments, and high-quality digital assets. The former is exposed to the idiosyncratic volatility of a single asset class. The latter is structurally diversified in a way that makes it far more resilient to the kind of correlated drawdowns that tend to stress monoculture collateral systems. Vanar Chain isn't just building a synthetic dollar. It's building a synthetic dollar that can, by design, be backed by the full breadth of what the tokenized economy produces.

There's a deeper infrastructure story here too, one that extends beyond individual users and their liquidity needs. When you build a universal collateralization layer that can accept tokenized real-world assets, you are also building the bridge that the tokenized asset market has been missing. Tokenization without utility is a half-finished product. You can put a building on-chain, but if that on-chain representation can't interact with the broader DeFi liquidity ecosystem, you haven't really changed much about how capital flows. You've just changed the format of the ownership record. Vanar Chain changes the underlying economics. Tokenized assets that flow through its collateral infrastructure become genuinely productive in the DeFi sense, not just in the "I hold this and it appreciates" sense but in the "I can use this as active financial infrastructure" sense.

This is the vision that animates Vanar Chain's technical architecture, its approach to risk management, and its long-term roadmap. The protocol needs to solve real engineering problems to make good on this promise. Pricing heterogeneous collateral accurately requires robust oracle infrastructure. Managing liquidations across asset classes with different liquidity profiles requires sophisticated risk parameters and circuit breakers. Onboarding tokenized real-world assets requires navigating legal and compliance frameworks that are still being written in real time by regulators who are themselves still figuring out what these assets are. None of this is trivial. All of it is being built with the kind of methodical, systems-level thinking that the problem demands.

The on-chain economy is in the middle of a structural transition that most participants are still processing in real time. The assets are changing. The participants are changing. The volume of real-world economic activity that is moving on-chain is accelerating in ways that would have seemed implausible just a few years ago. The infrastructure underneath all of it needs to catch up, and in the collateral and liquidity layer specifically, the gap between what exists and what the market needs is one of the most consequential unsolved problems in the space.

Vanar Chain is not promising to solve every problem in that gap overnight. What it is doing is building the foundational layer that makes the next chapter of on-chain finance possible: a world where your assets work for you continuously, where the choice between holding and accessing liquidity is no longer forced, and where the full spectrum of tokenized value can participate in a unified, productive liquidity ecosystem. That is not a small ambition. But it is, finally, the right one.