1. The darkest hour

During the Age of Discovery in the 18th and 19th centuries, Great Britain, as the "sun never sets" empire, used pounds to anchor gold and made it the world's currency, launching nearly two centuries of world colonization. After the two world wars, due to Britain's huge military spending and its use of gold to purchase weapons from the United States, the pound decoupled from gold. At this time, the US dollar stood on the stage of history and became the new global currency - the Bretton Woods system. Until the dollar crisis of the 1970s, the dollar's peg to gold existed in name only, and the dollar continued to be tied to oil.

In 2020, the COVID-19 epidemic broke out around the world, and crude oil futures once fell into negative values. The Federal Reserve released huge amounts of money, and Bitcoin successfully exceeded the market value of US$1 trillion in the 2020-2021 cycle, standing on the global financial stage as an emerging mainstream alternative asset. And will this also kick off the creation of new assets bound to the US dollar?

In August 2023, Fitch downgraded the U.S. rating to "AA+" from "AAA" because the expected financial deterioration over the next three years and the recurrence of government debt ceiling negotiations threatened the government's ability to meet its debt obligations. If the U.S. debt crisis and market recession occurs, it will inevitably repeat the mistakes of the 2008 economic crisis. A market collapse may lead to a sharp decline in the stock market, a sharp decline in corporate value, a negative impact on domestic and foreign investors, and a setback in investor confidence, leading to an economic recession and a financial crisis. The market continues to slump, with the three major indexes and global stock indexes all falling sharply.

The domestic market recession in the United States will not only trigger a crisis for banks and financial institutions, but the U.S. debt problem will extend to global concerns, because the health of the U.S. economy has an important impact on the global economy. This results in market instability and investor risk aversion. Banks may face liquidity problems and investors may sell off assets, exacerbating instability in the financial system. Not only selling highly liquid investment methods such as stocks, but also choosing a multi-polar financial order characterized by diversified currency hedging, gold, crude oil, digital currencies, and commodities.

But for the digital currency market, it should be a pattern of declining first and then rising! First of all, the digital currency market is not a pure financial market. It is not completely subject to the economic situation and financial market order of any single country. If the global financial market collapses, digital currency will inevitably experience a sharp decline following the U.S. stock market. But after the U.S. stock market falls, investors will realize that digital currency has the properties of risk aversion and asset preservation. Therefore, they will inevitably receive favor from investors and people in the United States and even around the world, and some stable digital currencies will surely receive great value recognition.

Darkest hour. As we all know, encrypted digital currencies have fallen deeply in 2022, with mainstream digital assets such as Bitcoin and Ethereum falling by more than 70%. Mainstream exchanges, asset management institutions, public chains, and lending platforms have gone bankrupt or suffered thunderstorms. Although it will stabilize and rebound in 2023, the extent will be extremely limited, and market liquidity will further shrink. Under extremely poor market liquidity, the "818" liquidation event occurred (the amount exceeded the liquidation volume of the FTX event). It can be said that the currency circle has entered its darkest moment.

darkness before dawn. Before a real bull market comes, the market always goes through a long period of decline, downturn and volatility. This is true for traditional financial markets, and it is also true for encrypted digital currencies. And this period is also a really difficult stage. But the dawn is coming, and the sunrise will surely bring flowers into bloom:

1. The Bitcoin halving event in 2024 will kick off the next round of bull market;

2. There will inevitably be a sharp decline before a big bull market, and the main reason is caused by the traditional financial market (debt crisis, corporate bankruptcy);

3. After the crisis, the bull market really begins;

4. The next high point of Bitcoin will be around $120,000.

2. Who rules the ups and downs? Market review of Bitcoin halving

On May 22, 2010, Laszlo Hanyecz, a programmer from Florida, USA, successfully exchanged 10,000 Bitcoins for 2 pizzas - the most expensive pizza in history.

2.1 Bitcoin’s block generation mechanism

The blockchain can be thought of as a distributed ledger. Each block is an account page, which records real transaction records. The blockchain ledger is not maintained by a central node like a bank, but is backed up by all PC users (i.e. nodes), and each user stores all transaction records.

Transaction records record the flow of money. Bitcoin/bitcoin is the native money that can be used for transactions on this blockchain, with a total amount of 21 million. It has only one issuance channel, which is to the person who created the block/account page. award. On the Bitcoin blockchain, all transaction records approximately every 10 minutes require someone to create an account page and permanently store the account page in Bitcoin's only global ledger. In addition to receiving block rewards, the creator can also receive transaction fees for all transactions in the created account page. This is block generation, also known as mining.

2.2 What is Bitcoin Halving

When the Bitcoin blockchain was born in 2009, the reward for creating a block was 50 BTC, and the reward was automatically halved every 210,000 blocks. Every 2016 blocks (about two weeks), the system will adjust the mining difficulty based on the block generation time of the previous cycle, so that the block generation time is stable at about 10 minutes. It is not difficult to conclude that the reward halving cycle is approximately once every 4 years. Bitcoin will usher in its fourth halving in 2024, and the reward for creating a block will drop to 3.125 BTC. Since the smallest unit of Bitcoin is Satoshi (SAT), which is 0.00000001 (one hundred millionth) Bitcoin, the block reward will be lower than 1 Satoshi for the first time after the 33rd halving in 2140, and Bitcoin mining rewards will be completely ended. .

History has proven that Bitcoin halving is an important catalyst for pushing Bitcoin into a new bull market. The first three halvings all ushered in a sharp increase in the price of BTC. The details are shown in the table below.

The countdown to the 2024 halving has begun, and countless project parties have begun gearing up to shine and stand out in the new halving cycle. The introduction of traffic and funds in traditional industries is also in full swing in many aspects. Driven by many combined forces, history will eventually repeat itself, and the start of a new round of bull market is just around the corner. Let’s objectively review the market conditions of the three halving cycles in BTC’s history.

2.3 The first halving

Before the first halving cycle, in the second half of 2011, there were many large-scale BTC theft incidents such as Mentougou. The price of BTC plummeted from 31.91U to 2.04U, a drop of 93.6%. Then BTC started a two-year cycle before and after the halving. uptrend market. At that time, Bitcoin was still in the era of early enthusiasts, and was mainly adopted by technicians and retail investors. There were very few people who knew and had contact with it in China. Discussions and fermentation about Bitcoin halving were mainly concentrated in overseas communities such as Facebook and bitcointalk forums. In 2012 November 28th - The first halving reduced the mining reward to 25 BTC per block. The price reached a maximum of 12.41U that day, which increased approximately 6 times in the year before the halving.

After the halving, with the birth of Bitcoin professional mining machines and the rapid expansion of application/payment scenarios, Bitcoin accelerated its rise, reaching 266U on April 10. After V God released Ethereum and smart contract technology on November 10, 2013 Reaching its climax, the price of Bitcoin reached a peak of 1242U one year and one day after the halving, rising 100 times one year after the halving.

In the two years before and after the first halving, Bitcoin rose 600 times. Then, with changes in the policy environment and thunderstorms on many exchanges, the price of Bitcoin began to fall into a deep bear for 14 months.

2.4 The second halving

July 10, 2016 – Second halving, mining rewards dropped to 12.5 BTC per block.

After experiencing a 600-fold increase in the first Bitcoin halving cycle, a large number of venture capital institutions and hedge funds participated, and the participating groups expanded rapidly. Major forums enthusiastically discussed the impact of halving on currency prices, computing power and mining. influence, and predict the rise in currency prices based on the previous round of experience. One year before the halving, BTC rose as expected, rising from 162U to 790U, a nearly 5-fold increase. However, the currency price experienced two corrections in a short period of time before and after the halving, and finally fell to 475U. Many people thought that this halving cycle was over, but they did not know that BTC would then start an 18-month bull market.

The rising trend continued until December 17, 2017, when the price of BTC soared to 19785U, a 122-fold increase during the entire halving cycle. Of course, many people attributed the rise after the halving to the ICO speculation boom brought by Ethereum. After the boom, history repeated itself, a year-long bear market arrived, and the currency price fell back to around 3000U.

2.5 The third halving

May 12, 2020 – The third and most recent halving saw miner rewards drop to 6.25 BTC.

After nearly 10 years of development, Bitcoin has gradually attracted the attention of traditional industry giants. Fidelity, JP Morgan, Facebook, etc. have successively joined in. The story of digital gold and safe-haven assets is well known to everyone, and countless "KOLs" have stepped forward to call for orders. The time was also one year before the halving was implemented. BTC started a new round of rise after trading sideways at 3000-4000U for nearly five months. However, the famous "312" event occurred near the halving (described in detail later). The cumulative decline in two days exceeded 50%, and the currency price returned to below 4000U. However, the rising expectations of the halving are still strong. After the correction, BTC started a crazy rising mode. Coupled with the support of traditional giants such as Paypal/Tesla and the breaking of narratives such as NFT, BTC rose to 64898U on April 14, 2021. . On November 10, 2011, the price of Bitcoin broke a new high, reaching 68998U.

Based on the market changes before and after the three historical halvings, the Bitcoin mining reward halving cycle can usually be broken down into two rounds before and after the halving. The increase before the halving is relatively gentle, and there are periodic highs without breaking the historical high, and it is approaching There will be a certain callback/sell-off when the halving occurs. After the halving, the rise will accelerate exponentially and reach a climax under the guidance of the inevitable trigger, reaching a record high. In particular, the strong demand brought about by the influx of traditional institutions/enterprises and the application craze on Ethereum finally ended the bull market due to thunderstorms and policy pressure.

The first three halvings have attracted early enthusiasts and programmers, venture capital institutions and hedge funds, traditional corporate giants and senior intellectuals respectively. The fourth halving in 2024 is coming, and the entire Bitcoin community is paying attention and being promoters. The application approval of Bitcoin ETF and the advancement of circle-breaking games such as the creator economy, as the Federal Reserve’s interest rate hike is coming to an end, will further attract the attention of a wider range of traditional financial markets and ordinary investors, and the bull market in 2024-2025 will inevitably come. , it is impossible to be absent.

3. Waterloo in the currency world? Analysis of major black swan events in recent years

Cryptocurrency has always survived doubts, but it has also developed rapidly amid doubts.

3.1 "94" Incident (2017.9.4)

Cause: On September 4, 2017, seven departments of the People's Bank of China, the Cyberspace Administration of China, the Ministry of Industry and Information Technology, the State Administration for Industry and Commerce, the China Banking Regulatory Commission, the China Securities Regulatory Commission and the China Insurance Regulatory Commission jointly issued the "Announcement on Preventing Token Issuance Financing Risks", announcing that Positioning ICO (Initial Coin Offering) as an "illegal financial activity", prohibiting ICO and new projects, and existing projects must be liquidated within a time limit, that is, any token issuance financing activities are clearly prohibited, and all ICO token trading platforms The transaction needs to be cleared and closed by the end of the month.

The "94 Ban" has allowed virtual currencies, which have been growing wildly, to be included in the strong financial regulatory framework. On that day, 12 token issuance platforms announced the suspension of token issuance business on their official websites, announcing that they would stop issuing new financing projects. 88 different DIGICCY exchanges and 85 token issuance and trading platforms in China have either stopped withdrawing coins or gone overseas to seek opportunities.

Market reaction: On the day the news was announced, Bitcoin once fell by more than -10%, and started plummeting again on September 8th. On September 14th, the decline even exceeded -20%. It quickly rebounded after oversold on September 15th. As of the close of trading on September 15th, the rebound rate exceeded 16%. .

Subsequent trends: Bitcoin has been on a meteoric rise since hitting the bottom on 9.15, and has been rising all the way, reaching its historical peak of $20,000 on December 17 of the same year. Summary: This incident caused the market to plummet for about 10 days, and then started a bull market that lasted for 3 months.

3.2 "312" Incident (2020.3.12)

Cause: Macroeconomic sentiments such as the epidemic, global stock markets, economic crisis, and liquidity panic have spread to the currency circle. The US stock market has triggered the circuit breaker mechanism twice within a week. Stock markets in various countries have plunged. The spread of the epidemic has caused most people to be pessimistic about the future. expected.

Market reaction: Since mid-February, the price of Bitcoin has been in decline, with a drop of more than -20% on March 12 alone. Due to the spread of panic and stampede liquidation, the maximum drop even exceeded -40% on March 13, APP There was a long downtime, and investors were unable to close positions through the APP.

Subsequent trend: Bitcoin has been rising since hitting the bottom on March 13th, starting a magnificent bull market. In the end, the price of Bitcoin exceeded 60,000 US dollars.

Summary: The super negative situation caused the market to fall for more than one month, and the price plummeted sharply, the turnover rate was high, and the chips were completely reshuffled. This is one of the conditions for a bull market to easily start. Of course, the subsequent slowdown in the impact of the epidemic has made expectations more optimistic, which is also an important reason for the launch of the bull market. More importantly, the Federal Reserve has also started an interest rate cut cycle, with a variety of benefits superimposed.

3.3 "519" incident (2021.5.19)

Cause: On the evening of the 18th, the China Internet Finance Association, the China Banking Association, and the China Payment and Clearing Association jointly issued the "Announcement on Preventing the Risks of Speculation in Virtual Currency Transactions" (hereinafter referred to as the "Announcement"). The announcement clearly states that relevant institutions are not allowed to carry out business related to virtual currency, and reminds consumers to increase their awareness of risk prevention and beware of losses of property and rights.

Market reaction: On May 19th, the market experienced a panic plunge. The maximum decline of Bitcoin once exceeded -48%, and then began a long period of shock-type decline, which lasted almost exactly 2 months, and ended on July 20th.

Follow-up trend: The price has continued to rise since July 21, starting the main rising wave market. The entire main rising wave has lasted for just 3 months. As of October 20, the price exceeded 66,000 US dollars. After that, after the head was established, the trend started. All the way down.

Summary: Policy negatives led to a sharp correction in the bull market, but the main force also used this opportunity to quickly wash away the unsteady follow-up orders during the bull market's main rise, and then completed the last wave of sprint in the bull market.

3.4 Luna incident (2022.5.9)

Cause: The reason for the collapse of luna is relatively complicated. There are three main theories out there. (1) Leverage liquidation (2) Institutional short selling (3) Team self-destruction

(1) Anchor itself: The rebalancing of positions by large investors caused panic runs, and the LUNA-UST dual currency mechanism of the Terra public chain (users can burn LUNA to mint equivalent UST, and vice versa) caused a death spiral, and the market plummeted, and LUNA The price collapsed rapidly. UST holders believed that the mortgage amount was insufficient, so they sold UST, and the price fell and became unanchored. At this point arbitrageurs minted LUNA with UST, and more LUNA flooded the market causing further price drops.

(2) The institution first borrowed 100,000 BTC, sold 25,000 of them into UST, and shorted 75,000 BTC at the same time. When BTC fell to $30,000, Citadel sold UST and decoupled UST. Do Kwon was forced to sell his BTC reserves at a low price, and the flow of BTC to the market pushed the price down again. Meanwhile, institutions remain short.

(3) Anchor, the most important demand scenario in the Terra ecosystem (annualized fixed interest rate reaches 18%), is constantly sucking blood. Until better application scenarios are created, it relies entirely on real money subsidies to maintain its rate of return. When a bear market comes, a crash seems to be a matter of time. Rather than being forced to die, it is better to simply design a way to die for yourself. In two years, the LUNA Foundation acquired 70,000 BTC, shorted BTC at a very small cost, and used leverage to short LUNA.

Market reaction: Luna’s panic plunge began on May 9, 2022, with the day’s decline reaching -52.85%. Until May 13, Luna’s price can be considered to be almost zero. Bitcoin is just in a downward cycle, and there is no panic decline.

Subsequent trends: The old Luna was removed from the shelves, and the new Luna was restarted on May 31, but it calmed down again after a brief period of speculation, and the current price is less than 0.4.

Summary: An in-depth understanding of the operating mechanism behind the currency and ecological scenarios have certain reference significance for judging price trends under extreme circumstances, and can also help avoid risks to a certain extent.

3.5 FTX incident (2022.11.8)

Cause: A private financial document disclosed by the well-known media CoinDesk pointed out that FTX and its sister company Alameda Research may have debt problems. Instantly triggers a crisis of trust among users. According to this document, most of Alameda's assets are FTX and Solana tokens that are closely related to it. Not only is the market liquidity poor, but the valuation has high volatility risks, but the company's liabilities are real US dollar liabilities. Combined with the previous findings by some researchers that FTX’s reserves are constantly draining, this has begun to cause some cryptocurrency investors to worry about the FTX exchange.

In May 2022, the stablecoin project LUNA suddenly collapsed, causing many cryptocurrency institutions to go bankrupt. At that time, Voyager was unable to redeem its loans to Three Arrows Capital and Alameda, which led to its bankruptcy and reorganization. Among them, the number one borrower is the bankrupt Three Arrows Capital, while the second place is FTX’s sister company Alameda. Analysis pointed out that at that time, Alameda was able to temporarily escape from the storm because it obtained FTX mortgage 172 million FTT worth approximately US$4.19 billion. However, it is precisely because too much FTT is staked that this causes FTX’s FTT tokens to become less liquid. The U.S. dollars borrowed back were used to plug Alameda's holes, resulting in a shortage of the company's reserves. Therefore, when the media revealed that FTX and Alameda may have debt problems at the beginning of that month, the panic in the market will cause a large number of users to begin to want to sell their FTT, and the lack of liquidity and FTX's own potential debt crisis will also lead to other buyers. holders were unwilling to participate in the acquisition, and FTX, which lacked reserves, was unable to maintain the stability of the FTT token price through acquisitions. This directly led to the collapse and plummeting of the FTT token price, which in turn triggered more and more FTT holders to sell at low prices, ultimately leading to FTX is headed for bankruptcy.

Market reaction: It plummeted 75% on November 8, 2022. It fell directly to 5.5 from the opening of 22 on that day. It continued to fall sharply in the following days, and the lowest price fell to around 1.2 on November 14. BTC fell in total on November 8 and November 9. Also more than 20%.

Subsequent trend: After the plunge, there were some rebounds in the middle, but the height did not exceed 3. To this day, its price only remains around 1. Summary: Thunderstorms in relatively influential exchanges are more likely to cause panic in the market than thunderstorms in a single currency pair, thereby causing the overall market to plummet.

3.6 SVB incident (2023.3.10)

Cause: In the past year, the Federal Reserve has raised interest rates eight times in a row, and the federal funds rate target range has risen to between 4.5% and 4.75%. After interest rates are raised, the currency appreciates, bond yields rise, and transaction prices fall, causing bond prices to fall. More bonds can be purchased with the same amount of funds. The bank held a large amount of bonds, which caused a sharp decline in assets, causing market panic and causing a run.

Market reaction: On March 10, Silicon Valley Bank in the United States became insolvent and was taken over by an insurance agency. European stock markets plummeted overnight. The Italian and Austrian markets fell by more than 4%. Markets such as Germany and Spain fell by more than 3%. France, the United Kingdom, etc. The market generally fell more than 2%. BTC dropped 7% on the day on 3.10, but not a panic-level drop. The most serious incident of this incident was that the USDC issued by Circle Company was seriously de-anchored to the US dollar, once falling to 0.86USD, and USDT also experienced a large premium, which had a serious impact on the stablecoin market.

Follow-up trend: BTC stabilized and began to rebound on March 11th. The rebound basically lasted for a month. As of April 11th, when it rose 6%, the main rebound of this wave basically came to an end.

3.7 Summary of foreseeable macro risks

Each bull-bear cycle will have corresponding risk events as the prelude and curtain. For example, "94" in 2017 and "519" in 2021 are both market events caused by policies, and the trend after policy events is often the last round of main rise in the bull market.

The start of each bull market will be accompanied by the reshuffle and reorganization of the previous cycle. For example, luna Thunder, FTX Capital, and Three Arrows Capital were all market leaders in the last bull market. Only when the market is fully shuffled, fluctuated, and fell will real new forces enter the market and start a new cycle.

2023 is the starting point of a new cycle, but it is by no means a big bull market cycle. The new bull market cycle, in addition to the Bitcoin halving, also requires a core factor - the marginal benefit of the macro environment, and our current environment is:

1. The Federal Reserve continues to raise interest rates, and continued high interest rates have led to reduced liquidity in the entire financial market.

2. The inversion of long-term and short-term interest rates on U.S. debt has strengthened expectations for further economic recession in the future. At the same time, it may cause systemic risks to some banks, such as the SVB incident. Some commercial banks borrowed short and bought long. Due to the inversion of interest rates, commercial banks suffered losses, causing bad expectations for users and causing a run.

3. SEC’s attitude towards the Bitcoin spot ETF applied by some institutions and whether it is finally approved.

4. US inflation and employment data. If inflation continues to be high and employment data remains good, the high interest rate environment will continue.

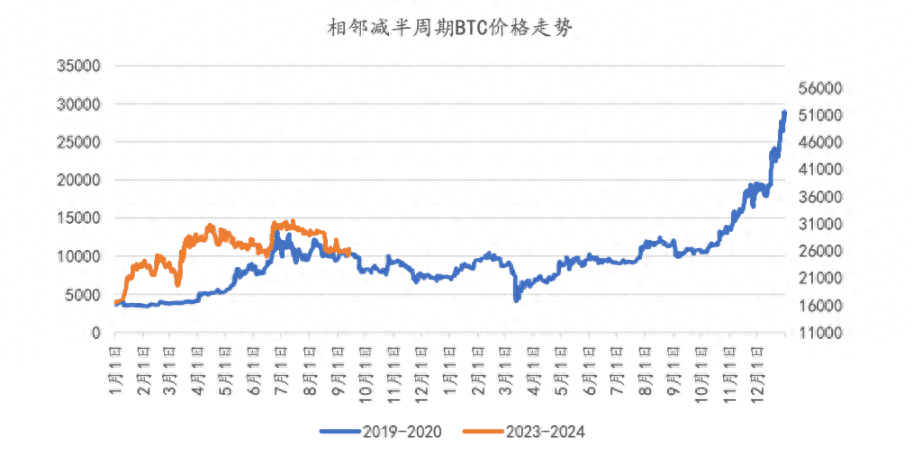

4. The history is surprisingly similar? 2019-2020 and 2023-2024

Everything has a certain cycle, especially the financial market.

4.1 Market trends

At the beginning of 2023, BTC experienced a small positive trend at the beginning of the year, but it began to correct after April. It hit the previous high in mid-June and then failed to stabilize and continued to correct. After June, the band market performance is similar to that of the same period in 2019, but overall it is far worse. 2019 is going strong.

BTC price trend during adjacent halving cycles

What is most closely related to the market trend is the impact of the Bitcoin halving cycle. As of today, there are more than 200 days left before the fourth Bitcoin halving. Looking back at the history of Bitcoin halving, it seems that every halving is accompanied by a rise in the price of Bitcoin:

4.2 Macro background in similar years

Looking at past Bitcoin bull and bear markets, we can see that macro liquidity has had an important impact on Bitcoin prices. Specifically, the Bitcoin bull market in 2012 occurred against the backdrop of the Federal Reserve's third round of quantitative easing and the European Central Bank's easing policy; the 2016 bull market was related to Brexit, and the Bank of England resumed its policy in response to uncertainty. A bond purchase plan was launched to further release liquidity. At the same time, the launch of Bitcoin futures attracted a large amount of OTC funds into the market; the bull market in 2020 was affected by the global epidemic, and the United States adopted a large-scale loose monetary policy, including unlimited quantitative easing, to inject a large amount of liquidity into the market. This has led to massive inflows into crypto markets such as Bitcoin, driving up the price of Bitcoin. In contrast, bear markets typically coincide with a global liquidity crunch. During the bear markets of 2014, 2018, and 2022, a global liquidity crunch caused capital to flow out of the Bitcoin market, depressing Bitcoin prices. These results demonstrate that global central bank monetary policies and liquidity conditions have an important impact on the Bitcoin market. Loose monetary policy and abundant liquidity tend to push Bitcoin prices upward, while tightening monetary policy and tight liquidity may exert downward pressure on Bitcoin prices.

Two other related reference data (essentially the impact of monetary policy and liquidity):

The correlation between liquidity and bull markets:

The US M2 growth rate reached its peak in January 2012, and BTC reached its peak about 22 months later (November 2013);

The US M2 growth rate reached its peak in October 2016, and BTC reached its peak about 14 months later (December 2017);

The US M2 growth rate reached its peak in February 2021, and BTC reached its peak about 9 months later (November 2013).

The correlation between the US election and the bull market:

After the US election in November 2012, BTC reached its peak about 12 months later (November 2013);

After the US election in November 2016, BTC reached its peak about 12 months later (November 2017);

After the US election in November 2020, BTC reached its peak about 12 months later (November 2021).

Most of the past three U.S. elections occurred near the peak or small peak of M2 money supply growth rate. It is speculated that using a looser monetary policy during the general election may be beneficial to economic prosperity.

4.3 Meso-level indicator data of major currency circles and their deduction logic

Several important indicator data are selected to describe the current status of the industry, compare the main influencing factors facing the encryption market in 2019, and try to deduce the future trends of Bitcoin and encryption markets.

4.3.1 Current development status of the encryption market and industry

(1) Market value increased slightly

As of September 14, 2023, the total cryptocurrency market capitalization was US$1.045 trillion, an increase of 4.9% from US$0.996 trillion in the same period last year. The current macroeconomic uncertainty has caused the cryptocurrency industry to generally fluctuate widely.

(2) Differentiation of rise and fall: rise and fall of cryptocurrency in the past half year

The cryptocurrency market has been a rollercoaster ride over the past half year, with most large projects underperforming, largely due to SEC and trading platform lawsuits, which impacted many of the top 100 coins. Bitcoin, along with other digital currencies (BCH, LTC, etc.), showed short-term strength in the second quarter, driven by news about the listing of ETFs and other institutions. Overall, wide fluctuations and no clear trend are still the main themes.

(3) Trading activity shrank

Liquidity, volatility, and trading volume across digital asset markets continue to compress, with many indicators falling back to pre-2020 bull run levels. With the exception of Tether (USDT), all major stablecoin assets are retreating and stablecoin supply is experiencing a sustained decline. Due to the unusual calm both on and off the chain, the supply held by long-term holders reached an all-time high of 14.74 million BTC. Conversely, supply in the short-term group, which represents the more active part of the market, has fallen to its lowest levels since 2011. The group of long-term holders held their positions firmly, and there was almost no outflow of assets. Short-term holders are hovering on the edge of profit, and most of the digital assets they hold were purchased above the current price range. Digital asset markets have experienced volatility compression and unusually low trading volumes, and have now fallen back into extremely narrow trading ranges.

(4) Bitcoin spot ETF progress

The loudest and most important story in the cryptocurrency market this year was the filing for a Bitcoin ETF by BlackRock, the world’s largest asset manager. The main beneficiary of this news was Bitcoin, which saw significant growth and set a new all-time high for 2023. As the world's largest asset manager, BlackRock is subject to intense scrutiny and only makes decisions after careful consideration. Even amid regulatory fog and the current market environment, BlackRock's choice to continue to increase its investment in the digital asset industry can be considered a signal to investors that cryptocurrency is a legitimate asset class with a lasting future. Second, ETFs will increase exposure to and demand for this asset class faster than most expect. The latest news is that a U.S. Court of Appeals sided with Grayscale in last year’s lawsuit against the SEC for rejecting its application for a spot Bitcoin ETF. This greatly increases the chances that spot Bitcoin ETF applications from companies like BlackRock, Fidelity and others will be approved, possibly as early as mid-October. Notable among them is the Grayscale Bitcoin Trust, which has become significantly less undervalued relative to AUM and has seen strong price appreciation for its token (GBTC).

(5) Liquidity staking continues to grow after the upgrade of Ethereum

In April this year, Ethereum underwent a major update called the Shanghai Upgrade (EIP-4895). The update allowed Ethereum stackers to withdraw their rewards and staked tokens, leading to rather unexpected consequences. Contrary to many people’s expectations, Ethereum’s staked ratio continues to rise even after withdrawals.

The liquid staking protocol has shown good performance, with both price and total value locked (TVL) climbing in the first few weeks of Q2. The LSD protocol group currently holds the top spot in the crypto market in terms of TVL. The situation on the chain is also interesting. Following last September’s merger, Ethereum is no longer a continuously inflationary currency. Its supply now depends on activity on the network. The recent surge in network activity has tested the deflationary nature of ETH during periods of high activity, further demonstrating the long-term benefits of transitioning to PoS.

(6) Decline in public and private fundraising

In the first half of 2023, the token sales market recovered. Compared with the second half of last year, the market has been rising and shining brightly. However, there is still a big gap from the peak figure in 2021, which is only equivalent to 30% of the same period in 2019.

4.3.2 Crypto market and industry development in 2019

2019 was the year that the crypto-asset industry gradually recovered from the downturn of the bubble burst, and it was also the year that the industry transitioned from primary market investment to secondary market trading style. Driven by the IEO model, the primary market experienced a brief boom in the first half of the year, and topics such as DeFi and stablecoins continued to ferment. With the start of Bitcoin's main rise, the trading attributes of crypto assets have begun to highlight, compliant exchanges have entered the game, and the development of financial derivatives has once again aroused the hype of participants. The cyclical rotation of the global macro-economy resonates with the crypto-asset halving cycle. Geopolitics and de-globalization processes have caused the hedging attributes and risky asset attributes of crypto-assets to overlap with each other.

(1) Market value increased by 44.1%

In 2019, the cryptocurrency market first rose and then fell, with the market value increasing from US$120 billion at the beginning of the year to US$180 billion at the end of the year, an increase of 44.1% throughout the year. The best-performing asset in 2019 was Bitcoin, with annual gains of 95%, far outpacing the S&P 500’s 29%, gold’s 19%, and silver’s 16%. Bitcoin’s market capitalization share rebounded to 71.5%. Among the top five currencies by market capitalization, Bitcoin performed best, with a 95% increase in 2019. The remaining four currencies experienced increases respectively: ETH (-2%), XRP (-45%), BCH (%38%), and LTC (+37%). The average increase of the top five currencies by market capitalization is approximately 20.6%.

(2) Cryptocurrency derivatives are developing rapidly

In 2019, cryptocurrency derivatives exploded. The number of derivatives exchanges has increased 12 times, with many spot players joining the derivatives market, such as Binance, Kraken, and Bitflyer. Spot exchanges increased by 130, from 270 at the beginning of 2019 to 400 at the end of the year. BTC perpetual swaps are the most popular product among derivatives trading, with BitMEX leading the way (52% share).

(3) USDT maintains advantage

In 2019, only USDT's proportion increased. The other four of the top five stablecoins, such as USDC, PAX, TUSD, and DAI, saw their market capitalization proportions decrease. Among them, TUSD's market capitalization proportion dropped the most and was surpassed by PAX. GUSD even dropped out of the top five stablecoins.

(4) Investment and financing are bleak, and IEO has become the only bright spot

Judging from the number of projects financed in the primary market, the number of IEO projects in 2019 is far smaller than the number of projects when the ICO broke out in 2017, and is a local hotspot. According to Cryptorank data, the number of IEOs in 2018-2019 was only 97, and the maximum monthly financing amount was 37.6 million USD, which was far lower than the financing data during the ICO peak period in 2017.

(5) DeFi leads the blockchain implementation scene, and the value locked in the entire network reaches a record high

In 2019, the locked value of DeFi increased from approximately 200M USD to a maximum of 700M USD, a growth rate of 350%. The top three DeFi applications in terms of market share are Maker, Synthetix and Compound, with Maker’s market share accounting for nearly 50%. With the launch of Maker's MCD function, its market share is expected to reach a new high.

(6) Bitcoin ETF has been repeatedly rejected

Although U.S. regulators have been leaving room for future approval of Bitcoin ETFs, every application for a Bitcoin ETF has been rejected. In October, an ETF trading plan jointly submitted by Bitwise Asset Management and NYSE Arca was rejected by the U.S. Securities and Exchange Commission (SEC) on the grounds that the proposal did not meet legal requirements to prevent market manipulation and other illegal activities. The intensifying Sino-US trade war in 2019 has restored investor confidence in cryptocurrencies such as Bitcoin, but the U.S. Securities and Exchange Commission remains stubborn and refuses any listing application for a Bitcoin exchange-traded fund.

summary:

From the perspective of crypto market and industry development, the performance of the cryptocurrency primary and secondary markets in 2023 (since the beginning of the year), including market value, trading activities, investment and financing, is generally weaker than that in 2019. What shows more potential in 2023 is that the application environment and approval progress of Bitcoin ETFs are significantly better than in 2019; in addition, Ethereum has grown into the world's largest blockchain platform through major upgrades and iterations, and its future development potential is still unlimited. .

4.3.3 Deduction

Facing the intertwined scenarios of the “halving market” in 2024 and the current high-interest macro environment, crypto-asset development opportunities and challenges coexist. Past experience tells us that monetary policy and liquidity are the dominant factors affecting the cryptocurrency market, and industry fundamentals determine the height and length of the market. Taking into account the current macro environment and industry development, if the historical price of Bitcoin is synthesized into a conceptual trend, it will look like this:

(1) Market forecast for 2023:

The proportion of long-term holders is high, liquidity is tight (interest rates are high and the pace of interest rate hikes has not reversed) and the industry lacks a new narrative (ETF approval is expected to be closer to the end of the year). The market is still on the eve of the halving cycle, and the whole year of 2023 Prices will maintain wide fluctuations, and there is a high probability that there will not be a bull market;

(2) 2024-2025 Bull Market Deduction:

The macro environment in 2023 will not be as good as that in 2019, but as inflation slows down and various economic indicators achieve their goals, the improvement in the macro interest rate environment in 2024-2025 is still worth looking forward to (slowing, stopping and starting of interest rate cuts). When the Federal Reserve adjusts its monetary When policies, especially interest rate cuts, are adopted, the market usually has more capital inflows; as the total market value of Bitcoin gradually increases, its price increase seems to be gradually decreasing, and the increase multiples gradually decrease after the first three halvings. Consider large majors. Investment institutions are beginning to get involved in the Bitcoin market. They not only invest in Bitcoin, but may also promote the creation of more cryptocurrency derivatives. These derivatives are often designed for arbitrage by institutional investors. In this way, Bitcoin’s price volatility may be suppressed. Based on these factors, it is expected that the halving market will still come as scheduled, but the increase multiple will be lower than the previous three times, and it is speculated that the increase will be in the 2-3 times range; in terms of time, the most pessimistic expectation in the industry is to cut interest rates by the end of next year, and the optimistic An interest rate cut is expected in the second quarter of next year. From the start of interest rate cuts to when M2 reaches its peak, the bull market cycle should be pushed back again. It may not be like the trend of the bull market in the fourth quarter of 2020. The current probability is that it will occur in 2025. The degree of recovery in liquidity and the impact of the new industry narrative will be important factors affecting the increase. The industry expects that the approval and listing of ETFs will bring in huge amounts of funds. However, compared with the magnificent bull market environment promoted by the loose liquidity in 2020-2021 and the vigorous development of DEFI, the market environment in 2024-2025 is currently insufficient. It is speculated that The probability of a huge rise is relatively low;

(3) Risk factors

A bullish market requires unexpected benefits, which are reflected in abundant capital inflows, unexpected interest rate cuts, loose regulatory approvals, and major innovations in the industry. These will all be factors that contribute to a super bullish market. But on the other hand, black swan events are often unpredictable. No one could have predicted the occurrence of the COVID-19 epidemic that would sweep the world in 2020. Moreover, the global bailout was basically accompanied by a financial crisis or a major economic recession, and the volatility of risk assets It usually increases, and risks and opportunities coexist - the darkness before dawn is often the most difficult stage.

5. A new narrative—the tipping point of the bull market

When everything is ready, all we need is the east wind.

5.1 2017 Bull Market

In January 2017, the price of Bitcoin was around $1,000, when several news reports indicated that the Bitcoin market was growing rapidly, attracting some early investors. From April to June, the price of Bitcoin rose significantly, from $1,000 to about $2,500. More investors began to feel the potential of the cryptocurrency market, and more people began to invest in Bitcoin. By the summer, more media coverage and attention made the Bitcoin market more famous, and the price of Bitcoin rose from $2,500 to about $5,000. Starting in October, Bitcoin futures contracts were officially launched on the Chicago Mercantile Exchange (CME) and the Chicago Board Options Exchange. (CBOE), making it easier for institutional investors to enter the cryptocurrency market. Bitcoin prices surged in the fourth quarter, eventually surpassing a high of $19,000 in December.

Bull market attribution:

Media reports and publicity: Bitcoin has been the focus of media attention throughout 2017. Various news reports and interviews have promoted Bitcoin’s popularity, thus triggering more people to invest.

Institutional investment: CME Group and Chicago Board Options Exchange have launched Bitcoin futures contracts, providing a more formal way for institutional investors so that some large financial institutions can invest in Bitcoin more easily.

Development of new tracks: Ethereum experienced rapid development in 2017 and became the main platform for decentralized applications and smart contracts. Ethereum’s ICO wave also reached its peak this year, with many new tokens issued through Ethereum’s smart contracts.

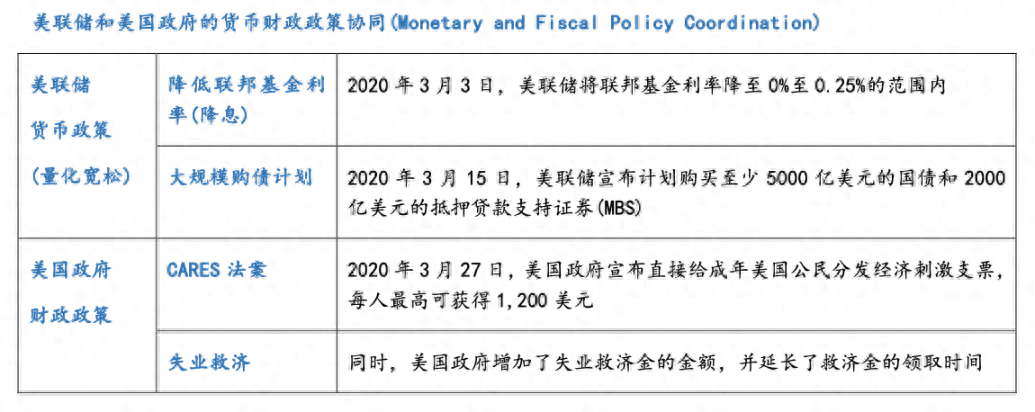

5.2 2020-2021 Bull Market

In January 2020, the price of Bitcoin was around $9,000 and the market was relatively stable. But at that time, the global outbreak of the new coronavirus caused a severe impact on the global economy. In response to the recession and turmoil in financial markets, the Federal Reserve embarked on a massive quantitative easing policy in March and April to stimulate the economy. Quantitative easing policies are often accompanied by rising inflation, and investors' concerns about inflation have led them to seek safe-haven assets. Some investors view Bitcoin as a hedge against inflation and have moved large amounts of assets into the cryptocurrency market to preserve their value. Bitcoin began to rise significantly in May, surpassing $10,000, driven by quantitative easing. From June to October, Bitcoin not only attracted the attention of individual investors, but also attracted widespread attention from large financial institutions. For example, US business intelligence company MicroStrategy announced in August that it had purchased more than $250 million in Bitcoin; online payment giant PayPal announced that it would allow users to buy, sell and hold Bitcoin on its platform; Goldman Sachs began to provide Bitcoin trading and settlement services , allowing its clients to trade crypto assets; Morgan Stanley announced that it will provide its clients with investment opportunities in Bitcoin funds. Since then, the price of Bitcoin has been soaring, breaking through $20,000 in November; $30,000 in December; $40,000 in January of the following year; and $60,000 in March.

Bull market attribution:

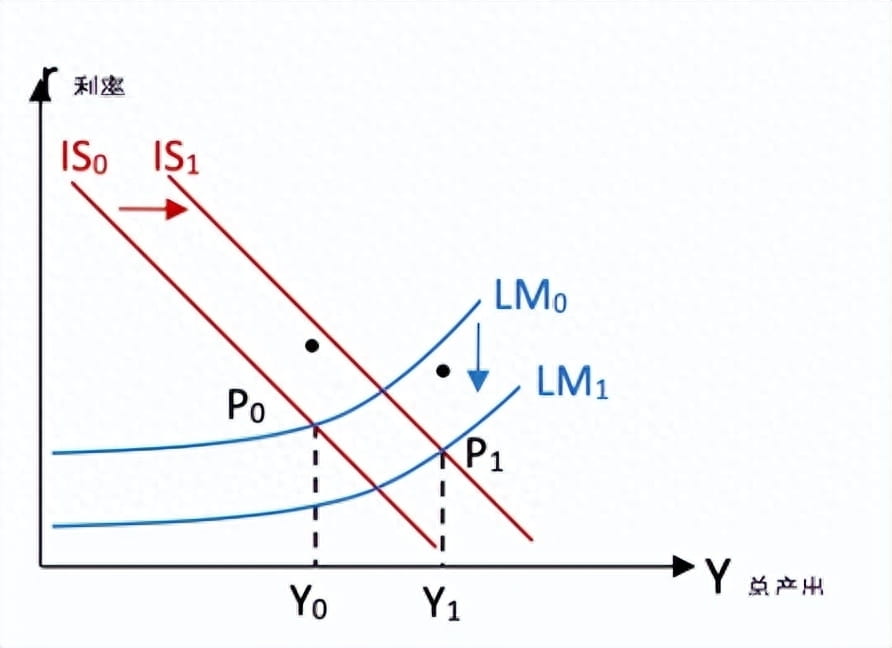

LM curve: L2 (r) = L1 (Y) - M/P, where M represents the money supply and P represents the price level. Lowering the federal funds rate means lowering the cost of loans, which will stimulate a large amount of money to be borrowed for investment; large-scale purchases of government bonds and MBS will significantly increase the money supply. Both will increase the value of M, causing the LM curve to shift downward.

IS Curve: Y = I (r) + G + (X – M), where G represents government spending. Massive checks and relief payments will increase government spending, increase G, and shift the IS curve to the right.

Result: The new equilibrium point P1 is reached, the corresponding total output Y1 > Y0, the total output increases significantly, economic activities are extremely active, consumption and investment are stimulated, and currency prices rise rapidly.

Institutional investment surges: 2020-2021 saw significantly higher participation from institutional investors compared to the 2017 bull run. In addition to the above-mentioned MicroStrategy, PayPal, Goldman Sachs, and Morgan Stanley, many other large financial institutions have also successively announced their involvement in cryptocurrency investments.

Diversification of cryptocurrency projects: Compared with 2017, 2021 has witnessed a more diversified trend in cryptocurrency, which is reflected in the emergence of a large number of new tokens and digital asset projects, enriching the digital asset ecosystem. It not only attracts some celebrities to enter cryptocurrency, but also promotes greater diversification of capital in the cryptocurrency market, which is conducive to the further development of the cryptocurrency industry. include:

New blockchain platforms: In addition to Bitcoin and Ethereum, 2021 has seen the rise of some new blockchain platforms, which provide infrastructure for different tokens and applications, such as Solana, AVAX, etc.

DeFi Tokens: DeFi is a hot trend in 2021, attracting a lot of funding and projects. DeFi tokens provide users with various financial services, including lending, staking, and liquidity mining, such as Uniswap, AAVE, etc.

NFT Tokens: NFTs have experienced explosive growth in 2021, attracting artists, media companies, and collectors. NFT tokens represent unique digital assets, such as Sandbox and more.

Social Tokens: There are a number of new social tokens emerging in 2021 that are tied to social media and content creators. These tokens can be used to reward and support the creator's fans, as well as promote social interaction, such as SOC, BAT, etc.

Chain gaming tokens: The gaming ecosystem on the blockchain is also growing in 2021, and some gaming tokens led by AXS have become popular digital assets for transactions in the virtual world and in-game incentives.

5.3 Factors driving the subsequent bull market

Interest rate cut: Currently, the U.S. inflation rate is still hovering near 3%. The Fed’s official hard requirement for the inflation rate is 2%, and Powell and other Fed officials have repeatedly stated that changing the inflation target is unlikely. So the timing of a rate cut depends largely on when U.S. inflation returns to 2%. But even if interest rates are cut, it is likely that the entire interest rate reduction cycle will take 2-3 years to complete. During the interest rate reduction cycle, currency prices may rise step by step. According to current data, interest rate cuts are expected to begin in the fall and winter of 2024.

U.S. presidential election: A new round of U.S. presidential election will be held at the end of 2024. Different presidents will implement slightly different economic policies. During Trump's administration, he repeatedly adopted expansionary fiscal policies to stimulate the economy, such as massive reductions in corporate income taxes and financial tax reforms. He also publicly criticized Federal Reserve Chairman Powell on many occasions, urging him to lower interest rates and implement quantitative easing policies. During Biden's administration, although he also allocated funds to support the construction of infrastructure, energy, medical and other fields, overall he was still conservative. It is expected that if Trump is elected, the cryptocurrency bull market will come faster. Even though Trump often criticizes the cryptocurrency industry, a recently disclosed financial report shows that Trump holds more than $2.8 million in Ethereum in a wallet and also made a profit of 490 from an NFT licensing agreement. Ten thousand U.S. dollars.

The cryptocurrency regulatory system is more mature: In the first half of 2023, the United States, Europe, Hong Kong, Singapore, Japan and South Korea began to establish regional cryptocurrency regulatory policies. As supervision becomes more stringent, laws become more mature, and transactions become more transparent, cryptocurrency may gradually get rid of its negative labels such as "unsafe" and "money laundering tool", thereby attracting large financial institutions to feel more confident about cryptocurrency and attracting larger amounts of funds. field. It is expected that 2024 will still be a year of rapid development of the regulatory system, and a relatively mature system will be formed in 2025.

Cryptocurrency projects are more diversified: It is expected that the next round of bull market cryptocurrency will show a more diversified trend, including token diversification, ecosystem diversification, and financial product diversification; among them, token diversification includes emerging AI tokens, Tokens (PYUSD) launched by large companies, etc., ecosystem diversification including decentralized e-commerce based on Web3, the emergence of decentralized data storage, etc., and financial product diversification including upcoming ETF funds, etc.

6. Write at the end

Cryptocurrency has experienced three spectacular bull and bear cycles, and Bitcoin also exceeded $1 trillion for the first time in 2021. This will mark the event when cryptocurrency becomes one of the world’s mainstream alternative assets. In a new bull-bear cycle, Bitcoin’s gains will also be limited by its huge asset size, and we expect the high to be around $120,000. From then on, when the pie of crypto assets forms a stable pattern and division on a global scale, the probability of an epic bull market will become smaller and smaller.

I am Brother Ming. I have been in the trading market for more than ten years. If you have any questions, you can talk to Brother Ming. Choice is greater than hard work. The circle determines your destiny!