Binance Research: Half-Year Report Highlights (H1 2023)

Main Takeaways

Binance Research publishes comprehensive half-yearly reports on the state of crypto – milestones to help our users navigate the dynamic world of digital assets.

This article in our Binance Research blog series previews their latest half-year report on H1 2023, examining major developments from January 1 to June 30 of this year.

These past six months have been challenging, marked by regulatory scrutiny and macroeconomic uncertainty. Nevertheless, crypto markets have shown growth and resilience overall, ending the half-year period on a positive note.

Thanks to Binance Research, you can take advantage of industry-grade analysis of the processes that shape Web3. By sharing these insights, we hope to empower our community with the latest knowledge from the field of crypto research. For a deeper dive, the full reports are available on the Binance Research website.

The first half of 2023 was a turbulent period for the maturing crypto industry. We witnessed the intensification of both regulatory scrutiny and institutional adoption. Despite 2023’s challenges thus far, the industry has shown resilience, with total crypto market capitalization growing over the last six months.

Crypto is a rapidly evolving industry, which necessitates periodic examination of the most significant market developments. Crypto markets hit a peak in late 2021, and we are now approaching the two-year mark since then. In light of this milestone, it is timely to take a step back and examine the state of the markets and key developments that have unfolded in various sectors of the Web3 space.

Today, we will examine highlights from Binance Research’s half-year report for H1 2023. In broad strokes, we will explore the landscape of major crypto and Web3 sectors, including layer-1 and layer-2 solutions, stablecoins, decentralized finance, non-fungible tokens, gaming, and institutional adoption.

The Past Year in Crypto

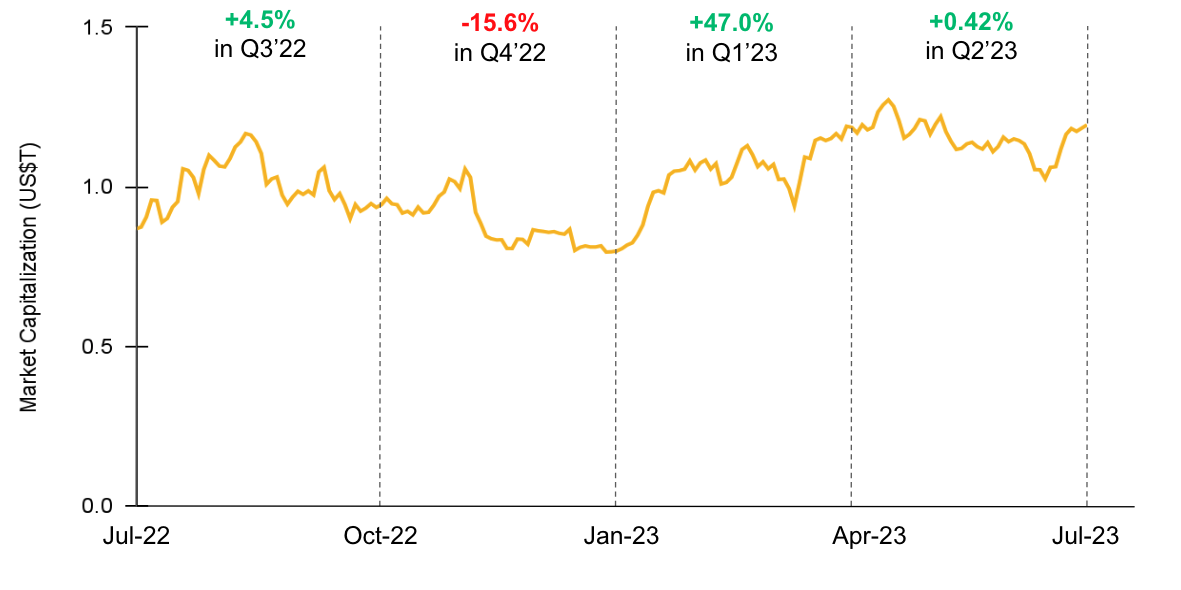

Looking broadly at crypto markets over the past year, H1 2023 was marked by recovery compared to the weaker performance of H2 2022.

Crypto market capitalization over the past year

Source: Coinmarketcap, Binance Research (June 30, 2023)

Closing at $1.17T on June 30, 2023, the total crypto market capitalization rose 30.3% from $0.90T a year ago. Despite ongoing macroeconomic uncertainties, the industry has enjoyed considerable upswings, with a 47% growth in Q1. Overall, the total crypto market capitalization has grown 47.6% since the start of 2023.

The Layer-1 Landscape

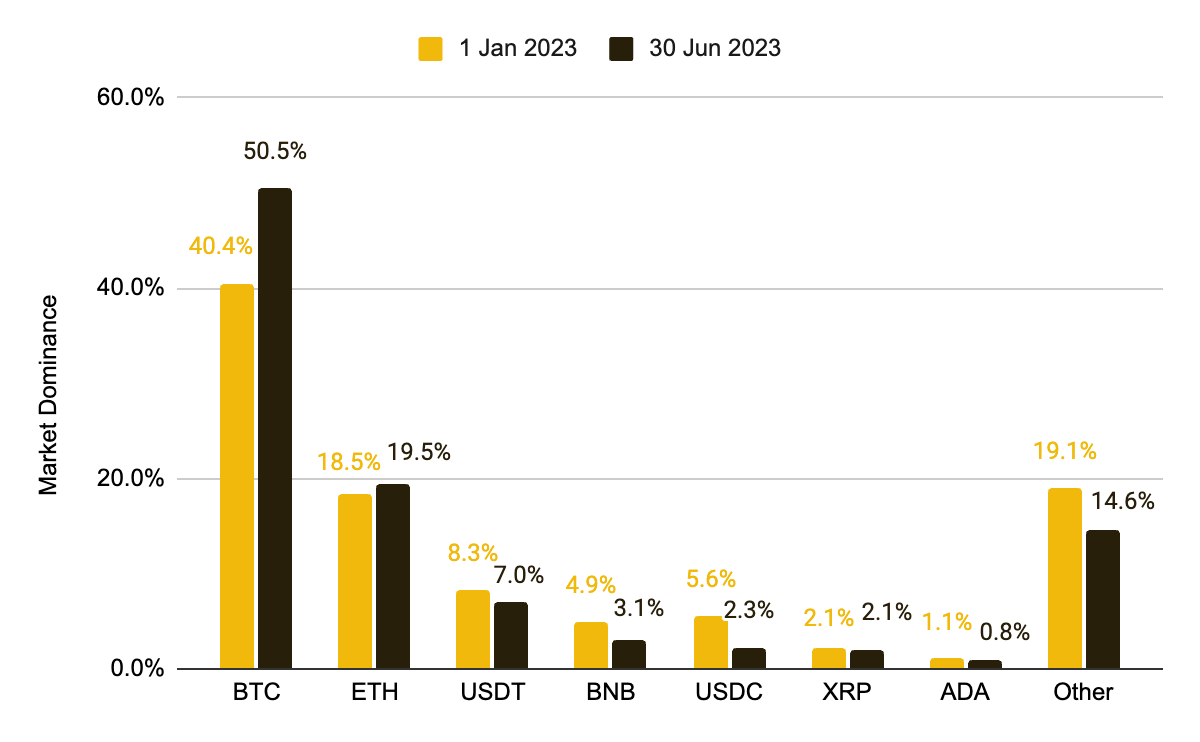

Bitcoin dominated the layer-1 (L1) landscape in the first half of the year. Driven by technological developments, including the advent of ordinals, the Bitcoin ecosystem has witnessed a resurgence in energy and excitement, with on-chain metrics indicating positive market sentiment and increased user engagement. Throughout H1 2023, the crypto pioneer has regained a majority market share, increasing its dominance from 40.4% to 50.5%.

L1 landscape by market dominance in H1 2023

Apart from ETH and XRP, which showed slight increases in market dominance, the majority of other top cryptocurrency assets declined. Combining this with the fact that the overall crypto market capitalization grew across H1 2023, it could indicate that money moved from alternative assets into BTC.

While Bitcoin has had an eventful start to the year, the other major L1s have also been innovating at a rapid pace. Financial metrics show that Ethereum remains the leading L1 network behind Bitcoin, beating the others in market capitalization, trading volume, and revenue generation by a considerable margin.

The Layer-2 World

The layer-2 (L2) sector has experienced multiple strong points over the last year and touched new heights in 2023. Focusing on Ethereum’s L2 scaling solutions, a number of high-quality projects are now fully functioning below the base L1 chain. While optimistic rollups have retained their market dominance, zero-knowledge (ZK) competitors are catching up fast.

Metrics of major L2s in H1 2023

Source: l2beat.com, l2fees.info, Binance Research (July 5, 2023)

Stablecoins

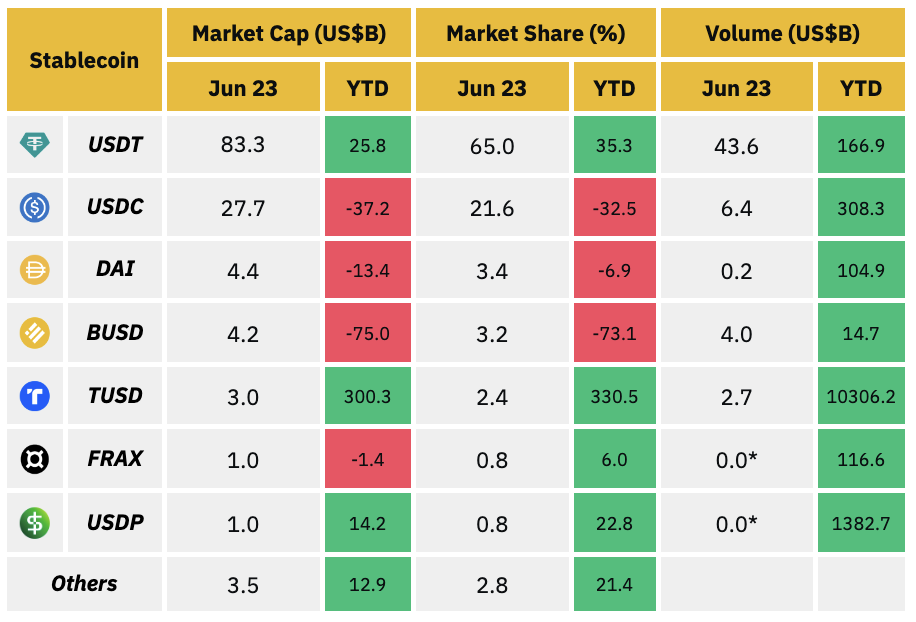

The stablecoin market contracted this year, largely due to a shifting regulatory landscape. Despite a modest decline of 7.0% since the start of 2023, the stablecoin sector retains a total market capitalization of $128.1B.

The global stablecoin market saw a downward trajectory in H1 2023

Source: DeFiLlama, Binance Research (June 30, 2023)

In this competitive landscape, centralized stablecoins remain dominant, comprising over 90% of the overall market. In particular, Tether’s USDT has consolidated its market position amid the decreasing stablecoin market value, primarily at the expense of other competitors.

Metrics of major stablecoins by the end of H1 2023

Source: CoinMarketCap, DeFiLlama, Binance Research (June 30, 2023)

Decentralized Finance

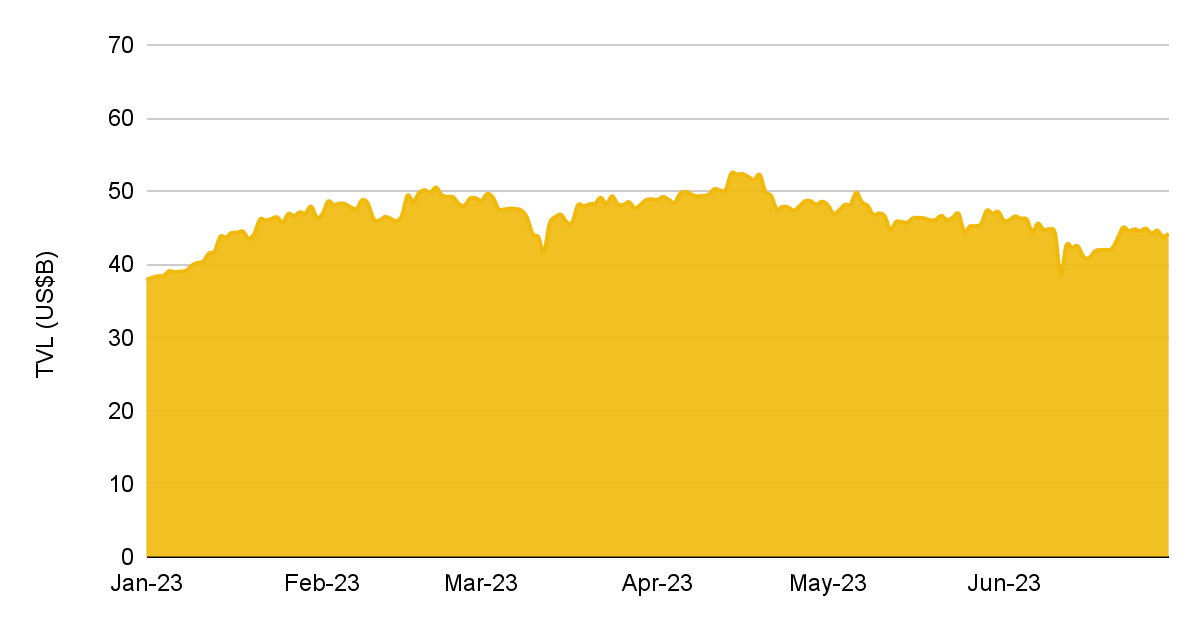

Despite a mixed 2022, decentralized finance (DeFi) has seen steady growth in 2023. Since the start of the year, the total value locked (TVL) in DeFi increased 16.7% to $44.2B. Today, DeFi is embedded throughout the entirety of the crypto industry. Though still in its early stages, DeFi is projected to reach a revenue milestone of $231.2B by 2030.

DeFi TVL grew 16.7% in H1 2023

Note: The DeFi TVL considered in this figure excludes liquid staking.

Source: DeFiLlama, Binance Research (June 30, 2023)

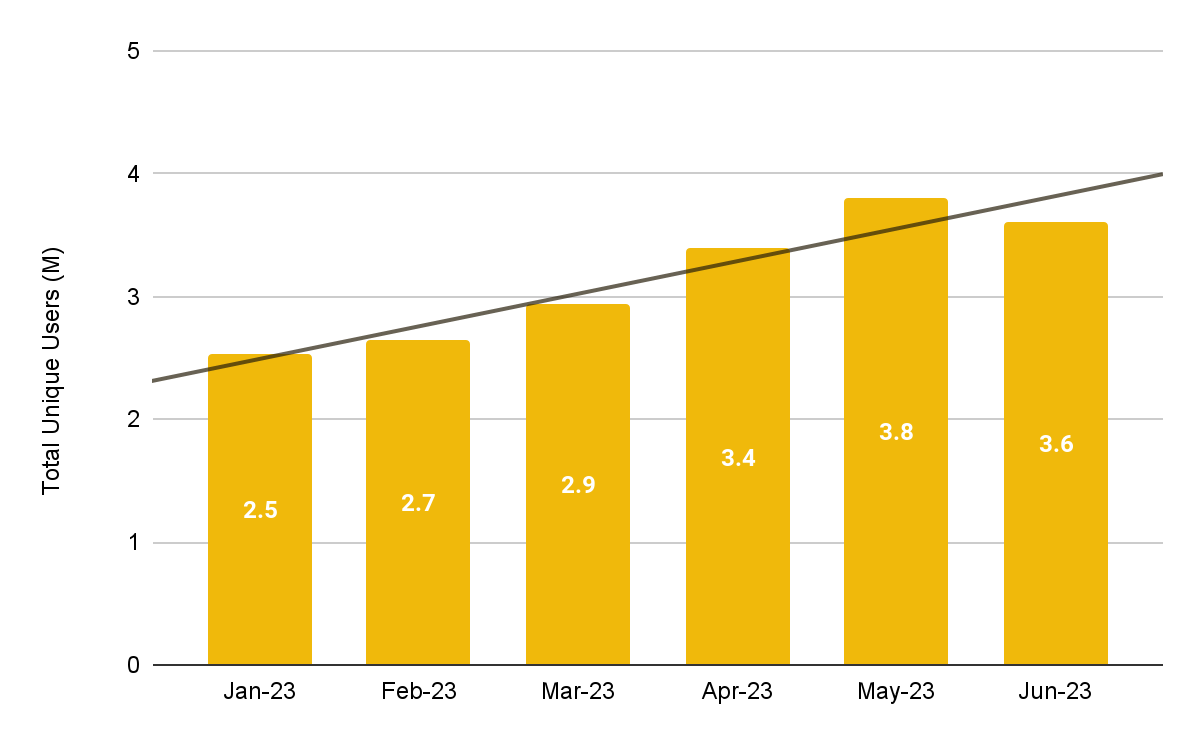

DeFi products continue to attract a significant number of users, with transaction activity painting a promising picture. The trend for this year has shown a positive shift in user engagement for DeFi protocols, with the number of unique monthly users climbing 42.5% from an average of 2.5M to 3.6M.

Number of unique monthly users across all DeFi protocols in H1 2023

Non-Fungible Tokens

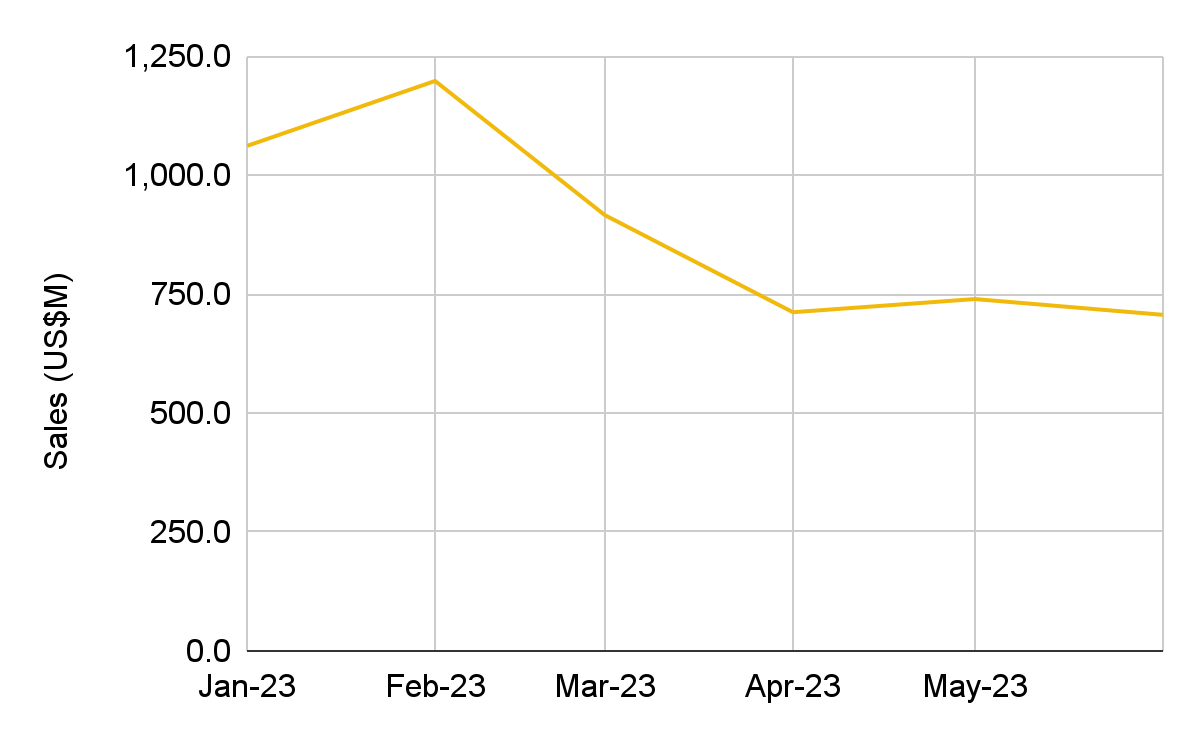

Non-fungible tokens (NFTs) have had a challenging year thus far. Sales peaked in February 2023 before seeing a general decline over the next few months. NFTs recorded $5.3B in sales volume in the first half of 2023, representing a decrease of 75.9% since the previous year.

Monthly NFT sales in H1 2023

Source: CryptoSlam, Binance Research (June 30, 2023)

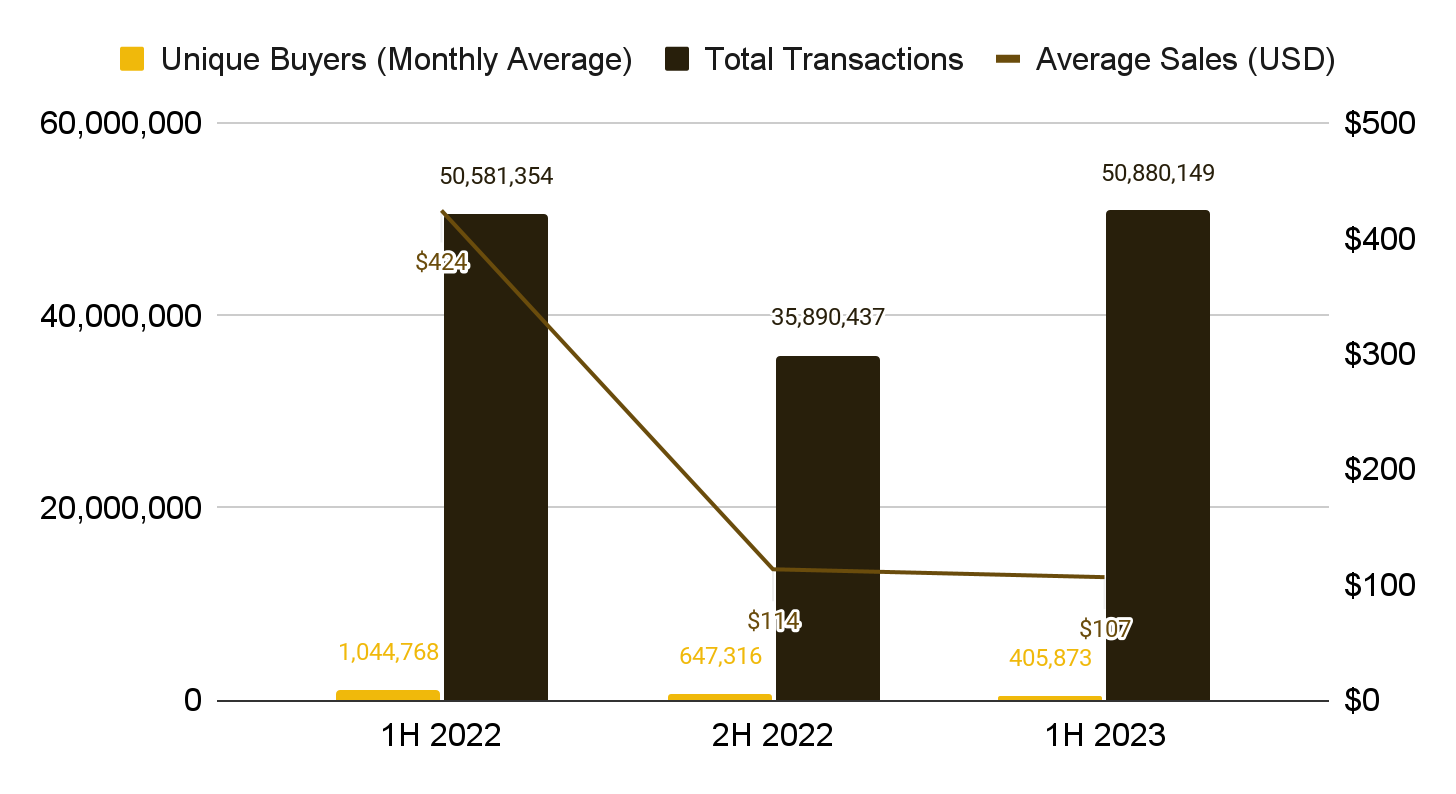

The sharp fall in NFT sales over the last year was accompanied by a 74.9% decline in average NFT sale prices. Nonetheless, some underlying metrics have improved. Specifically, transaction volume has increased, with the total number of transactions on a yearly and half-yearly basis being 0.6% and 41.8% higher, respectively.

Total transactions and the number of unique buyers rebounded in H1 2023

Source: CryptoSlam, Binance Research (June 30, 2023)

Gaming

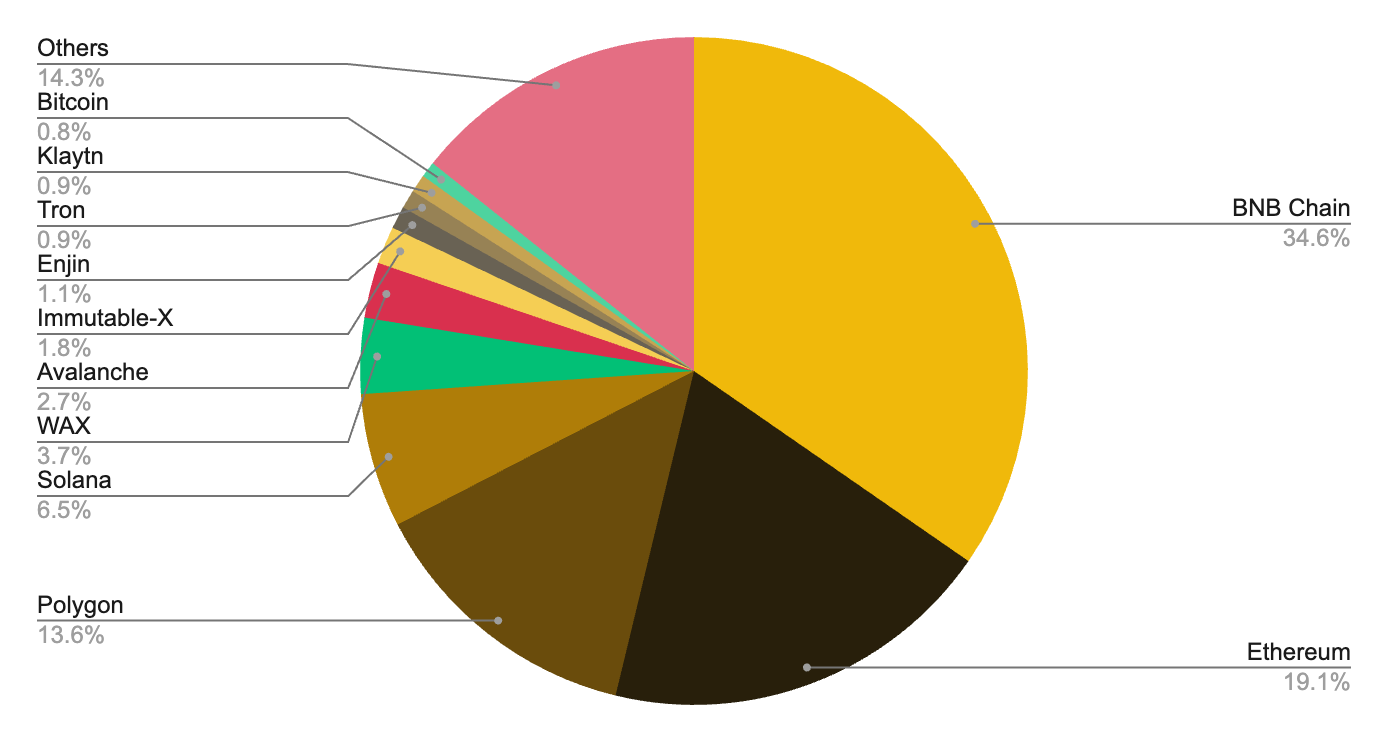

Compared to the excitement of previous years, retail interest in gaming and Metaverse sectors has been significantly lower so far this year. Despite this, the market capitalization of gaming-related tokens has grown, and developers remain committed to building. In H1 2023, the gaming landscape was led by three major blockchains, with over 67% of games built on BNB Chain, Ethereum, and Polygon.

Composition of the blockchain gaming market in H1 2023

Source: PlaytoEarn.net (June 30, 2023)

The market capitalization for gaming-related tokens has increased 48% over the last year, ending the first half of 2023 at $12.1B. Gaming-related tokens have benefited from the broad-based recovery in the crypto market.

Market capitalization of gaming-related tokens in H1 2023

Source: Footprint Analytics - @shudu (June 30, 2023)

Institutional Adoption

Throughout 2023, blockchain innovations have increasingly attracted institutions from traditional finance (TradFi) as they embrace the technology. Many are exploring its potential benefits with increased experimentation and expanded accessibility.

CBDC pilots

Central banks have continued to launch and expand their pilot programs for central bank digital currencies (CBDCs) to enhance payment services and build a more integrated financial system. Major developments in this space have included the following:

China has made a significant push to roll out its digital yuan (e-CNY), including initiatives with public transport and salary payments.

Hong Kong announced its e-HKD pilot program in May as part of the city’s exploration of a possibility to implement a retail CBDC.

The Colombian central bank partnered with Ripple to leverage its CBDC platform for piloting use cases and improving its payment system.

The Bank of Japan has also joined the ranks of those unveiling their CBDC pilot projects, announcing in April its plan to test the use of a digital yen.

Thailand launched its retail CBDC pilot in June with three payment providers, aiming to involve up to 10,000 users in its regulatory sandbox through August.

Crypto accessibility

Traditional financial institutions have started offering the opportunity to trade cryptocurrency assets. Significant developments in this field included the following:

BlackRock, the world’s largest asset manager, filed for a spot Bitcoin exchange-traded fund (ETF) on June 15. If approved, Coinbase will serve as its custodian.

EDX Markets, a new digital assets exchange backed by prominent financial institutions such as Citadel Securities, Fidelity Investments, and Charles Schwab, was launched on June 20.

Germany’s DZ Bank announced plans to offer BTC trading in February. This was followed by the DWPBank in March, which launched its own platform.

The Chicago Board Options Exchange has been approved to provide access to digital assets by the Commodity and Futures Trading Commission (CFTC).

Previously only available to institutions, Fidelity Investments has released its Fidelity Crypto platform to enable BTC and ETH trading access for retail users.

Hong Kong’s Securities and Futures Commission implemented a new crypto licensing framework, with investors allowed to trade digital assets from June 1.

Closing Thoughts

H1 2023 in the digital-asset space was turbulent, with continued volatility against a fragile macroeconomic environment. Investors remain cautious, with increased regulatory scrutiny of crypto firms contributing to uncertainty in the market. Projects are also feeling pressured as activity slows and funding runs out.

Despite these setbacks, we have witnessed unprecedented institutional adoption. The renewed push for spot Bitcoin ETFs has driven newfound momentum and boosted investor confidence. As we begin the second half of the year, we look forward to seeing further innovations, greater adoption, and an even brighter future for the world of Web3.

Binance Research

The Binance Research team is committed to delivering objective, independent, and comprehensive analyses of the crypto space. They publish insightful takes on Web3 topics, including but not limited to the crypto ecosystem, blockchain applications, and the latest market developments.

This article is only a brief snapshot of the full report, which features comprehensive analysis of crypto and Web3 sectors in H1 2023. The half-year report dives deeper into top layer-1 networks, such as Bitcoin, Ethereum, BNB Chain, Solana, and many more; layer-2 scaling solutions, encompassing optimistic and ZK-rollups; stablecoins, including an examination of the regulatory landscape and emerging models; DeFi innovations, such as liquid staking and decentralized exchanges (DEXs); NFTs, including ordinals, inscriptions, and BRC-20 tokens; gaming and the metaverse; and fundraising and institutional adoption.

With such an extensive scope of research, you won’t want to miss these exclusive insights. To read the full version of the report, click here. You can find other in-depth Web3 reports on the Insights & Analysis page of the Binance Research website. Don’t miss the opportunity to empower yourself with the latest insights from the field of crypto research!

Further Reading

General Disclosure: This material is prepared by Binance Research and is not intended to be relied upon as a forecast or investment advice and is not a recommendation, offer, or solicitation to buy or sell any securities or cryptocurrencies or to adopt any investment strategy. The use of terminology and the views expressed are intended to promote understanding and the responsible development of the sector and should not be interpreted as definitive legal views or those of Binance. The opinions expressed are as of the date shown above and are the opinions of the writer; they may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Binance Research to be reliable, are not necessarily all-inclusive, and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given, and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Binance. This material may contain ‘forward-looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. This material is intended for information purposes only and does not constitute investment advice or an offer or solicitation to purchase or sell in any securities, cryptocurrencies, or any investment strategy, nor shall any securities or cryptocurrency be offered or sold to any person in any jurisdiction in which an offer, solicitation, purchase, or sale would be unlawful under the laws of such jurisdiction. Investment involves risks.