Introduction

An all-time high rally at which Bitcoin approached 100,000 towards the middle of January, the biggest cryptocurrency by market valuation dropped to less than 70,000 at the end of January 2026. The fall undid weeks of gains and raised discussions as to whether the bull market is finished or is taking a break. The slide was caused by a combination of macroeconomic factors, liquidity shocks, investor psychology and geopolitical tensions. The article breaks down the forces behind the fall, the reaction in the market and evaluates the ability of the Bitcoin to maintain its peaks.

The ETF Boom and Bust

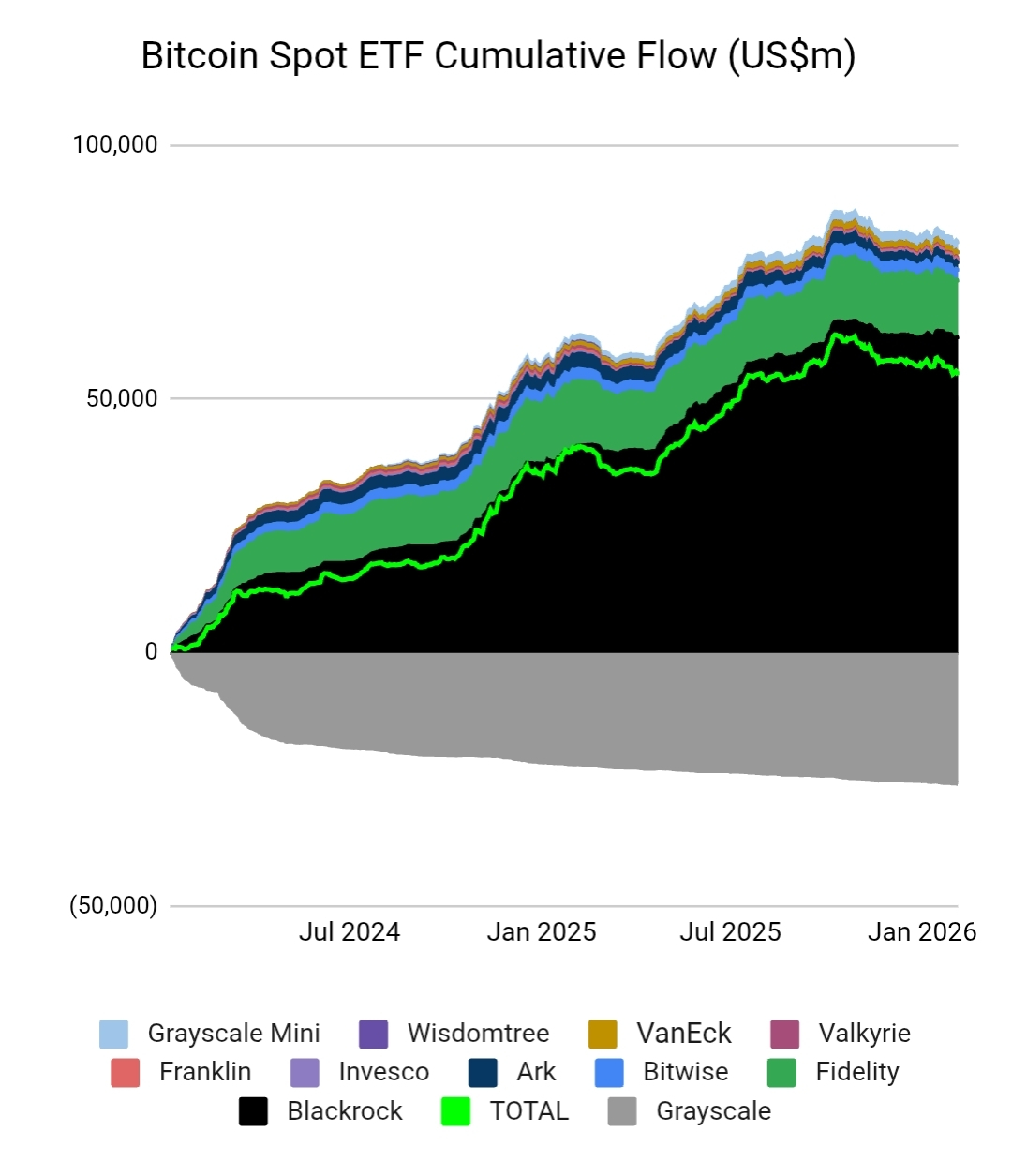

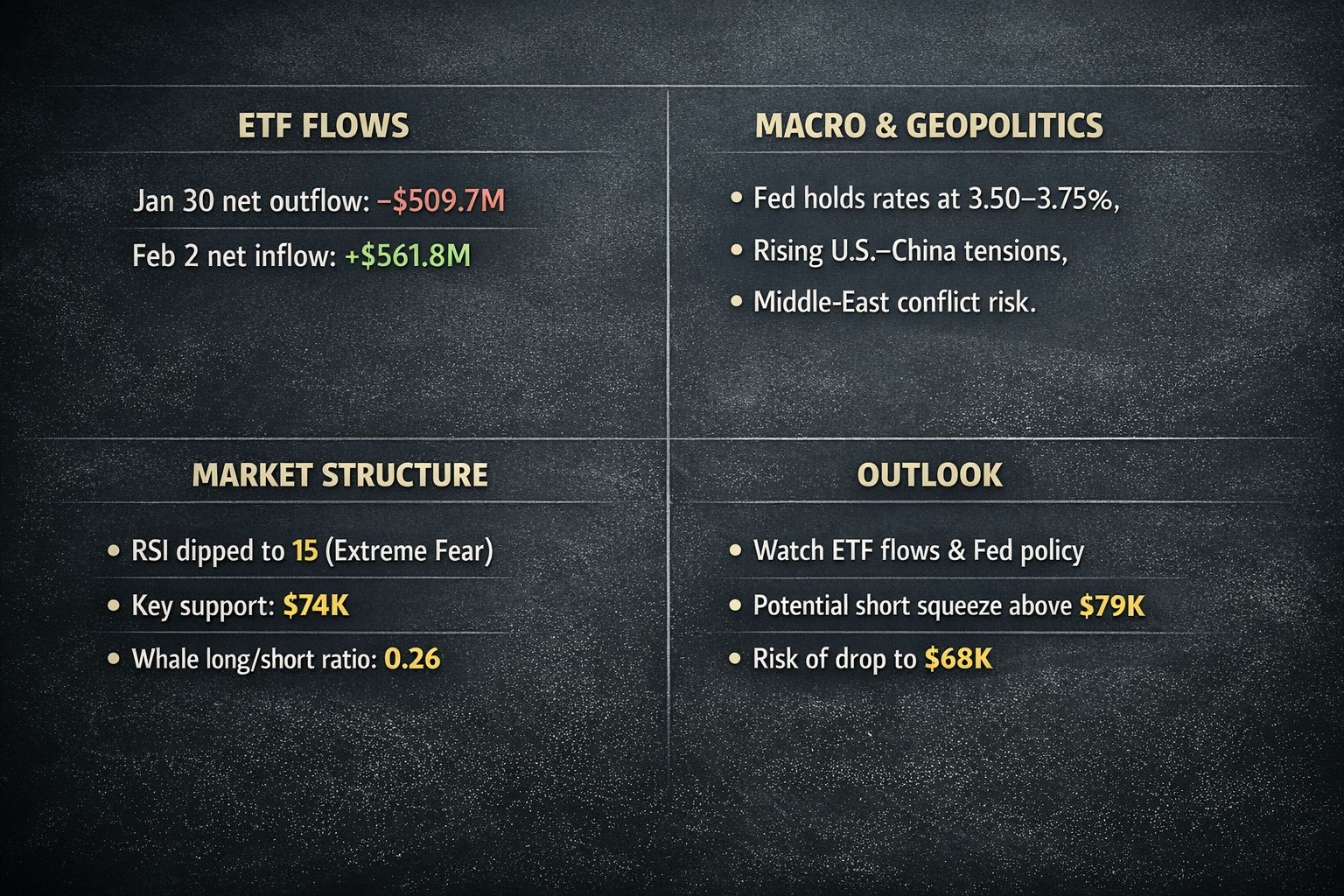

Whether the U.S. spot Bitcoin ETFs would roll out in November 2025 would have been a watershed moment. Due to the attraction of billions of products offered by BlackRock, Fidelity, Bitwise, Ark and others, demand increased. The premature flows spurred Bitcoin to new levels. There was a sharp reversal of flows towards the end of January, however. According to the information provided by Farside Investors, Bitcoin ETFs experienced net outflows of approximately 509.7 million dollars on 30 January 2026, with the majority of funds being withdrawn by BlackRocks iShares Bitcoin Trust (528.3 million dollars). Outflows were one of the sharpest daily declines since the launch and an indicator of declining investor confidence.

When the decline became a trend, panic was compounded. As early as early February, cumulative net outflows since November were of over 6 billion, the longest monthly period outflows in the history of the funds. Highly purchased institutional investors began selling to make losses and short-term traders jumped on the negative. After the fall, analysts observed that over 62 percent of ETF investors were under water, further putting pressure of sale to break even.

One bright spot was that net inflows returned to the tune of $561.8 million a day, according to the table of Farside 2 February daily flow. Large deposits into Fidelity FBTC and BlackRock IBIT indicated that some of the institutions were buying the dip. Nevertheless, such inflows never canceled out the past outflows and the market sentiment was weak.

Macro Headwinds: Rate Policy and Liquidity.

The monetary policy of U.S. again took centre stage. Inflation had moderated to the 2 percent target of the Federal Reserve by the end of 2025, but unemployment was creeping up and economic growth was slowing down. The Fed governors argued that rates should be reduced drastically in 2026 and those argued that the Fed should avoid cutting the rates too early, a step that would trigger inflation again. There was uncertainty on whether rates would remain higher than long prompting markets to be shaken.

Risk assets fell when the Fed maintained its target range of 3.50 -3.75 in January and suggested being cautious up to mid-2026. The correlation between Bitcoin and equities increased to 0.75, which indicates that the performance of S&P 500 or Nasdaq affected crypto more significantly. Increased rates decrease the liquidity on speculative assets, and risk-free returns become fairly appealing. Investors sold volatile positions and went to cash, money market funds or bonds.

Elsewhere, the central banks of Europe and Asia cautioned that financial situations may tighten further, lowering liquidity around the globe. The commodity supply shocks (especially gold and silver which dropped dramatically) were indications of a general unwinding of the speculative trades. The volatility index of the bond market has skyrocketed with the increase in yields of long-term treasury bonds, which damaged leveraged Holdings in crypto.

Geopolitical Tensions and Flight to Safety.

Late in January the situation of geopolitical risks increased. Negotiations between the Chinese and the U.S. on the issue of technology transfer ended. Iran and western powers were threatening each other by use of shipping lanes, and this caused fear of disruption of supply of energy. In the Middle East the situation escalated with proxy groups going on a collision course. In response, markets took a flight towards so-called safe havens, such as the U.S. dollar and short-term treasuries, and risky assets, such as Bitcoin, traded down. Bitcoin has been doublespeaked historically as the digital version of gold, but during the crisis tends to be positive-correlated with stocks, indicating that it is a high-beta asset instead of a safe-haven one.

The other reason was that India had decided to remove the tariffs on American products at the same time that the U.S had removed tariffs on Indian products. This trade deal marked a calming of global tensions at the expense of including provisions in which India had to stop purchasing Russian oil and promised to make half a trillion dollars of imports into the United States. On the one hand, the policy was beneficial to trade, but it put pressure on new currencies of the emerging markets that strengthened the dollar and burdened dollar-denominated assets such as Bitcoin.

Big Players: GameStop, Strategy and Whales.

Volatility was augmented by news surrounding major corporate players. The meme-stock hero GameStop announced that it would acquire a consumer size buyer in a high-impact deal. Other analysts guessed that GameStop could sell its Bitcoin reserves to fund the acquisition, but these rumors were never proved. Nonetheless, market confidence was burdened by the speculation.

Strategy (previously MicroStrategy) owned more than 190,000 bitcoins as of the end of 2025, although the average cost basis was close to $74,000. Another instance is when the company had a negative mark-to-market holding when Bitcoin fell to 74,500. CEO Michael Saylor restated his long-term bullishness and actually purchased more coins, although the market was concerned that additional crashes might compel him to sell more in order to cover leverage. The same happened to other corporates which have large BTC exposure.

Whale positioning data reflected approximately 596 large long positions and 1,245 large short positions and long to short ratio was approximately 0.26. The average entry prices of short sellers were close to 92753, and it implied that they were well into the profit. This disparity increased the downward movement since shorts increased positions. Contrarily, a short squeeze would be a possibility in the event that the price rebounds above the major levels of resistance since underwater shorts would be in a hurry to cover.

Technical Support Levels and Breakdown.

Even before the crash, technical analysts had indicated that there are some signs of warning. Bitcoin had been over its 100-day exponential moving average (EMA) and even close to its upper Bollinger band all of December and January. This stance signified overextensioning. With price holding at around the 98,000 mark, the Relative Strength Index (RSI) dropped to overbought to approximately 15 indicating the state of extreme fear and oversold. Stop-loss orders started to cascade into a liquidation as soon as Bitcoin fell below its major support at 79,000 USD. A bunch of clusters around the 74,000 area drove a large number of traders out of their positions which briefly put the price to test the 68,000 level.

Although the lower, the higher-low pattern of 2025 was still preserved in the long-term graphs. Support areas were found to be at 74000 and 68000, and the resistance is 79000 and 81000. In case the price is able to recover to an amount of an overall of all ETFs realized price to investors: that is, $86,600, sentiment would be significantly enhanced since all holders underwater will be out of the red.

Likelihoods: Backsliding or Increasing Pain?

Bitcoin will either go back above $70,000 or drop even further depending on a number of factors that are subject to change:

ETF Flows: The prices may stabilize with continued institutional inflows such as those experienced on 2 February. More volatility is expected in case outflows start back up.

1 - Macro Policy: The liquidity will be determined by the upcoming Fed decisions, inflation data and rate expectations. Reduction of rates or policy understanding would boost risk appetite.

2 - Geopolitics: The reduction in the risk-off pressure would be due to de-escalation of the world tension and a stable supply of energy. On the other hand, unforeseen wrangles may lead to additional sell-offs.

3 - Whale and Corporate Behavior: In case such large holders as Strategy or GameStop sell, the market might revisit lows. Conversely, conviction by whales may lead to a short squeeze.

4 - Expansive Crypto Trends: Investor sentiment will be impacted by the performance of the Altcoins, the development of DeFi and regulatory transparency (particularly amid the new administration following the 2024 election in the U.S.).

Summary: The Death of Simple Risk.

The decline to below 70,000 was a cold shock that the Bitcoin journey is unstable, especially when it attracts the mainstream financial system in the form of ETFs. There is an ebb and flow of liquidity as institutions either put in or take out capital. All of the macro headwinds, geopolitics, corporate movements and technical dynamics are interconnected.

These episodes are points of entry to long-term believers. To traders, structured risk management in crucial support levels is critical. Most importantly, the crash is a reminder that the age of easy risk in crypto has ended, future rallies are probably going to be more scrutinized, volatility will increase and structural repricing will grow slower. The only way not to lose direction in the future is to understand the motivations of the movements of the market.