Most blockchain projects explain themselves through technology specifications and promise to solve problems that sound important in whitepapers. Plasma reversed this narrative by starting with straightforward economic observation that Tether generates thirteen billion dollars annually from Treasury yields backing its one hundred seventy-two billion dollar stablecoin supply but captures almost nothing from the trillions of dollars in daily USDT transactions flowing across competing blockchains. The project emerged not as idealistic decentralization experiment but as calculated strategic move by parties with enormous vested interest in redirecting stablecoin transaction value into infrastructure they control. I’m describing deliberate vertical integration disguised as community blockchain project.

The October 2024 friends and family round raising three point five million dollars from Bitfinex and select investors signaled what would become transparent throughout Plasma’s development. The company behind this round was iFinex Incorporated which owns both Bitfinex exchange and Tether stablecoin issuer creating organizational structure where strategic investor and primary product beneficiary are essentially same entity. The February 2025 Series A raising twenty to twenty-four million dollars led by Framework Ventures made the strategic backing even clearer with Paolo Ardoino participating as both institutional investor through his Bitfinex role and personal angel investor while simultaneously serving as CEO of Tether.

The Investor Network Revealing Institutional Confidence

The presence of Peter Thiel through Founders Fund investment in May 2025 added significant credibility signal beyond crypto-native investors. Thiel cofounded PayPal and demonstrated track record identifying infrastructure plays that reshape how money moves. His participation suggested belief that stablecoin-optimized blockchain represents genuine innovation rather than incremental improvement on existing chains. They’re betting that purpose-built infrastructure for specific use case outcompetes general-purpose platforms trying to serve everyone.

The involvement of Christian Angermayer as Plasma cofounder creates additional connection point to Tether ecosystem. Angermayer manages Tether’s profit reinvestment through Apeiron Investment Group meaning he orchestrates how Tether deploys its billions in annual earnings into various projects and ventures. The overlapping relationships between Plasma leadership, Tether management, Bitfinex operations, and profit deployment create interconnected network where distinguishing independent blockchain project from Tether subsidiary becomes increasingly difficult. If it becomes that Plasma succeeds in capturing significant stablecoin transaction volume, the benefits flow directly to parties who funded and guided its development.

The participation of prominent crypto traders like Cobie and Zaheer Ebtikar through Split Capital alongside institutional players like Mirana Ventures, Cumberland DRW, Flow Traders, Bybit, IMC Trading, and Nomura Holdings demonstrates that sophisticated market participants saw value proposition clearly. These aren’t speculative retail investors chasing next hot token but professional traders and financial institutions making calculated bets on infrastructure that could reshape stablecoin settlement. Their involvement validates thesis that capturing even small percentage of existing USDT transaction volume creates substantial business opportunity.

The Pre-Deposit Campaign Mechanics Creating Manufactured Demand

The June 2025 deposit campaign demonstrates how modern crypto projects manufacture urgency and social proof before launching actual products. Plasma announced one billion dollar deposit cap for users who wanted allocation in upcoming token sale with participation levels determined by deposit size and lockup duration. The mechanics created game theory situation where participants needed to deploy capital immediately or risk missing opportunity. We’re seeing coordination between genuine market demand and carefully engineered scarcity that makes separating organic interest from FOMO-driven speculation impossible.

The initial five hundred million dollar cap filled within two minutes of opening causing immediate backlash from community members who felt bot activity and insider access prevented fair participation. The rapid sellout created perception of overwhelming demand while simultaneously frustrating thousands of potential participants who couldn’t get transactions confirmed fast enough. Plasma responded by raising cap to one billion dollars which then filled within thirty minutes demonstrating that previous cap wasn’t reflecting actual demand ceiling but rather creating artificial scarcity that generated headlines and social proof.

The controversy around whale domination versus retail access reveals tensions inherent in modern token launches. Analysis showed top three contributors deployed over one hundred million dollars collectively while one user paid thirty-nine ETH approximately one hundred four thousand dollars in gas fees to ensure their ten million dollar deposit executed before vault filled. These gas wars where participants compete by paying higher transaction fees demonstrate desperation to secure allocation in what they perceived as can’t-miss opportunity. The median deposit of approximately thirty-five thousand dollars suggests relatively wealthy participant base where typical retail investor lacked capital to participate meaningfully.

The equal distribution of twenty-five million XPL tokens worth approximately twenty-five million dollars to all pre-depositors regardless of deposit size created viral social media moment. Someone who deposited one dollar received same eight thousand three hundred ninety dollar bonus as person who deposited ten thousand dollars generating stories about incredible returns from minimal investment. This airdrop strategy generated enormous positive sentiment and created thousands of token holders with vested interest in Plasma’s success who would promote project through social channels. The psychological impact of receiving unexpected windfall far exceeded rational economic analysis of whether underlying blockchain justified valuations being discussed.

The August Yield Program Demonstrating Binance Partnership Value

The August 2025 announcement of two hundred fifty million dollar USDT yield program through Binance Earn demonstrated Plasma’s ability to leverage established platform relationships for user acquisition. The program offered daily USDT rewards plus distribution of one hundred million XPL tokens representing one percent of total supply to participants. The offering filled within one hour reaching capacity limit showing continued strong demand for exposure to Plasma ecosystem before mainnet launch. The partnership with Binance specifically rather than smaller exchange provided legitimacy and distribution reach impossible for new project to achieve independently.

The mechanics where users locked USDT on Binance and received both stablecoin yield and XPL token allocation created dual incentive structure appealing to different investor types. Conservative participants focused on stable yield from lending markets could justify participation through predictable returns while speculators focused on XPL token upside potential in anticipation of mainnet launch and subsequent price discovery. This combination allowed Plasma to attract capital from broader demographic than pure speculative token sale would reach.

The rapid filling of capacity in these various campaigns created pattern where missing one opportunity meant scrambling to catch next wave. This manufactured momentum where each successful raise generated headlines leading to increased interest in subsequent offerings creating self-reinforcing cycle. The progression from three point five million friends and family round through billion dollar deposit campaigns to three hundred seventy-three million public sale demonstrated escalating scale and broadening participation that validated project trajectory in eyes of market participants comparing Plasma to previous successful blockchain launches.

The September Mainnet Launch Revealing Market Reception Reality

The September 25 2025 mainnet beta launch with simultaneous XPL token generation event represented culmination of year-long capital raising and community building efforts. The network launched with over two billion dollars in stablecoin liquidity and more than one hundred DeFi protocol integrations including Aave, Ethena, Fluid, and Euler providing immediate ecosystem depth that new blockchains typically require months or years to develop. This coordinated launch where major protocols deployed on day one demonstrated pre-existing relationships and likely incentive arrangements ensuring Plasma wouldn’t face empty ecosystem problem that kills many promising chains.

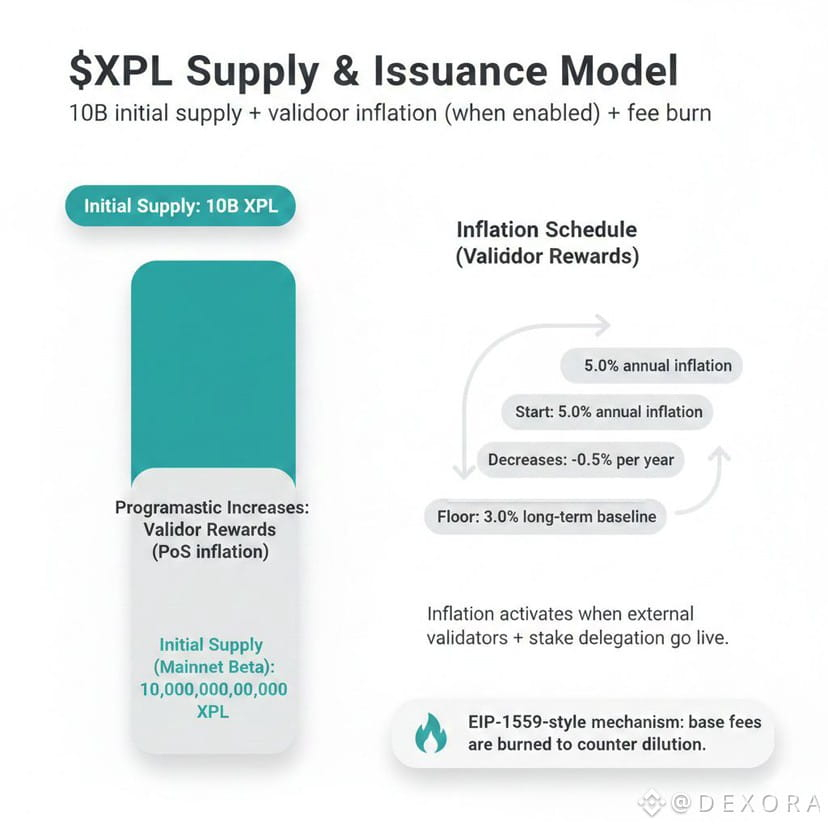

The token price action tells more complicated story than launch day celebrations suggested. XPL peaked around one dollar fifty-four shortly after launch before declining eighty-five percent to approximately twenty cents in subsequent months. This price collapse despite maintaining significant TVL and transaction activity reveals disconnect between infrastructure usage and token value capture. The deflationary tokenomics where base fees get burned following EIP-1559 model should theoretically create value accrual for XPL holders but actual market behavior suggests traders view token primarily as speculative vehicle rather than productive asset generating returns.

The TVL trajectory from eight billion dollars within three weeks of launch declining to approximately one point eight billion dollars by late 2025 demonstrates challenge of converting mercenary yield farmers into genuine users. The initial deposits came overwhelmingly from users chasing XPL token incentives distributed to lenders and borrowers within ecosystem. When those incentive rates inevitably decreased as token emissions slowed, capital flowed back to established chains offering better risk-adjusted returns. This pattern repeats across most new chain launches where inflated APYs attract temporary capital that exits once subsidies end leaving question of whether any organic user base remains.

The Tron Competitive Response Validating Threat Assessment

The immediate defensive reaction from Tron cutting energy unit prices by sixty percent from two hundred ten sun to one hundred sun reducing USDT transfer costs from over four dollars to under two dollars demonstrates that established players viewed Plasma as legitimate competitive threat. Tron generates over two billion dollars annually in fee revenue primarily from USDT transactions making it most successful stablecoin settlement layer to date. The willingness to sacrifice half of that revenue overnight signals recognition that maintaining market share against zero-fee competitor requires immediate price matching regardless of profit impact.

This competitive dynamic vindicates Plasma’s core thesis that stablecoin users care primarily about cost and speed rather than broader blockchain ecosystem features. If Tron with its massive existing user base and network effects felt compelled to slash fees within days of Plasma launch, it suggests real risk of user migration if cost differential remained significant. However, Tron’s response also demonstrates that zero-fee model isn’t sustainable competitive advantage if other chains can simply lower their own fees to match. The race to bottom on transaction costs may benefit users but questions whether any blockchain can generate sufficient revenue from stablecoin transfers to justify valuations being placed on native tokens.

The broader competitive landscape includes not just Tron but also Ethereum with one hundred sixty-six billion dollars in stablecoin supply, emerging players like Circle’s Arc blockchain and Stripe’s Tempo payments infrastructure, and potential Google stablecoin initiatives. Each competitor brings different advantages whether Ethereum’s massive developer ecosystem and security guarantees, Circle’s regulatory compliance and institutional partnerships, or Stripe’s merchant relationships and payment processing expertise. Plasma must articulate why being purpose-built specifically for stablecoins outweighs disadvantages of being new entrant without established network effects or proven security track record.

The Regulatory Headwinds Creating Geographical Limitations

The European Union’s MiCA regulation creates existential challenge for Plasma’s USDT-centric business model. The framework requires stablecoin issuers to obtain authorization as credit institutions or electronic money institutions, maintain sixty percent of reserves in EU bank accounts for significant stablecoins, and prohibits interest payments to holders. Tether CEO Paolo Ardoino publicly criticized these requirements as creating systemic banking risks and has not pursued MiCA authorization meaning USDT cannot be offered or traded to EU consumers starting June 2025.

For Plasma whose entire value proposition centers on frictionless USDT transfers, losing access to European market represents significant limitation on addressable user base and transaction volume. While custody and transfer of existing USDT remain legal under ESMA clarification, inability to onboard new EU users or facilitate trading severely constrains growth potential in major developed market. The challenge requires either supporting MiCA-compliant stablecoin alternatives like Circle’s USDC which undermines Plasma’s close relationship with Tether or accepting that European market remains largely inaccessible which limits global payments narrative underpinning investment thesis.

The regulatory environment in United States remains uncertain with various stablecoin bills proposed but none enacted creating operational ambiguity for projects built around specific issuers. If future US legislation imposes restrictions on Tether similar to EU’s MiCA framework, Plasma faces risk that its primary product becomes legally problematic in multiple major jurisdictions simultaneously. This regulatory concentration risk inherent in being deeply aligned with single stablecoin issuer creates vulnerability that more neutral infrastructure providers avoiding explicit favoritism might better navigate.

Contemplating Trajectories Beyond Launch Momentum

Looking several years forward, success requires transitioning from subsidized user acquisition to sustainable economic model where participants use Plasma because it genuinely provides superior experience rather than because token incentives make participation profitable. The zero-fee USDT transfers funded by Plasma Foundation spending create temporary competitive advantage but cannot continue indefinitely without revenue sources replacing subsidy spending. The three hundred seventy-three million dollars raised provides runway but at estimated two point eight million daily in incentive distribution, burn rates consume capital quickly unless transaction volume grows dramatically or fee structures change.

The relationship with Tether creates both opportunity and constraint. If Tether decides Plasma is preferred settlement layer and actively directs users toward it through wallet integrations and exchange partnerships, that institutional support could rapidly drive adoption beyond what independent blockchain achieves alone. However, this dependency means Plasma’s fate remains tied to Tether’s strategic priorities and regulatory standing. If Tether faces legal challenges or regulatory crackdowns that damage its market position, Plasma as closely associated infrastructure suffers collateral damage regardless of technical merits.

The vertical integration story where Tether captures transaction value currently flowing to competing chains makes compelling business sense for Tether shareholders and explains strategic backing from iFinex entities and Paolo Ardoino personally. Whether this translates into value for XPL token holders represents separate question entirely. The token could remain merely functional gas token required for validator operations while Tether captures majority of economic value through increased USDT usage and potential future fee sharing arrangements. The disconnect between network success and token holder returns plagues many blockchain projects where infrastructure value doesn’t automatically accrue to native token beyond speculative trading.

The technology works as advertised with fast transactions, EVM compatibility, and Bitcoin anchoring providing security narrative. The partnerships exist with major DeFi protocols and institutional backers providing credibility. The capital is available with hundreds of millions raised enabling continued development and marketing. What remains uncertain is whether technical capabilities and financial backing translate into genuine market need that billions of people actually experience as improvement over existing stablecoin transfer methods. The answer to that question determines whether Plasma represents successful infrastructure play reshaping global payments or expensive experiment demonstrating that being purpose-built for specific use case doesn’t automatically create sustainable competitive advantage in commoditized market where users ultimately care only about cost, speed, and reliability regardless of underlying technical architecture.