Plasma is not designed to grow by bootstrapping DeFi first.

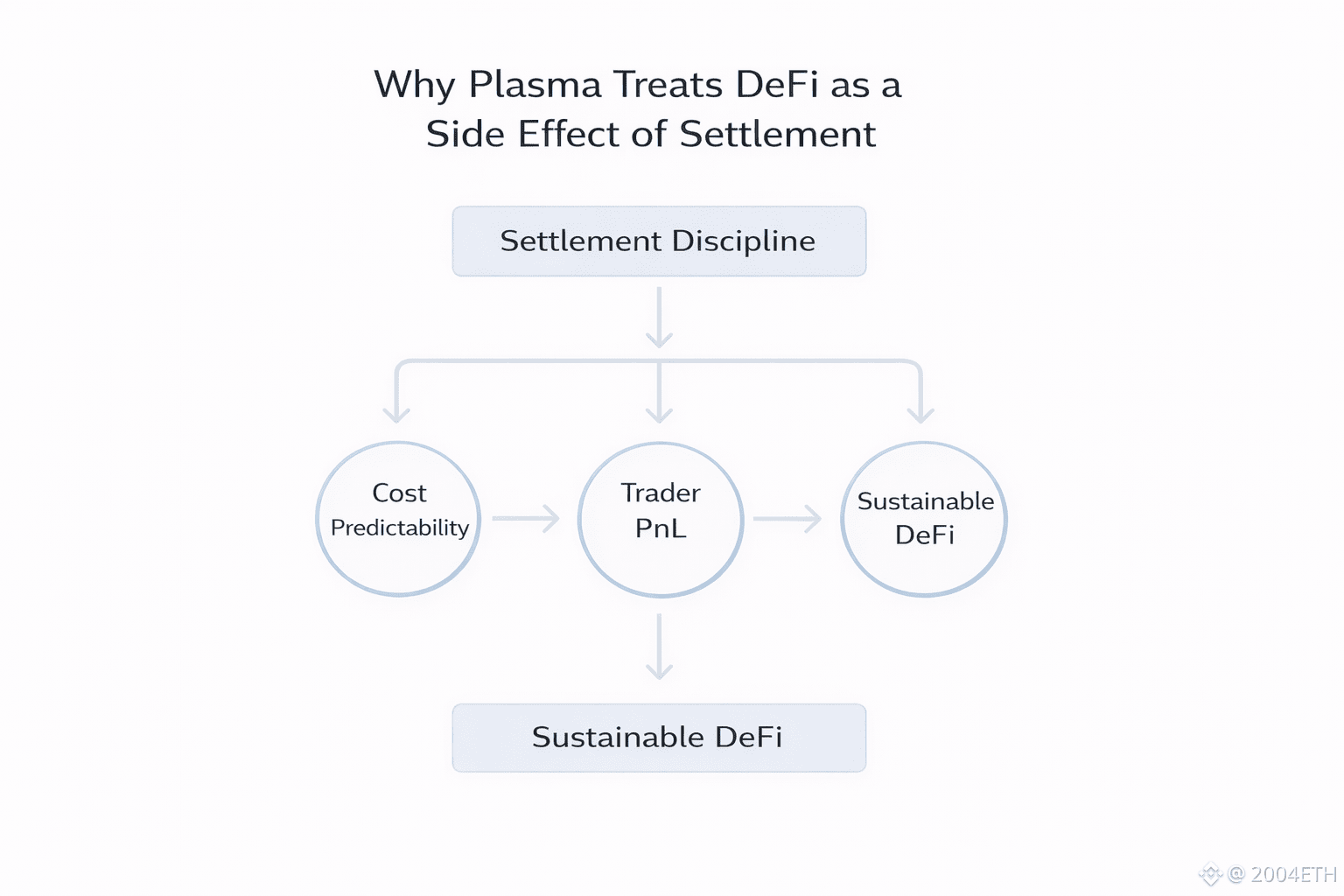

From the start, the system is built around settlement discipline, predictable execution, constrained behavior, and cost stability. DeFi is expected to form only after those conditions exist, not before.

That design choice explains much of what looks unusual about Plasma’s ecosystem today.

Instead of pushing liquidity at any cost or optimizing for early headline metrics, Plasma puts most of its weight on whether settlement can function the same way when usage becomes continuous. The underlying assumption is simple. If settlement only works when conditions are ideal, it is not reliable enough to support real economic activity.

This leads Plasma down a different path than most DeFi ecosystems.

In incentive driven environments, liquidity usually arrives first. Activity follows because rewards are available. Settlement volume looks healthy as long as incentives remain attractive. The moment those incentives decline, the weakness shows. Usage drops, positions unwind, and protocols that looked active turn out to have been highly subsidized.

Plasma flips that sequence.

Settlement reliability is treated as a prerequisite, not a result. Execution paths are intentionally narrow. Validator behavior is constrained rather than optimized for responsiveness. The system is built to behave the same way when demand increases, instead of adapting dynamically once pressure appears.

XPL fits into this picture in a very specific way.

It is not there to attract users or amplify yields. XPL exists to make settlement rules stick over time. Validators stake XPL to signal long term commitment to a fixed behavior profile, even in situations where relaxing constraints might improve short term outcomes.

This changes how activity develops on top of the network.

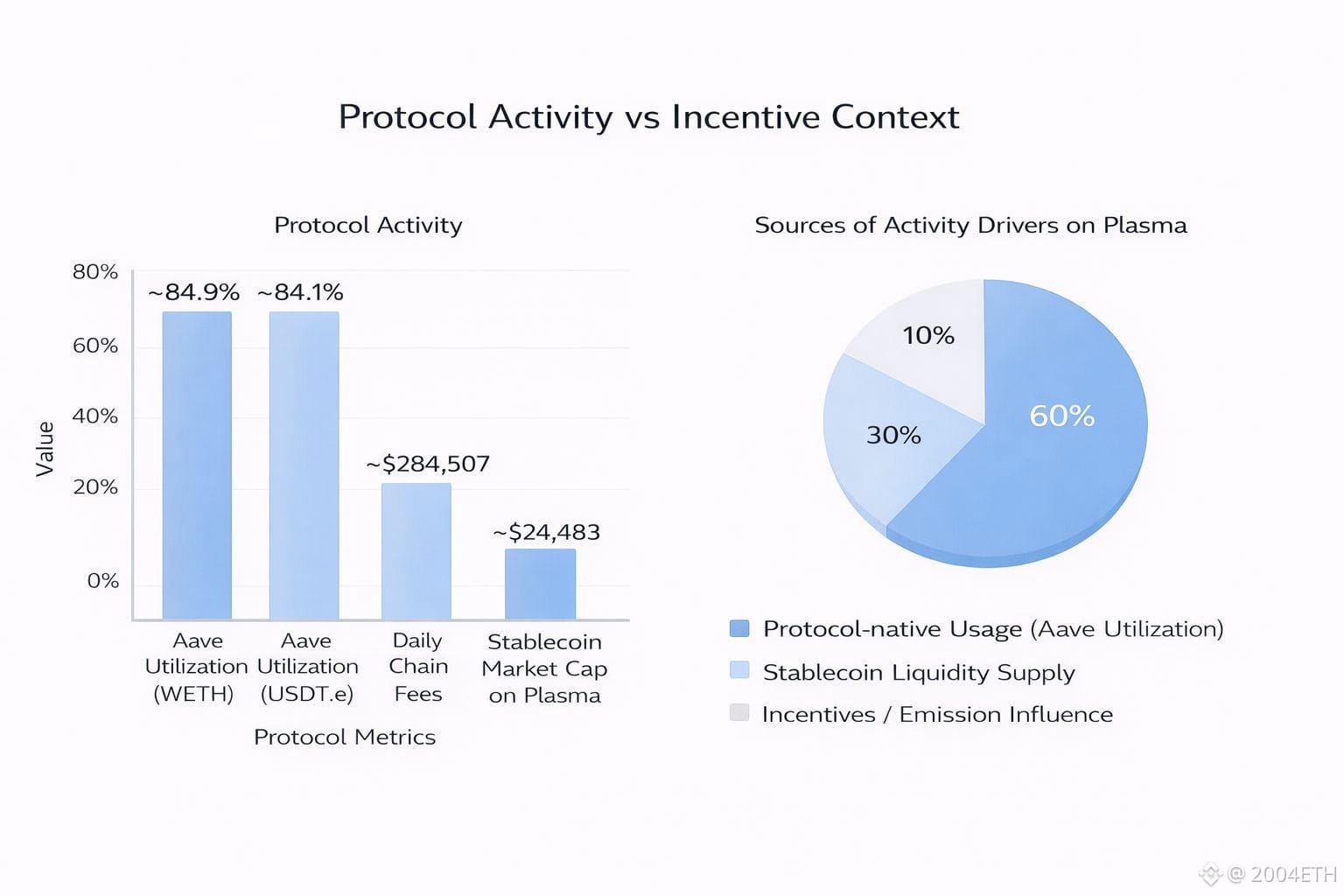

When incentives are generous, almost any ecosystem can look active. When incentives fade, only systems with genuine demand remain usable. Recent activity on Plasma suggests that utilization has not disappeared alongside declining emissions. Liquidity no longer behaves like a constant operating expense, and participation increasingly reflects traders taking positions based on expected profitability rather than rewards.

That pattern does not emerge by accident.

It suggests that DeFi on Plasma is functioning as a consumer of settlement reliability, not as a mechanism to manufacture it. Protocols that require continuous subsidies struggle to survive in this environment. Those that remain tend to be smaller, but their activity is easier to explain in economic terms.

This approach is not designed to appeal to every type of user.

Plasma does not offer the flexibility or rapid iteration that incentive heavy DeFi ecosystems rely on. It is unlikely to attract short lived capital chasing temporary yield opportunities. For some participants, this will feel restrictive or unexciting.

But that restriction appears intentional.

As stablecoin usage increasingly moves toward settlement and capital management, systems that depend on constant incentives face a structural problem. Activity becomes harder to sustain once rewards normalize. Plasma seems to accept that reality and design around it, rather than postponing it.

Instead of trying to force DeFi growth early, Plasma allows activity to emerge where settlement reliability makes it viable.

If the ecosystem continues to operate with limited incentives and stable utilization, it will not be because liquidity was aggressively pulled in. It will be because the settlement layer was stable enough for economic activity to justify itself.

That is a narrow and opinionated design choice.

For settlement focused infrastructure, it may also be the more honest one.