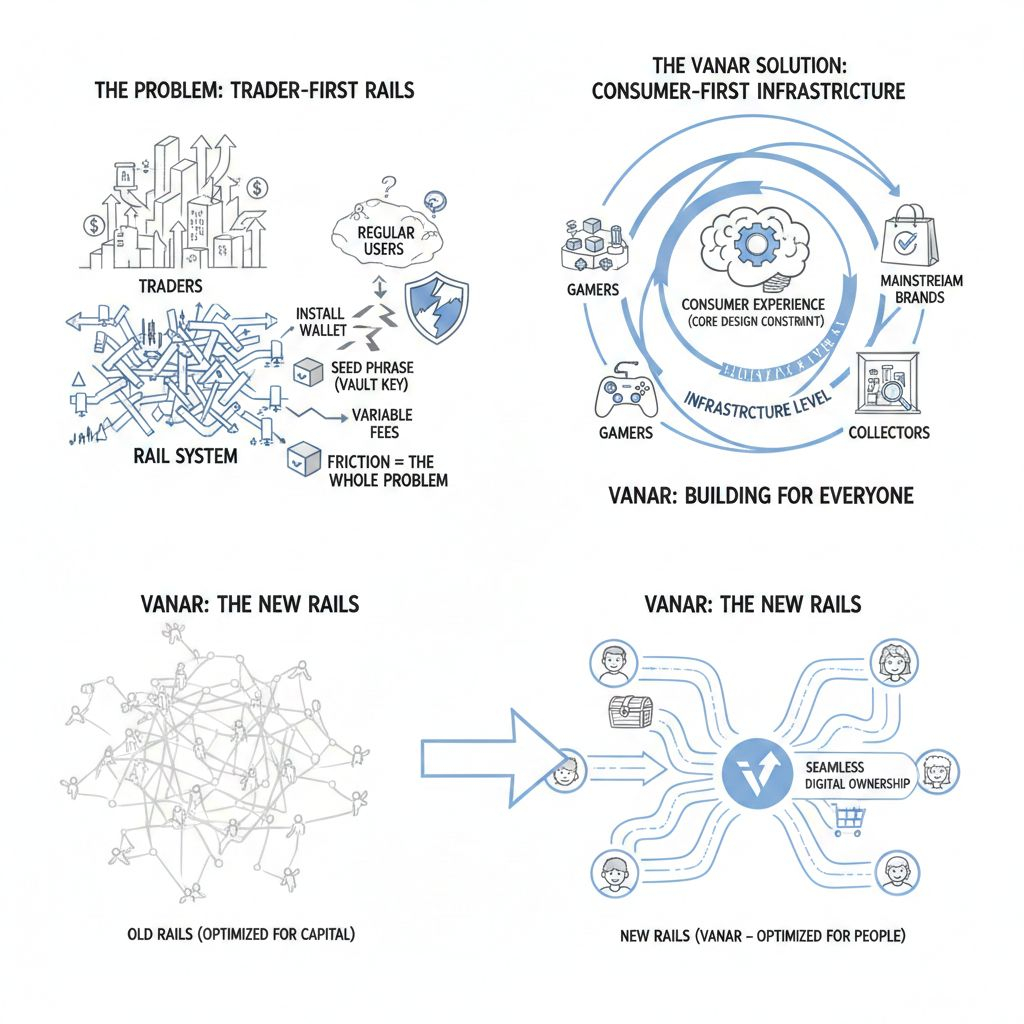

Vanar Most consumer crypto products do not break because people hate digital ownership. They break because the rails underneath them were built for traders first, and regular users only get invited in after the fact. That is why the first experience often feels like a test you did not sign up for: install a wallet, store a seed phrase like it is a vault key, pay fees that change without warning, and hope you do not make one mistake that is impossible to reverse. If you are building for gamers, collectors, or mainstream brands, that friction is not a small inconvenience. It is the whole problem. Vanar is trying to solve that mismatch at the infrastructure level by treating consumer experience as the core design constraint, not a feature that gets added once the chain is already optimized for capital flow.

This matters more right now because the environment is less forgiving. Liquidity is not evenly available the way it was during peak cycles, so ecosystems cannot assume they can buy usage with incentives and keep it later. Regulation is more hands on, which means partners with reputations to protect will not integrate systems that feel unpredictable in how accounts, payments, data, and risk are handled. And competition is brutal. Many networks can claim speed or low fees, so the differentiator shifts toward distribution, reliability, and whether real products keep running when attention moves elsewhere. Vanar is taking a clear stance here. It is leaning into entertainment and consumer software as the on ramp, with Virtua Metaverse and the VGN games network repeatedly described as known surfaces connected to the ecosystem, instead of pitching itself as a general purpose chain that will maybe attract consumer apps later.

The most important thing to understand about the vision is what it implies about incentives and timelines. Vanar did not start from a blank slate infrastructure pitch. It evolved from a consumer oriented identity and documented a transition from the earlier TVK branding into Vanar Chain with the VANRY token. That kind of shift is not automatically positive, but it does reveal intent: align the chain story, the token story, and the product distribution story into one lane. When a team builds around consumers, the chain has to care about boring things that actually decide outcomes, like whether fees stay stable enough for micro purchases, whether onboarding can be smoothed without taking custody, and whether partners can trust the platform to behave consistently.

From here, I always prefer to look at what is measurable before what is claimed. Vanars explorer shows the network has processed a very large number of lifetime transactions and has a very large number of wallet addresses. That does not prove adoption by itself, because addresses are not the same thing as people and raw transaction totals can be inflated by automated behavior. But it does establish that this is not a theoretical chain. It is running and being used, and the scale is large enough to justify deeper questions instead of quick dismissal. The right next step is not to celebrate those totals. It is to ask what they are made of. Are transactions spread across many applications, or concentrated in a small cluster. Are users coming back, or is activity mostly bursts tied to campaigns. Is there meaningful fee demand, or is volume mostly empty calories. The public explorer is only the first layer, but it gives you the entry point for that investigation.

The second layer is developer reality. Consumer chains do not win by having one or two internal products that make the charts look busy. They win when outside builders choose them because shipping feels easier and the economics make sense. Vanar does have a public documentation surface and it includes protocol level disclosures, such as how block rewards and inflation are structured. I take that seriously because token design is not cosmetic. If a network is going to last, especially if it wants brands and long term partners, it has to be clear about how security is funded and how supply expands. Vanars docs describe a long horizon inflation profile with higher issuance early on to fund ecosystem development and early staking dynamics. That is a reasonable pattern in crypto, but it creates a clear test. The ecosystem must convert spending into sticky usage and fee demand quickly enough that issuance does not become a permanent ceiling on price and sentiment.

Partnerships and integrations are where people often get distracted, because this space is full of shallow announcements. With Vanar, the meaningful part is not a random list of names. It is the repeated emphasis that there are actual consumer facing surfaces tied to the ecosystem, like Virtua and VGN, and that the chain is designed for mainstream verticals like gaming and entertainment. The only responsible way to treat that is as a hypothesis. If those products are truly driving real onchain commerce, you should see consistent activity patterns, repeat behavior, and a distribution of transactions that is not dependent on a single contract. If it is mostly marketing, you will see spikes, concentrated activity, and weak retention. That is not a moral judgment. It is just how consumer ecosystems behave when they have not found durable loops yet.

Roadmap credibility is similar. A lot can be promised, but consumer infrastructure has to deliver on reliability and iteration. Vanar has also been pushing broader positioning around AI native design and payment or real world aligned narratives. That can be strategic if it becomes real integrations, because it would reduce dependency on purely gaming cycles. But it can also be a sign of scope expansion, which is dangerous if the team has not already nailed the core execution path. The clean way to evaluate roadmap credibility is to track shipped milestones, third party developer launches, and the quality of onchain activity over time, not just new storylines.

When you compare Vanar to other consumer adjacent ecosystems, the tradeoffs become clearer. Ronin is a strong reference point because it has proven consumer scale throughput, but it has also shown how concentrated activity can be when a chain depends heavily on a few flagship products. Immutable is another useful benchmark because it has built deep studio pipelines and tooling designed to abstract crypto complexity, and it benefits from Ethereum adjacency, but even there you can observe that transaction volume and user growth do not always move together. Vanars potential advantage is control. Being an L1 gives it freedom to tune fee behavior, performance, and storage choices in a way that can match consumer product needs. Its weakness is bootstrapping. It must build security, liquidity gravity, and builder mindshare in a market where other ecosystems already have entrenched pipelines and proven distribution.

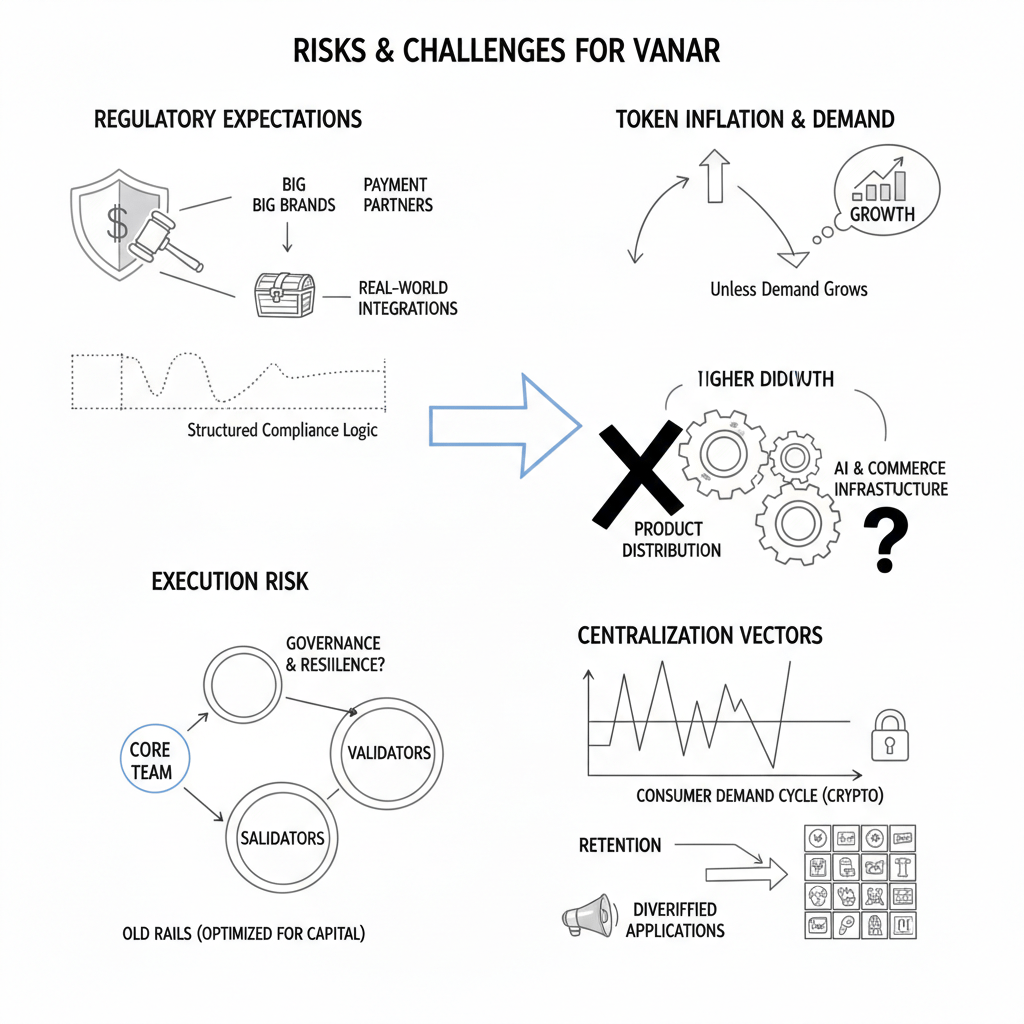

Now for risks, without turning this into doom. If Vanar wants to attract bigger brands, payment partners, or real world aligned integrations, regulatory expectations rise. That can introduce friction in product design because partners often want more structured compliance logic and less ambiguity. Token inflation is another practical risk, not because inflation is automatically bad, but because early higher issuance creates sell pressure unless demand grows. Execution risk is high because Vanar is trying to balance multiple ambitions at once: consumer scale infrastructure, a broader AI and commerce narrative, and real product distribution surfaces. Focus dilution is a common failure mode. Centralization vectors also matter, because many consumer chains start with a small validator set and heavy reliance on a core team and a few flagship apps. That can be fine early, but it becomes a long term governance and resilience question. And finally there is market dependency. Consumer demand is cyclical, and crypto makes that cycle sharper. The way out is retention and diversified applications, not louder announcements.

The long term outlook comes down to whether Vanar can turn its consumer positioning into repeatable economic behavior. If you watch one thing, watch whether activity diversifies across many apps and contracts rather than clustering around one surface. If you watch a second thing, watch whether fees and retention start to look like a real digital economy rather than incentive driven motion. And if you watch a third thing, watch whether external builders show up with production apps, verified contracts, and a visible culture of maintenance and audits. If those trends strengthen over the next one to two years, Vanar has a real chance at multi cycle durability because it would be anchored in product usage, not token attention. If they do not, the chain will likely trade like many consumer narratives do: sharp bursts during favorable liquidity windows and long quiet stretches when the market focuses elsewhere.