In its first ever survey, Binance Research analyzed typologies and views from the largest VIP and institutional clients that use some of the services offered within the Binance ecosystem.

Long-term investing is one of the most popular strategies for large and institutional clients. Despite this, lending and borrowing platforms are not yet widely used, with non-custodial decentralized platforms being barely explored. On the other hand, DEX have been experimented by most participants, yet, as of today, are not widely used owing to their lower liquidity (than CEX) and steeper learning curve.

Stablecoins are used by nearly all market participants, with USDT being the “go-to stablecoin”. Amidst the recent turmoil regarding Tether, many investors have been exploring alternative offerings, particularly USDC and PAX.

From the perspective of large market players, Bitcoin is expected to maintain its dominance by the end of 2019, with its market cap expected to represent 40% to 60% of the industry total cap.

Regulations, both local and global, seem to be the key indicator that investors look for as it was ranked both the largest risk and key growth driver for the future of the cryptocurrency and digital asset industry. Furthermore, new product offerings (such as brokerage services and the creation of new derivatives markets) also are expected to be key drivers of the future growth for this industry.

Finally, cryptoasset initiatives by companies like Facebook, Samsung or JP Morgan are not seen as future growth drivers for this industry.

In late May 2019, Binance Research organized its first-ever poll distributed across large institutional and VIP clients using Binance’s wide range of services such as exchange platforms and OTC trading desk. This report discusses some of the results and findings stemming from the collected responses. This report was prepared in cooperation with the Binance Trading desk1.

1. Experience and typologies

Over one hundred of institutional and VIP clients were reached by email with a link to complete this survey. Data was collected anonymously, with the added option for each client to leave a follow-up email address.

Roughly half of the clients responded and a large majority filled in answers to most of the questions. However, though we did not make every question mandatory, we decided to exclude clients who did not answer more than 30% of the questions that were retrieved. As a result, our sample is size is made of 41 key institutional and VIP clients. As we acknowledge that any of the results described in the next sections should be interpreted with extreme caution and should not be generalized to the entire institutional landscape, these results still provide some insightful views and metrics about the non-retail market segment.

1.1 Typologies of large institutional and VIP clients

In this section, we will dig into what are the different profiles from institutional and VIP clients.

Chart 1 - Average holding time for cryptoassets (excluding stablecoins)

Amongst our large institutional clients, more than half stated they typically hold positions for more than a week, whereas only a third said they would engage in high-frequency trading and other market making strategies.

Regarding utilization of trading platforms, we noticed a big disparity in how many exchanges were used among clients.

In general, we found a clear positive relationship between the capital owned by clients and the actual amount of exchanges used, indicating that clients with larger funds tend to use more exchange platforms than clients with less capital.

Beyond this general correlation,, a second relationship was observed in clients who hold positions for less than a day; these users on average use more exchange platforms than others. By nature, cross-platform arbitrage strategies tend to require the use of many trading venues and markets to extract more opportunities, which likely explains this phenomenon. Higher frequency trading takes advantage of smaller price differentials, so having more platforms at one’s disposal is crucial to this strategy’s success.

Regarding accounting and profit currency, 90% of the clients use USD as the benchmark currency, which is in line with our initial expectations, as USD stablecoins and USD-denominated platforms are the leading forces of the cryptocurrency and digital asset industry2. A few clients replied with local European currencies such as CHF or EUR as the accounting currencies.

Chart 2 - Stablecoin usage (%) across institutional and VIP clients

When it comes to stablecoins, nearly all the responders use stablecoins for various functions such as trading and as a store of value. Without much surprise, USDT was the go-to stablecoin but PAX and USDC appear to also be widely used. Among USDT alternatives, USDC appeared (unsurprisingly) particularly popular for non-Chinese clients whereas Chinese clients prefer PAX. However a few clients indicated that they were currently looking for alternatives for USD Tether (USDT) with similar liquidity profiles (link to our report where we said USDT had best liquidity).

Interestingly DAI, the crypto-backed stablecoin minted in the Maker ecosystem, was used by almost 20% of the participants.

Finally , 87% of the respondents have used an OTC desk (e.g., Binance Trading Desk, Galaxy Digital, Cumberland, Huobi OTC) before.The main reason cited for using OTC services selected was that these desks act as a fiat crypto gateway, followed by better liquidity and less trading hassle. The last two reasons were particularly significant across large institutions, as measured by their reported AuM.

1.2 Experiences in the industry

In this section, past experiences from institutional and VIP clients are discussed.

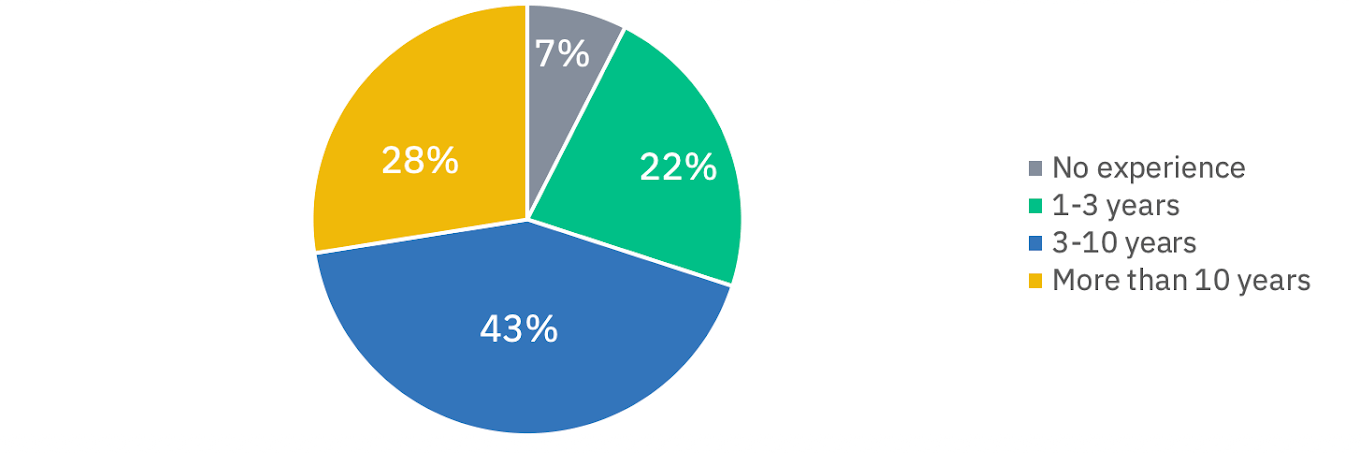

Chart 3 - Past experiences in the traditional financial industry

Most of the respondents have prior experience in the financial industry with only 7% of the respondents having no experience in the financial industry before being involved in the cryptocurrency and digital asset industry, whereas 71% had at least 3 years of experience in the traditional financial industry.

Regarding their experience in the cryptoasset industry, most of the large players have been involved for a few years in the industry, with a mere 7% being in the space for less than a complete year.

Interestingly, the two broadest categories are 2-3 years (30%) and 5-7 years (18%). They represent initial joining periods of 2013-2014 and 2016-2017, which are respectively the two largest rally periods: the Bitcoin rally of 2014 (pre-MtGox’s shutdown) and the 2017 rally.

Chart 4 - Current experience in the cryptoasset industry

When questioned about whether they trade other asset classes, institutional and VIP clients, more than half of the respondents have traded other asset classes. Among them, 50% also conduct trades in the equity market and 25% are involved in foreign currency trading.

67.5% of the respondents are involved in leveraged trading, either through margin borrowing or futures contracts. Interestingly, there was no clear pattern between the use of leveraged trading and past experience in the financial industry.

1.3. Decentralization and custodianship

Regarding methods of storage, the clients with large Asset under Management (over USD 25 million) store (at least partially) their digital assets in cold wallets and/or through the use of dedicated third-party custody services, in addition to the use of exchange platforms for trading. For large clients (i.e., capital dedicated specifically to cryptoasset investing & trading volumes above USD 5 million), “cold wallets” was almost always selected as one of their answers.

Chart 5 - Storing methods for cryptoassets

The vast majority of the sampled users rely on exchanges to keep some of their digital assets. One of the potential explanations is that market participants with high turnover buy and sell frequently digital assets and need to keep funds on exchange as the exchange platforms typically charge some additional fees3 to withdraw along with better liquidity of centralized exchanges.

Given the volatility of the asset class, it is also important one has access to the inventory necessary to trade in and out of positions quickly and on-chain transactions remain too slow for most participants.

Realistically, no market making or prop-trading strategy could be efficiently operated without funds held on centralized exchanges. It will be interesting to revisit this finding once the cryptoasset landscape shifts over to greater volumes on decentralized non-custodial platforms, such as Binance DEX. Furthermore, hot wallets (such as mobile applications like Trust Wallet, Coinbase Wallet) are not widely used for storing funds with only a third of the respondents using them.

We also found out that decentralized exchanges and on-chain protocols are not yet very popular among large market participants. 55% of the respondents responded that they have tried decentralized exchanges but most of the respondents argued that the lack of liquidity, compliance concerns, and non-intuitive user experiences () were key factors for avoiding decentralized exchanges. Regarding the use of custodial lending/borrowing platforms (such as Nexo or BlockFi), 33% of the participants use it. Without surprise, participants who use these platforms tend to be investors with long-term investment strategies. For people not using these platforms, the counterparty risk was mentioned many times as the main reason for not using any of them.

Non-custodial cryptoasset borrowing and lending platforms and protocols4 are even less popular amongst these institutional players, with only 12% of the surveyed participants using them. Interestingly, some of the participants not using custodial lending/borrowing platforms (owing to suspicion regarding the credit risk of custodial lending/borrowing platforms) do in fact use non-custodial alternatives, which feature technological risks that they could handle.

2. Market views

2.1 Risks and potential growth drivers for the industry

Participants were requested to pick a score between 1 to 5 for each of the risks on a list. In the next tables, 1 represents the highest whereas 5 represents the lowest.

Table 1 - Ranks of 5 risks for the cryptoasset industry (1 highest, 5 lowest)

AVERAGE | MEDIAN | QUARTILE 1 | QUARTILE 3 | |

|---|---|---|---|---|

Technology failure (hack, etc.) | 1.67 | 1 | 1 | 2 |

Change in global & local jurisdictions (e.g., China, America, EU) | 2.39 | 2 | 2 | 3 |

Tether legal issues | 2.64 | 3 | 2 | 3 |

Security test (Howey test) | 2.76 | 3 | 2 | 3 |

Privacy risk | 3.06 | 3 | 2 | 4 |

When requested to evaluate potential risks & negative factors for the cryptoasset industry, the biggest concern is undoubtedly technology risks such as getting hacked. Surprisingly, Tether (USDT) is not one of the largest risks selected, despite the recent turmoil with the ongoing legal dispute over Tether’s backing. In spite of the growing popularity of privacy coins like Monero (XMR), most of the respondents do not yet weigh potential risks related to the blockchain inherent privacy concerns5.

Table 2 - Ranks of 8 potential growth drivers for the cryptoasset industry (1 highest, 5 lowest)

AVERAGE | MEDIAN | QUARTILE 1 | QUARTILE 3 | |

|---|---|---|---|---|

Change in global and local regulations | 1.79 | 1 | 1 | 2 |

ETFs | 2.24 | 2 | 1 | 3 |

Traditional brokerages offering crypto service (e-trade, Fidelity) | 2.64 | 2 | 2 | 4 |

Development of options contracts | 2.67 | 2 | 2 | 3 |

Physically settled futures contracts (e.g., Bakkt) | 2.76 | 2 | 2 | 4 |

Stablecoin by Facebook | 3.06 | 3 | 2 | 4 |

Samsung initiatives such as Samsung Coin or phone built-in crypto-wallets | 3.09 | 3 | 2 | 4 |

Stablecoin by JPMorgan | 3.27 | 4 | 3 | 4 |

Initiatives from private companies such as Facebook, JPMorgan (stablecoins) and Samsung were generally ranked as low potential growth drivers for the cryptoasset industry, whereas changes in global and local regulations are by far considered the largest single potential growth driver in the future of the cryptoasset industry. It is worth noting that respondents who ranked regulations as a threat also often rank it as a potential growth driver. Regulation can either assist and foster growth by providing a framework within which crypto projects can work and flourish, or it could stymie growth and development, thus demonstrating the potential large upsides and downsides that regulation has on this space, depending on how it evolves. In general, regulation, both local and global, seems to be the key factor that is widely monitored by the sampled market participants.

The ETF proposal in the US remains a large topic of interest and many players expect it to also be a major growth driver for the cryptocurrency and digital asset industry. In general, any development of auxiliary financial products (e.g., ETFs, options, regulated futures and brokerage services) could become significant growth drivers for the industry.

2.2 The future of Bitcoin and other large cryptoassets

This last section discusses the expectations of market participants on which cryptoassets they are most bullish by the end of 2019 along with the expected market dominance of Bitcoin6.

Chart 6 - Bitcoin expected dominance (%) as the end of December 2019

At the time of the survey, Bitcoin market dominance was at almost exactly 60%, so most participants expect this to roughly remain the same or regress slightly.

More than 80% of the participants expect Bitcoin market capitalization to be between 40% and % at the end of December 2019. It illustrates the special status of Bitcoin as the bellwether of the cryptocurrency and digital asset industry.

The participants were requested to select the most undervalued segment in the digital asset industry out of four key categories.

Blockchain Infrastructure (e.g., Ethereum, Zilliqa, Icon, Nebulas) was selected as the most undervalued segment for 42% of the respondents.

Store of Value/Currency/Payment/Settlement (e.g., Bitcoin, Monero, Ripple) came in second, and was selected by 36% of them.

Services and DApps built on the blockchain (e.g., Exchange tokens, Social Media, Gambling and Gaming, Data storage, etc) was only selected by 15% of the participants.

Others received 6% of the replies with specific responses such as Privacy Coins, etc. Some participants even indicated that all digital assets were overvalued.

3. Final comments

This first report, based on a public poll of our clients, represents a first joint effort between Binance Research and Binance Trading to gather market intelligence about the participants in this industry. Unfortunately, the sample remains small and all results discussed in previous sections are strongly tied to participants in our ecosystem. In spite of Binance’s fairly large presence in the cryptoasset ecosystem, some large participants may not use any of our services and as a result, would not have been targeted by our survey, which would ultimately leave these results to be biased.

Nonetheless, while this analysis did not aim at proxying the entire industry, it still reveals some interesting insights and market views from some of the largest participants in the ecosystem.

If repeated in the future at a larger scale, this type of analysis would help for trend analysis about the market participants, and ultimately help in painting a more comprehensive picture of the cryptoasset market.

Telegram channel: https://t.me/BinanceOTC↩

See our past report: The Evolution of Stablecoins. https://research.binance.com/analysis/stablecoins-evolution↩

In addition to various blockchain fees such as gas.↩

See our past report about DeFi and borrowing/lending non-custodial protocols. https://research.binance.com/analysis/decentralized-finance-lending-borrowing↩

See our past report about Monero’s latest fork that discusses the fungibility issue with non-privacy coins. https://research.binance.com/analysis/monero-hard-fork↩

Refer to Binance Academy to understand the importance of this. https://academy.binance.com/glossary/bitcoin-dominance↩