Author | Day

Produced by|Baihua Blockchain (ID: hellobtc)

Since the DeFi Summer in 2020, after all these years of development, although the entire track has gradually become more complete and various infrastructures have been derived, after reaching its peak in May 2021, the prices of traditional DeFi blue chips such as UNI, LINK, AAVE, and SNX performed extremely poorly. They seem to be unable to escape the embarrassing situation of being gradually forgotten by the market hotspots, once again verifying the concept of "loving the new and disliking the old" in the circle.

Some time ago, the term "DeFi is an outdated blue chip" was even circulated in the community. Readers have become numb to DeFi. As long as the title of a media article contains DeFi, the number of readers will inevitably not be high. Some people are not even interested in reading it. After all, there is no investment value in the short term. How many people can really be interested in it if it only mentions technology?

But on the other hand, it is undeniable that DeFi (decentralized finance) does not rely on old and inefficient infrastructure, but uses blockchain technology to build a financial system, provide transactions, borrow crypto assets and other services, and has long become an indispensable part of the blockchain industry. Recently, various actions of traditional DeFi blue chips such as UNI and MKR have gradually increased. This article will briefly sort out the changes from DeFi1.0 to DeFi3.0 and introduce the innovations of each stage.

01 DeFi 1.0: Building the basic framework

DeFi1.0 is the initial stage of the rise of decentralized finance. It mainly completed the construction of the basic framework of financial services on the blockchain and introduced several key concepts, such as stablecoins, AMM DEX, borrowing, liquidity incentives, and incentive staking.

Notable developments and innovations in the DeFi 1.0 phase:

The rise of stablecoins such as Tether (USDT), USD Coin (USDC) and DAI, as a medium of exchange of value, provides a foundation for transactions and lending in the DeFi ecosystem;

The emergence of AMMs (automated market makers) and liquidity incentives, powering DEXs like Uniswap and Curve, enabling peer-to-peer trading without the need for intermediaries;

The emergence of lending platforms such as AAVE and Compound allows users to earn interest on their crypto assets or use crypto assets as collateral for lending;

The emergence of incentivized staking, which rewards users with governance tokens to motivate them to provide liquidity to DeFi platforms, has served as the main catalyst for the development of DeFi, increasing DeFi TVL from hundreds of millions to tens of billions.

DeFi1.0 is the construction of the DeFi basic framework and plays a vital role in the development of DeFi. However, there are also some problems.

The development of DeFi 1.0 is mainly concentrated on Ethereum. Due to Ethereum's own scalability issues, the cost of user participation is not low. In addition, although incentive staking has achieved great success in DeFi, liquidity providers come for high rewards and have no loyalty at all. Once the rewards are cancelled, customers will be lost, which will lead to a sharp drop in prices and the project will enter a death spiral.

Moreover, when the token price fluctuates greatly, the liquidity provider will also face the risk of loss (impermanent loss). Liquidity is distributed on different platforms, and splitting liquidity and providing liquidity will also lock up funds, resulting in low capital efficiency.

Despite various problems, these projects have laid the foundation for the current development of DeFi and found the direction for subsequent development. The project parties work hard to overcome these challenges and push the ecosystem further.

02 DeFi 2.0: Product diversification and improved capital efficiency

DeFi2.0 aims to solve the existing problems of DeFi1.0 while expanding its functionality.

Notable developments and innovations in the DeFi 2.0 phase include:

The number of DeFi protocol forks of other public chains such as BSC, Solana, and Fantom has increased sharply. The emergence of cross-chain protocols has promoted asset bridging. The outbreak of new public chains is everyone's effort to circumvent Ethereum's scalability issues.

AAVE, Uniswap, Sythetix and other established DeFis have begun to support other public chains;

The increase in Layer2 solutions has improved Ethereum’s scalability and reduced costs;

Build novel financial products based on DeFi 1.0, such as derivatives, smart pools, DEX aggregators, etc.;

The development of decentralized autonomous organizations (DAOs) has gained traction, enabling communities to collectively govern DeFi protocols;

The emergence of ve governance tokens, (3,3) models, and ve(3,3) models enable the interests of users and protocols to remain consistent for a relatively long period of time, thereby motivating them to contribute to the development of the protocol. The core of ve is that users obtain non-transferable and non-circulating governance veTokens by locking tokens. The longer the lock-up period, the more governance veTokens can be obtained. Users obtain a corresponding proportion of voting rights based on the proportion of veTokens, giving them the right to participate in community governance. Representatives of these are Curve and OlympusDAO (3,3) models, which are developed in GMX;

Uniswap launched version V3, which centralizes liquidity and allows users to choose to provide liquidity in custom price ranges, improving capital efficiency and flexibility.

Compared with DeFi 1.0, DeFi 2.0 has brought about a significant expansion of products and functions, marking a major change in the entire DeFi ecosystem. The perfect development of DeFi also means that opportunities are decreasing, and people's attention is gradually shifting from it to other concepts, such as the metaverse NFT, Layer2, AI, etc.

03 DeFi 3.0: Fixed-income products

With the continuous development of DeFi, the basic framework has been built, the TVL market size has grown from zero to more than 43 billion US dollars now, and the total market value of cryptocurrencies has reached about 1.2 trillion US dollars. The crypto industry is gradually becoming mature and complete, and the capital retention in the industry is increasing. Many users have become accustomed to investing in the industry and are optimistic about the future development of the industry, rather than cashing out the money immediately after making money. Therefore, with the increase of idle assets in the industry, the demand for how to obtain stable returns is also gradually increasing.

The ETH staking yield of more than 4% and the annualized yield of US Treasury bonds of about 5% in the market just meet this demand. Therefore, the development of DeFi gradually shifts to these two lines: inward development - LSDFi, outward development - RWA.

Inward LSD—LSDFi

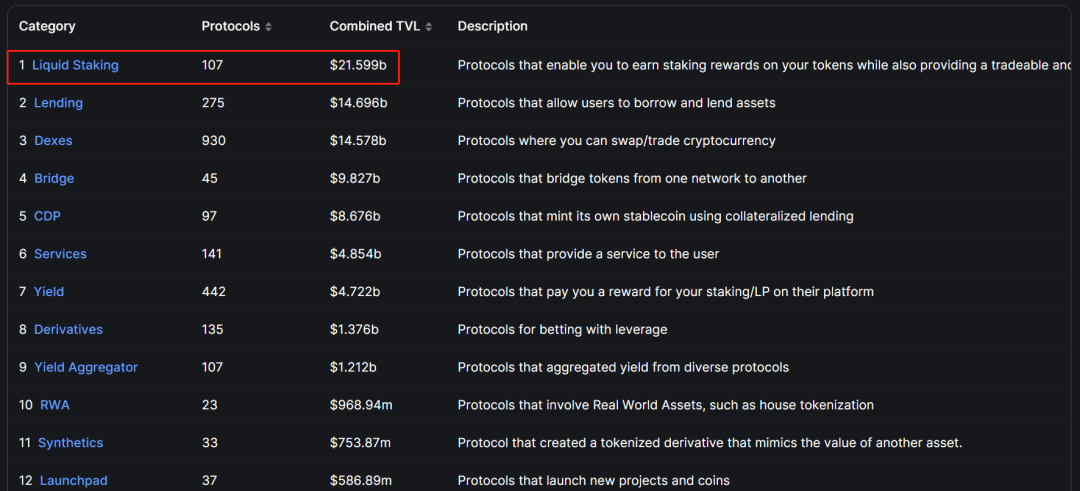

As of July 28, the total locked volume of DeFi was approximately US$43.2 billion, and Ethereum staking increased from zero in 2020 to more than US$40 billion now, of which the LSD track accounted for more than US$21 billion, accounting for about 50% of DeFi's total TVL. It has become the largest track in DeFi. It can be said that LSD has developed into an indispensable part of DeFi, and in the future, as the market value and staking rate of Ethereum increase, its share will become larger and larger.

The emergence of liquid pledge derivative solutions such as Lido, Frax, and RPL has provided greater liquidity for pledged assets. At the same time, with the gradual improvement of the LSD track and the continuous expansion of the Ethereum pledge market, LSD is also developing vertically, deriving LSDfi, which achieves higher returns through layers of nesting dolls. For more information about LSDfi, please refer to Baihua’s previous article "After the Ethereum Shanghai upgrade, the pledge volume did not decrease but increased, and the call for LSDFi rose."

Binance Research’s Classification of LSDfi

Outward RWA

RWA, Real World Assets (RWAs), is the tokenization of real-world assets. The concept of RWA was first proposed in 2017, when assets such as real estate and luxury goods were put on the chain, but ultimately failed to take off. However, with the development of DeFi over the years, the concept of RWA has found a fertile ground for development.

In the first half of this year, the relevant concept was brought up again, and some traditional institutions began to test the waters. Goldman Sachs launched the GS DAP platform to help the European Investment Bank (EIB) issue 100 million euros of digital bonds; private equity firm Hamilton Lane tokenized part of its equity funds and sold them to investors; Siemens issued 60 million euros of digital bonds on the blockchain; Bank of China International (BOCI) announced a partnership with UBS to issue tokenized notes worth 200 million yuan.

In addition, in the field of Crypto, old DeFi protocols such as MakerDAO, Aave, and Compound have also begun to target the RWA track, making the related concept gradually hot. According to CoinMarketCap data, the total market value of RWA concept tokens exceeds US$2.5 billion.

The RWA mentioned so far is mainly divided into two categories. One is that on-chain assets are invested off-chain to obtain income, and the other is that off-chain assets are put on-chain and obtain economic benefits. Realize the interoperability of on-chain and off-chain assets, increase liquidity and earn income at the same time. At present, the most popular RWA concepts are digital dollars USDT, USDC, DAI, etc., that is, mapping U.S. debt to the chain and tokenizing it.

What are the projects related to the RWA track?

MakerDAO: In 2022, MakerDAO co-founder proposed the MakerDAO Endgame plan to introduce some RWA assets as collateral for the stablecoin Dai. MakerBurn data shows that a total of 11 RWA projects have been introduced, with $2.48 billion in assets as collateral for MakerDAO, accounting for 53% of its total assets and contributing 53.9% of its revenue;

AAVE: AAVE will launch the RWA market in 2021, allowing collateralized lending of real assets. Data shows that the Aave RWA market size is only 76.65 million US dollars. However, with the launch of the stablecoin GHO, RWA will be introduced like DAI.

Superstate: A new company founded by the founder of Superstate Compound, seeking to tokenize U.S. debt on Ethereum;

Centrifuge: Centrifuge is one of the earliest DeFi protocols involved in RWA, and the technology provider behind protocols such as MakerDAO and Aave. Currently, Centrifuge has a total of 17 RWA asset pools with a total value of US$230 million.

Ondo Finance: Ondo Finance is a decentralized investment bank. It mainly invests in U.S. listed money market funds off-chain. On-chain, it cooperates with the decentralized lending protocol Flux Finance to provide stablecoin lending services. It launched a tokenized fund at the beginning of the year, allowing stablecoin holders to invest in bonds and U.S. Treasuries.

Maple Finance: Maple Finance's mainstream business is lending/institutional credit lending. In April, it announced plans to launch a lending pool that invests in U.S. Treasury bonds to expand its lending model with real assets as collateral.

RealT: RealT is a compliant real estate tokenization platform established in 2019. It has processed over $52 million in real estate tokenization, and more than 970 houses have been tokenized on the RealT platform.

Toucan: Toucan converts carbon credits into tokens and uses DeFi to facilitate the trading of carbon credits.

04 Summary

The above is the development path of DeFi. It can be seen that the development direction of the blockchain industry is to continuously optimize and improve on this basis when bottlenecks or deficiencies appear in its original technology.

Is DeFi really going to fail? In fact, LSD had already exploded at the beginning of the year, and the concept of RWA has been mentioned repeatedly in recent months.

Do you think LSD and RWA will be the future of DeFi? Or are there other possibilities? Welcome to comment, exchange and discuss.