Reference reading: "Understand what the CFTC position weekly report is in one article"

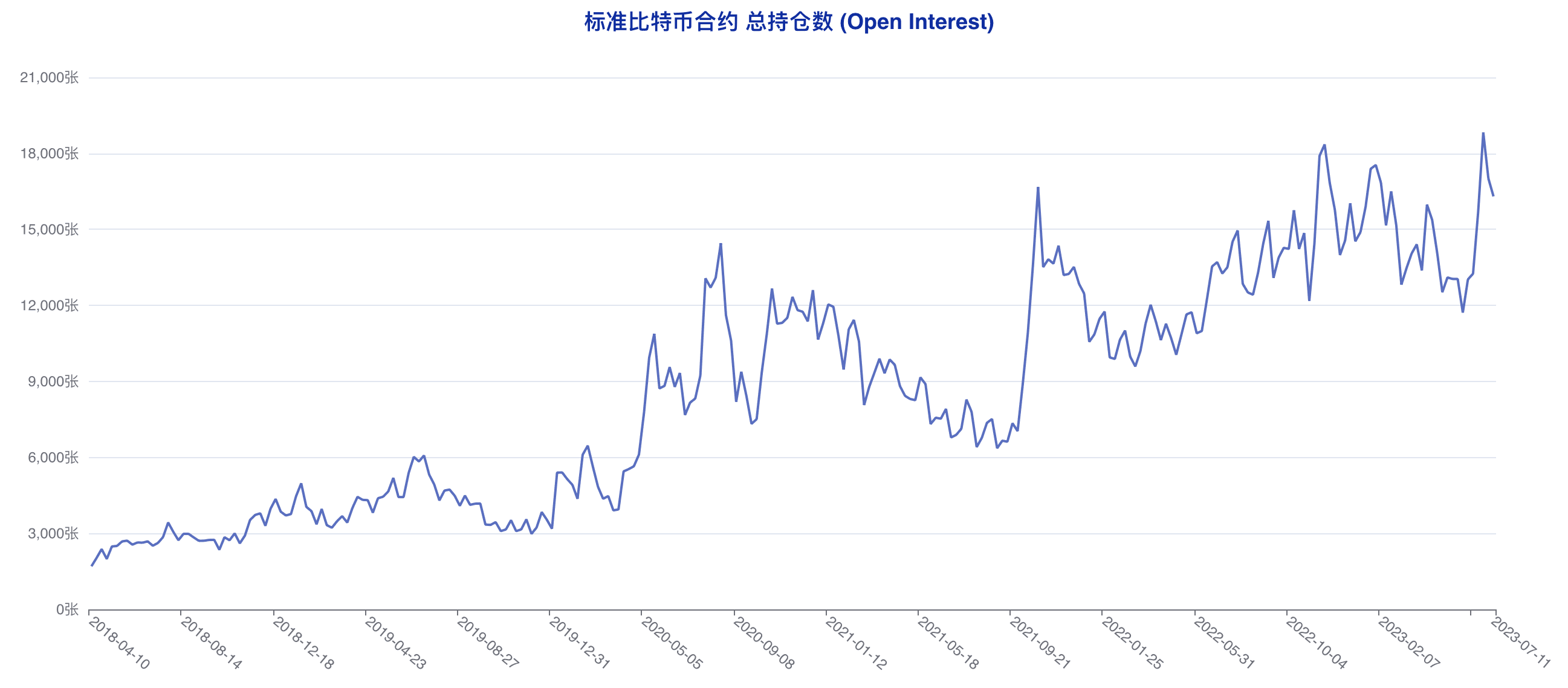

The latest CFTC CME Bitcoin Position Weekly Report (July 5 - July 11) released on July 15 showed that the total open interest of Bitcoin standard contracts further fell from 17008 to 16302. During the statistical period, the price of Bitcoin remained in a narrow range of about US$500. The lack of a clear unilateral preference in the market has exacerbated the wait-and-see sentiment in the short-term market, which in turn caused the total open interest to further decline.

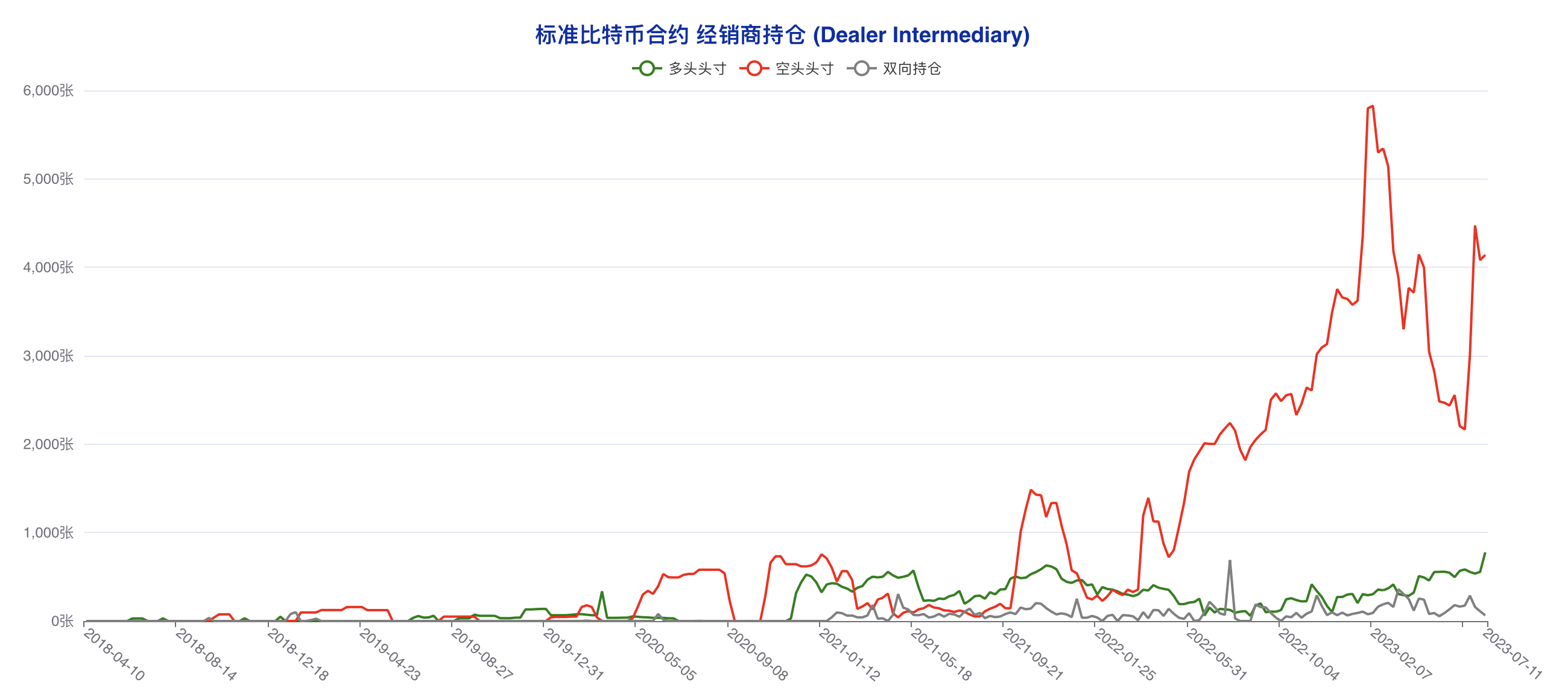

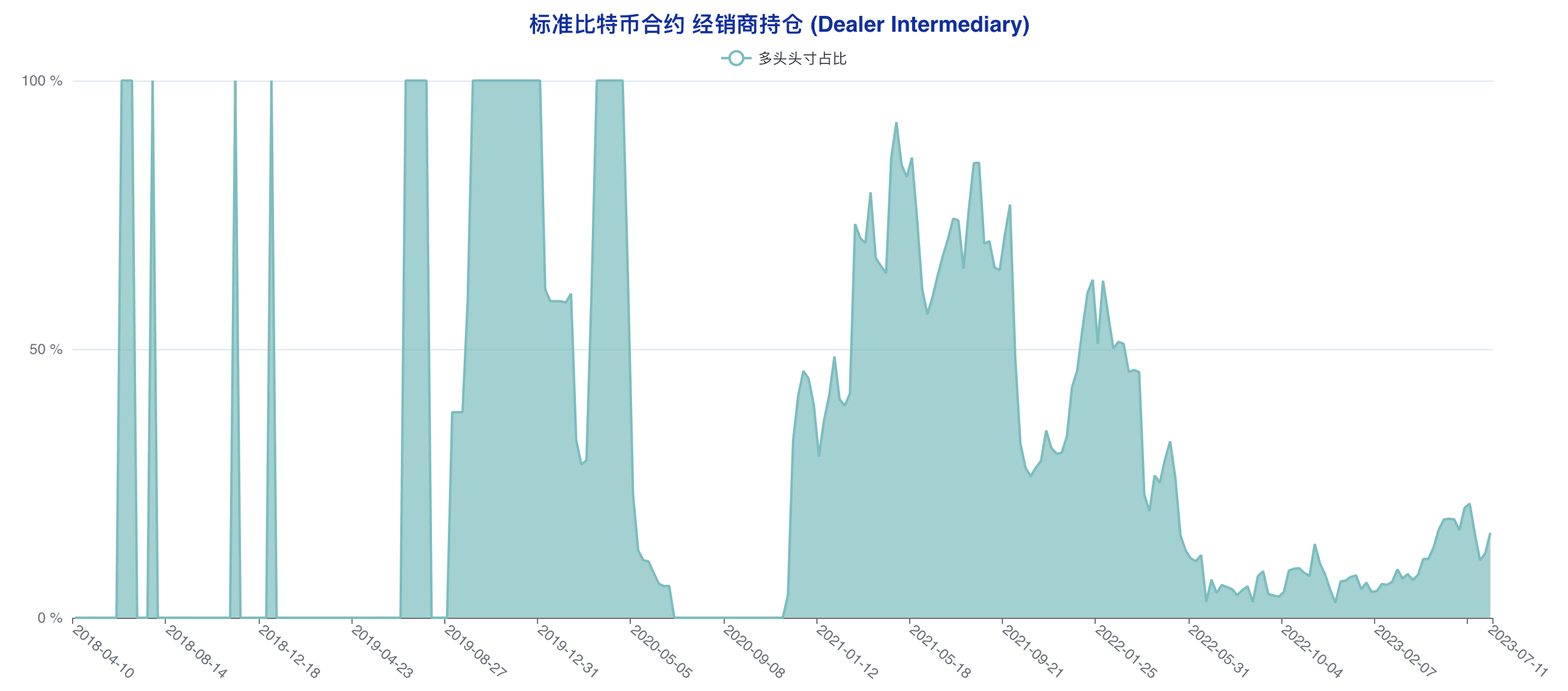

The long position of the largest dealer account increased from 556 to 777. This value unexpectedly hit a record high under this market background. The short position simultaneously increased from 4081 to 4140. Although this type of account continued to perform during the latest statistical period The two-way simultaneous accumulation of long and short positions did not continue the idea of net long position adjustment in the previous statistical period. However, the performance of long positions hitting a record high cannot be ignored. Judging from the performance of net long position adjustment in the previous statistical period, large institutions There is no doubt that the optimistic attitude towards the market outlook is evident.

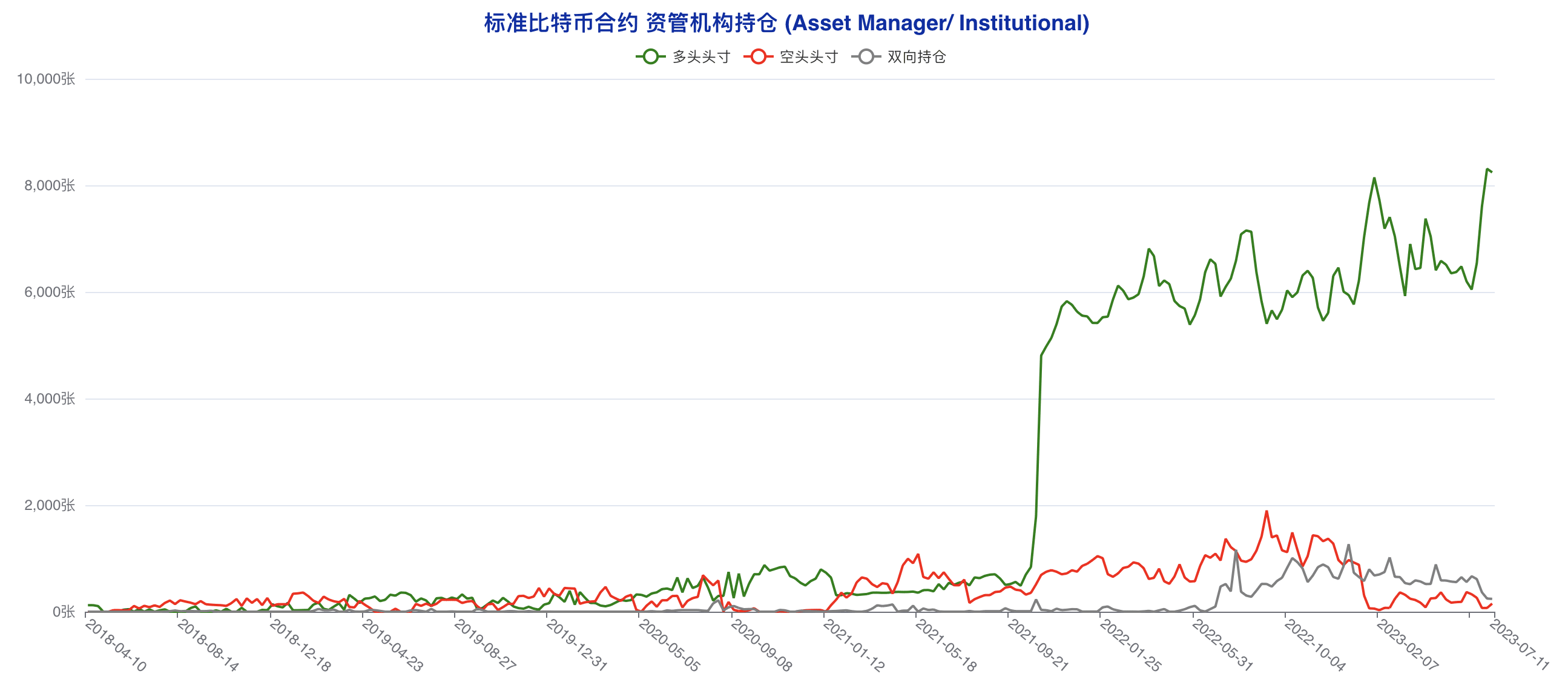

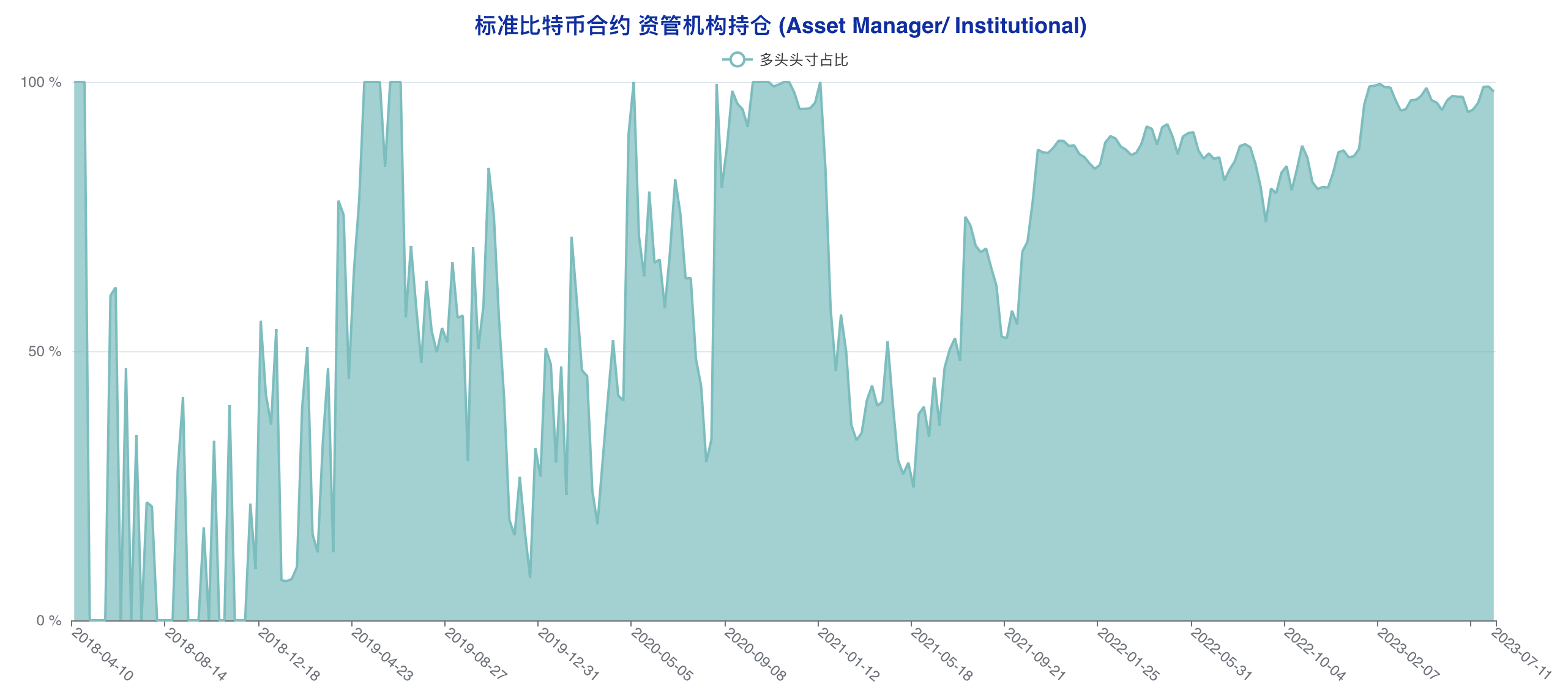

The long positions of asset management institutions decreased from 8311 to 8243, and the previous four-week upward trend came to an end. The short positions increased from 70 to 152. Asset management institutions carried out a long-awaited net cold adjustment in the latest statistical period, and the proportion of long positions declined slightly. The firm bullish attitude expressed by such accounts in the face of volatile market has loosened slightly, but considering that the adjustment range is not large, such accounts as a whole are still in the optimistic camp.

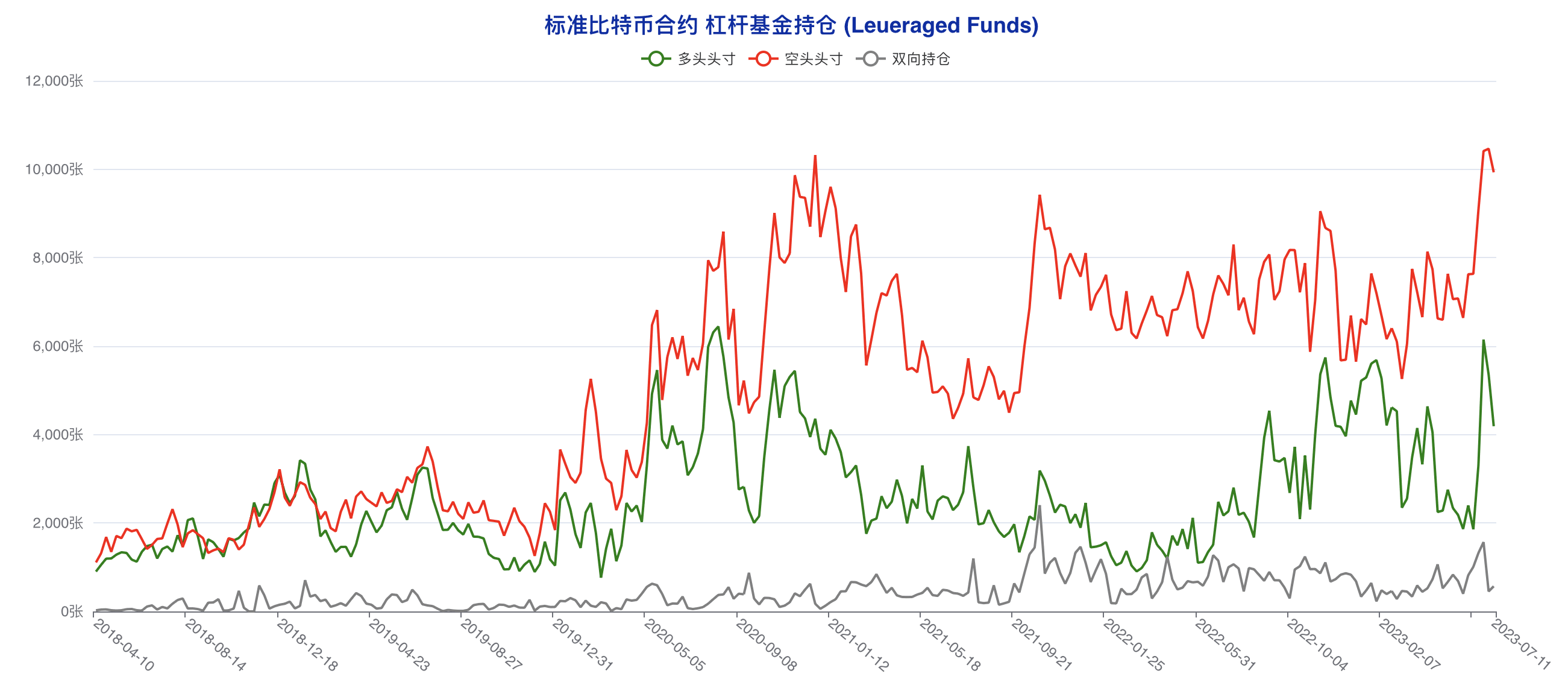

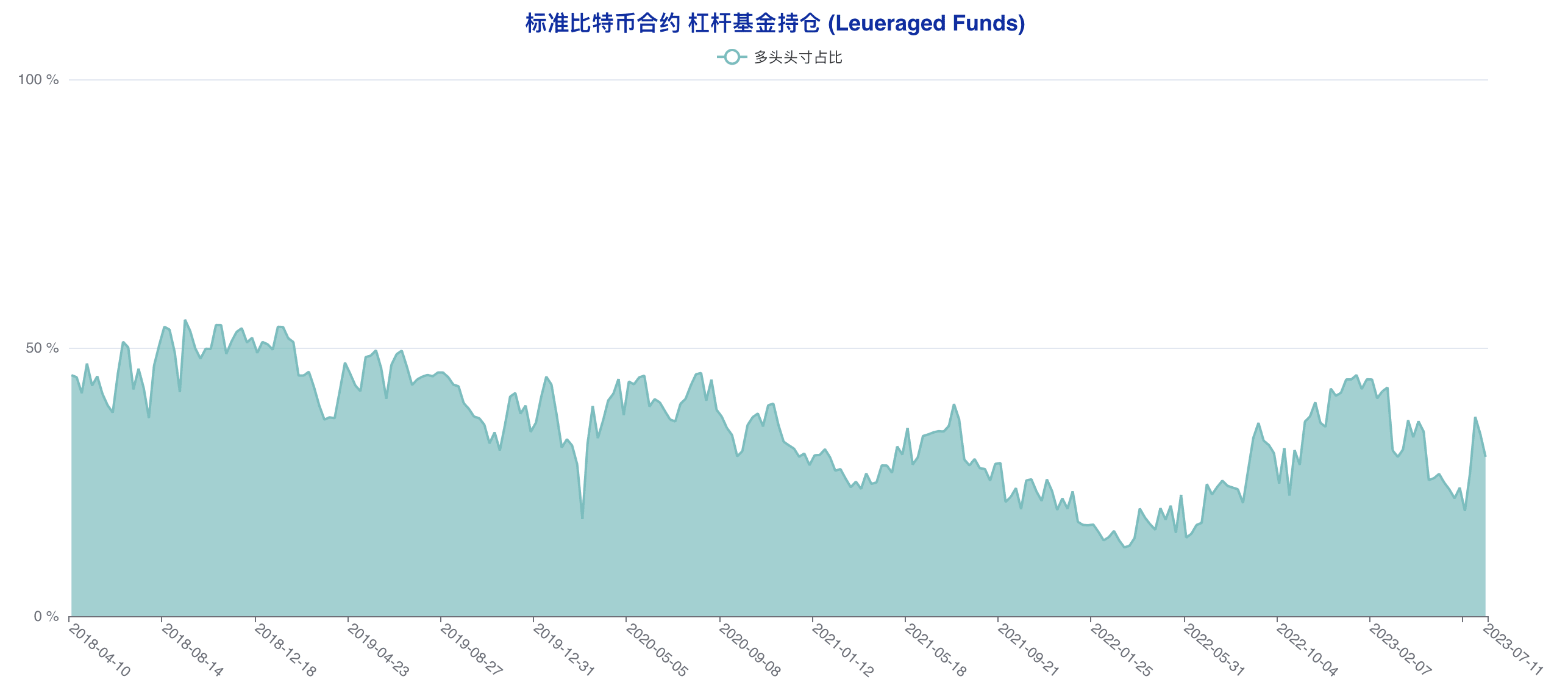

The leveraged fund long position decreased from 5356 to 4189, and the short position decreased from 10464 to 9931, which is a decline from the historical high. This type of account has carried out a two-way reduction of long and short positions in the latest statistical period. After the relatively aggressive net air conditioning in the previous statistical period, the proportion of long positions has further decreased significantly, and this type of account has continued to have a bearish attitude towards the future market.

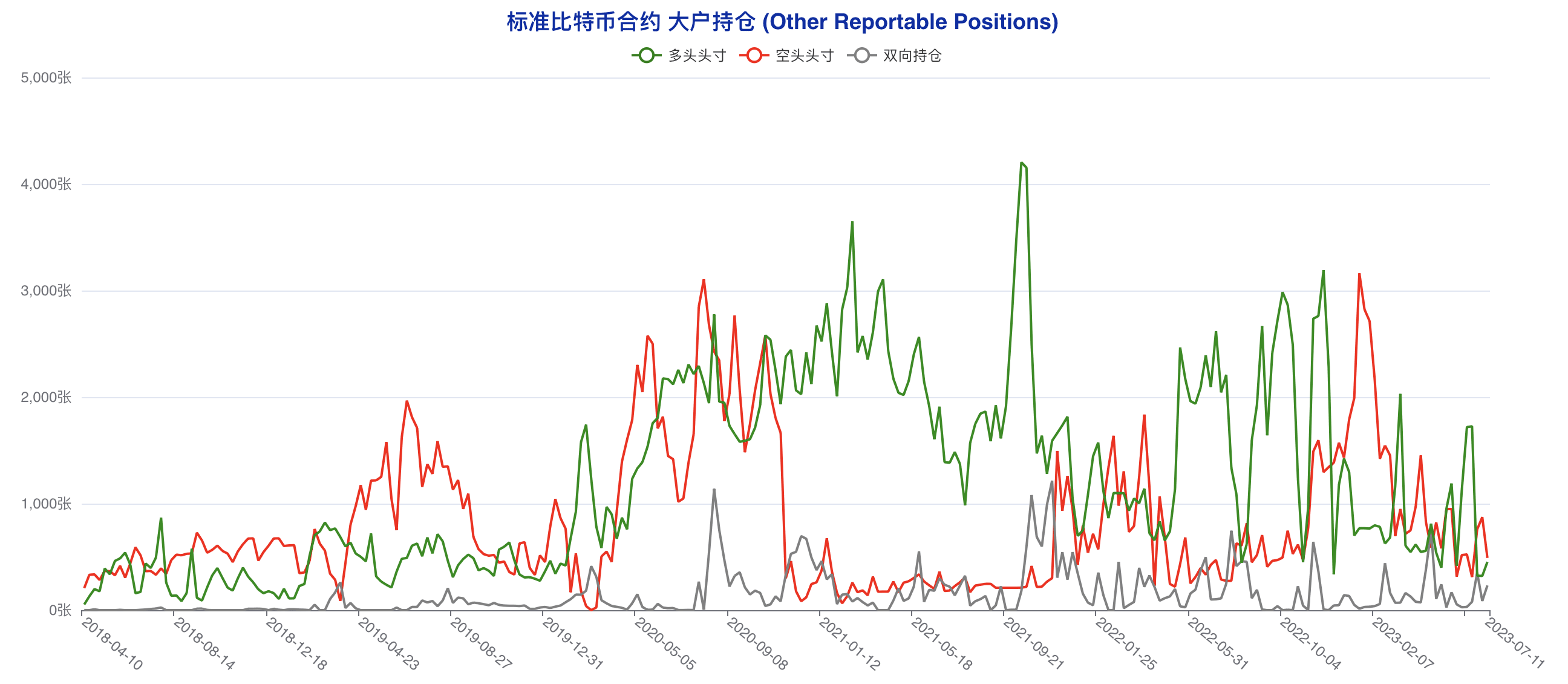

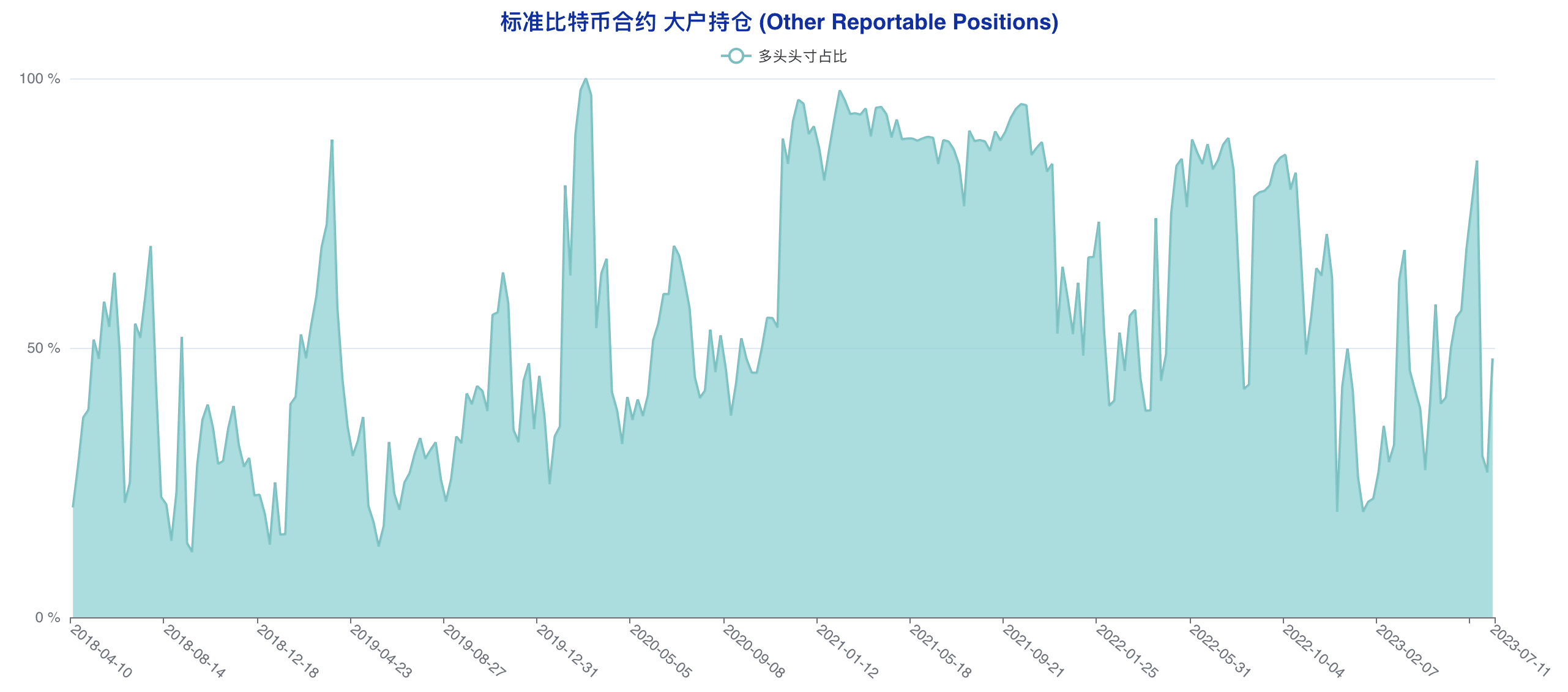

The long positions of large accounts increased from 321 to 453, and the short positions decreased from 873 to 490. Large accounts made a clear net long adjustment in the latest statistical period, and the long and short positions quickly approached an approximately equal level. Such accounts changed their bearish attitude in the previous statistical periods to a bullish one. The "defection" of such accounts means that the short-term short-side power has been further weakened.

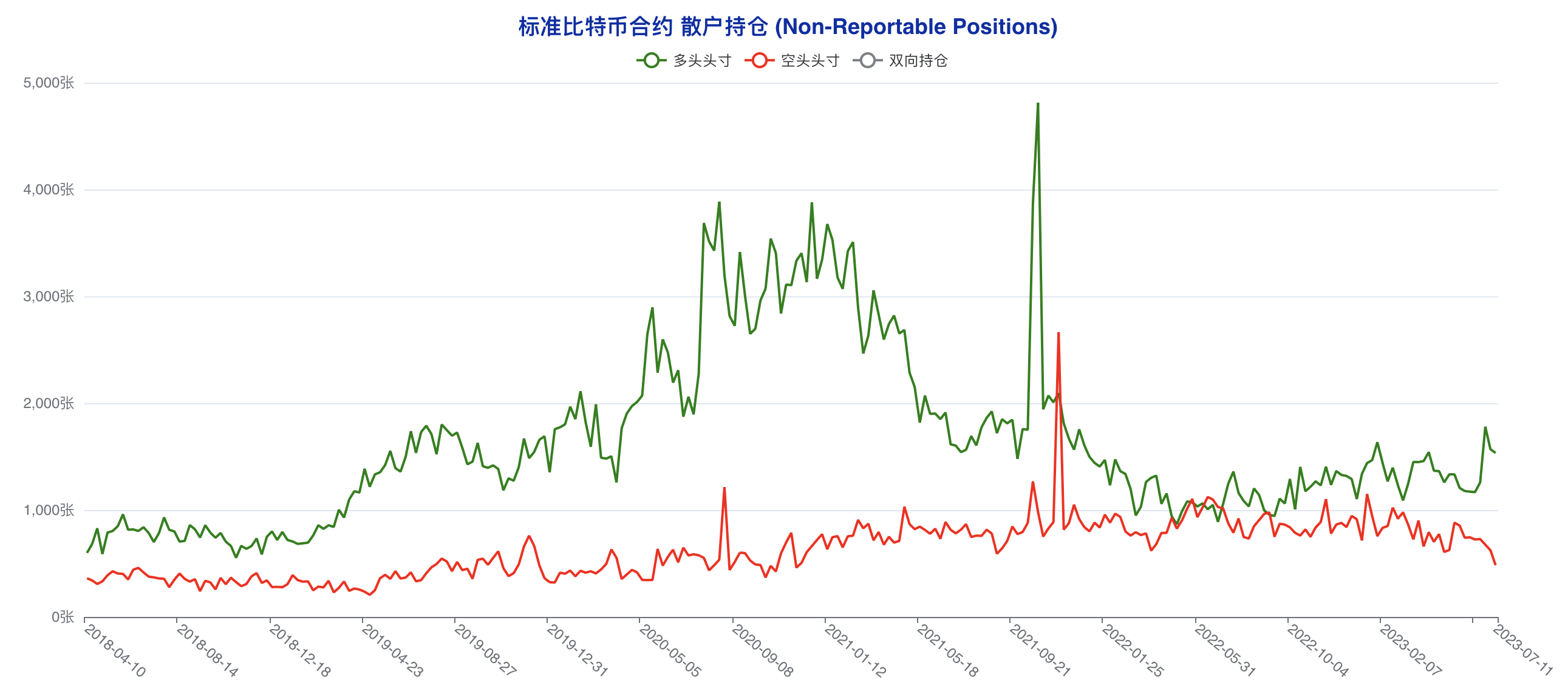

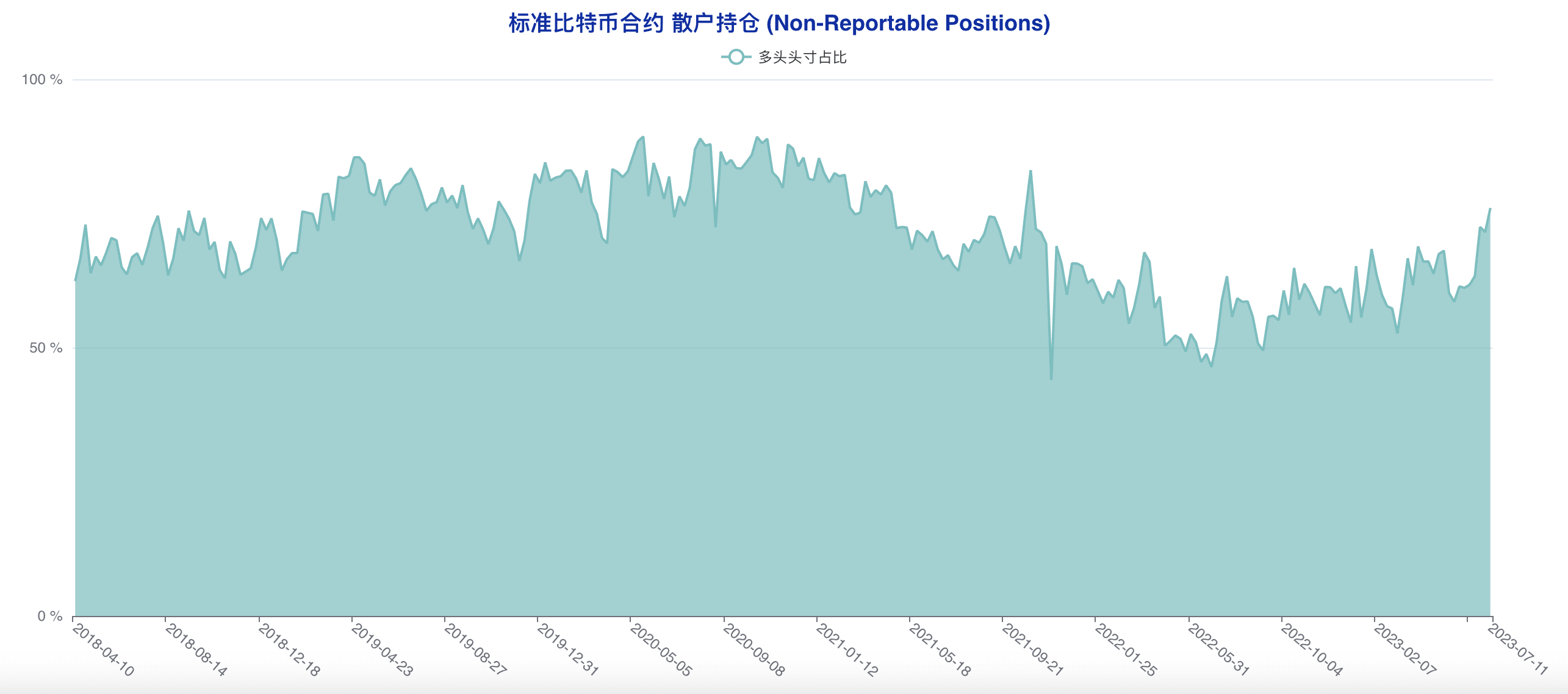

The retail investors’ long positions dropped from 1568 to 1535, and the short positions dropped from 624 to 484. Retail investors reduced their long and short positions simultaneously during the latest statistical period. The overall position adjustment was very limited, and there was no clear preference between long and short positions.

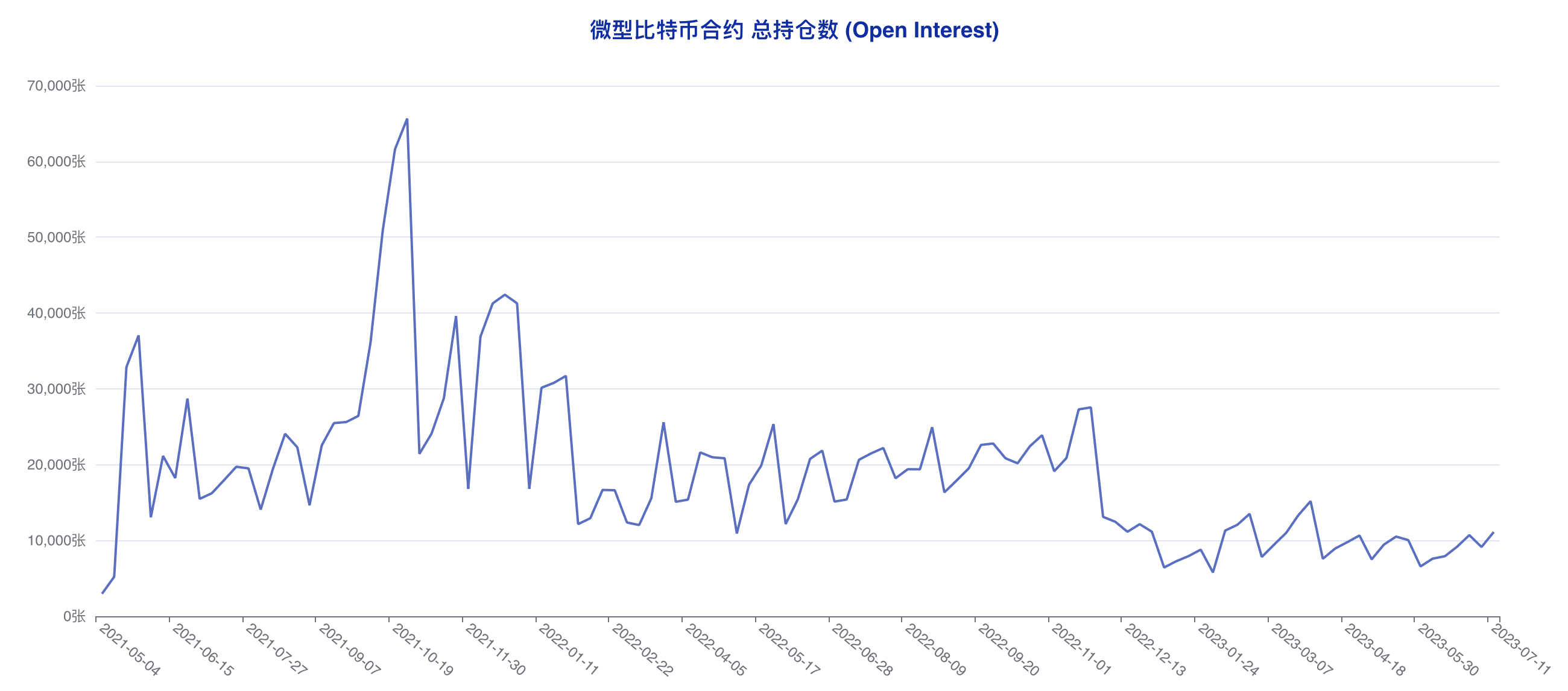

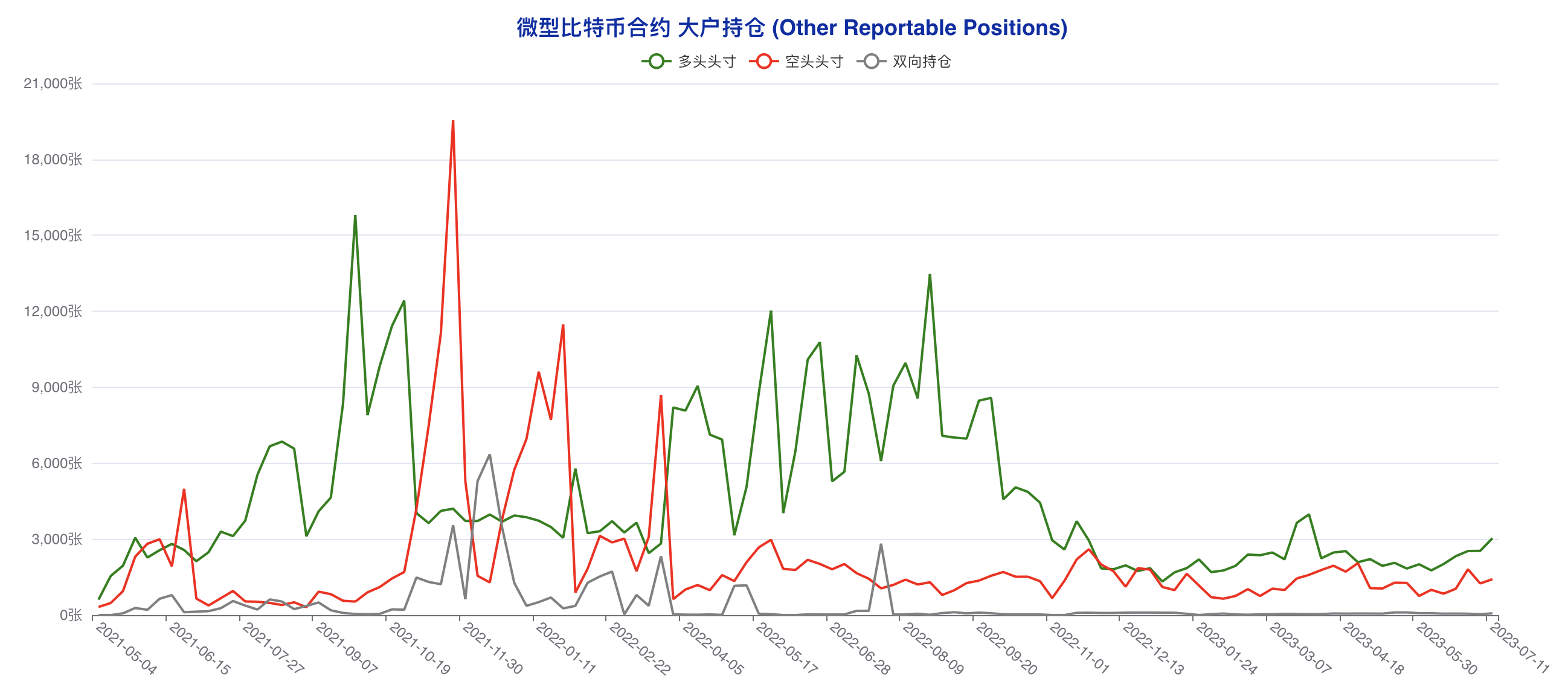

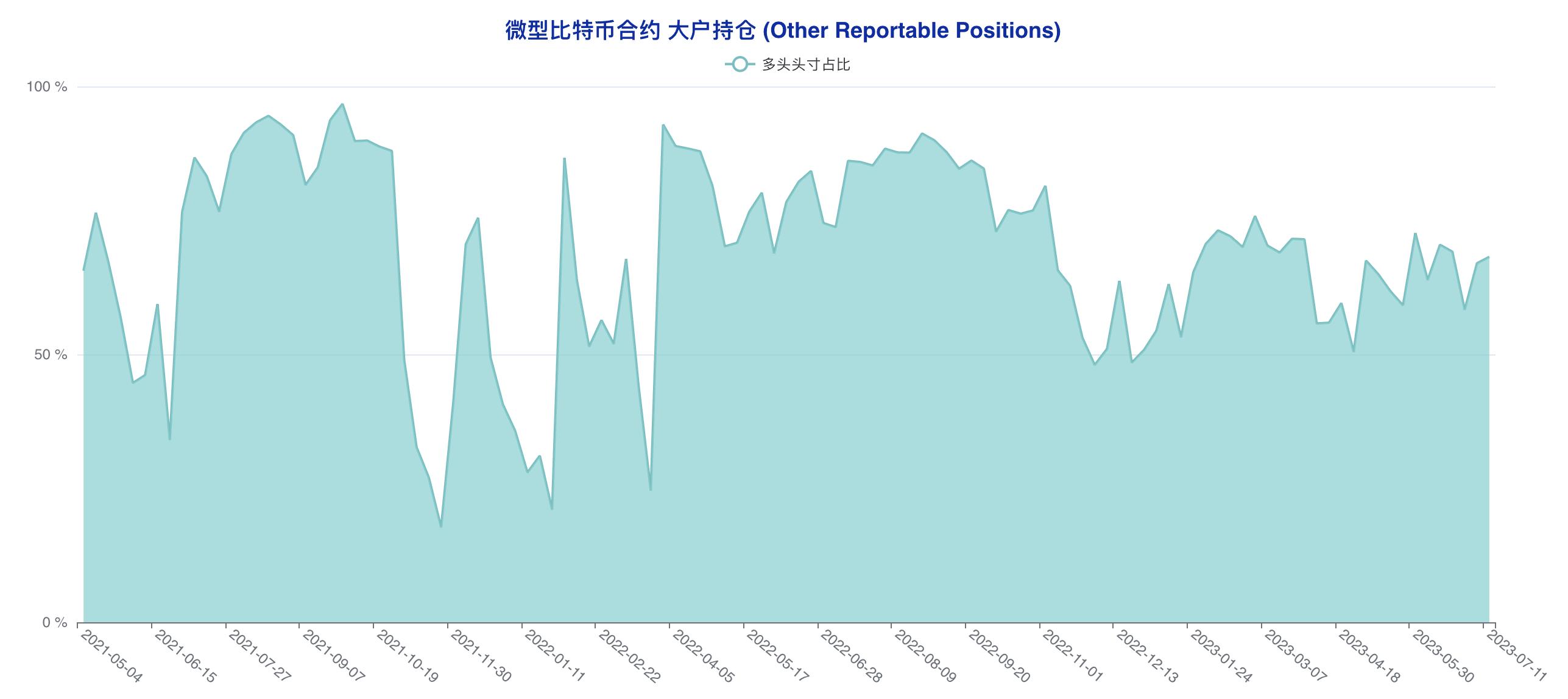

Total open interest in Bitcoin micro contracts rose from 9,138 to 11,107.

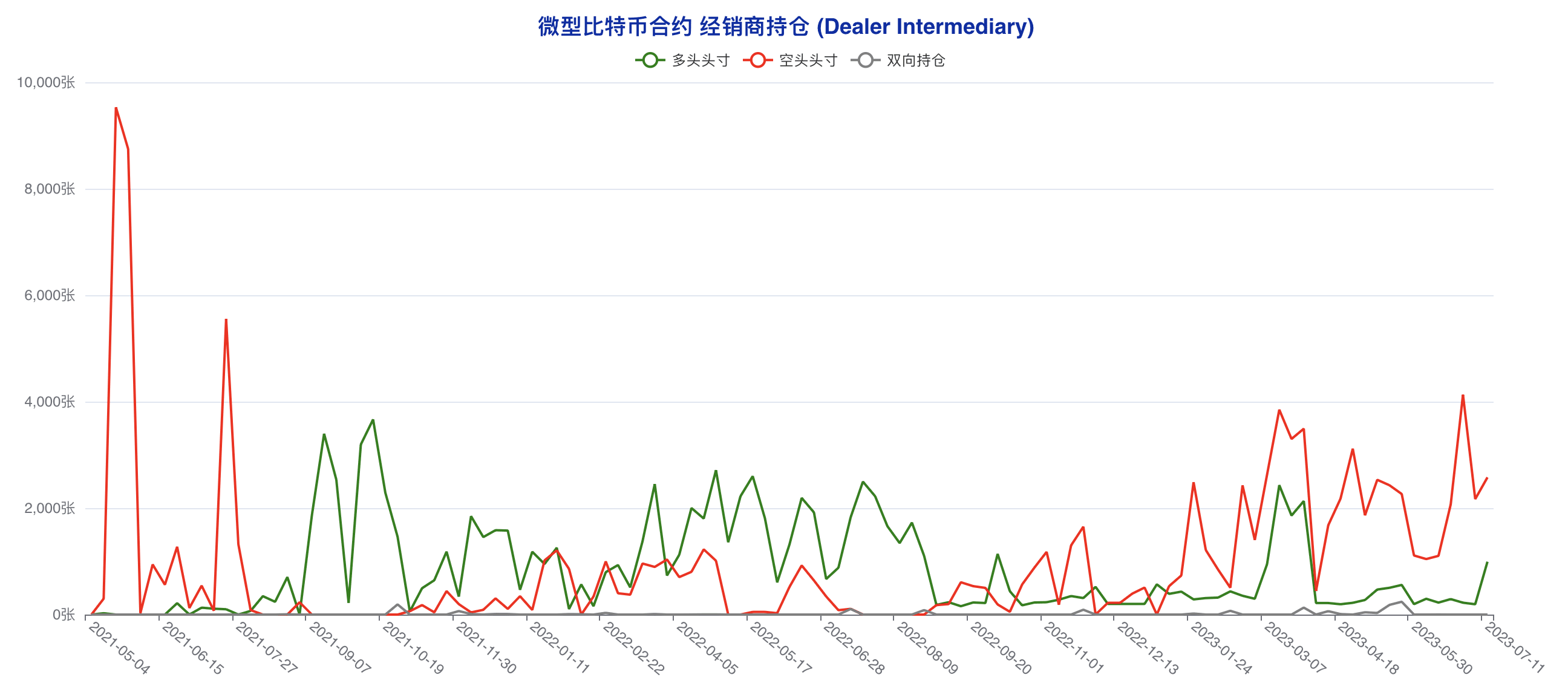

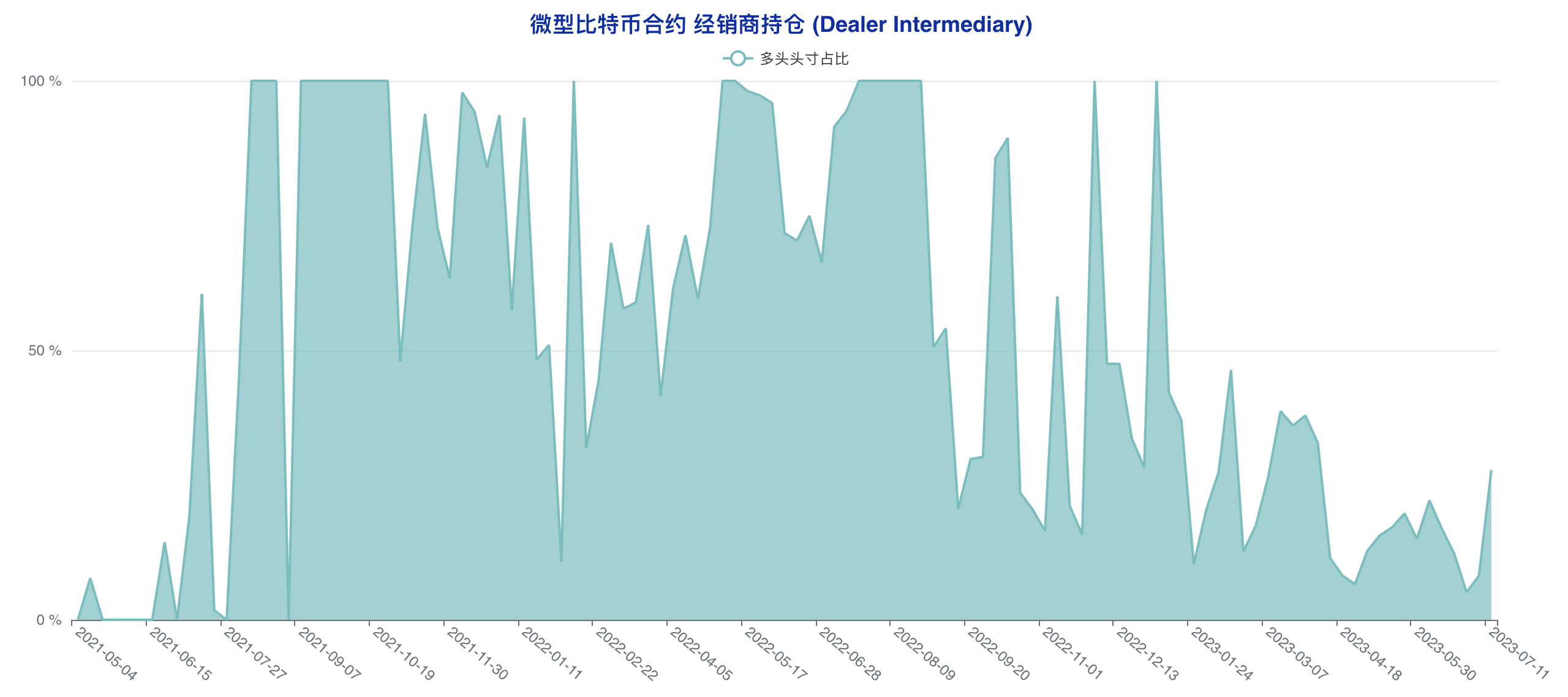

The long positions of dealer accounts increased from 194 to 993, and the short positions increased from 2170 to 2578. This type of accounts increased their long and short positions in micro contracts at the same time, and the proportion of long positions increased significantly, which consolidated the bullish attitude of this type of accounts towards the future market.

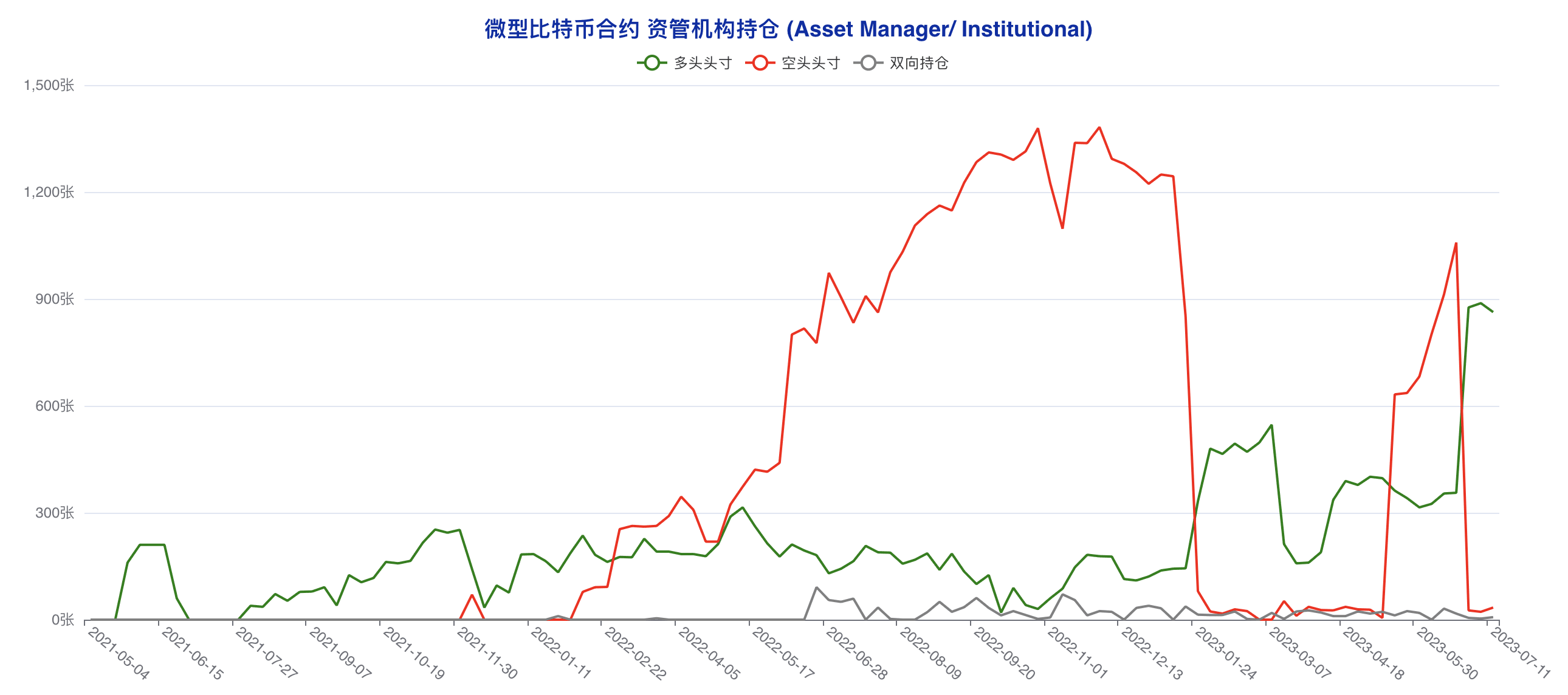

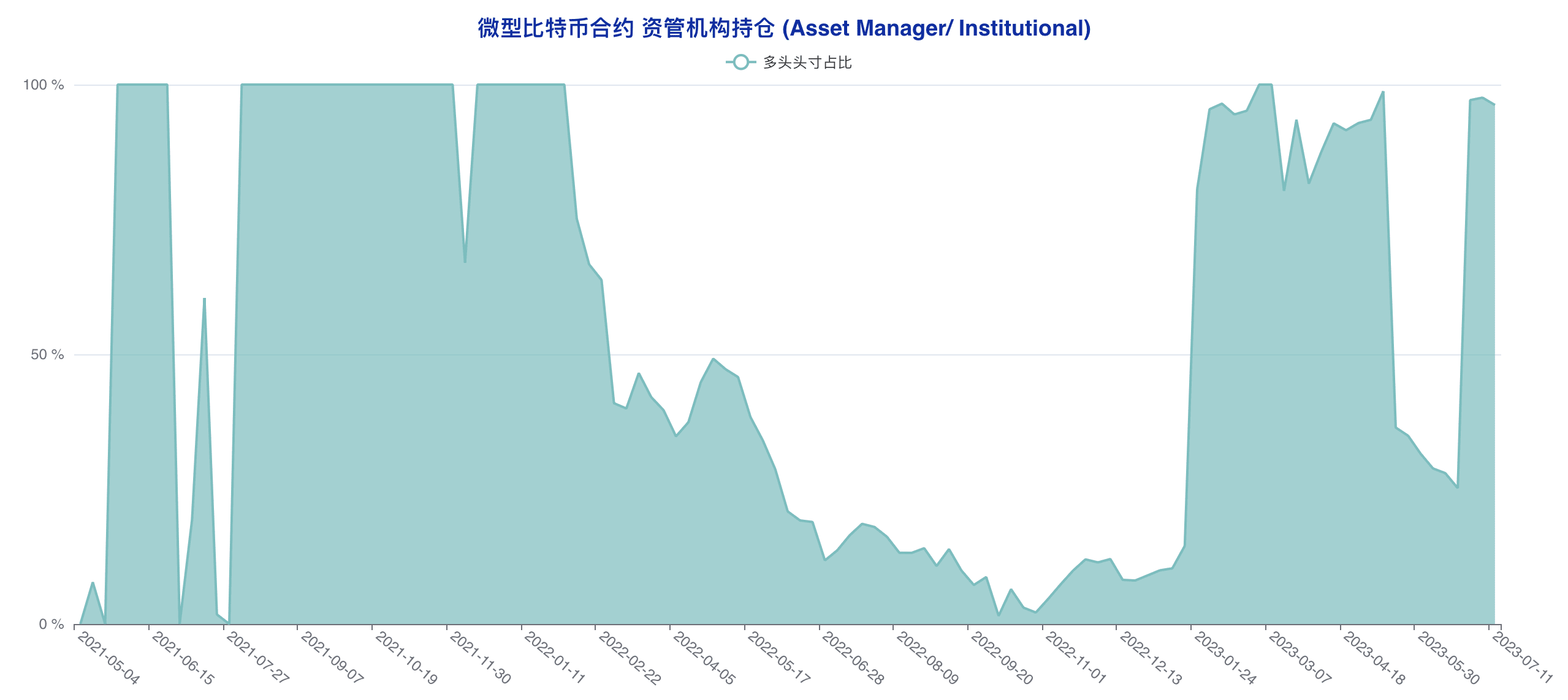

The long position of the asset management institution account decreased from 888 to 863, and the short position increased from 22 to 34. The asset management institution conducted a net cold position adjustment in the micro contract, which is a risk hedging operation when combined with the standard contract.

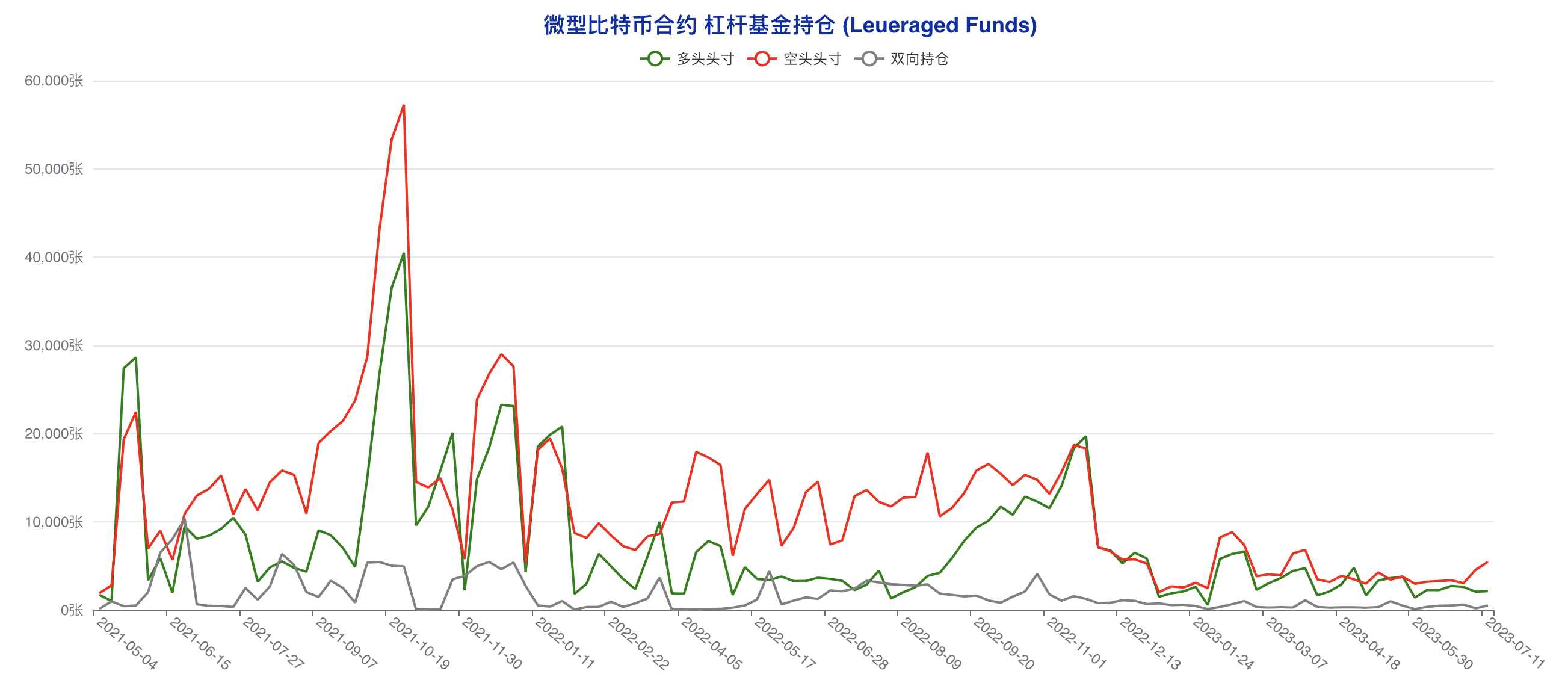

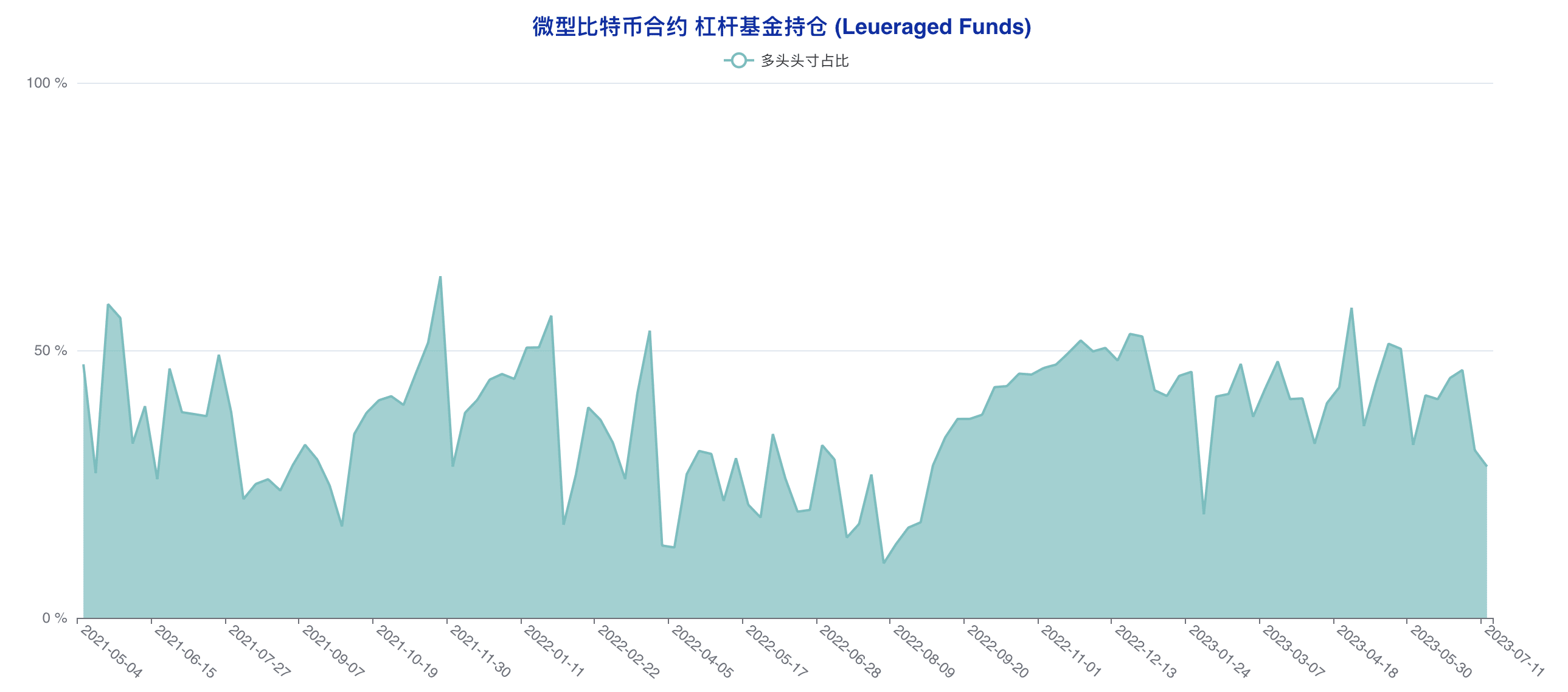

Leveraged fund long positions increased from 2093 to 2159, and short positions increased from 4585 to 5477. Leveraged funds increased their long and short positions simultaneously during the latest statistical period, and the proportion of long positions decreased, consolidating the bearish attitude expressed in the standard contract.

The long positions of large investors increased from 2536 to 3037, and the short positions increased from 1249 to 1416. This type of accounts increased their long and short positions simultaneously during the latest statistical period. Since the long-short position ratio did not change much, the information that can be interpreted is limited.

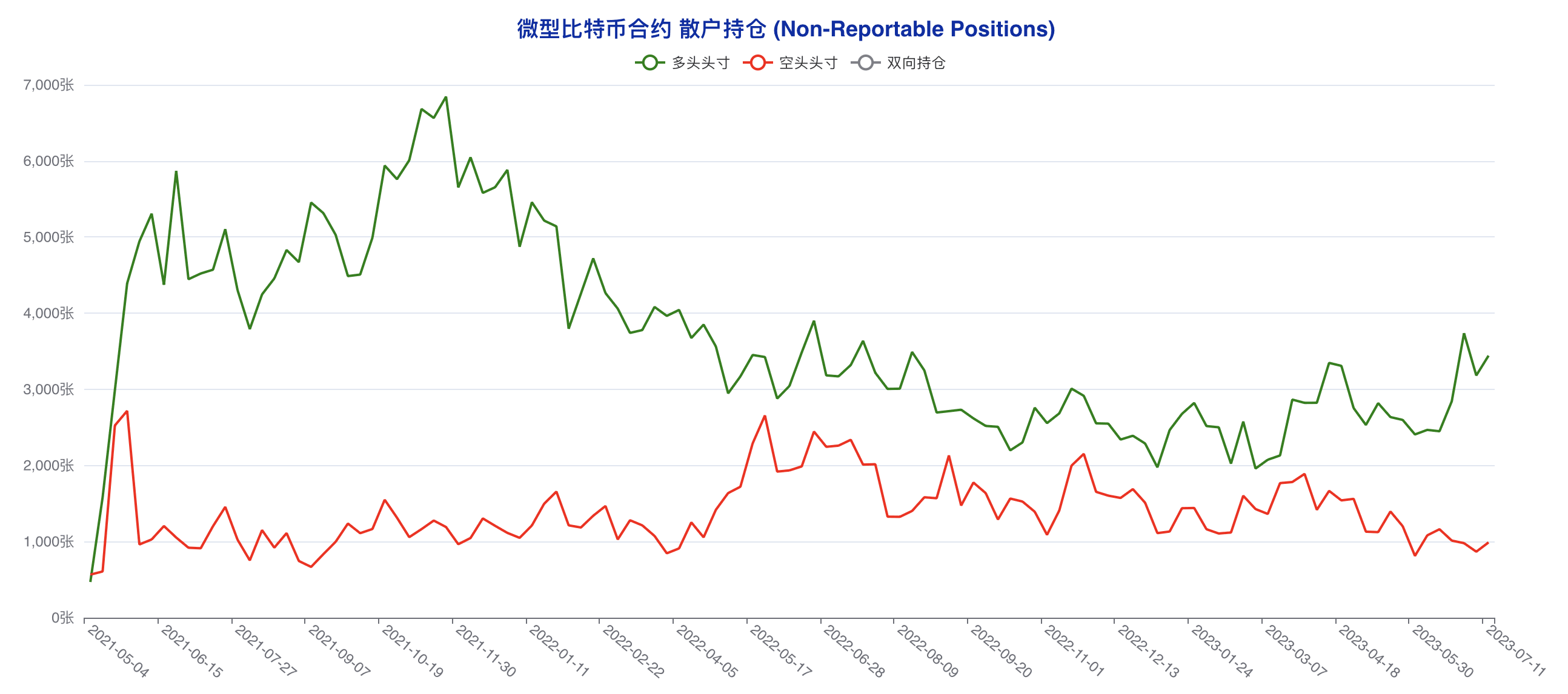

Retail long positions increased from 3182 to 3442, and short positions increased from 867 to 989.