Original English link: https://www.nervos.org/knowledge-base/understanding_nervos_ckb_issuance_model

Bitcoin’s most important value proposition in the economic field is its fixed issuance mechanism, which does not change due to any factors, and is also predictable, so that we can know the production and timing of new coins. For example, we know that the last Bitcoin will be mined around 2140. The total supply of 21 million sums it up. In contrast, Ethereum does not have a fixed and predictable monetary policy because it has been adjusted many times, such as the implementation of EIP-1559.

Nervos shares the same philosophy and value proposition as Bitcoin, as CKB’s primary and secondary issuance are also fixed and predictable. The primary issuance, like Bitcoin, is halved approximately every 4 years, while the secondary issuance remains unchanged, which means that CKB’s inflation rate will decrease year by year and eventually approach zero.

This value proposition is important because it provides a stable and predictable monetary policy for network participants (whether miners, developers, investors, companies or users), safeguarding their legal and economic interests. For example, in the business world, legal certainty is crucial when investing in new jurisdictions, as it ensures investors' economic prospects. In addition, it allows the operating costs of the network to be calculated in a simpler and more precise way, such as when purchasing mining equipment.

We believe that for a network centered on preservation and storage of value, the monetary policy and issuance schedule of Nervos CKB must be completely fixed, which is also one of the three constants of the Nervos network.

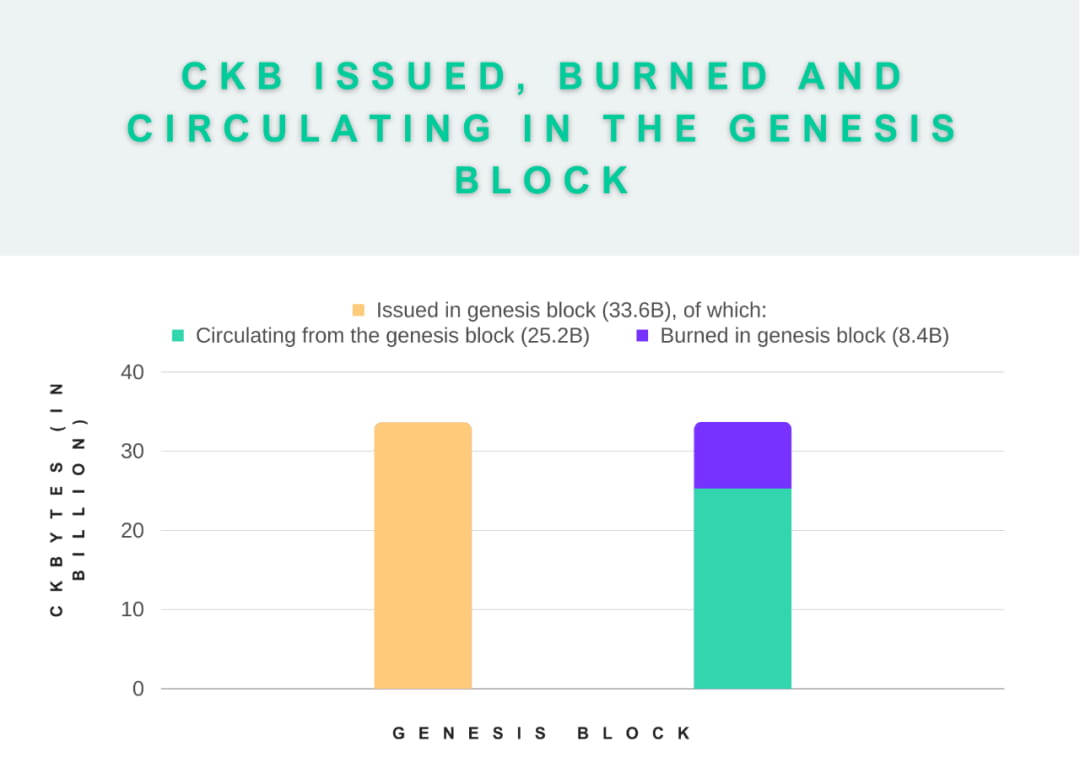

Genesis Block

In the genesis block, the initial issuance of CKB is 33.6 billion, of which 25%, or 8.4 billion CKB, are immediately destroyed and will never enter circulation. Therefore, the circulation of CKB in the genesis block is 25.2 billion.

It is important to note that "burned" is not the same as "unissued". The 8.4 billion CKB that have been issued but not circulated (burned) will affect the secondary issuance because of the 25% destroyed in the genesis block, 15% (i.e. 5.04 billion CKB) are hard-coded as "occupied" capacity, and the other 10% (i.e. 3.36 billion CKB) are hard-coded as "liquid" state, i.e. not occupying capacity. This means that even if no CKB is used to store state, or all circulating CKB is deposited in the Nervos DAO, miners and the treasury will still receive CKB issued in the secondary issuance.

Note: Secondary issuance is not always 15% to miners and 10% to the treasury. As more and more CKB is mined, this number will decrease. The “at least” mentioned in the above picture refers to the moment when the mainnet is launched.

Therefore, when we discuss issued CKB below, we will include the 8.4 billion CKB that were destroyed. For example, when calculating inflation data, we will consider all 33.6 billion CKB issued in the genesis block. If we talk about CKB in circulation, we will use the number of 25.2 billion and exclude the 8.4 billion CKB that were destroyed.

The two major components of the CKB issuance mechanism: primary issuance and secondary issuance

Primary issuance (basic issuance)

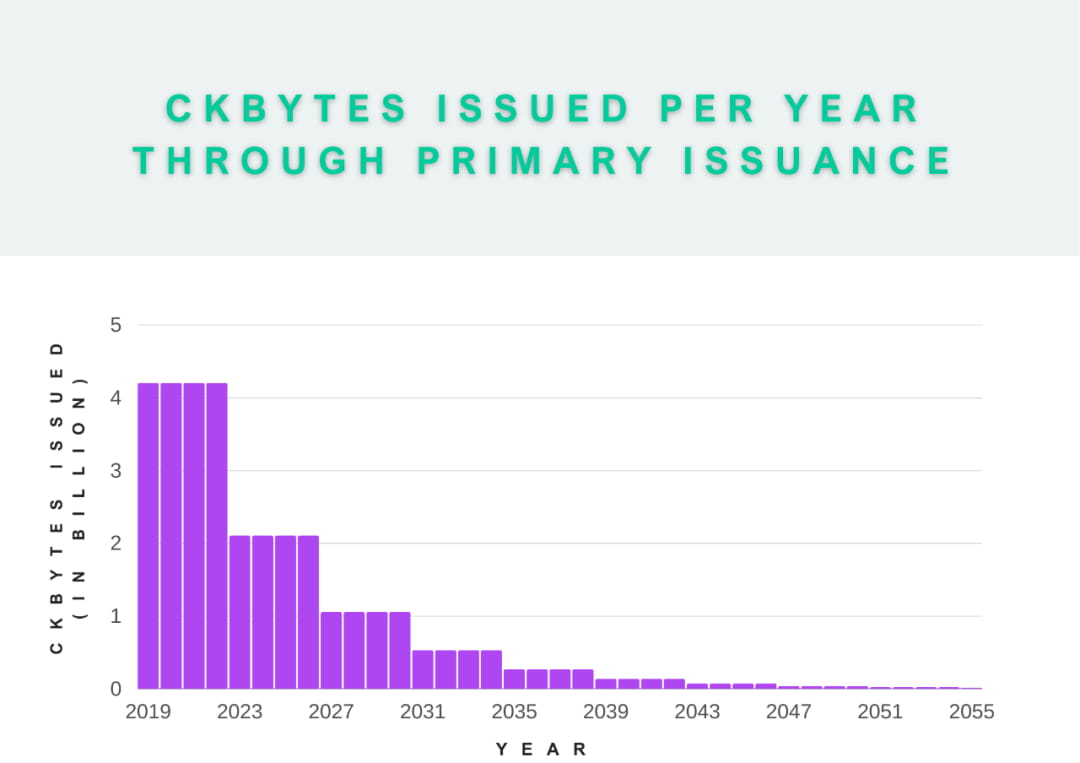

The total amount of primary issuance is fixed at 33.6 billion CKB. Similar to Bitcoin, the block reward of primary issuance is halved approximately every 4 years until all 33.6 billion CKB are mined. The first halving event of CKB is expected to come in mid-November 2023. Therefore, there is a maximum limit for primary issuance, just like Bitcoin.

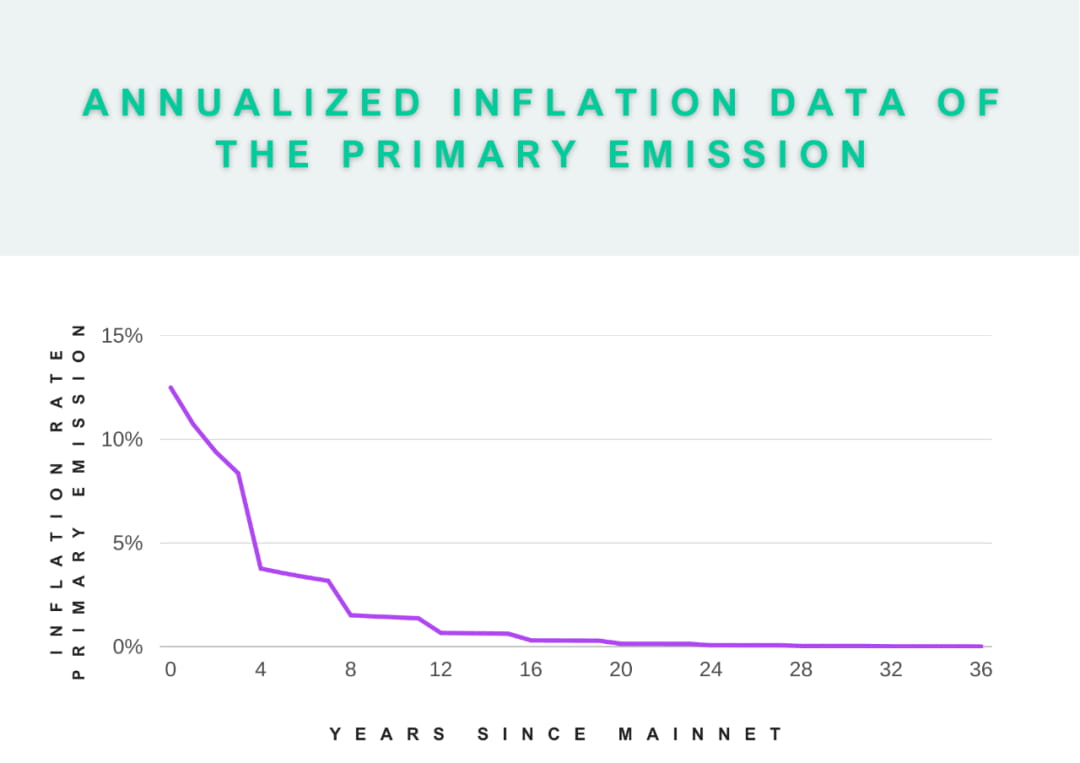

For example, in the first four years after the launch of the Nervos mainnet, the amount of CKB generated through primary issuance each year was 4.2 billion. After the first halving event in November 2023, the amount of CKB issued through primary issuance will drop to 2.1 billion CKB per year until the next halving. As shown in the figure below, the amount of CKB issued through primary issuance will be reduced by half each time the halving occurs, so the inflow rate of new CKB will also drop by 50%.

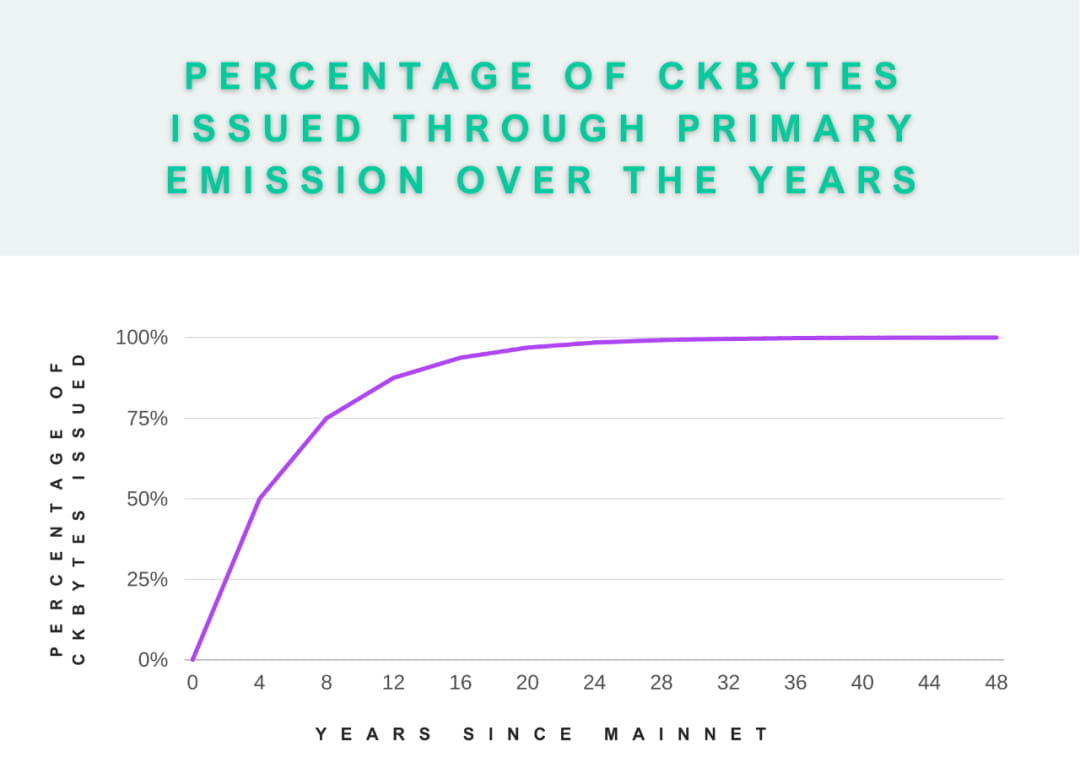

Therefore, in the first four years after the launch of the Nervos mainnet, the primary issuance generated a total of 16.8 billion CKB, accounting for 50% of the total primary issuance of 33.6 billion. In the second four years, the primary issuance will generate 8.4 billion CKB, that is, the total CKB generated through primary issuance in the first eight years will account for 75% of the total primary issuance. By 2031, the 12th year after the mainnet launch, the total CKB generated through primary issuance will reach 29.4 billion, accounting for 87.5% of the total primary issuance.

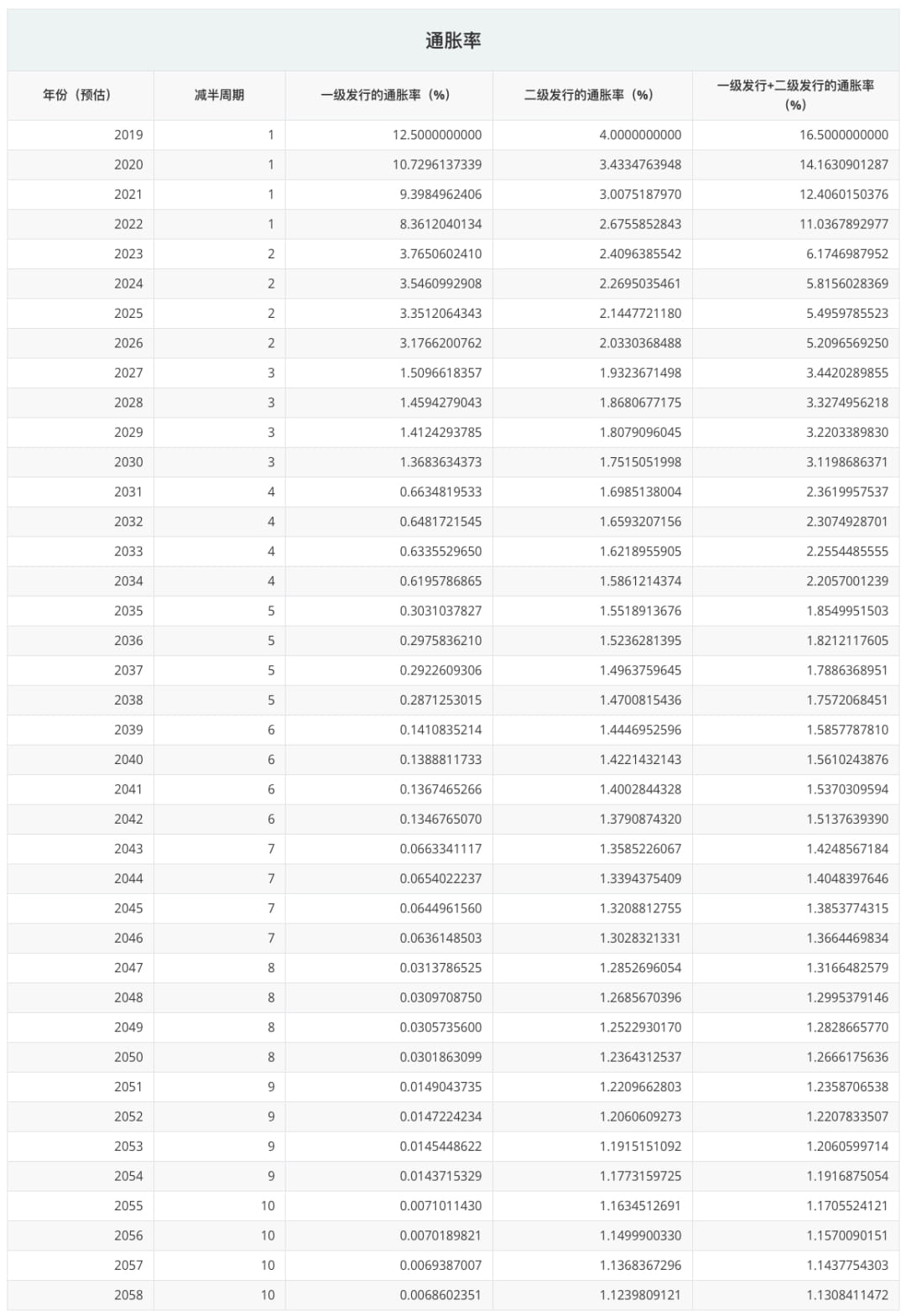

By now, you may have noticed that the first few years after the Nervos mainnet launch saw the largest issuance, and that issuance dropped significantly after each halving event. This is also evident from the inflation rate: in the first year after the mainnet launch, the inflation rate for primary issuance was 12.5%, four years later, after the first halving in 2023, the inflation rate will drop to 3.765%, and after the fourth halving in 2031, the inflation rate will drop to 0.663%. Since the total primary issuance is fixed at 33.6 billion CKB, the inflation rate brought by primary issuance will also drop to zero when all CKB issued in primary issuance are mined.

In the table below, we can see the changes in primary issuance after each halving.

[1] Note: The Nervos CKB mainnet was launched on November 15, 2019 (UTC). Therefore, each year in the table should be understood as from November to November of the following year.

[2] Note: This refers to the number of halving events that will occur.

All tokens issued at the first level are distributed to miners as rewards to incentivize them to maintain network security, and can therefore only be obtained through mining.

Secondary issuance

In addition to the primary issuance (basic issuance), there is also a secondary issuance, with a fixed issuance of 1.344 billion CKB per year. Therefore, the secondary issuance is different from the primary issuance, and there is no hard cap, that is, there is no maximum limit.

From the above figure we can see that after the second halving, the amount of CKB issued in the secondary issuance in each block will exceed the amount of CKB issued in the primary issuance, so from the perspective of mining rewards, the secondary issuance will become more and more important. When the primary issuance is exhausted, only the rewards for the secondary issuance will remain.

Secondary issuance can be seen as a way to collect state rent, that is, to tax network participants who occupy on-chain state through inflation. This ensures that miners' income is predictable and based on the demand for value storage rather than the demand for transactions. This is critical to the network security model that prioritizes value storage in Layer 1 blockchains (such as Nervos CKB) while moving most transactions to Layer 2.

But if you don't occupy on-chain state, but hold CKB like a long-term holder, do you also have to pay this tax? Is it fair? If you do, it's really unfair. Therefore, Nervos designed a special smart contract called Nervos DAO, which allows you to hedge the inflation caused by secondary issuance. CKB holders can deposit their tokens into Nervos DAO to get a part of the secondary issuance, which just offsets the inflationary effect of secondary issuance. Therefore, for long-term holders, as long as they lock their tokens in Nervos DAO, the inflationary effect of secondary issuance is only superficial. As the impact of secondary issuance decreases, these users actually have tokens with a maximum limit like Bitcoin.

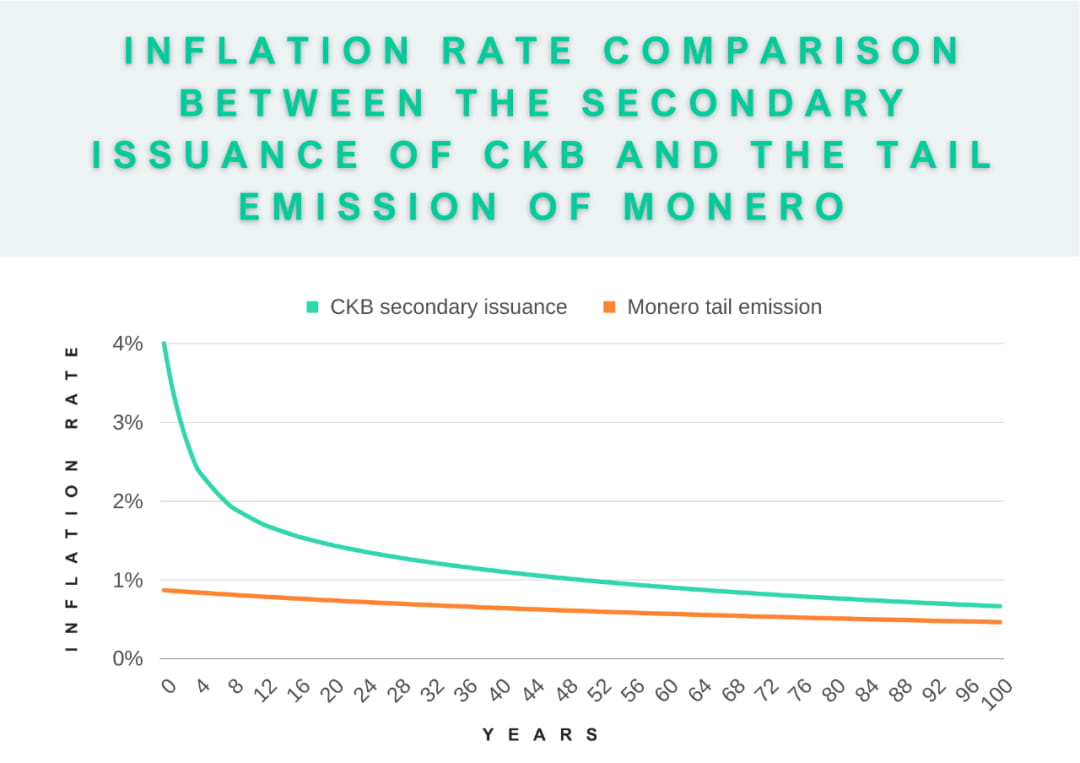

A simple way to understand secondary issuance is to think of it as long-tail issuance. For example, Monero's long-tail issuance scheme prevents miners from relying entirely on transaction fees, so they are guaranteed a certain amount of income regardless of how the fee market and transaction volume change. In this way, the block reward will never be zero, which incentivizes them to continue to mine honestly, thereby ensuring the security of the network for a long time.

Note: Monero’s long-tail issuance scheme was implemented on its mainnet in late May 2022, while CKB’s secondary issuance has been implemented since the launch of the Nervos mainnet in November 2019.

The above figure clearly shows how the inflation rate caused by Nervos secondary issuance and Monero's long-tail issuance plan gradually decreases and approaches zero. The essential difference between the two is that Monero's long-tail issuance plan affects all participants in the Monero network, while Nervos' secondary issuance only affects those participants who have not deposited CKB into Nervos DAO. Therefore, it is only a targeted inflation and will not affect all Nervos participants.

In fact, if we look at the nominal compensation rate that Nervos DAO depositors receive, we can see that it decreases over time. This is because as a depositor in the Nervos DAO, you always get a fixed share of the new supply, but the inflation rate of the new supply itself is constantly decreasing. This causes the compensation rate (APC) to actually decrease over time, which also means that the total supply of CKB is growing more and more slowly, and both the inflation rate and the Nervos DAO compensation rate will gradually approach zero.

If we compare the inflation rates of primary and secondary issuance over the years, we can find that depositors in Nervos DAO are only affected by the inflation rate of primary issuance, just like Bitcoin has a hard cap. CKBs that are not in Nervos DAO, whether they are on-chain or in circulation, will be diluted by secondary issuance.

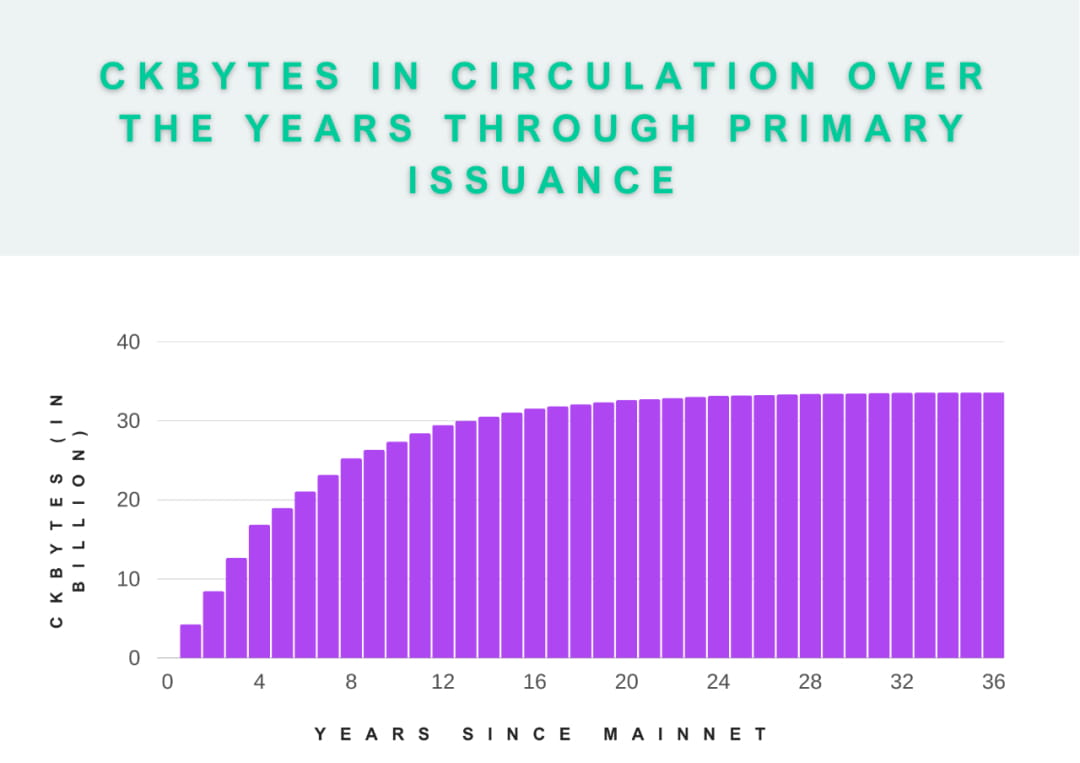

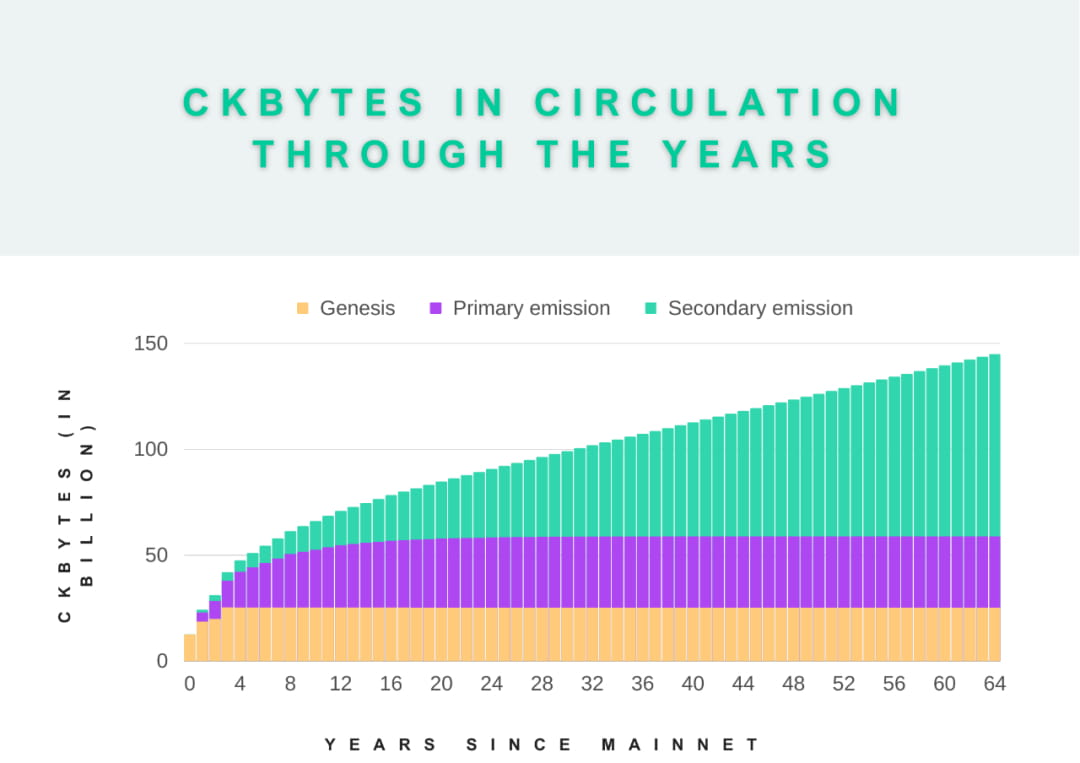

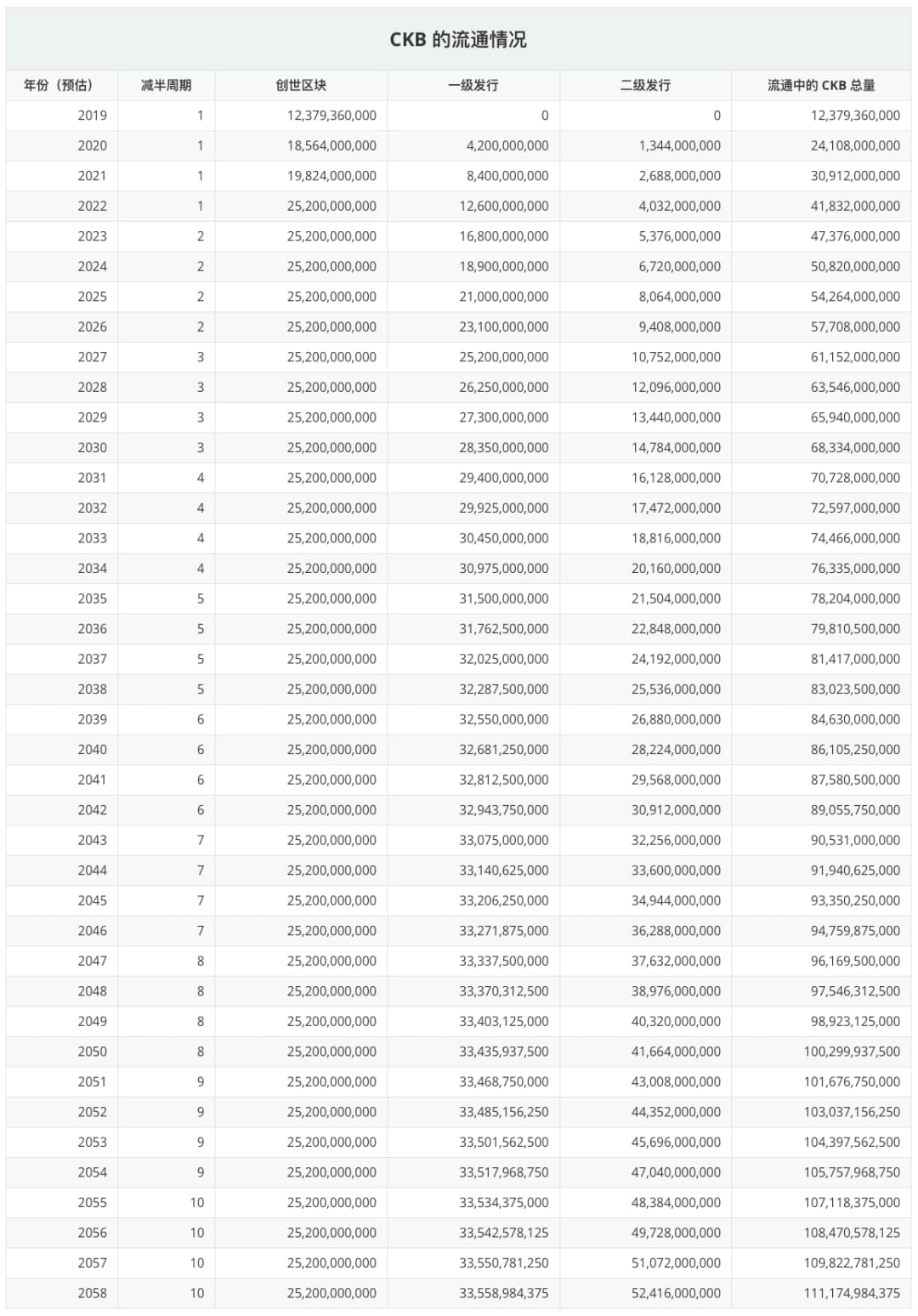

In the image below you can see the amount of CKB in circulation over the years.

Note: Both the chart above and the table below take into account the genesis block’s 25.2 billion CKB and the unlock date. The secondary issuance of 134.4 million CKB per year is also taken into account, without taking into account the CKB that has been destroyed and belongs to the treasury. If you want to know how much CKB from the secondary issuance has been destroyed so far, you can check it here:

https://explorer.nervos.org/nervosdao

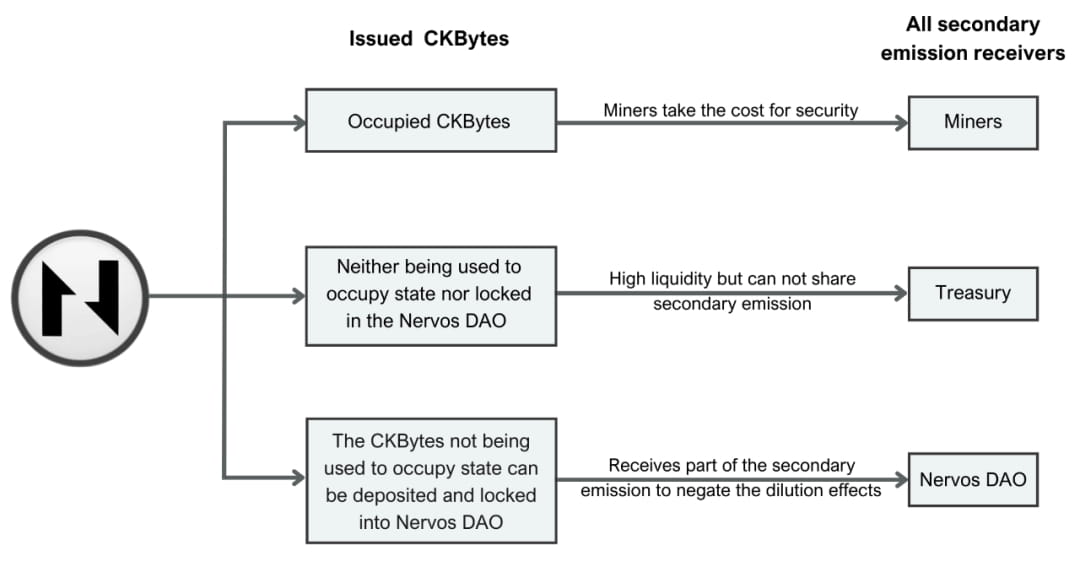

Token Allocation for Secondary Offering

Secondary issued CKB will be distributed to miners, Nervos DAO depositors, and the treasury in proportion to how much CKB occupies the on-chain state, how much CKB is locked in the Nervos DAO, and how much CKB is in circulation.

Let’s look at an example to better understand it. Assuming that 50% of the existing CKB occupies the on-chain state, 35% is locked in Nervos DAO, and the remaining 15% is in circulation (they do not occupy the on-chain state or are stored in Nervos DAO), the secondary issuance of CKB will be distributed like this:

50% of secondary issuance is used for miner rewards

35% of the secondary issuance is given to Nervos DAO depositors, who share these rewards according to the proportion of deposited tokens, thereby eliminating the dilution of long-term holders caused by the secondary issuance.

The remaining 15% of secondary issuance goes to the treasury, and its use is determined by the community through the governance mechanism. As long as the treasury is not activated through a hard fork, these CKB will be destroyed.

Summarize

Although slightly more complex, the issuance mechanism of Nervos CKB is very similar to that of Bitcoin and reinforces its value proposition of a stable and predictable issuance model. The biggest difference between the two models is that CKB introduces a long-tail issuance scheme, namely secondary issuance, to ensure the security of the network in the long run, rather than relying on transaction fees to incentivize miners. This secondary issuance will not affect all participants in the network, because Nervos DAO depositors can turn their CKB into a hard-capped token like Bitcoin to avoid the inflationary impact of secondary issuance.

Related Links

Crypto-Economics of the Nervos Common Knowledge Base:https://github.com/nervosnetwork/rfcs/blob/master/rfcs/0015-ckb-cryptoeconomics/0015-ckb-cryptoeconomics.md

Understanding the economic model of Nervos CKB:https://medium.com/@Chema_es/understanding-the-economic-model-of-nervos-ckb-408e2b74478b

The CKByte Issuance Model of Nervos:https://talk.nervos.org/t/the-ckbyte-issuance-model-of-nervos/5321

A detailed description of Nervos (CKB) supply and issuance:https://medium.com/@m.quinn/a-detailed-description-of-nervos-ckb-supply-and-issuance-1d55c4b101f9

Nervos CKByte Distribution, and Why We Are Burning 25% in the Genesis Block:https://medium.com/nervosnetwork/nervos-ckbyte-distribution-and-why-we-are-burning-25-in-the-genesis-block-9a7ddf7f6779

Bitcoin, Ethereum, Nervos: Inflationary or Deflationary:https://www.cryptowendyo.com/bitcoin-ethereum-nervos-inflationary-deflationary/

CKB Supply calculation:https://docs.google.com/spreadsheets/d/1G8eofv1qqs96aEUqEk9vZ8qxeUqSn31KCNoQlwLMyJA/edit#gid=1511634195