Author: Clara Medalie Translated by: Cointime.com 237

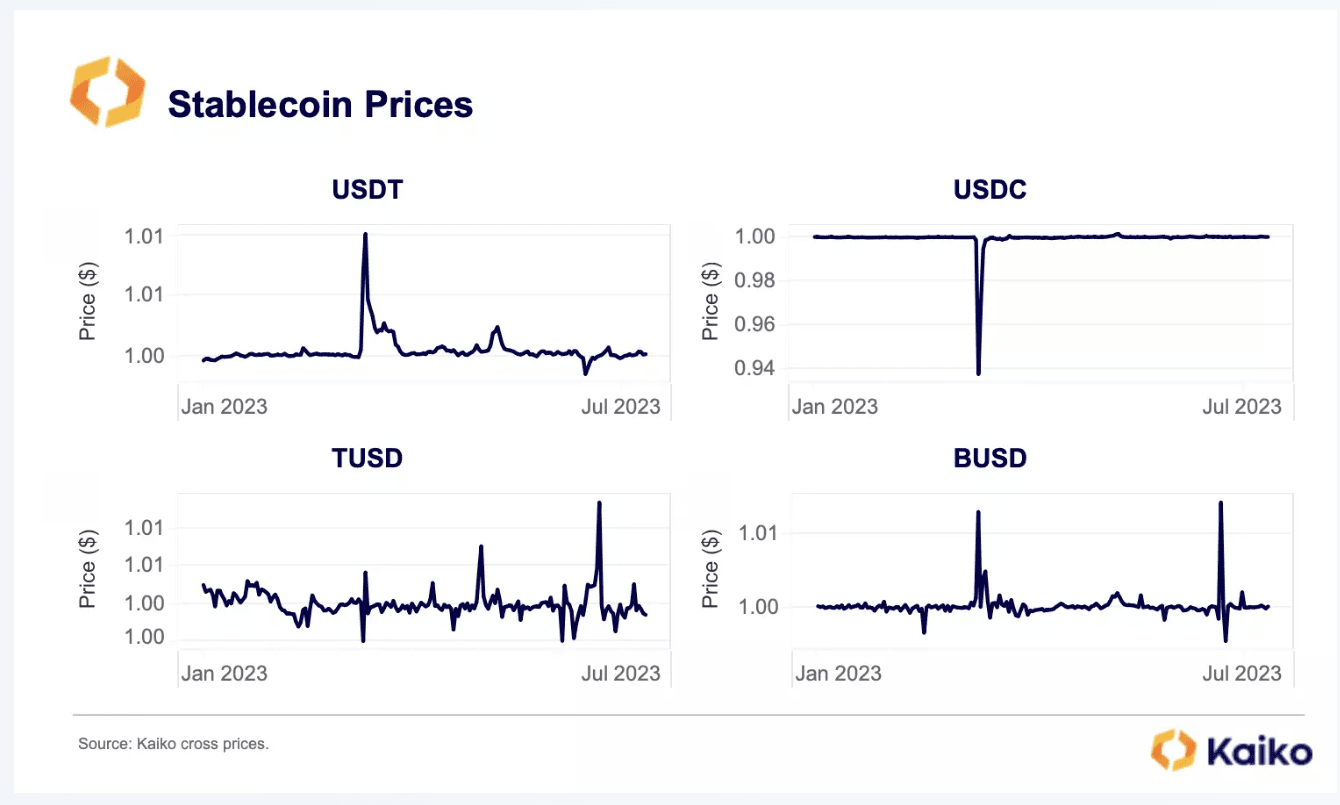

Stablecoins are systemically important in the cryptocurrency market, so even the tiniest decoupling could trigger massive market contagion. It is therefore worrying that stablecoins have been particularly volatile since the beginning of 2023: TUSD fluctuated when Prime Trust shut down, USDT decoupled due to mysterious selling pressure, BUSD has become increasingly unstable since Paxos stopped issuing it, and USDC collapsed during the banking crisis in March.

While the reasons for volatility vary for each stablecoin, this volatility highlights a larger problem: the crypto market’s high reliance on centralized stablecoins that often lack reserve transparency. While upcoming regulatory measures in Europe have put pressure on stablecoins to improve governance, there is still a long way to go. Today’s deep dive will explore the current state of stablecoin market structure to gain a deeper understanding of current risks.

Stablecoin Market Structure

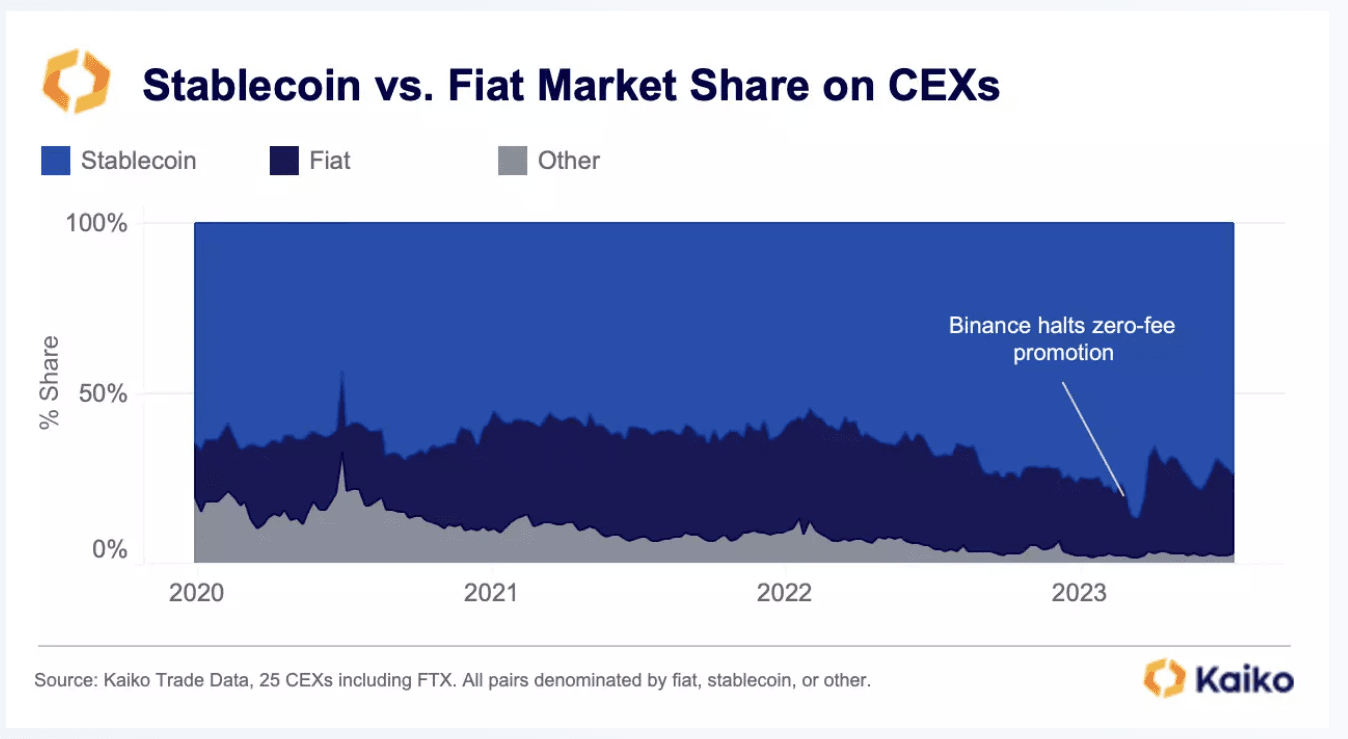

Currently, 74% of all cryptocurrency transactions on centralized exchanges use stablecoins. This share has increased by 10% since the beginning of 2020, but is far lower than the all-time high in March, when 87% of cryptocurrency transactions involved stablecoins. The rapid growth of stablecoin market share is almost entirely due to Binance's zero-fee trading promotion.

After Binance stopped the project, we observed an almost instantaneous drop in the stablecoin market share. Overall, the data shows that fiat currencies play a relatively small role in the global cryptocurrency market, accounting for only 23% of the market share.

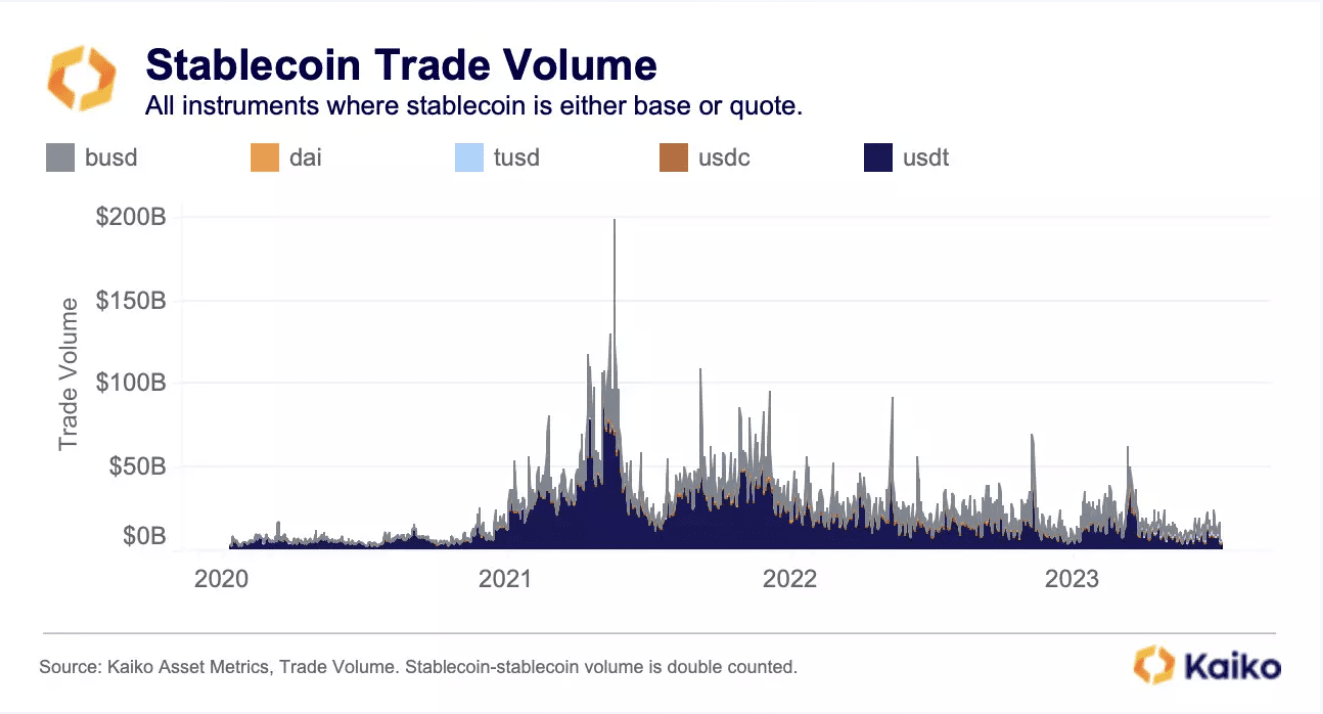

To get an idea of the actual size of these markets, let’s look at the trading volumes of the top five stablecoins (Tether, USDC, Binance USD, TrueUSD, and DAI) on centralized and decentralized exchanges.

Since the start of the second quarter, about $10-15 billion has been traded daily across these five stablecoins. While this is a far cry from the all-time highs reached during the 2021 bull run, it is still considerable trading volume.

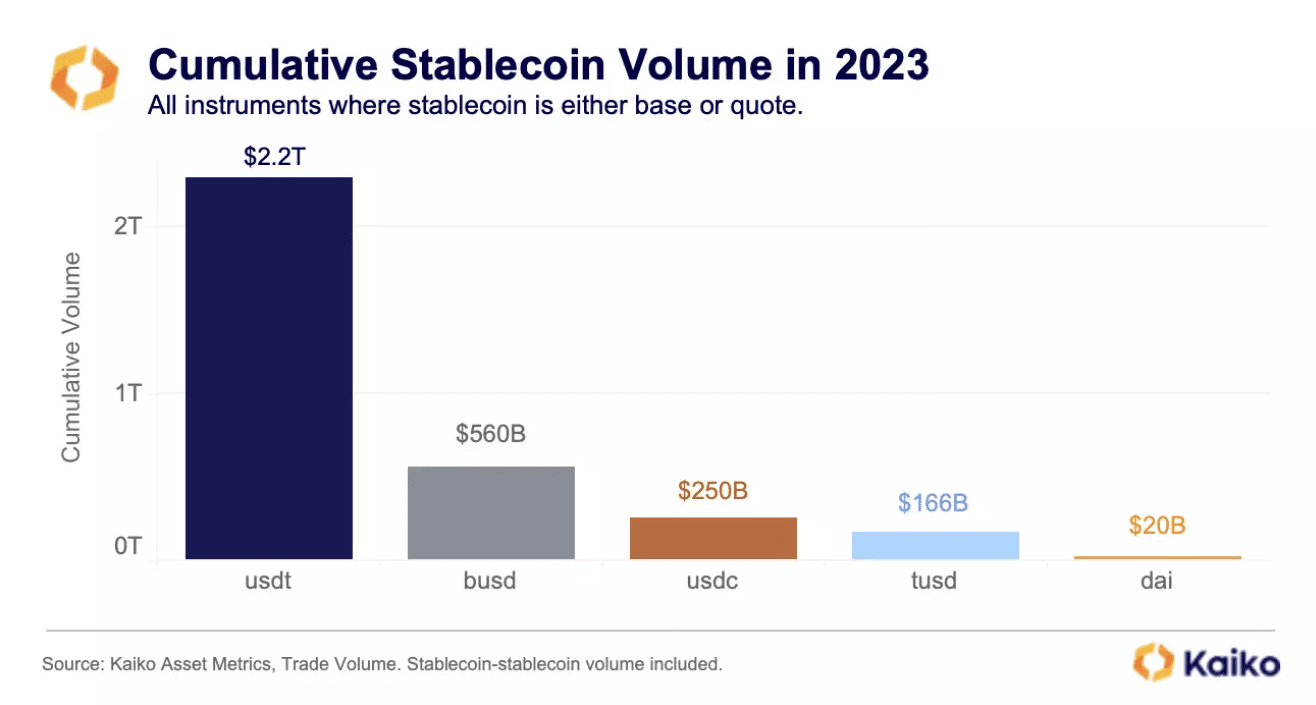

From another perspective, the cumulative trading volume of stablecoins in 2023 exceeded US$3 trillion, with Tether dominating.

Today, Tether holds a staggering 70% market share on centralized exchanges. Binance’s BUSD almost became a top competitor, but its issuer Paxos was forced to stop issuing it earlier this year. BUSD’s market share is now slowly declining, from a high of 30% to just 6% today before it officially ends in 2024.

The biggest surprise this year may be the rapid rise of TUSD, which has soared from less than 1% to 19% of the market in just three months. TUSD was once a little-known stablecoin with almost no trading volume before Binance selected it as the successor to BUSD and began promoting the zero-fee BTC-TUSD trading pair. The vast majority of TUSD's trading volume comes from this one trading pair.

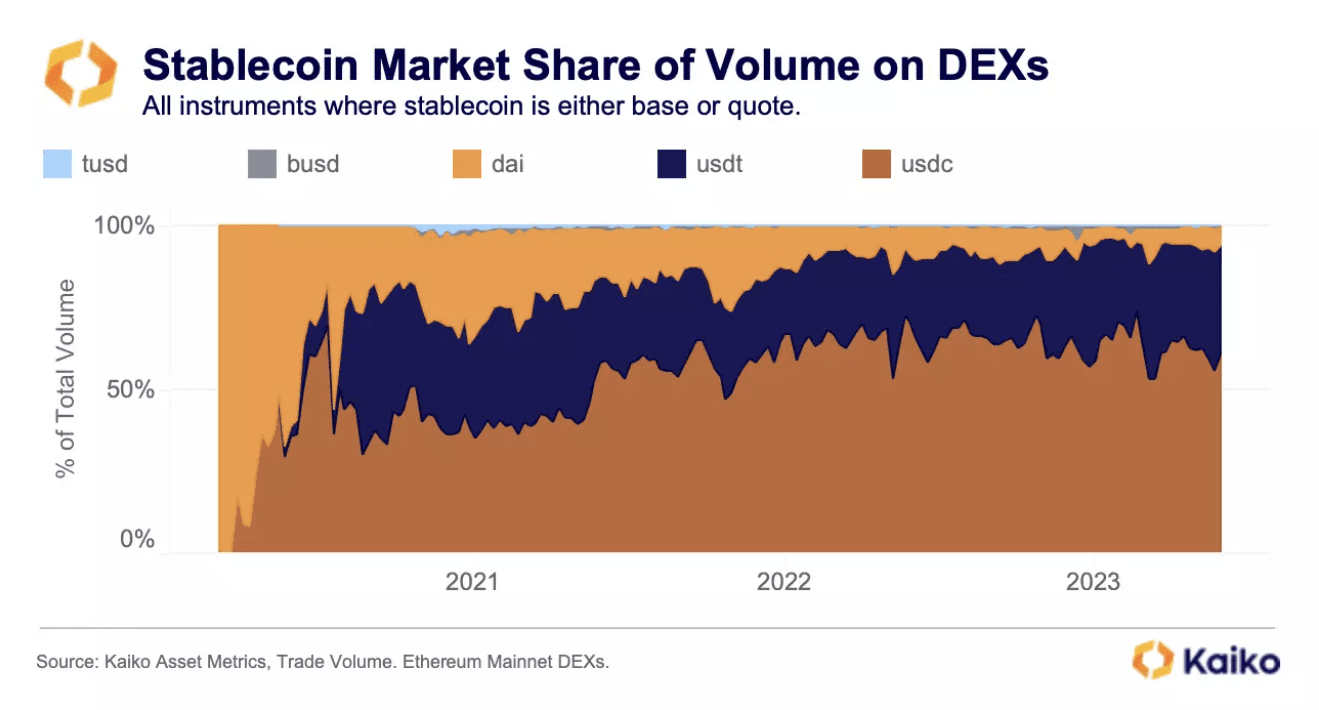

On decentralized exchanges, the distribution of market share is quite different. The most obvious trend is the rapid decline of DAI, the only top decentralized stablecoin. In the past, DAI accounted for the majority of DeFi activity, but its dominance was quickly replaced by USDC and USDT.

One explanation for this shift involves the relative capital efficiency of each stablecoin: DAI requires excess collateral to mint $1 worth of DAI, while USDC and USDT do not, allowing these centralized stablecoins to quickly attract more users and capital. Today, USDC has a systemic presence in DeFi protocols, especially in lending protocols, where it accounts for a high percentage of total collateral.

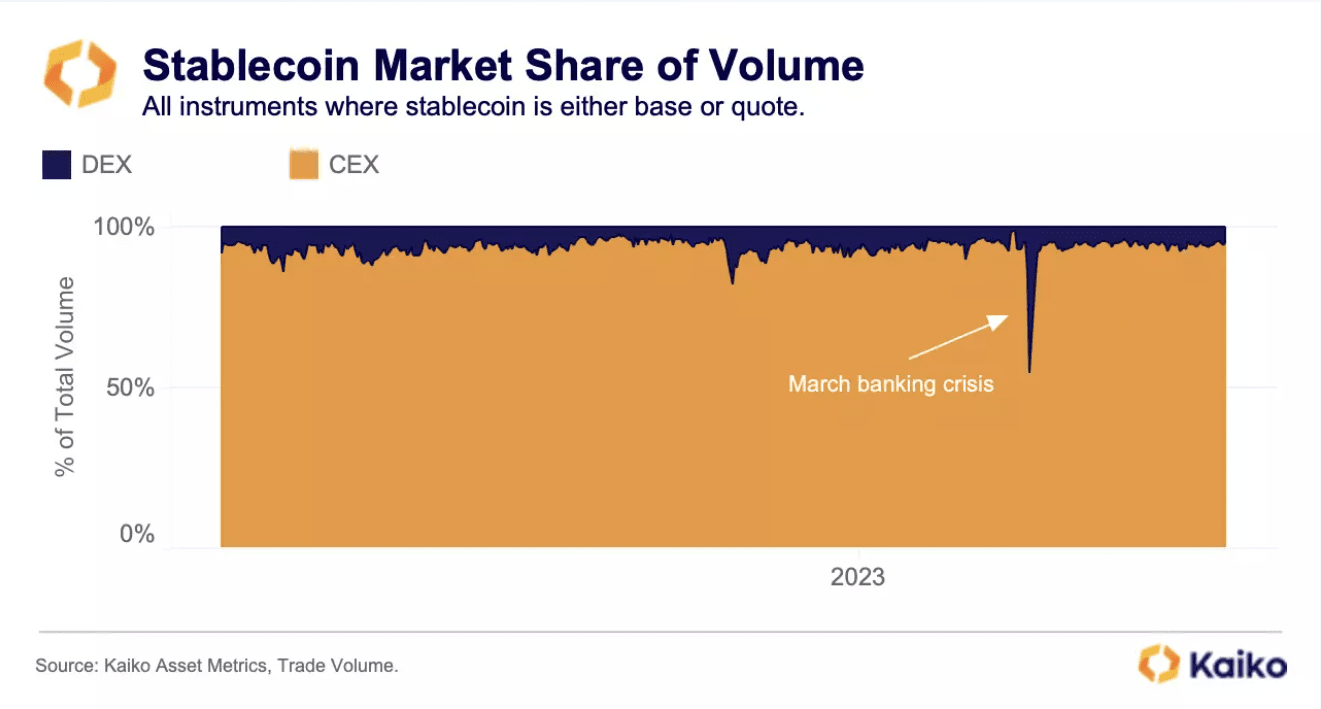

Overall, the vast majority of stablecoin trading today occurs on centralized exchanges. Only 5% of stablecoin trading is executed on decentralized exchanges, although there was a temporary spike to 45% during the banking crisis in March. [Kaiko’s DEX data includes the most liquid protocols on the Ethereum mainnet, which currently have the majority of trading volume on cross-chain].

The CEX to DEX volume ratio shows that stablecoins are nowadays mainly traded on centralized exchanges.

in conclusion

The trading volume ratio of centralized exchanges (CEX) to decentralized exchanges (DEX) shows that stablecoins are now mainly traded on centralized exchanges.

Based on this information, we can draw the following conclusions about the current state of the stablecoin market structure:

1. The vast majority of cryptocurrency activities involve centralized stablecoins, not fiat currencies.

2. Tether accounts for the majority of these transactions, although TUSD is rapidly increasing its market share.

3. The main use of stablecoins is to be traded on centralized exchanges.

This week, the European Banking Authority told stablecoin issuers that they must take immediate steps to comply with the upcoming MiCA regulation, which puts some stablecoins in a precarious position given the general lack of transparency and governance issues. While Circle has made significant efforts to improve USDC’s transparency (and even Tether has made some efforts in the past year), the relatively unknown TUSD currently provides the least information about its reserves or corporate structure, and therefore poses the greatest risk.

While TUSD is not yet a systemically important stablecoin, Binance is a highly influential exchange, so any activity on it should be scrutinized. However, transparency has historically never seemed to be a major concern for stablecoin users, and unless a direct ban is implemented or regulators coordinate legislation across major regions, we may continue to see similar market structures.