Ethereum’s Gas spot market is also likely to benefit from the derivatives market.

Original title: Opportunities and Considerations of Ethereum’s Blockspace Future

Written by: Drew Van der Werff, Alex Matthews

Compiled by: Lynn, MarsBit

✍🏼 Produced by Drew Van der Werff and Alex Matthews of BH Digital in partnership with Frontier.

Too long to read

History shows that derivatives can strengthen spot markets, providing stakeholders along the supply chain with more tools to manage their businesses. Similarly, Ethereum’s gas spot market has the potential to benefit from a derivatives market.

As Ethereum gas derivatives grow, there is an opportunity to implement a comprehensive set of products for a better user and developer experience (i.e., they can rely on paying a fixed gas price), as well as greater efficiency in price discovery around Ethereum blockspace. Additionally, in most markets, the volume of derivatives significantly outnumbers spot, providing significant opportunities in a large design space.

Regulatory/legal, market, and protocol specific factors need to be considered when designing these products. In addition, the sophistication of market stakeholders must increase to support active trading in these products.

It’s hard to know when this market will develop, but there is some tailwind around the consolidation of gas buyers (i.e. due to developments in L2s/account abstraction), the increase in products available for hedging (i.e. staking products), and increased complexity across stakeholders in the trading supply chain (i.e. through infrastructure improvements)

Throughout history, there have been examples of increased volatility in commodity markets due to exogenous events. While factors outside of the market have helped reduce these risks for those producing and consuming commodities (i.e. globalization leading to more efficient shipping/transportation and networks), derivatives act as a broader price discovery tool. Additionally, derivatives can be used to better manage businesses that rely on commodities. Similar opportunities exist around Ethereum blockspace. With the development of blockspace derivatives, stakeholders can provide a better user experience, have more tools to manage their businesses, and improve the efficiency of price discovery in blockspace. Below we outline the current state of Ethereum blockspace, historical analogies with traditional markets, and attempt to build on the research of others to present key considerations for developing a blockspace derivatives market.

Introduction to Ethereum's Blockspace

Ethereum's business model revolves around selling block space. Block space is utilized by a variety of participants to interact with smart contracts, power applications, support additional infrastructure layers, or settle transactions directly. However, like most resources, the supply is limited. In order to determine who or what consumes this supply, gas is created. Gas is used by stakeholders to specify how much they are willing to pay for their transaction to be included.

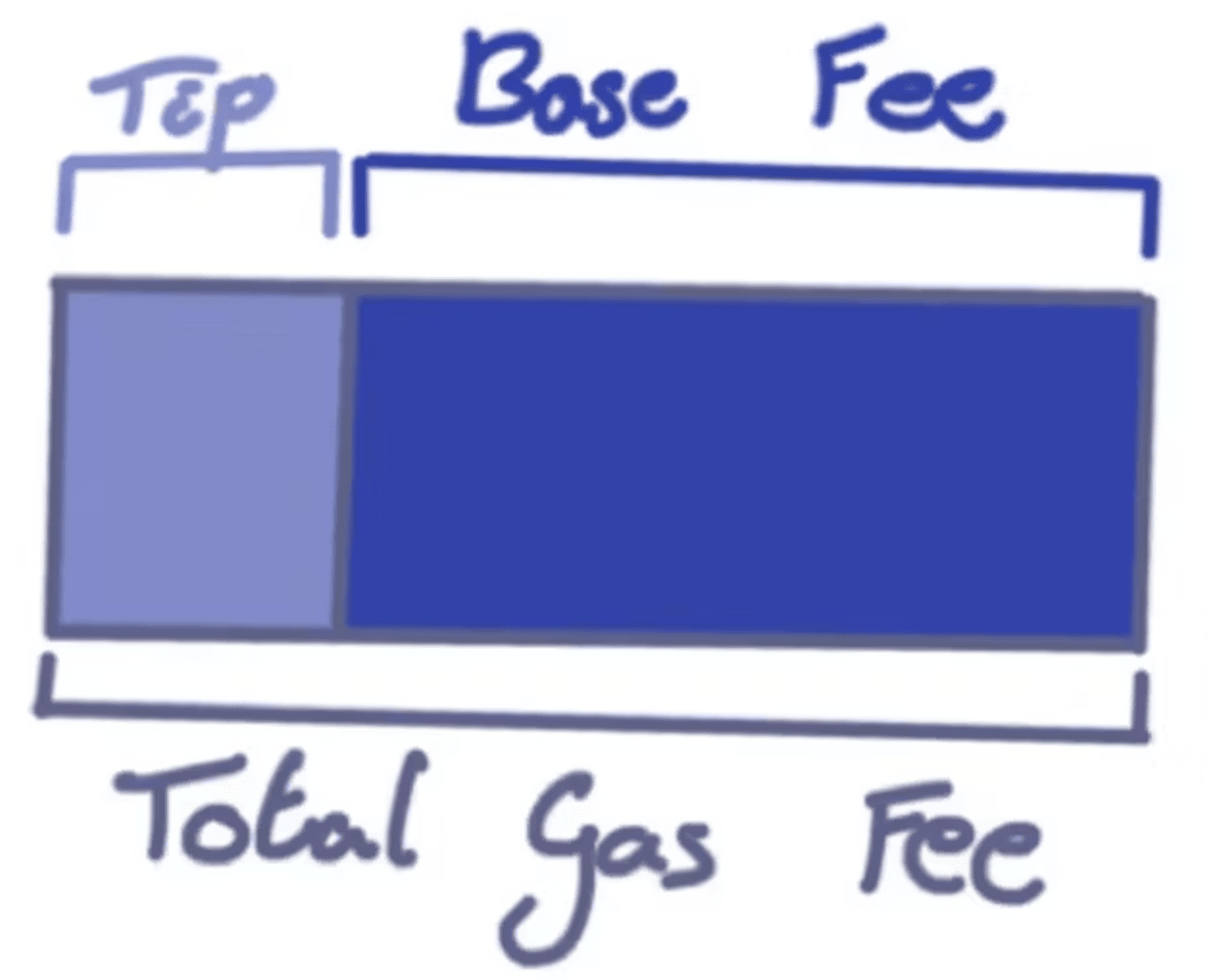

Ethereum's gas and its usage has evolved, with the most recent key change occurring in August 2021. With the London hard fork and the implementation of EIP-1559, Ethereum transitioned its fee market to consist of a base fee (which is burned) and a tip to validators. Following this change, the market now has a protocol reference rate that is driven by the base fee and ensures that for physical delivery, there is a minimum cost associated with transactions included in a block.

In September 2022, the merger happened! While subtle, this also changes some dynamics relevant to any potential derivatives markets. After the merger, the validator responsible for proposing a new block that is finalized will be known after two epochs, giving the market 12 minutes to know who will stack the next block (which may have interesting implications for potential physical delivery markets).

Finally, in the near future, the community may launch a new fee market related to data storage, referred to as EIP-4844. This market will be Ethereum’s first multi-dimensional fee market, separating data storage and execution. More on the implications of this, as well as other roadmap items, are discussed below.

What can we learn from other commodity markets

To begin to understand the potential design and market structure of blockchain derivatives markets and their potential impact on spot markets[1], we surveyed traditional markets and looked at various attributes. Below are a few key characteristics of the markets we identified as the most comparable.

Non-tradable underlying indices: In its current form, Ethereum gas is not directly tradable; we seek markets based on non-tradable underlying indices.

Cash vs. Spot: Given the dynamics between block space actually delivered and cash exchanged at expiration, we look for derivatives markets that are cash-settled, but spot markets are physically settled.

Stakeholders: A lot of activity and speculation needs to be driven by actual use of the commodity/goods.

Market Microstructure: Which block a trade is placed on can have a significant impact/dramatically change how much a buyer is willing to pay. Because of this, we look for markets that have similar microstructure dynamics driven by quality/geography/other metrics.

Based on these factors, we find that the most relevant markets are oil and VIX. We discuss this in more detail below, but it is important to note that these two markets are heavily used by various stakeholders to achieve a range of goals (i.e. better manage their business, hedge, take a view, etc.).

oil

Until the 1980s, the oil market was largely dominated by a select group of market participants, namely parties with large oil exports. By the late 1980s, a healthy spot market had developed, slowly replacing fixed-term, fixed-price contracts. However, even with this development, there was still a problem - this market required physical delivery. Given the complexity of delivering oil, these markets continued to be dominated by a small number of players with long-term partnerships, rather than opening up to a wider range of players.

As these markets continue to mature, benchmarks such as the US WTI are developed to track the sum of spot prices in certain regions. This allows the market and other stakeholders to support and exchange oil in a standardized way (that is, you do not need to understand the nuances of a region or market to trade oil). Through this development, not only are more participants able to express their views on prices, increasing the liquidity depth of the market, but derivatives can now be developed on this index (products based on the index are mainly cash settled). The result of this is that more stakeholders are able to contribute to price discovery, which can be said to increase efficiency and provide producers and consumers with more powerful tools to manage their businesses. Currently, WTI and Brent futures contracts on the ICE and NYMEX exchanges can reach billions of barrels/day, while global oil demand is around 100 million barrels/day; futures trading volume exceeds daily oil consumption by more than 25 times.

Volatility Index /VIX

Volatility Index /VIX

The VIX market originated from financial economics research in the late 80s and early 90s, which proposed a set of volatility indices that can be used as underlying assets for futures and options trading. Volatility indices play a similar role to market indices, that is, traders can speculate on a group of aggregated stocks, or in the case of VIX, the underlying volatility in the broader market. This allows participants to both speculate on future market uncertainty and hedge against the situation where volatility will rise when the market falls but investors' stock portfolios will be affected. However, unlike stock indices, VIX itself cannot be traded. Because of this, only cash-settled derivatives on top of VIX can be traded. Despite this, the VIX futures market has grown from an average of only about 460 contracts per day since its inception in 2004 to about 210,000 contracts in 2022. This market structure is similar to the current natural gas market. The underlying gas cannot be traded, but it is an observable and quantifiable property of the Ethereum block space market. Because of this, creating a standardized gas reference price is necessary for cash settlement of futures/options/swaps/ETPs. Fortunately, this has become easier with EIP-1559, which serves as a reliable oracle for congested blockspace.

Product Design Considerations

While we can draw historical analogies to illustrate the impact that derivatives markets may have on the robustness of Ethereum blockspace markets, Ethereum blockspace carries unique characteristics that will determine how reference benchmarks and derivatives products are designed. We believe the following should be of utmost importance to anyone working on developing markets/products. Here are some considerations around the following:

Market Structure: This section includes considerations around blockspace/gas market participants, whether price makers can hedge effectively, potential consolidation on the buy side, reference rate design, regulation, and some miscellaneous items.

Protocol/Roadmap: This section includes considerations around multi-dimensional spot gas markets, heterogeneity of the blockspace, miscellaneous, and potential future roadmap items.

Cash vs. Physical Settlement: Cash vs. physical settlement is defined, and some design potentials for the physical settlement blockchain space are discussed.

market structure

Blockspace/gas market participants: In any such market, there are price takers and price makers:

It is necessary for price takers to interact with the market in order to manage risk in their business. Returning to the oil market, these are both the producers of oil and the subsequent supply chain participants involved in its refining or commercial use cases. Similarly, in the gas derivatives market, there are validators who provide blockspace, but then there are developers/users of applications that require blockspace. [4] Stakeholders may want to secure fixed revenue for blockspace in advance, while applications/wallets may want to secure predictable fixed costs for their future blockspace needs:

Short: A party promises to sell block space in the future at a currently agreed-upon price. The risk to this party is that future block space is sold too cheaply.

Long: A party commits to buy block space in the future at a currently agreed fixed price. This party faces the risk of overpaying for future block space.

Price makers are market participants who speculate and take pricing risk. In traditional markets, these roles are played by market maker arms of banks, asset managers, high frequency trading entities, etc. These participants are critical to creating more liquidity and efficient markets. In gas markets, we see this role being played by digital asset market makers, investment firms, and in the long run (just like oil producers have their own trading operations), validators themselves. However, there are not enough price makers in the market today, mainly due to the lack of a liquid spot market to hedge block space risk.

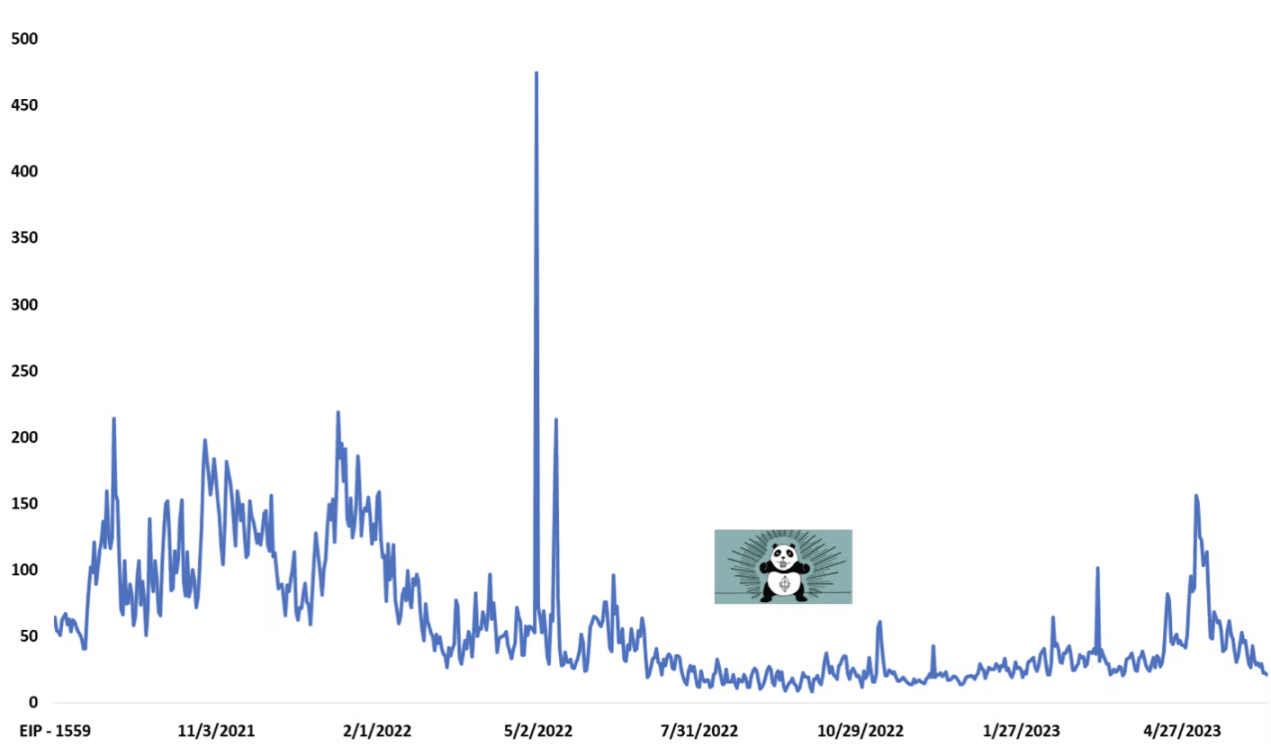

Price makers cannot hedge effectively: The auction mechanism that drives the base fee for block space can be manipulated (especially over shorter periods of time), and tips can be uncapped. As shown in the figure below, the average gas price is volatile, and the volatility is quite large if viewed by block.

Ethereum Average Gas Price (Gwei)

These factors create significant risk for price makers who expose themselves to uncapped variable blockchain costs. Some of this can be addressed through time-based indexing to smooth variable blockchain costs (reducing the impact of one-time spikes in costs on reference rates), or through the use of alternative investment products with caps on losses/gains. However, these approaches come with trade-offs as they may not meet the needs of the sell/buy side and often weaken the hedging effect of derivatives on long/short positions. Given this, we expect validators, block builders, and searchers to play a role in initially seeding the short side of the market as they have natural supply or access to physical blockspace, existing capabilities around optimizing and using blockspace supply, and experience around managing blockspace risk.

Consolidation of Buyers: As L2 evolves and the majority of users likely access blockspace via rollups/non-L1, we expect buyers of L1 blockspace to consolidate via L2 operators/people who complete L2 transactions on L1. Outside of L2, we expect buyers of blockspace to consolidate further, moving toward infrastructure and roles that abstract users from purchasing blockspace, such as block builders/AA/MPC+ middleware. Designing products for these stakeholders rather than individual consumers with widely varying goals and needs should help narrow product designs.

Reference Rate Design: If a product is cash-settled, a reference rate is a key design feature for the market to thrive. This aspect of the design is a balance of long/short needs and considerations for the protocol’s underlying gas auction mechanism. Any future team builds will need to optimize this reference rate. Even just deciding if the reference rate will be built on the base fee and tip will have tradeoffs and impact the time period used/various other factors.

Regulation: Financial products, such as derivatives (i.e., swaps, options, and futures), are generally highly regulated. For example, in the United States, the Commodity Futures Trading Commission is the primary regulator responsible for overseeing most commodity-based derivatives that are offered, acquired, or sold by "U.S. persons." If a team goes this route, they may be required to (i) comply with certain CFTC rules and (ii) register with the CFTC. In addition, if the product is offered outside of the United States, there may be additional regulatory regimes that need to be complied with. Finally, the global regulatory environment for digital asset derivatives is highly uncertain, and in many jurisdictions, there is a lack of clear frameworks and guidance surrounding the legal treatment, regulation, and classification of digital assets and market participants. Therefore, teams involved in building products - such as Ethereum blockchain derivatives - should seek appropriate legal advice before offering any such products, whether in the United States or elsewhere.

Miscellaneous: There are also some practical items that need to be optimized, including how these products are settled (i.e. daily/monthly), how collateral is managed, the mark-to-market of derivatives used for settlement and collateral management, and the types of hedging (i.e. insurance-like products) that each side of the transaction takes.

Protocol / Roadmap

Multi-dimensional spot gas market: For the first time in Ethereum history, as part of EIP-4844, there will be a multi-dimensional fee market that creates two prices for Ethereum blockspace - one for data and one for execution. These two spot markets will use separate but similar pricing/auction mechanisms. However, given the different consumers and use cases for data blockspace vs. execution blockspace, there will likely be pricing differences between the two markets. Because of this, anyone designing blockspace derivatives may need to take this into account, and depending on how the spot market develops after EIP-4844, there may be interesting hedging/trading opportunities across these two markets for buyers/speculators and risk managers. Additionally, although very early, researchers across the community have mentioned additional forks of the fee market that would create additional microstructure.

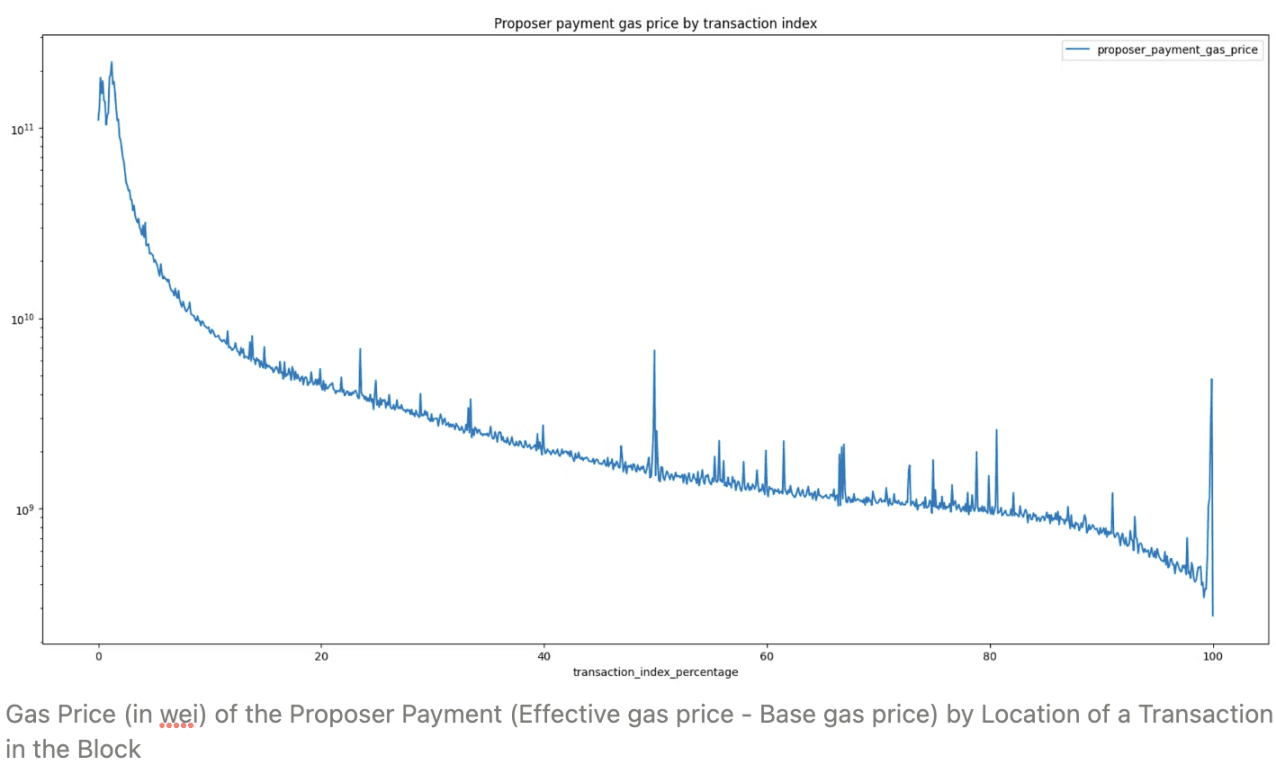

Heterogeneity of Blockspace: Not all blockspace is homogeneous. For example, there is blockcrowding, which consists of blockspace where users simply pay a fee to be included. Then there is scramble, where users pay a fee to signal a desire to be included in a particular order in a block. Given how consumers behave in these microstructures, derivatives may need to account for these dynamics, or be designed for these specific players. While difficult to estimate, we have an understanding across quantitative and qualitative sources of where user preferences have historically been to help inform where near- and long-term opportunities may exist.

In the above chart, we can see that some users are willing to pay multiples of the price for blockspace at the top and back of the block (i.e. contention), but most users pay just to be included (i.e. congestion). A leading Ethereum Foundation researcher also recently speculated that a significant number of users prioritize congestion over contention. While there may be a near-term market related to contention based on the above and other MEV-related dynamics, we do expect that in the long term, the largest market for blockspace derivatives will be focused on congestion.

Miscellaneous: Beyond this, there are a number of considerations that could impact the derivatives market. These include forks and probabilistic finality, inclusion rates, and potential censorship of block builders and/or validators.

Further Developments: While it may be a few years away, there will be further dynamics that will impact the blockspace and any derivatives. Aside from EIP-4844, we believe the most relevant and important changes are MEV-Burn, any form of changes to validator caps/staking economics, single-slot finality, and ePBS.

Cash settlement and physical delivery

Gas derivatives can be settled in "cash" or through "physical delivery." See below for more details, but cash-settled products generally do not perfectly replicate the deliverable spot market because they provide synthetic exposure to the commodity, usually based on a reference rate. Because of this, the existence of a physically delivered derivatives mechanism is critical to ensuring that the broader derivatives market on the blockchain space accurately reflects the deliverable spot market conditions.

Physical Delivery: Physical delivery of Ethereum blockspace (and really any commodity market) is more complex than in cash markets. Both parties to any such derivative must physically settle the goods upon expiration of the derivative. In the case of a validator-application transaction, this would require the validator to deliver blockspace to the buyer. We discuss some potential means of physically delivering blockspace below:

Block builders offering this as a service: As written before, due to economies of scale and the technical requirements around full dank sharding, block building is likely to continue to be dominated by a small number of actors that can afford to be active in these markets. Block builders are obviously natural buyers/sellers of blockspace (they are in the business of managing/optimizing blockspace after all) and can also provide a service to applications/blockspace consumers to provide the actual delivery of blockspace.

Validator Coordination / Middleware: In addition to block builders, validators are the main stakeholders in the market for physical delivery of blockspace. This will be driven by the desire to help manage the currently volatile revenue stream of the entire validation business, and allow a new market to develop where validators can sell future blockspace for a premium. In order to achieve this, validators will need to unite and use middleware as a coordination mechanism.

Selling future blockspace in-protocol: While this would require significant changes to the protocol, there have been others considering mechanisms to sell future blockspace in-protocol, with some precedent from other networks already discussing designs, research articles by Vitalik on inclusion lists, Barnabe Monnot/Ma around initial PBS research, and Alex Stokes on soft pre-confirmations. We have also seen some teams experiment and get proof of concept working in Ethereum’s testnet using smart contracts and OTC-style transactions. Finally, other POS chains have considered integrating and embracing blockspace futures in-protocol to more efficiently allocate blockspace based on consumer demand.

Space derivatives

We recognize that there have been various attempts at hashrate derivatives around the Bitcoin network. There has been some growth in these markets, but they are still limited at this point. While these markets may be ahead of their time, there are also market structural frictions around hashrate derivatives that are not present in the potential Ethereum blockspace market — most importantly there is a wider range of natural market participants, increasing the likelihood of growth in a liquid two-sided market. That said, we also acknowledge that it is still early days. After all, futures volumes in the more mature ETH market still pale in comparison to derivatives volumes in traditional commodity markets. Furthermore, for this market to thrive, actors such as block builders, validators, and applications will need to become more sophisticated, with competition on these fronts becoming so intense that teams can either leverage these products to gain a competitive advantage over one another, or can offer a unique product that relies heavily on managing future blockspace. Even given the timing, we believe blockspace futures can have a unique impact on Ethereum, helping stakeholders better manage frictions around gas and hardened blockspace. We hope this post inspires a wave of discussion, developer tinkering, some hackathon projects (!), and innovation over the next decade.

🙏🏼 Thanks to Ankit Chiplunkar, Julian Ma, and Tomasz K. Stanczak, and others for comments, collaboration, and review.