All quoted data in this article come from the official stablecoin authorities as of 2022/05/14

Ranking of commonly used stablecoins and total market capitalization

Common stablecoins are listed below, because stablecoins are not necessarily 100% anchored in value. The ranking and market capitalization data come from coingecko. The focus of the subsequent discussion in this article is on algorithmic stablecoins.

Centralized fiat-backed stablecoin

At present, the basic logic of this type of stablecoin is that centralized institutions promise that all stablecoins will be pegged to the U.S. dollar at a ratio of 1:1 and subject to supervision. Commonly used stablecoins are usdt, usdc, and busd. Let’s talk a little bit about the situations of these three, they are slightly different.

USDT: Issued by tether, it is the largest stablecoin on the market. It has a long history and wide coverage. It supports multiple chains and is one of the few that supports the btc chain. Almost every few years there are rumors of USDT exploding, and the ratio of USDC/USDT has even reached 1.1 a few days ago. Let’s analyze based on the data whether there is a possibility of USDT exploding. The current total assets of usdt are US$76,870,542,583.18, and there are audit reports every quarter. Let’s take a look at the latest audit report.

83.74% of the collateral is cash equivalent, of which real cash and bank deposits only account for 6.36%, and the rest are mostly treasury bonds and commercial paper. There are also 6.36% in other investments, even including digital currencies. From personal analysis, the overall situation is still healthy. Although there is not much cash, it should be no problem for daily payments. The rest is a black box model of the bank. You don’t know where the money has been used, but for savers, this is not a problem. What's important is that you can prove that you have so much money. The only black swan event is a run. When there is extreme panic, a run will cause the bank to break, but the probability is very small, just like the run on the four major banks will also cause the same problem. As a practitioner, I don’t expect this phenomenon to happen. Of course, when the anchor broke on the 12th, I also entered the market to speculate in stable coins, which was also very fantasy. After all, there are not many opportunities to speculate in stablecoins.

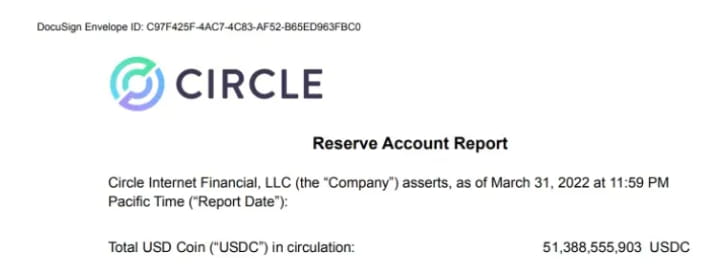

USDC: issued by circle company, is completely anchored 1:1 by cash and short-term US government debt, and is audited every month. The latest issue is the audit report in March. There are no problems and the security is excellent.

BUSD: Co-issued by Binance and Paxos and fully anchored by cash reserves. Monthly audit reports, coupled with the endorsement of the world’s largest exchange, provide excellent security. The audit report is as follows:

Summary: Currently commonly used centralized legal currency mortgage stablecoins have minimal risk, and their security is BUSD=USDC>USDT. Playing in the currency circle, you can hold coins safely without having to worry too much. If USDT explodes, it will be almost a devastating blow.

Algorithmic Stablecoin

Currently, algorithmic stablecoins are mainly divided into three types. Let’s briefly divide them into categories:

Over-collateralization: Use other currencies to over-collateralize and mint stablecoins. Contains DAI, MIM

Hybrid algorithm: Use part of other currencies as collateral, usually other stable coins, and then use part of the ecological currency to anchor. Contains Frax, USN, etc.

Algorithm anchoring: Simply rely on algorithmic mechanisms such as burning casting for anchoring. It includes UST, USDN, USDX, etc.

COME ON

The algorithmic stablecoin issued by the maker platform is supported by mortgage assets. Officially, it is called a collateralized debt warehouse CDP. Simply put, if you pledge BTC or eth, you need to mint DAI at a cost of 150% of the mortgage rate. This debt will lock the collateral assets in the CDP (that is, you will BTC and ETH are locked) until you repay DAI, and because they are all over-collateralized, it means that the value of the collateral is higher than the value of the debt. Based on the status of BTC and ETH in the currency circle, no one should be willing to directly mortgage without repaying it. At this time, the question arises. If the value of the collateral rises, everything will be easy. If the pie oversold, what will happen to DAI? In the event of emergency liquidation, Dai can redeem collateral worth exactly $1 based on the price of the oracle at the time of emergency liquidation, which is the standard liquidation mechanism.

How to anchor: When demand stimulus pushes the price of Dai above the exchange rate, CDP holders can take advantage of the opportunity to participate in maintaining exchange rate stability. This allows CDP users to issue Dai, which can be used to purchase assets with additional variable purchasing power. Conversely, when the price of Dai is below $1, CDP users can purchase Dai at a cheaper price to repay their CDP debt at a variable discount. Of course, the method of unanchoring arbitrage is the same as above.

To put it bluntly, when the price of DAI is higher than 1 US dollar, the DAI in the hands of those who participate in staking will be more valuable. For example, if they exchange it for more USDC, it will actually return to the anchor in the process of exchange. If the price of Dai drops below $1, then mortgagors can buy back DAI for less money in exchange for their collateral.

Summary: Because the collateral is hard currency and the mortgage rate is high enough, large-scale liquidation can only occur in a black swan situation when currency prices plummet. Overall, it is the most stable stablecoin with the least risk. .

ME

Most of the logic is similar to DAI, but it supports multiple chains, such as eth, bsc, avax, ftm, etc., and also supports multiple assets in multiple chains for mortgage. It is precisely because it supports more currency mortgages that logically speaking That is, liquidation is more likely to occur and more arbitrage is needed to anchor the currency price. That is, the fluctuations are greater than DAI, and defi returns are higher, so that many large defi investors are deeply involved, but overall I think it is risky. More chains and more tokens mean the need for more contracts, which means there is more room for problems. More links lead to more ways to cause trouble. We can analyze it later when we have time. .

Summary: It is also an over-collateralized stablecoin, and overall it is relatively stable. The risk lies in the fact that there are many altcoins that can be mortgaged. It has also been unanchored during its growth, but it was not serious and eventually came back. If you are a deep DeFi player, you can hold it, but it is not recommended for novice users.

FRAX

Frax is also a dual-token system, including a stablecoin Frax and a governance token FXS. Frax is the first stablecoin protocol to feature a hybrid algorithm: part of the supply is backed by collateral (USDC) and part of the supply is algorithmically backed (FXS). The Collateral to Algorithm Ratio (CR) depends on the market pricing of the frax stablecoin. Analyze what will happen if the anchor breaks. When Frax is lower than 1 US dollar, users will switch to fxs to smash the market if they want to leave. At this time, fxs will be lower, which will cause the anchor to be more serious, and it will look like it will also spiral to death. , but here comes the clever point, CR will rise at this time, selling frax can only get less fxs at this time, and the selling will be alleviated at this time. On the contrary, when Frax price premium, CR falls back, and arbitrageurs buy more Fxs at a cheaper cost to cast Frax back and forth as an anchor. At this stage, CR has been maintained above 0.8, that is, more than 80% of usdc is used as collateral. When the scope of use is not wide, the risk of being unanchored and unable to come back is small. Frax is also the main force in the defi track and will idle USDC collateral is reallocated to blue-chip DeFi protocols to obtain cash flow for FXS holders. It also works closely with Curve and CVX to derive a bunch of defi products.

Summary: Stablecoin + DEFI is the most expensive to play, suitable for defi players to use for financial management, and regular users do not need to contact it.

USDN: Stable currency issued by Waves (unanchored)

Some people may have heard of waves, commonly known as Russian Ethereum, regardless of politics ~ but it did surge during that period. Around March, it was also suspected that it was Pond's, because it was revealed that the project party borrowed money to continue minting, commonly known as spiraling. You can look into the specific reasons, and let’s analyze the logic.

In this set of logic, there are first three currencies: Waves, USDN and NSBT, which are a little complicated to understand.

Waves is similar to LUNA, a public chain currency that can be mortgaged to generate USDN. By locking waves in a smart contract, USDN of the same value can be minted. USDN is similar to UST, an algorithmic stablecoin, and the upper limit of the token is the maximum value of waves. At this time, the question arises. What is NSBT? It can be understood as a buffer for the treasury. Because the price of waves will fluctuate, the market value of waves stored in the smart contract is different from the market value of USDN. When the price of waves falls, the reserve The asset will be lower than its corresponding value in USDN. Theoretically, the anchor is unanchored. In this case, the smart contract will detect insufficient reserves, generate NSBT and make the NSBT/Waves trading pair, so that you can buy NSBT at a discount. Once waves rise, the contract will return to liquidate NSBT. , you will make a profit after returning to anchor. To put it more bluntly, buying NSBT means that it will return to the anchor, and provide financial support for the return of the anchor, and then gain profits after supporting the return of the anchor. From this point of view, this is also a project that relies on consensus to gamble on human nature. Once it is maliciously shorted or there is a problem with the consensus, As long as it starts to collapse, it won't end well. At present, USDN has shown signs of being unanchored. If it continues, it may be in the same situation as luna, and there is also a lot of room for arbitrage. It is recommended to pay attention.

Summary: Returns always coexist with risks. It is not recommended to buy USDN, but it is recommended to pay attention.

USDD: Stable currency issued by the Sunco Bo Fed

Summary: Combining a decentralized algorithmic stablecoin with a semi-centralized management method, I believe there will be no problems at this stage. After all, it only has a market value of 200 million, but I will not participate.

USN: a stable currency officially issued by near

USN is minted by depositing NEAR tokens into the reserve fund, and can always be redeemed for equivalent NEAR based on the price of NEAR/USN. Doesn’t it feel like UST, but here comes the cool operation. First The difference is that the first 1 billion USN in circulation will be backed by USDT 1:1. In addition, NEAR worth US$1 billion is pledged in USN's decentralized banking protocol, which is guaranteed even if the price of NEAR fluctuates violently. USN is overcollateralized. The second point is different from the situation of UST. USN is minted during the swap process with NEAR. The NEAR used to mint USN is then staked on the NEAR blockchain to generate staking rewards, which are distributed to USN holders. The point is that minting/burning USN does not change the supply of NEAR. In other words, the death spiral and upward spiral similar to LUNA and UST are avoided. Near in the reserve fund can be staked through voting. Distributed to USN holders via Near and Aurora (EVM) lending protocols. There are currently about 11 points, which is quite high among stablecoin financial management. In addition, the additional function is to become a native asset of near, paying for gas and storage fees on the chain. The casting method is also the arbitrage method of direct swap when the anchor breaks.

Summary: The NEAR ecology has gradually increased this year. Overall, the current volume is supported by the official treasury. There is no problem for the time being. The current stablecoin income is acceptable, but as the volume increases in the future, the risks will also increase. Big, I don’t know if the near move is considered a good move.

USDX: kava is considered stable, but the market value is too low. If someone asks, tell me a story.

Together with Luna, it belongs to the cosmos ecosystem. It can be understood as MIM on the cosmos ecology. It supports mortgage casting of usdx. The problem is that kava did not close the ibc bridge when ust plummeted. Then ust can be mortgaged and cast into usdx, so that usdx is unanchored. Now It is very difficult to re-anchor, unless the project party pays for the losses themselves or uses user consensus to actually buy it. At this stage, ust can no longer be circulated in the cosmos ecosystem, so there is no way to arbitrage.

UST: I wrote about it in the previous article. If you haven’t read it, you can read it.

Big summary:

The stabilization track is equivalent to the Federal Reserve in the currency circle. It is an area where risks and returns coexist, and it is also a very important position. Quite a few people want to compete for supremacy, and there should be many challengers in the future. Let’s see who can compete for the top spot in the end! It is not recommended for novice users to easily invest in the stable track. They must make decisions after their own research and analysis. It is better to get the stable U in hand than to choose the stable U. If you are looking at someone else’s annualized rate of 20, you may not be able to make it. Got the principal~